A chart shows that the Baltic Dry Index is weakening, putting continued pressure on freight rates for the two main vessel types.

2026-06-08 23:25:44

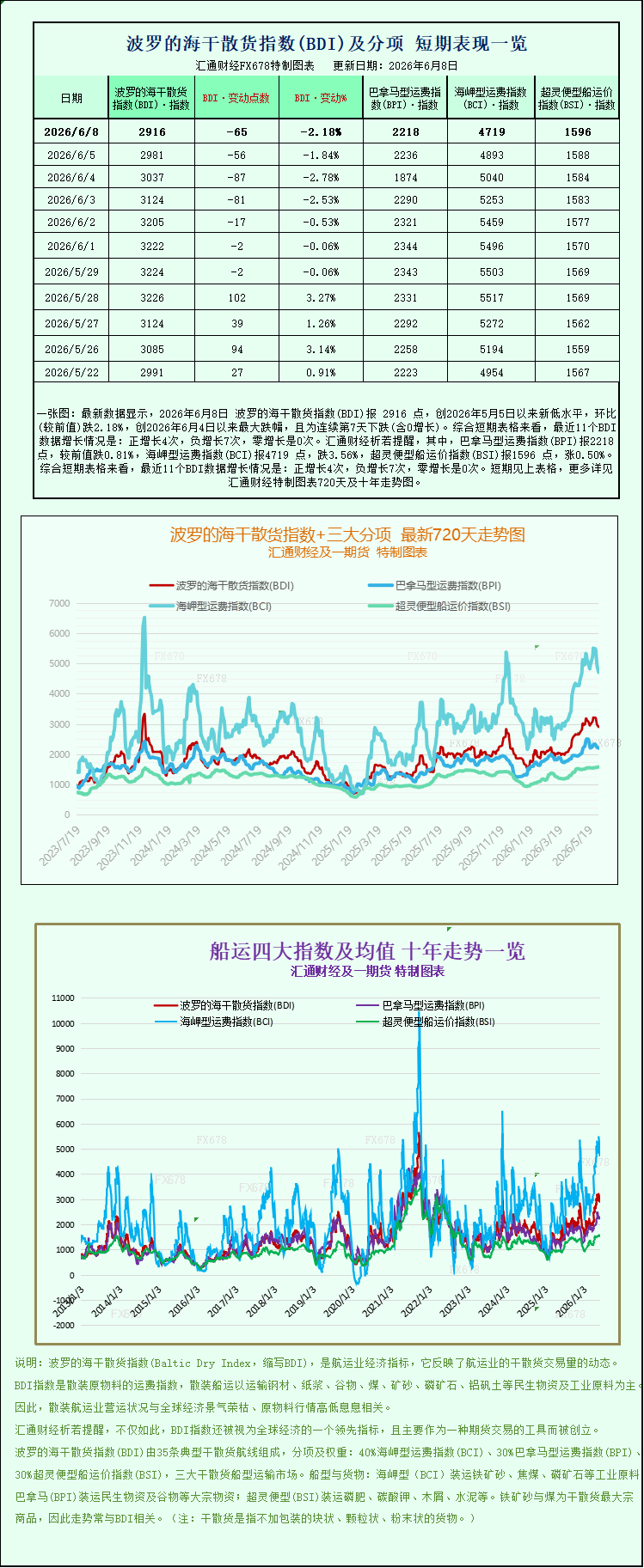

Latest data shows that the Baltic Dry Index (BDI) closed at 2916 points on June 8, 2026, a new low since May 5, 2026, down 2.18% month-on-month, the largest drop since June 4, 2026, and marking the seventh consecutive day of decline (including zero growth). Looking at the short-term charts, the BDI has seen positive growth 4 times, negative growth 7 times, and zero growth in the last 11 data points. Specifically, the Panamax Freight Index (BPI) closed at 2218 points, down 0.81% from the previous value; the Capesize Freight Index (BCI) closed at 4719 points, down 3.56%; and the Supramax Freight Index (BSI) closed at 1596 points, up 0.50%. For detailed 720-day and 10-year trend charts of the Baltic Dry Index and its three main sub-indices, please refer to the specially designed charts.

The Baltic Dry Index (BDI), a bellwether for the international shipping market, has seen a significant decline, indicating an overall weakening trend. This drop is primarily driven by a simultaneous decline in freight rates for the two main dry bulk vessel types: Capesize and Panamax. This is compounded by multiple factors, including changes in supply and demand in the commodity market and weak downstream demand. As a result, the dry bulk shipping market is under short-term pressure, with different vessel sizes showing divergent price trends.

As a core benchmark for the global dry bulk shipping industry, the Baltic Dry Index (BDI) comprehensively tracks freight rates for three major dry bulk carrier types: Capesize, Panamax, and Supramax. It directly reflects the global demand for seaborne commodities such as minerals, grains, and energy raw materials, as well as the overall health of the shipping market. On that day, the index fell 65 points, a drop of 2.2%, closing at 2916 points, ending its previously relatively stable trend and signaling a weakening of global dry bulk shipping demand.

Among the various ship types, Capesize vessels, the largest in size and primarily responsible for long-distance bulk mineral transportation, became the core factor dragging down the overall market. The Capesize shipping index fell sharply by 174 points, a drop of 3.6%, closing at 4719 points, the most significant decline among the three ship types. These vessels generally have a deadweight tonnage of around 150,000 tons and are the mainstay of transoceanic transportation of basic industrial raw materials such as iron ore and thermal coal. Their revenue changes are deeply tied to the operation of real industries such as steel and thermal power. Data shows that the average daily earnings of Capesize vessels decreased by $1,576 to $39,295 that day, resulting in a significant reduction in shipowners' operating profits.

The sharp decline in Capesize freight rates is inextricably linked to the continued weakness in the upstream iron ore market. International iron ore futures prices fell for the fourth consecutive trading day on Monday, with market pessimism continuing to spread. Currently, iron ore inventories at major ports are at high levels, ensuring ample supply, while the downstream steel industry is experiencing poor operating conditions, continuously squeezing steel mill profit margins. To control production costs and mitigate operational risks, most domestic and overseas steel mills have proactively slowed down their raw material procurement pace and reduced iron ore imports, directly leading to a sharp decrease in ocean-going iron ore shipping orders. The continued weakness on the demand side has created an imbalance between supply and demand in the Capesize vessel market, which primarily transports minerals, causing freight rates and shipowners' daily earnings to decline in tandem. At the same time, the number of new Capesize vessel orders and short-term charter orders has also decreased significantly, with shipping companies and shippers adopting a wait-and-see attitude, further exacerbating the downward pressure on this sector.

Panamax vessels, a mainstay of the dry bulk market, also faced a challenging market. The Panamax index fell 18 points to 2218 points that day; the average daily revenue per vessel decreased by $155, ultimately recording $19,966. This vessel type, with a deadweight range of 60,000 to 70,000 tons, primarily handles short-to-medium-haul, inter-regional shipping of essential goods and energy products such as coal, grain, and fertilizer. Its routes cover numerous global trade routes, making it widely applicable. The decline in Panamax freight rates is due to both the overall dry bulk market environment and a temporary cooling of global demand for grain and coal. Currently, some major grain-producing regions are entering their traditional off-season, leading to a decrease in international cross-regional grain transport orders. Coupled with adjustments in energy supply structures in many regions, the growth in coal seaborne demand is weak. These multiple factors combined have resulted in a cooling of Panamax chartering activity, causing freight rates to fall accordingly.

In stark contrast to the decline in freight rates for the two main vessel types, the market for small dry bulk carriers bucked the trend with a slight increase. The index representing Supramax vessels rose 8 points to close at 1596. These smaller vessels are highly maneuverable and have shallow drafts, allowing them to call at more small and medium-sized ports. They primarily handle short-haul, small-volume freight orders and are relatively less affected by fluctuations in the international long-distance bulk commodity transportation market. Stable demand for short-haul goods transportation within the region supported the slight increase in freight rates for small vessels, preventing a broad-based decline in the overall dry bulk market. The divergence in market conditions between different tonnage vessels became increasingly apparent.

In summary, the recent decline in the Baltic Dry Index is the result of a multi-faceted impact from the shipping market, the commodity market, and downstream industries. In the short term, the high iron ore inventory and weak steel mill profitability are unlikely to reverse quickly, and there is a lack of strong upward momentum in seaborne demand for grain and coal. Therefore, freight rate pressure on Capesize and Panamax vessels will continue. However, Supramax vessels, relying on the resilience of short-haul regional trade, have shown relatively stable performance.

The future market trend will depend on two factors. First, it's crucial to monitor whether iron ore prices can stabilize and rebound, and the progress of steel industry resumption of production, which will directly determine the demand for large mining vessels. Second, it's essential to closely monitor changes in global food production and sales, energy trade policies, and new international shipping orders and capacity deployment. Given these multiple variables, the Baltic Dry Index is likely to maintain a volatile trend, and the divergence in market performance among different ship types may continue for some time. For shipping companies, traders, and other industry players, caution is still necessary in the current market environment. Close monitoring of supply and demand changes is essential, along with careful planning of capacity and procurement schedules.

The Baltic Dry Index (BDI), a bellwether for the international shipping market, has seen a significant decline, indicating an overall weakening trend. This drop is primarily driven by a simultaneous decline in freight rates for the two main dry bulk vessel types: Capesize and Panamax. This is compounded by multiple factors, including changes in supply and demand in the commodity market and weak downstream demand. As a result, the dry bulk shipping market is under short-term pressure, with different vessel sizes showing divergent price trends.

As a core benchmark for the global dry bulk shipping industry, the Baltic Dry Index (BDI) comprehensively tracks freight rates for three major dry bulk carrier types: Capesize, Panamax, and Supramax. It directly reflects the global demand for seaborne commodities such as minerals, grains, and energy raw materials, as well as the overall health of the shipping market. On that day, the index fell 65 points, a drop of 2.2%, closing at 2916 points, ending its previously relatively stable trend and signaling a weakening of global dry bulk shipping demand.

Among the various ship types, Capesize vessels, the largest in size and primarily responsible for long-distance bulk mineral transportation, became the core factor dragging down the overall market. The Capesize shipping index fell sharply by 174 points, a drop of 3.6%, closing at 4719 points, the most significant decline among the three ship types. These vessels generally have a deadweight tonnage of around 150,000 tons and are the mainstay of transoceanic transportation of basic industrial raw materials such as iron ore and thermal coal. Their revenue changes are deeply tied to the operation of real industries such as steel and thermal power. Data shows that the average daily earnings of Capesize vessels decreased by $1,576 to $39,295 that day, resulting in a significant reduction in shipowners' operating profits.

The sharp decline in Capesize freight rates is inextricably linked to the continued weakness in the upstream iron ore market. International iron ore futures prices fell for the fourth consecutive trading day on Monday, with market pessimism continuing to spread. Currently, iron ore inventories at major ports are at high levels, ensuring ample supply, while the downstream steel industry is experiencing poor operating conditions, continuously squeezing steel mill profit margins. To control production costs and mitigate operational risks, most domestic and overseas steel mills have proactively slowed down their raw material procurement pace and reduced iron ore imports, directly leading to a sharp decrease in ocean-going iron ore shipping orders. The continued weakness on the demand side has created an imbalance between supply and demand in the Capesize vessel market, which primarily transports minerals, causing freight rates and shipowners' daily earnings to decline in tandem. At the same time, the number of new Capesize vessel orders and short-term charter orders has also decreased significantly, with shipping companies and shippers adopting a wait-and-see attitude, further exacerbating the downward pressure on this sector.

Panamax vessels, a mainstay of the dry bulk market, also faced a challenging market. The Panamax index fell 18 points to 2218 points that day; the average daily revenue per vessel decreased by $155, ultimately recording $19,966. This vessel type, with a deadweight range of 60,000 to 70,000 tons, primarily handles short-to-medium-haul, inter-regional shipping of essential goods and energy products such as coal, grain, and fertilizer. Its routes cover numerous global trade routes, making it widely applicable. The decline in Panamax freight rates is due to both the overall dry bulk market environment and a temporary cooling of global demand for grain and coal. Currently, some major grain-producing regions are entering their traditional off-season, leading to a decrease in international cross-regional grain transport orders. Coupled with adjustments in energy supply structures in many regions, the growth in coal seaborne demand is weak. These multiple factors combined have resulted in a cooling of Panamax chartering activity, causing freight rates to fall accordingly.

In stark contrast to the decline in freight rates for the two main vessel types, the market for small dry bulk carriers bucked the trend with a slight increase. The index representing Supramax vessels rose 8 points to close at 1596. These smaller vessels are highly maneuverable and have shallow drafts, allowing them to call at more small and medium-sized ports. They primarily handle short-haul, small-volume freight orders and are relatively less affected by fluctuations in the international long-distance bulk commodity transportation market. Stable demand for short-haul goods transportation within the region supported the slight increase in freight rates for small vessels, preventing a broad-based decline in the overall dry bulk market. The divergence in market conditions between different tonnage vessels became increasingly apparent.

In summary, the recent decline in the Baltic Dry Index is the result of a multi-faceted impact from the shipping market, the commodity market, and downstream industries. In the short term, the high iron ore inventory and weak steel mill profitability are unlikely to reverse quickly, and there is a lack of strong upward momentum in seaborne demand for grain and coal. Therefore, freight rate pressure on Capesize and Panamax vessels will continue. However, Supramax vessels, relying on the resilience of short-haul regional trade, have shown relatively stable performance.

The future market trend will depend on two factors. First, it's crucial to monitor whether iron ore prices can stabilize and rebound, and the progress of steel industry resumption of production, which will directly determine the demand for large mining vessels. Second, it's essential to closely monitor changes in global food production and sales, energy trade policies, and new international shipping orders and capacity deployment. Given these multiple variables, the Baltic Dry Index is likely to maintain a volatile trend, and the divergence in market performance among different ship types may continue for some time. For shipping companies, traders, and other industry players, caution is still necessary in the current market environment. Close monitoring of supply and demand changes is essential, along with careful planning of capacity and procurement schedules.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.