CPI Outlook: Inflation Rebound Not Due to Overheated Economy, Fed Rate Hike Logic Incorrect

2026-06-09 19:38:29

On Tuesday (June 9), the US dollar index underwent a deep correction during the Asian and European sessions. Previously, the US dollar index had broken through the 100-point mark due to the explosive non-farm payroll data. Currently, the US dollar index is trading around 99.74.

In addition to the easing of geopolitical tensions weakening the dollar's appeal, two recently released microeconomic surveys have taken a breathalyzer test of the US real economy from the demand side (consumers) and the supply side (small and medium-sized enterprises), respectively.

The New York Fed's May Consumer Expectations Survey concluded that "household financial prospects continue to weaken, nominal short-term inflation has fallen (price growth minus wage growth), but expectations for essential spending have surged."

It reveals the financial anxiety of American residents caught between stagnant wage growth and high cost of living.

The core conclusion of the May NFIB Small Business Confidence Index, as reported by my colleague, is that " business confidence and certainty both declined, with a sharp drop in both hiring positions and plans, but the willingness to raise prices bucked the trend and rose." This reflects the predicament faced by the cornerstone of the US economy—small and medium-sized enterprises (SMEs)—as they are struggling to absorb costs and are forced into strategic contraction.

The New York Fed's report illustrates the substantial recession facing the household sector through three dimensions:

Nominal decline in inflation expectations and structural fragmentation: Although the median one-year inflation expectation fell slightly by 0.1 percentage point to 3.5%, the breakdown was extremely stark. Basic living needs surged across the board: expected rent increases jumped 1.4 percentage points to 7.4%, food expectations rose to 5.8%, and housing price expectations hit a new high since July 2022 (3.5%).

The "walled city" of the workplace and the harsh winter of re-employment: Residents expect the probability of facing unemployment in the next 12 months to rise to 15.1%; more importantly, the average probability of finding new employment after unemployment has fallen to 43.7%, hitting a record low since December 2025. Once ordinary people lose their jobs, the difficulty of returning to the workforce is increasing exponentially.

Household finances are teetering on the brink: Household income growth expectations for the next year are firmly capped at 2.8%, while spending growth is projected at a high 5.0%. This creates a massive purchasing power gap of 2.2%. As a result, the net percentage of households pessimistic about their financial situation has hit a new low since October 2022, with default concerns significantly intensifying among the lower and middle-income groups.

The NFIB Small Business Confidence Index, from the perspectives of production and employment, confirms that the real economy is rapidly slowing down.

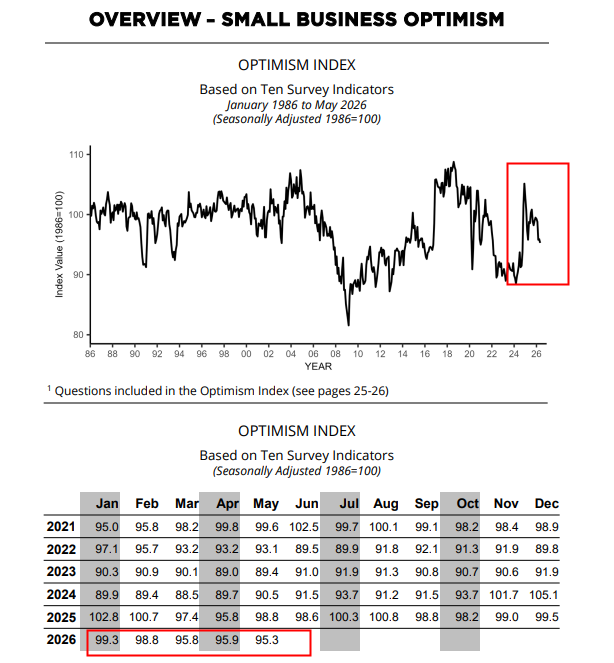

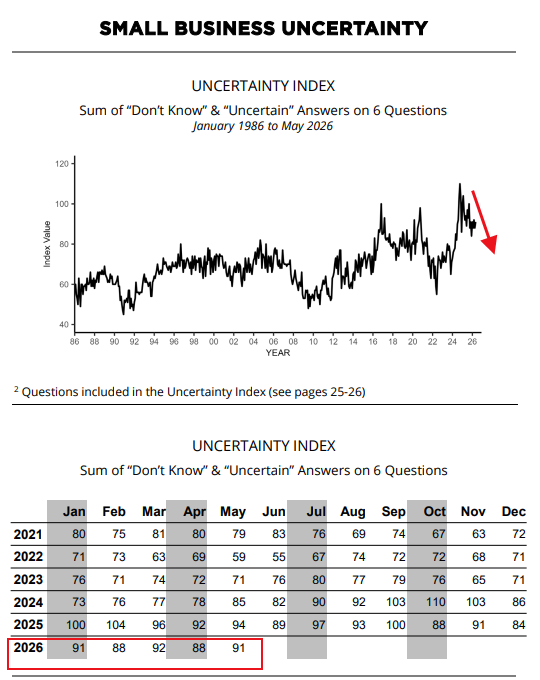

Confidence and investment both slump: The NFIB Small Business Confidence Index fell to 95.3 in May, while the Uncertainty Index surged to 91. Due to high uncertainty about the future, the proportion of businesses planning capital expenditures in the next six months dropped to 16%, a return to the low point seen during the 2009 subprime mortgage crisis.

(Small business confidence trend chart, source: NFIB Small Business Optimism Index Survey)

(Chart showing the trend of uncertainty in small businesses, source: NFIB Small Business Optimism Index Survey)

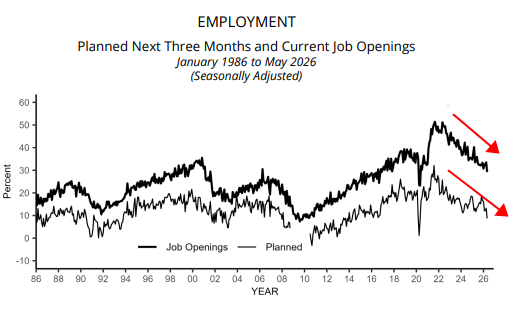

Demand for labor has plummeted: the number of job vacancies has dropped by 5 percentage points to 29%, and the net percentage of companies planning to create new jobs in the next three months has plunged to 9%, both hitting their lowest levels since May 2020 (the early stages of the pandemic). Companies have stopped expanding and have even begun to lock in headcount (hiring positions).

(Comparison chart of small business hiring and hiring plans, source: NFIB Small Business Optimism Index Survey)

Cost-driven price increases are a "poisoned chalice" approach: Under the heavy pressure of high labor and fuel costs, the net percentage of companies that actually raise prices has surged 6 percentage points to 36%, and the percentage that plans to raise prices in the future is as high as 34%.

By aligning the two reports, we can draw the following clear conclusions about the US domestic economy:

The US economy is bidding farewell to its "resilient" state and heading towards "cost-push stagflation" caused by the breakdown of micro-chains.

The consumer engine is facing a slowdown: Consumption, which accounts for two-thirds of the US economy, is suffering a slow decline as "income expectations (2.8%) fall short of spending expectations (5.0%)". As the savings of low- and middle-income groups are depleted and the debt default rate (12.6%) rises, the consumer winter is spreading from the bottom up.

The job market has shifted from "hot" to "involution": the NFIB shows that companies are hesitant to hire (demand has plummeted), and the New York Fed shows that residents are afraid to lose their jobs (re-employment rate hits a record low). The "strong employment" that served as a moat for the US economy in the past few years has completely reversed its intrinsic momentum.

A negative feedback loop is forming: residents lack money, businesses can't sell their products, increased uncertainty leads to businesses cutting capital expenditures, hiring cessation increases the risk of unemployment, and further spending cuts occur. This vicious cycle at the micro level means that the risk of a hard landing for the economy is rapidly accumulating.

These two extremely conflicting micro-surveys tonight have put tomorrow's May CPI report in the spotlight.

The market generally expects the year-on-year CPI growth rate in May to rebound to a high of 4.2% (previous value was 3.8%), driven by factors such as energy.

From a forward-looking perspective, tomorrow's CPI report will most likely show extremely strong "inflation stickiness" or even a surge beyond expectations.

The core basis for this inference lies in the "cost shifting" on the supply side: In the May NFIB report, as many as 36% of small and medium-sized enterprises have taken measures to raise prices, which forms a perfect loop with the strong bullish expectations of residents for food and rent (7.4%) in the New York Fed survey.

This means that even though demand in the real economy has begun to weaken, due to high labor and geo-fuel costs, businesses are forced to impose "defensive price increases" on consumers, making it highly likely that inflation in core services and housing (shelter) will rise rather than fall tomorrow.

If the CPI rebounds as expected tomorrow, the market will have to face the painful reality that the Federal Reserve will postpone interest rate cuts or even maintain high interest rates for longer.

However, investors must understand the underlying logic: if inflation rebounds tomorrow, it does not mean that the economy is "overheating," but rather a typical cost-push "stagflation." This means that the Federal Reserve can at most keep interest rates unchanged, and it will be difficult to raise interest rates, because raising interest rates cannot lower oil prices or boost employment.

(US Dollar Index Daily Chart, Source: FX678)

At 19:31 Beijing time, the US dollar index is currently at 99.72.

In addition to the easing of geopolitical tensions weakening the dollar's appeal, two recently released microeconomic surveys have taken a breathalyzer test of the US real economy from the demand side (consumers) and the supply side (small and medium-sized enterprises), respectively.

The New York Fed's May Consumer Expectations Survey concluded that "household financial prospects continue to weaken, nominal short-term inflation has fallen (price growth minus wage growth), but expectations for essential spending have surged."

It reveals the financial anxiety of American residents caught between stagnant wage growth and high cost of living.

The core conclusion of the May NFIB Small Business Confidence Index, as reported by my colleague, is that " business confidence and certainty both declined, with a sharp drop in both hiring positions and plans, but the willingness to raise prices bucked the trend and rose." This reflects the predicament faced by the cornerstone of the US economy—small and medium-sized enterprises (SMEs)—as they are struggling to absorb costs and are forced into strategic contraction.

New York Fed data: The "purchasing power scissors gap" in household fundamentals

The New York Fed's report illustrates the substantial recession facing the household sector through three dimensions:

Nominal decline in inflation expectations and structural fragmentation: Although the median one-year inflation expectation fell slightly by 0.1 percentage point to 3.5%, the breakdown was extremely stark. Basic living needs surged across the board: expected rent increases jumped 1.4 percentage points to 7.4%, food expectations rose to 5.8%, and housing price expectations hit a new high since July 2022 (3.5%).

The "walled city" of the workplace and the harsh winter of re-employment: Residents expect the probability of facing unemployment in the next 12 months to rise to 15.1%; more importantly, the average probability of finding new employment after unemployment has fallen to 43.7%, hitting a record low since December 2025. Once ordinary people lose their jobs, the difficulty of returning to the workforce is increasing exponentially.

Household finances are teetering on the brink: Household income growth expectations for the next year are firmly capped at 2.8%, while spending growth is projected at a high 5.0%. This creates a massive purchasing power gap of 2.2%. As a result, the net percentage of households pessimistic about their financial situation has hit a new low since October 2022, with default concerns significantly intensifying among the lower and middle-income groups.

NFIB Data: Defensive Contraction of Small and Medium-Sized Enterprises

The NFIB Small Business Confidence Index, from the perspectives of production and employment, confirms that the real economy is rapidly slowing down.

Confidence and investment both slump: The NFIB Small Business Confidence Index fell to 95.3 in May, while the Uncertainty Index surged to 91. Due to high uncertainty about the future, the proportion of businesses planning capital expenditures in the next six months dropped to 16%, a return to the low point seen during the 2009 subprime mortgage crisis.

(Small business confidence trend chart, source: NFIB Small Business Optimism Index Survey)

(Chart showing the trend of uncertainty in small businesses, source: NFIB Small Business Optimism Index Survey)

Demand for labor has plummeted: the number of job vacancies has dropped by 5 percentage points to 29%, and the net percentage of companies planning to create new jobs in the next three months has plunged to 9%, both hitting their lowest levels since May 2020 (the early stages of the pandemic). Companies have stopped expanding and have even begun to lock in headcount (hiring positions).

(Comparison chart of small business hiring and hiring plans, source: NFIB Small Business Optimism Index Survey)

Cost-driven price increases are a "poisoned chalice" approach: Under the heavy pressure of high labor and fuel costs, the net percentage of companies that actually raise prices has surged 6 percentage points to 36%, and the percentage that plans to raise prices in the future is as high as 34%.

Macroeconomic conclusion: The initial signs of stagflation, characterized by both supply and demand stagnation, have emerged.

By aligning the two reports, we can draw the following clear conclusions about the US domestic economy:

The US economy is bidding farewell to its "resilient" state and heading towards "cost-push stagflation" caused by the breakdown of micro-chains.

The consumer engine is facing a slowdown: Consumption, which accounts for two-thirds of the US economy, is suffering a slow decline as "income expectations (2.8%) fall short of spending expectations (5.0%)". As the savings of low- and middle-income groups are depleted and the debt default rate (12.6%) rises, the consumer winter is spreading from the bottom up.

The job market has shifted from "hot" to "involution": the NFIB shows that companies are hesitant to hire (demand has plummeted), and the New York Fed shows that residents are afraid to lose their jobs (re-employment rate hits a record low). The "strong employment" that served as a moat for the US economy in the past few years has completely reversed its intrinsic momentum.

A negative feedback loop is forming: residents lack money, businesses can't sell their products, increased uncertainty leads to businesses cutting capital expenditures, hiring cessation increases the risk of unemployment, and further spending cuts occur. This vicious cycle at the micro level means that the risk of a hard landing for the economy is rapidly accumulating.

US CPI forecast for tomorrow: Interest rate hike unlikely.

These two extremely conflicting micro-surveys tonight have put tomorrow's May CPI report in the spotlight.

The market generally expects the year-on-year CPI growth rate in May to rebound to a high of 4.2% (previous value was 3.8%), driven by factors such as energy.

From a forward-looking perspective, tomorrow's CPI report will most likely show extremely strong "inflation stickiness" or even a surge beyond expectations.

The core basis for this inference lies in the "cost shifting" on the supply side: In the May NFIB report, as many as 36% of small and medium-sized enterprises have taken measures to raise prices, which forms a perfect loop with the strong bullish expectations of residents for food and rent (7.4%) in the New York Fed survey.

This means that even though demand in the real economy has begun to weaken, due to high labor and geo-fuel costs, businesses are forced to impose "defensive price increases" on consumers, making it highly likely that inflation in core services and housing (shelter) will rise rather than fall tomorrow.

If the CPI rebounds as expected tomorrow, the market will have to face the painful reality that the Federal Reserve will postpone interest rate cuts or even maintain high interest rates for longer.

However, investors must understand the underlying logic: if inflation rebounds tomorrow, it does not mean that the economy is "overheating," but rather a typical cost-push "stagflation." This means that the Federal Reserve can at most keep interest rates unchanged, and it will be difficult to raise interest rates, because raising interest rates cannot lower oil prices or boost employment.

(US Dollar Index Daily Chart, Source: FX678)

At 19:31 Beijing time, the US dollar index is currently at 99.72.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.