Institutions: Gold is not a speculative asset, but a cornerstone of long-term value storage.

2026-04-24 10:47:38

In the global asset allocation arena, gold has always held a unique position, standing in stark contrast to conventional investment options such as stocks and bonds. Most investors struggle to understand gold's asset attributes, believing it lacks real return support and has an unclear valuation system. However, Jeff Sarti, a renowned wealth manager, offers a disruptive perspective, redefining gold's core positioning and providing an in-depth analysis of its long-term allocation value and future development trends, drawing on long-term market experience and the macroeconomic landscape.

For most investors, gold has always been a unique outlier in the asset market. This type of asset cannot generate operating cash flow, does not pay dividends to its holders, and cannot be reasonably priced using traditional financial valuation models. In conventional investment logic, gold is often regarded as a niche asset lacking growth potential.

Jeff Sarti, CEO of Morton Wealth, believes that gold's inherent weaknesses are precisely its core strength in maintaining a long-term market position. He states that gold is not a traditional investment product, but rather a high-quality savings asset. Over a long period, gold's most fundamental function is to stably store wealth value.

Since 2015, Salty's institution has consistently invested in gold assets, maintaining a stable holding pace. At the beginning of the year, gold prices experienced a rapid surge, igniting market speculation. However, in his view, this short-term irrational rise harbors hidden risks. He stated that even as the long-term investment logic for gold continues to strengthen, there remains a widespread misunderstanding of gold's fundamental function within the market.

From a historical perspective, Salty defines gold as the ultimate store of value. Throughout the history of human economic development, various fiat currency systems have constantly changed, rising and falling, but only gold has transcended the changes of time and continued to play its role as an anchor of value.

The global reserve currency landscape is constantly evolving, with new and old currencies frequently replacing each other. Gold, however, has withstood the test of several economic cycles, and its value stability has never been broken. Many fund managers actively avoid gold because they consider it a non-yielding asset and difficult to value. Salty, however, believes such concerns are overly simplistic and complicated. He adds that gold's most crucial practical role is to hedge against the risk of asset devaluation caused by global debt expansion and continued currency depreciation.

In his view, a qualified value-saving asset should maintain a stable price trend. A healthy market is one where gold maintains a reasonable and stable price range ; an extreme surge in gold prices would indicate serious problems in the global economic system.

Based on its deep understanding of gold, Salty has developed a sound and long-term asset allocation plan. Over the past decade, its institutions have consistently maintained a reasonable proportion of precious metal holdings, generally at a high single-digit level. Gold accounts for approximately 5% to 6% of the portfolio, while mining stocks account for a supplementary allocation of 2% to 3%, thus perfecting its precious metal asset portfolio.

The institution abandoned short-term market timing and speculation, strictly adhering to a standardized asset rebalancing mechanism. When gold prices hit a record high in January, the institution took reasonable profits, realizing some gains. Meanwhile, due to the greater volatility of mining stocks and their susceptibility to production costs such as energy, they were only used as a tactical supplement to gold holdings to balance overall portfolio risk.

Setting aside short-term price fluctuations, Salty remains bullish on gold in the long term, primarily due to the underlying structural economic risks globally . He states bluntly that, based on various economic accounting indicators, the fiscal situations of many countries have long been unbalanced, relying on increased money supply to maintain operations.

In the future, policymakers in various countries will likely continue their currency devaluation strategies, coupled with financial regulation to stabilize markets. Yield curve manipulation may also become a common tool. Not just individual economies, but many countries globally face the problem of runaway debt, compounded by complex economic uncertainties, making it nearly impossible to resolve debt crises through economic growth alone. Once inflation stimulus policies are fully implemented, it will become a key turning point for economic development, at which point the market will need to further increase its allocation to gold.

Currently, the overall allocation to gold in the global investment market is severely undervalued, with institutional investors exhibiting particularly pronounced underweighting . The average gold holding in global investment portfolios is less than 0.2%. This insufficient market participation indicates that the current gold price rally is still in its early stages, driven by macroeconomic fundamentals and has not yet formed a widespread speculative bubble.

Jeff Salty believes that the real signal of a gold price peak is not a change in technical patterns, but rather the widespread public awareness of its value. Only when gold truly enters the mainstream public consciousness and becomes a widely discussed asset should we be wary of market risks.

Overall , gold is just one important component of a diversified asset allocation strategy. Combined with physical assets and low-correlation investments, it can effectively mitigate market risks. In an environment of high debt, persistent inflation, and rising stagflation risks, the advantages of physical assets will continue to be prominent.

In the future, gold will gradually shed its label as a short-term speculative asset and become a core underlying asset for safeguarding the stability of investment portfolios, continuing to play an irreplaceable role in protecting value in a complex and ever-changing macroeconomic environment.

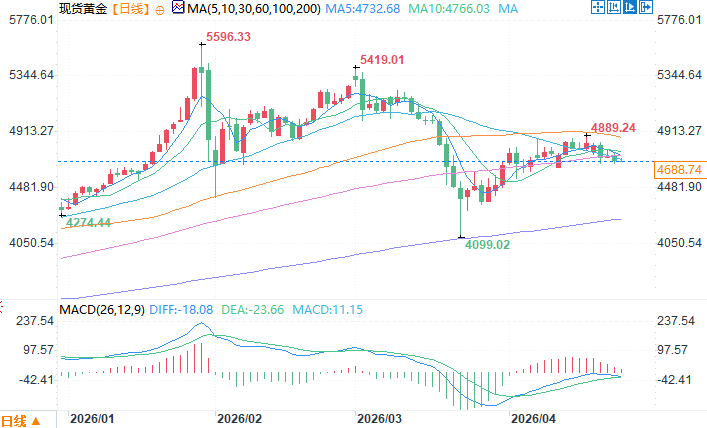

Spot gold daily chart source: EasyForex

At 10:47 AM Beijing time on April 24, spot gold was trading at $4680.54 per ounce.

I. Gold's core positioning: value storage rather than an investment target.

For most investors, gold has always been a unique outlier in the asset market. This type of asset cannot generate operating cash flow, does not pay dividends to its holders, and cannot be reasonably priced using traditional financial valuation models. In conventional investment logic, gold is often regarded as a niche asset lacking growth potential.

Jeff Sarti, CEO of Morton Wealth, believes that gold's inherent weaknesses are precisely its core strength in maintaining a long-term market position. He states that gold is not a traditional investment product, but rather a high-quality savings asset. Over a long period, gold's most fundamental function is to stably store wealth value.

Since 2015, Salty's institution has consistently invested in gold assets, maintaining a stable holding pace. At the beginning of the year, gold prices experienced a rapid surge, igniting market speculation. However, in his view, this short-term irrational rise harbors hidden risks. He stated that even as the long-term investment logic for gold continues to strengthen, there remains a widespread misunderstanding of gold's fundamental function within the market.

II. Gold's Underlying Advantages: A Hard Currency with Value That Transcends Cycles

From a historical perspective, Salty defines gold as the ultimate store of value. Throughout the history of human economic development, various fiat currency systems have constantly changed, rising and falling, but only gold has transcended the changes of time and continued to play its role as an anchor of value.

The global reserve currency landscape is constantly evolving, with new and old currencies frequently replacing each other. Gold, however, has withstood the test of several economic cycles, and its value stability has never been broken. Many fund managers actively avoid gold because they consider it a non-yielding asset and difficult to value. Salty, however, believes such concerns are overly simplistic and complicated. He adds that gold's most crucial practical role is to hedge against the risk of asset devaluation caused by global debt expansion and continued currency depreciation.

In his view, a qualified value-saving asset should maintain a stable price trend. A healthy market is one where gold maintains a reasonable and stable price range ; an extreme surge in gold prices would indicate serious problems in the global economic system.

III. Institutional Allocation Strategy: Rational Layout and Balanced Asset Management

Based on its deep understanding of gold, Salty has developed a sound and long-term asset allocation plan. Over the past decade, its institutions have consistently maintained a reasonable proportion of precious metal holdings, generally at a high single-digit level. Gold accounts for approximately 5% to 6% of the portfolio, while mining stocks account for a supplementary allocation of 2% to 3%, thus perfecting its precious metal asset portfolio.

The institution abandoned short-term market timing and speculation, strictly adhering to a standardized asset rebalancing mechanism. When gold prices hit a record high in January, the institution took reasonable profits, realizing some gains. Meanwhile, due to the greater volatility of mining stocks and their susceptibility to production costs such as energy, they were only used as a tactical supplement to gold holdings to balance overall portfolio risk.

IV. Macroeconomic Background Support: Economic Risks Solidify the Foundation for Gold's Upward Movement

Setting aside short-term price fluctuations, Salty remains bullish on gold in the long term, primarily due to the underlying structural economic risks globally . He states bluntly that, based on various economic accounting indicators, the fiscal situations of many countries have long been unbalanced, relying on increased money supply to maintain operations.

In the future, policymakers in various countries will likely continue their currency devaluation strategies, coupled with financial regulation to stabilize markets. Yield curve manipulation may also become a common tool. Not just individual economies, but many countries globally face the problem of runaway debt, compounded by complex economic uncertainties, making it nearly impossible to resolve debt crises through economic growth alone. Once inflation stimulus policies are fully implemented, it will become a key turning point for economic development, at which point the market will need to further increase its allocation to gold.

V. Market Status and Future Outlook

Currently, the overall allocation to gold in the global investment market is severely undervalued, with institutional investors exhibiting particularly pronounced underweighting . The average gold holding in global investment portfolios is less than 0.2%. This insufficient market participation indicates that the current gold price rally is still in its early stages, driven by macroeconomic fundamentals and has not yet formed a widespread speculative bubble.

Jeff Salty believes that the real signal of a gold price peak is not a change in technical patterns, but rather the widespread public awareness of its value. Only when gold truly enters the mainstream public consciousness and becomes a widely discussed asset should we be wary of market risks.

Overall , gold is just one important component of a diversified asset allocation strategy. Combined with physical assets and low-correlation investments, it can effectively mitigate market risks. In an environment of high debt, persistent inflation, and rising stagflation risks, the advantages of physical assets will continue to be prominent.

In the future, gold will gradually shed its label as a short-term speculative asset and become a core underlying asset for safeguarding the stability of investment portfolios, continuing to play an irreplaceable role in protecting value in a complex and ever-changing macroeconomic environment.

Spot gold daily chart source: EasyForex

At 10:47 AM Beijing time on April 24, spot gold was trading at $4680.54 per ounce.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.