One chart: The Baltic Dry Index weakened significantly, putting pressure on freight rates across all major vessel types.

2026-06-09 22:30:36

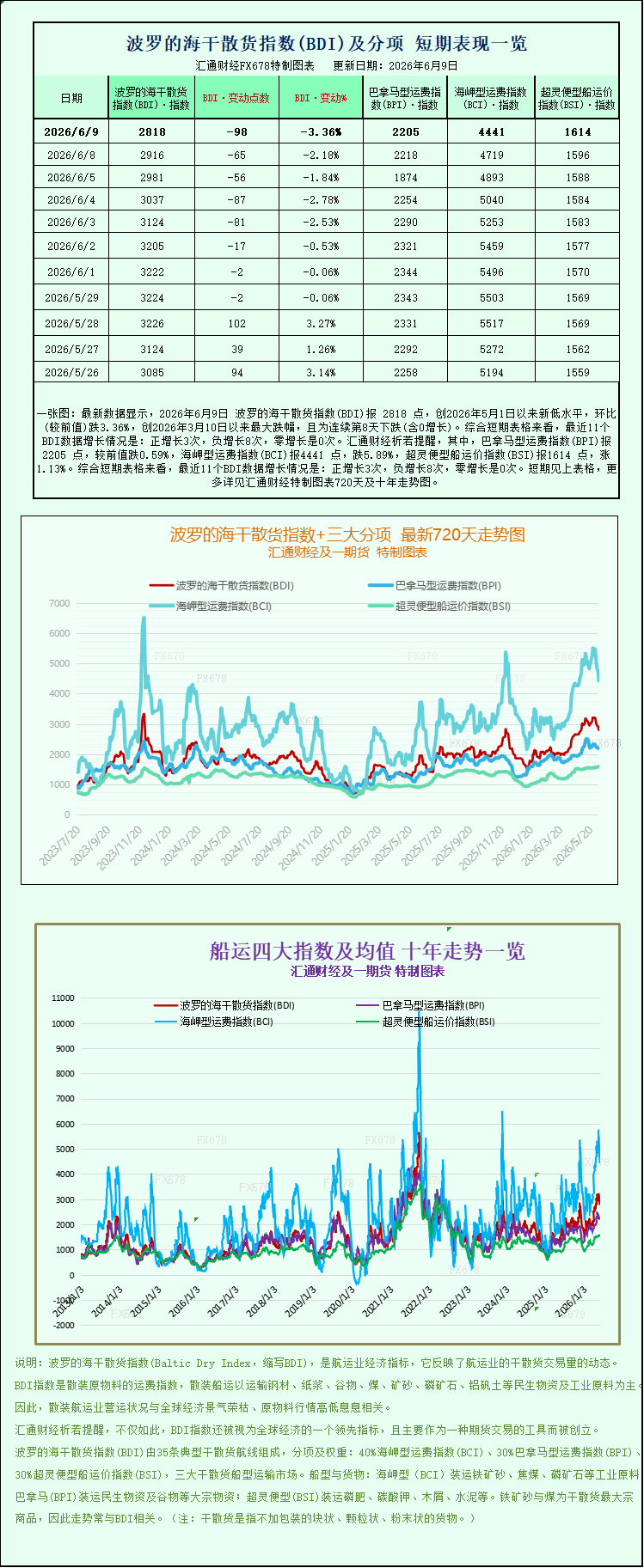

Latest data shows that the Baltic Dry Index (BDI) closed at 2818 points on June 9, 2026, a new low since May 1, 2026, down 3.36% month-on-month, the largest drop since March 10, 2026, and marking the eighth consecutive day of decline (including zero growth). Looking at the short-term charts, the recent 11 BDI data points show: 3 positive increases, 8 negative increases, and 0 zero increases. Specifically, the Panamax Freight Index (BPI) closed at 2205 points, down 0.59% from the previous value; the Capesize Freight Index (BCI) closed at 4441 points, down 5.89%; and the Supramax Freight Index (BSI) closed at 1614 points, up 1.13%. For detailed 720-day and 10-year trend charts of the Baltic Dry Index and its three main sub-indices, please refer to the specially designed charts.

The Baltic Dry Index (BDI), a bellwether for the international shipping market, has once again seen a significant decline, highlighting the overall weakening trend. This drop was primarily driven by a simultaneous decline in freight rates for the two main bulk carrier types, Capesize and Panamax. Only Supramax freight rates bucked the trend with a slight increase, demonstrating a clear market divergence. Considering the upstream and downstream supply chains, this round of freight rate declines is deeply intertwined with global commodity demand, domestic industrial production rhythms, and fluctuations in energy and ferrous metal prices, further solidifying the short-term pressure on the dry bulk shipping market.

Data shows that the Baltic Dry Index (BDI), which comprehensively reflects freight rates for dry bulk carriers of different tonnages, plummeted 98 points, a drop of 3.4%, closing at 2818 points, continuing its overall downward trend. As a core benchmark for global dry bulk shipping, the BDI directly reflects the supply and demand relationship in international commodity shipping. This significant reduction indicates that global dry bulk shipping demand is currently weak, and there is an imbalance between shipping capacity supply and freight demand in the shipping market.

Among the various vessel sub-categories, Capesize vessels were the biggest drag on the index decline, experiencing the most significant drop. The sub-index representing Capesize freight rates fell by 278 points in a single day, a drop of 5.9%, ultimately closing at 4441 points. This vessel type is a major force in ocean-going dry bulk shipping, with a typical deadweight capacity of 150,000 tons per ship. It primarily handles the transoceanic transport of heavy raw materials such as iron ore, thermal coal, and bulk mineral products. Its freight rate fluctuations are directly linked to the prosperity of the global steel, thermal power, and other heavy industrial supply chains. In terms of actual operating revenue, the average daily revenue of Capesize vessels shrank significantly by $2,524 to $36,771, resulting in a marked narrowing of profit margins.

Industry analysts point out that the sharp drop in Capesize freight rates is primarily driven by weakening demand for ferrous metal commodities in China. Recently, the domestic steel industry has entered its traditional off-season, resulting in insufficient downstream steel demand, which has directly impacted the upstream iron ore market. As of Tuesday, iron ore futures prices had fallen for five consecutive trading days, indicating a continued cooling of market enthusiasm for iron ore procurement and ocean shipping. Simultaneously, the domestic coal market has also seen a significant easing in prices. Previously, the industry conducted large-scale production shutdowns for safety inspections. With these inspections completed, many coal mines have gradually resumed normal production, significantly increasing market coal supply and causing a sharp drop in coking coal and coke prices. As iron ore and coal are the most important cargoes transported by Capesize vessels, the simultaneous weakening of demand and prices for both commodities has directly led to a decrease in ocean charter orders. Shipowners have been forced to lower freight rates to attract cargo, resulting in a rapid decline in the Capesize market.

Panamax vessels, following closely behind, also failed to escape the downward trend in freight rates, although the decline was relatively mild. The Panamax freight rate index fell 13 points, a decrease of 0.6%, closing at 2205 points. This vessel type, with a deadweight tonnage between 60,000 and 70,000 tons, is suitable for a wide range of routes and is a mainstay in the global transport of bulk cargo such as grains, small-to-medium-sized coal, and fertilizers. Its routes cover many major waterways in the Atlantic and Pacific Oceans, accommodating both industrial raw materials and agricultural products, thus broadening its market reach. On that day, the average daily operating revenue of Panamax vessels decreased by $120 to $19,846. Although the decline in revenue per vessel was far less than that of large Capesize vessels, it still reflects the overall weakness in freight demand. On the one hand, demand for industrial coal transportation decreased as the energy market cooled; on the other hand, global grain trade entered a period of relative stability, limiting the short-term increase in long-distance grain shipping. These multiple factors combined led to a simultaneous decline in Panamax freight rates.

Amidst a general market downturn, small Supramax vessels emerged as the only sector to buck the trend, demonstrating independent performance. The Supramax freight rate index rose 18 points, or 1.1%, to close at 1614 points. These vessels, with their smaller tonnage and higher operational flexibility, can call at small and medium-sized ports. Besides handling conventional bulk cargo, they also undertake short-haul and feeder transport of small-volume general cargo, regional building materials, and minor agricultural products. Their freight rate increase was primarily driven by stable short-haul freight demand within the region, coupled with relatively controllable overall capacity deployment for this vessel type, resulting in a healthy supply-demand relationship. This led to a slight rebound against the backdrop of a sharp decline in mainstream large vessel freight rates, creating a differentiated pattern in the dry bulk shipping market: "large vessels are cold, small vessels are stable."

Judging from the current market environment, the Baltic Dry Index is likely to remain weak and volatile in the short term. The seasonal weakness in the domestic steel industry has not yet reversed, and demand for core commodities such as iron ore and coal is unlikely to rebound rapidly. Freight rates for the two main vessel types, Capesize and Panamax, remain under pressure. Meanwhile, the slow pace of global economic recovery and insufficient growth in international commodity trade also constrain long-distance dry bulk shipping.

For shipping companies, the operating profits of large bulk carriers are being continuously squeezed, and operational pressure is gradually increasing; while smaller and medium-sized vessels, with their greater flexibility and advantages in feeder shipping, have stronger risk resistance. Future market trends will closely monitor the progress of domestic infrastructure and manufacturing resumption of work and production, as well as changes in the prices and trade flows of bulk commodities such as iron ore, coal, and grain. These factors will be key variables influencing the direction of dry bulk shipping freight rates.

The Baltic Dry Index (BDI), a bellwether for the international shipping market, has once again seen a significant decline, highlighting the overall weakening trend. This drop was primarily driven by a simultaneous decline in freight rates for the two main bulk carrier types, Capesize and Panamax. Only Supramax freight rates bucked the trend with a slight increase, demonstrating a clear market divergence. Considering the upstream and downstream supply chains, this round of freight rate declines is deeply intertwined with global commodity demand, domestic industrial production rhythms, and fluctuations in energy and ferrous metal prices, further solidifying the short-term pressure on the dry bulk shipping market.

Data shows that the Baltic Dry Index (BDI), which comprehensively reflects freight rates for dry bulk carriers of different tonnages, plummeted 98 points, a drop of 3.4%, closing at 2818 points, continuing its overall downward trend. As a core benchmark for global dry bulk shipping, the BDI directly reflects the supply and demand relationship in international commodity shipping. This significant reduction indicates that global dry bulk shipping demand is currently weak, and there is an imbalance between shipping capacity supply and freight demand in the shipping market.

Among the various vessel sub-categories, Capesize vessels were the biggest drag on the index decline, experiencing the most significant drop. The sub-index representing Capesize freight rates fell by 278 points in a single day, a drop of 5.9%, ultimately closing at 4441 points. This vessel type is a major force in ocean-going dry bulk shipping, with a typical deadweight capacity of 150,000 tons per ship. It primarily handles the transoceanic transport of heavy raw materials such as iron ore, thermal coal, and bulk mineral products. Its freight rate fluctuations are directly linked to the prosperity of the global steel, thermal power, and other heavy industrial supply chains. In terms of actual operating revenue, the average daily revenue of Capesize vessels shrank significantly by $2,524 to $36,771, resulting in a marked narrowing of profit margins.

Industry analysts point out that the sharp drop in Capesize freight rates is primarily driven by weakening demand for ferrous metal commodities in China. Recently, the domestic steel industry has entered its traditional off-season, resulting in insufficient downstream steel demand, which has directly impacted the upstream iron ore market. As of Tuesday, iron ore futures prices had fallen for five consecutive trading days, indicating a continued cooling of market enthusiasm for iron ore procurement and ocean shipping. Simultaneously, the domestic coal market has also seen a significant easing in prices. Previously, the industry conducted large-scale production shutdowns for safety inspections. With these inspections completed, many coal mines have gradually resumed normal production, significantly increasing market coal supply and causing a sharp drop in coking coal and coke prices. As iron ore and coal are the most important cargoes transported by Capesize vessels, the simultaneous weakening of demand and prices for both commodities has directly led to a decrease in ocean charter orders. Shipowners have been forced to lower freight rates to attract cargo, resulting in a rapid decline in the Capesize market.

Panamax vessels, following closely behind, also failed to escape the downward trend in freight rates, although the decline was relatively mild. The Panamax freight rate index fell 13 points, a decrease of 0.6%, closing at 2205 points. This vessel type, with a deadweight tonnage between 60,000 and 70,000 tons, is suitable for a wide range of routes and is a mainstay in the global transport of bulk cargo such as grains, small-to-medium-sized coal, and fertilizers. Its routes cover many major waterways in the Atlantic and Pacific Oceans, accommodating both industrial raw materials and agricultural products, thus broadening its market reach. On that day, the average daily operating revenue of Panamax vessels decreased by $120 to $19,846. Although the decline in revenue per vessel was far less than that of large Capesize vessels, it still reflects the overall weakness in freight demand. On the one hand, demand for industrial coal transportation decreased as the energy market cooled; on the other hand, global grain trade entered a period of relative stability, limiting the short-term increase in long-distance grain shipping. These multiple factors combined led to a simultaneous decline in Panamax freight rates.

Amidst a general market downturn, small Supramax vessels emerged as the only sector to buck the trend, demonstrating independent performance. The Supramax freight rate index rose 18 points, or 1.1%, to close at 1614 points. These vessels, with their smaller tonnage and higher operational flexibility, can call at small and medium-sized ports. Besides handling conventional bulk cargo, they also undertake short-haul and feeder transport of small-volume general cargo, regional building materials, and minor agricultural products. Their freight rate increase was primarily driven by stable short-haul freight demand within the region, coupled with relatively controllable overall capacity deployment for this vessel type, resulting in a healthy supply-demand relationship. This led to a slight rebound against the backdrop of a sharp decline in mainstream large vessel freight rates, creating a differentiated pattern in the dry bulk shipping market: "large vessels are cold, small vessels are stable."

Judging from the current market environment, the Baltic Dry Index is likely to remain weak and volatile in the short term. The seasonal weakness in the domestic steel industry has not yet reversed, and demand for core commodities such as iron ore and coal is unlikely to rebound rapidly. Freight rates for the two main vessel types, Capesize and Panamax, remain under pressure. Meanwhile, the slow pace of global economic recovery and insufficient growth in international commodity trade also constrain long-distance dry bulk shipping.

For shipping companies, the operating profits of large bulk carriers are being continuously squeezed, and operational pressure is gradually increasing; while smaller and medium-sized vessels, with their greater flexibility and advantages in feeder shipping, have stronger risk resistance. Future market trends will closely monitor the progress of domestic infrastructure and manufacturing resumption of work and production, as well as changes in the prices and trade flows of bulk commodities such as iron ore, coal, and grain. These factors will be key variables influencing the direction of dry bulk shipping freight rates.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.