One chart: Baltic Dry Index rises across the board, hitting a new high in more than a month.

2026-07-15 01:22:12

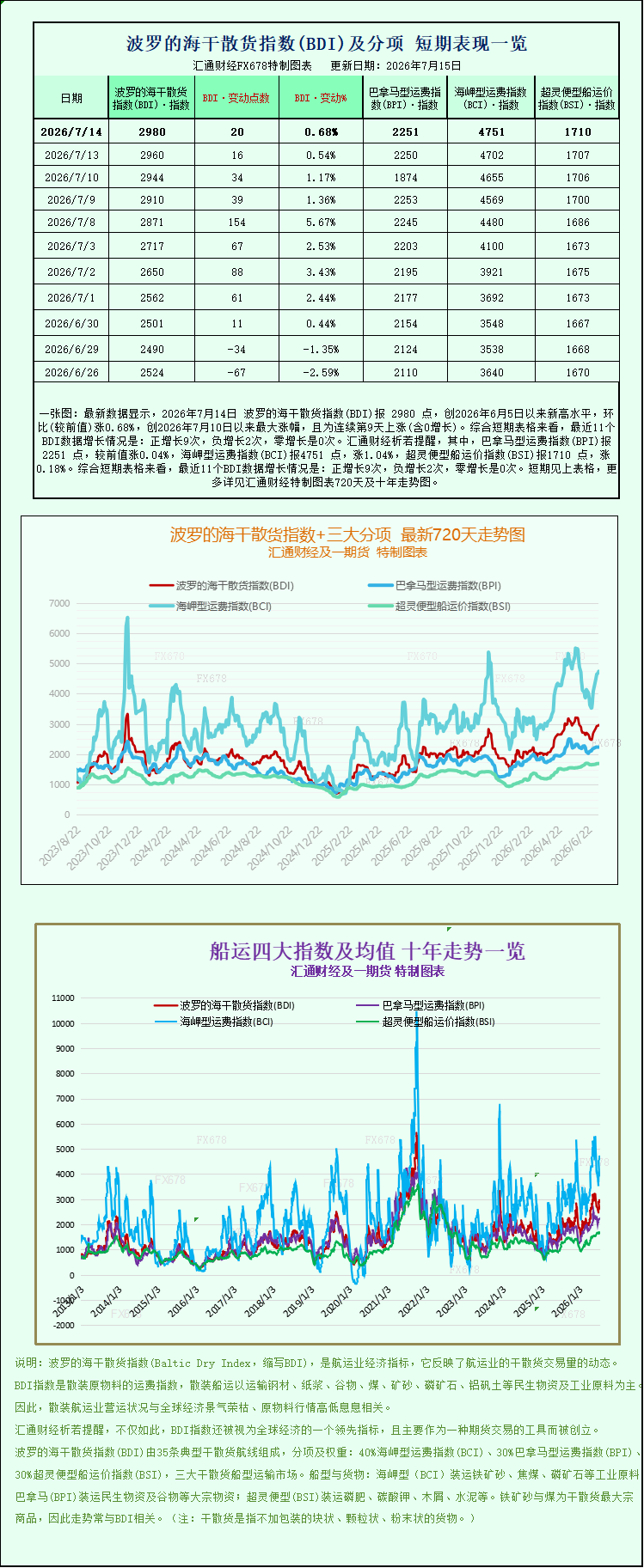

Latest data shows that the Baltic Dry Index (BDI) reached 2980 points on July 14, 2026, a new high since June 5, 2026, up 0.68% month-on-month, the largest increase since July 10, 2026, and marking the 9th consecutive day of increase (including zero growth). Looking at the short-term charts, the recent 11 BDI data points show: 9 positive increases, 2 negative increases, and 0 zero increases. Specifically, the Panamax Freight Index (BPI) was 2251 points, up 0.04% from the previous value; the Capesize Freight Index (BCI) was 4751 points, up 1.04%; and the Supramax Freight Index (BSI) was 1710 points, up 0.18%. For detailed 720-day and 10-year trend charts of the Baltic Dry Index and its three sub-indices, please refer to the charts specially created by FX678.  On July 14th local time, the Baltic Dry Index (BDI), a key indicator of the international shipping market, surged on Tuesday, breaking its highest level since early June. Freight rates for all major vessel types strengthened simultaneously, and shipping profits across all categories rose, driving a temporary recovery in the shipping market. The Baltic Dry Index is the most valuable benchmark for the global dry bulk shipping industry, comprehensively measuring spot charter rates for Capesize, Panamax, and Supramax vessels, directly reflecting the transoceanic transport market for bulk commodities such as iron ore, coal, and grain. In this market move, the index rose 20 points, or 0.7%, closing at 2980 points, the highest level in over a month since early June, indicating a significant increase in market bullish sentiment. All vessel types saw positive growth, with no specific segment experiencing a decline in freight rates. This synchronized rise across the entire sector is rare in the recent shipping market, fully reflecting the overall recovery in global dry bulk shipping demand. As the core driver of the market's rise, the Capesize index saw the most significant increase, climbing 49 points in a single day, a 1% increase, closing at 4751 points, also a new high in over a month. Capesize vessels are the mainstay of ocean-going bulk raw material transportation, with standard deadweight tonnage reaching 150,000 tons. They primarily handle long-distance sea transport of two major industrial raw materials globally: iron ore and thermal coal. Their freight rate fluctuations are directly related to the supply and demand of the steel and thermal power industry chains, making them a core indicator of the dry bulk market. Supporting data shows that the average daily charter rate for Capesize vessels increased by $445, ultimately reaching $39,583 per day, significantly improving shipowners' daily operating profits and further expanding the profit margins of ocean-going shipping companies. This round of strong Capesize freight rates is not driven by a single factor; multiple geopolitical and supply-demand factors have combined to push up the cost of raw material shipping. First, the geopolitical tensions in the Strait of Hormuz have escalated again, increasing the risk of navigating this vital global shipping route for energy and commodities. Traders and shipyards have raised shipping risk premiums, passively increasing the base cost of ocean shipping. Second, a strike has been confirmed at BHP Billiton's operations terminal in Port Hedland. Port Hedland is a key hub for Australian iron ore exports, and the limited port handling efficiency has directly fueled market concerns about a contraction in seaborne iron ore supply. Traders are locking in forward capacity in advance, further pushing up chartering demand. Meanwhile, domestic steel mills' restocking demand continues to be released, becoming a key endogenous driver supporting forward iron ore prices and seaborne demand. The domestic steel industry has entered a phase of raw material restocking, with many steel mills purchasing overseas iron ore in a concentrated manner. This has led to a surge in ocean shipping orders, continuously supporting Capesize vessel charter rates, and iron ore futures have risen in tandem, creating a positive correlation between upstream and downstream markets. The Panamax market remained relatively stable, with the Panamax index rising slightly by 1 point to close at 2251 points. This vessel type has a deadweight range of 60,000 to 70,000 tons and is mainly responsible for transoceanic coal and grain transportation, suitable for multiple grain and coal trade routes from Central America, Australia to Asia, and South America to Asia. Freight rate data shows that the average daily charter rate for Panamax vessels increased by $6, reaching $20,260 per day. Compared to the significant increase in Capesize vessels, the increase in Panamax vessels was moderate. This is mainly because the global supply and demand for grain transportation remained balanced, with stable shipments from grain exporting countries. Sufficient capacity on some routes also prevented a sharp rise in freight rates. However, the continued stable purchasing demand from downstream power plants and feed companies maintained the bottom of freight rates, resulting in a steady upward trend. The small vessel sector also saw a market recovery, with the Supramax index rising 3 points, or 0.2%, to close at 1710 points, the highest level since June 22nd. Supramax vessels, with their shallower drafts, are well-suited for loading and unloading operations in small and medium-sized ports. Their routes cover short-haul bulk cargo transportation, and trade in small and medium-tonnage coal, fertilizer, and grain within the region. Increased activity in regional shipping trade has driven a sustained recovery in this segment. Although the price increase per vessel is not as significant as that of large ocean-going vessels, the continuous small increases over several days reflect a simultaneous improvement in demand in the small and medium-sized short-haul shipping market. The market recovery is gradually spreading from mainline ocean shipping to regional feeder routes, forming a comprehensive recovery pattern. Industry analysts point out that the simultaneous rise in the Baltic Dry Index across all vessel types signifies that the dry bulk shipping market has broken free from its previous prolonged slump and entered a period of overall recovery. In the short term, the possibility of continued escalation of geopolitical conflicts in the Strait of Hormuz remains, and the risk premium for commodity shipping will continue to support freight rates. Strikes at Australian ports are disrupting iron ore export supply, coupled with continued raw material restocking by domestic steel mills, providing a basis for upward movement in Capesize vessel freight rates. In the medium to long term, global coal trade demand remains rigid, and with the peak electricity season approaching in the Northern Hemisphere, thermal power plants will increase their overseas coal purchases, which is expected to continue to support Panamax shipping demand. The global grain trade cycle is stable, with the peak export season for grains from South America and the Black Sea gradually beginning, which will also continue to provide stable order support for small and medium-sized vessels. However, the market also faces potential suppressive factors that require close monitoring. On the one hand, the pace of global manufacturing recovery is diverging, and the recovery in overseas industrial demand is weaker than expected. If subsequent bulk commodity purchases decline, it may weaken forward chartering demand. On the other hand, the continuous delivery of new dry bulk vessels in recent years means that long-term shipping capacity is still in an expansion cycle. If the recovery in demand is not as strong as the growth rate of shipping capacity, the upside potential for freight rates will be significantly constrained. From the perspective of supply chain transmission, the continued rise in the Baltic Dry Index will have multiple market impacts. For shipping companies, the increase in average daily charter rates directly boosts their revenue and profits, improving the performance expectations of listed dry bulk shipping companies. For commodity traders, rising shipping costs will increase the overall cost of raw material imports, which may indirectly affect downstream steel, electricity, and grain and oil end products. For international trade, the recovery in freight rates indirectly confirms the increased activity in global physical commodity trade, which is an important signal of the recovery in real economic and commercial activities.

On July 14th local time, the Baltic Dry Index (BDI), a key indicator of the international shipping market, surged on Tuesday, breaking its highest level since early June. Freight rates for all major vessel types strengthened simultaneously, and shipping profits across all categories rose, driving a temporary recovery in the shipping market. The Baltic Dry Index is the most valuable benchmark for the global dry bulk shipping industry, comprehensively measuring spot charter rates for Capesize, Panamax, and Supramax vessels, directly reflecting the transoceanic transport market for bulk commodities such as iron ore, coal, and grain. In this market move, the index rose 20 points, or 0.7%, closing at 2980 points, the highest level in over a month since early June, indicating a significant increase in market bullish sentiment. All vessel types saw positive growth, with no specific segment experiencing a decline in freight rates. This synchronized rise across the entire sector is rare in the recent shipping market, fully reflecting the overall recovery in global dry bulk shipping demand. As the core driver of the market's rise, the Capesize index saw the most significant increase, climbing 49 points in a single day, a 1% increase, closing at 4751 points, also a new high in over a month. Capesize vessels are the mainstay of ocean-going bulk raw material transportation, with standard deadweight tonnage reaching 150,000 tons. They primarily handle long-distance sea transport of two major industrial raw materials globally: iron ore and thermal coal. Their freight rate fluctuations are directly related to the supply and demand of the steel and thermal power industry chains, making them a core indicator of the dry bulk market. Supporting data shows that the average daily charter rate for Capesize vessels increased by $445, ultimately reaching $39,583 per day, significantly improving shipowners' daily operating profits and further expanding the profit margins of ocean-going shipping companies. This round of strong Capesize freight rates is not driven by a single factor; multiple geopolitical and supply-demand factors have combined to push up the cost of raw material shipping. First, the geopolitical tensions in the Strait of Hormuz have escalated again, increasing the risk of navigating this vital global shipping route for energy and commodities. Traders and shipyards have raised shipping risk premiums, passively increasing the base cost of ocean shipping. Second, a strike has been confirmed at BHP Billiton's operations terminal in Port Hedland. Port Hedland is a key hub for Australian iron ore exports, and the limited port handling efficiency has directly fueled market concerns about a contraction in seaborne iron ore supply. Traders are locking in forward capacity in advance, further pushing up chartering demand. Meanwhile, domestic steel mills' restocking demand continues to be released, becoming a key endogenous driver supporting forward iron ore prices and seaborne demand. The domestic steel industry has entered a phase of raw material restocking, with many steel mills purchasing overseas iron ore in a concentrated manner. This has led to a surge in ocean shipping orders, continuously supporting Capesize vessel charter rates, and iron ore futures have risen in tandem, creating a positive correlation between upstream and downstream markets. The Panamax market remained relatively stable, with the Panamax index rising slightly by 1 point to close at 2251 points. This vessel type has a deadweight range of 60,000 to 70,000 tons and is mainly responsible for transoceanic coal and grain transportation, suitable for multiple grain and coal trade routes from Central America, Australia to Asia, and South America to Asia. Freight rate data shows that the average daily charter rate for Panamax vessels increased by $6, reaching $20,260 per day. Compared to the significant increase in Capesize vessels, the increase in Panamax vessels was moderate. This is mainly because the global supply and demand for grain transportation remained balanced, with stable shipments from grain exporting countries. Sufficient capacity on some routes also prevented a sharp rise in freight rates. However, the continued stable purchasing demand from downstream power plants and feed companies maintained the bottom of freight rates, resulting in a steady upward trend. The small vessel sector also saw a market recovery, with the Supramax index rising 3 points, or 0.2%, to close at 1710 points, the highest level since June 22nd. Supramax vessels, with their shallower drafts, are well-suited for loading and unloading operations in small and medium-sized ports. Their routes cover short-haul bulk cargo transportation, and trade in small and medium-tonnage coal, fertilizer, and grain within the region. Increased activity in regional shipping trade has driven a sustained recovery in this segment. Although the price increase per vessel is not as significant as that of large ocean-going vessels, the continuous small increases over several days reflect a simultaneous improvement in demand in the small and medium-sized short-haul shipping market. The market recovery is gradually spreading from mainline ocean shipping to regional feeder routes, forming a comprehensive recovery pattern. Industry analysts point out that the simultaneous rise in the Baltic Dry Index across all vessel types signifies that the dry bulk shipping market has broken free from its previous prolonged slump and entered a period of overall recovery. In the short term, the possibility of continued escalation of geopolitical conflicts in the Strait of Hormuz remains, and the risk premium for commodity shipping will continue to support freight rates. Strikes at Australian ports are disrupting iron ore export supply, coupled with continued raw material restocking by domestic steel mills, providing a basis for upward movement in Capesize vessel freight rates. In the medium to long term, global coal trade demand remains rigid, and with the peak electricity season approaching in the Northern Hemisphere, thermal power plants will increase their overseas coal purchases, which is expected to continue to support Panamax shipping demand. The global grain trade cycle is stable, with the peak export season for grains from South America and the Black Sea gradually beginning, which will also continue to provide stable order support for small and medium-sized vessels. However, the market also faces potential suppressive factors that require close monitoring. On the one hand, the pace of global manufacturing recovery is diverging, and the recovery in overseas industrial demand is weaker than expected. If subsequent bulk commodity purchases decline, it may weaken forward chartering demand. On the other hand, the continuous delivery of new dry bulk vessels in recent years means that long-term shipping capacity is still in an expansion cycle. If the recovery in demand is not as strong as the growth rate of shipping capacity, the upside potential for freight rates will be significantly constrained. From the perspective of supply chain transmission, the continued rise in the Baltic Dry Index will have multiple market impacts. For shipping companies, the increase in average daily charter rates directly boosts their revenue and profits, improving the performance expectations of listed dry bulk shipping companies. For commodity traders, rising shipping costs will increase the overall cost of raw material imports, which may indirectly affect downstream steel, electricity, and grain and oil end products. For international trade, the recovery in freight rates indirectly confirms the increased activity in global physical commodity trade, which is an important signal of the recovery in real economic and commercial activities.

On July 14th local time, the Baltic Dry Index (BDI), a key indicator of the international shipping market, surged on Tuesday, breaking its highest level since early June. Freight rates for all major vessel types strengthened simultaneously, and shipping profits across all categories rose, driving a temporary recovery in the shipping market. The Baltic Dry Index is the most valuable benchmark for the global dry bulk shipping industry, comprehensively measuring spot charter rates for Capesize, Panamax, and Supramax vessels, directly reflecting the transoceanic transport market for bulk commodities such as iron ore, coal, and grain. In this market move, the index rose 20 points, or 0.7%, closing at 2980 points, the highest level in over a month since early June, indicating a significant increase in market bullish sentiment. All vessel types saw positive growth, with no specific segment experiencing a decline in freight rates. This synchronized rise across the entire sector is rare in the recent shipping market, fully reflecting the overall recovery in global dry bulk shipping demand. As the core driver of the market's rise, the Capesize index saw the most significant increase, climbing 49 points in a single day, a 1% increase, closing at 4751 points, also a new high in over a month. Capesize vessels are the mainstay of ocean-going bulk raw material transportation, with standard deadweight tonnage reaching 150,000 tons. They primarily handle long-distance sea transport of two major industrial raw materials globally: iron ore and thermal coal. Their freight rate fluctuations are directly related to the supply and demand of the steel and thermal power industry chains, making them a core indicator of the dry bulk market. Supporting data shows that the average daily charter rate for Capesize vessels increased by $445, ultimately reaching $39,583 per day, significantly improving shipowners' daily operating profits and further expanding the profit margins of ocean-going shipping companies. This round of strong Capesize freight rates is not driven by a single factor; multiple geopolitical and supply-demand factors have combined to push up the cost of raw material shipping. First, the geopolitical tensions in the Strait of Hormuz have escalated again, increasing the risk of navigating this vital global shipping route for energy and commodities. Traders and shipyards have raised shipping risk premiums, passively increasing the base cost of ocean shipping. Second, a strike has been confirmed at BHP Billiton's operations terminal in Port Hedland. Port Hedland is a key hub for Australian iron ore exports, and the limited port handling efficiency has directly fueled market concerns about a contraction in seaborne iron ore supply. Traders are locking in forward capacity in advance, further pushing up chartering demand. Meanwhile, domestic steel mills' restocking demand continues to be released, becoming a key endogenous driver supporting forward iron ore prices and seaborne demand. The domestic steel industry has entered a phase of raw material restocking, with many steel mills purchasing overseas iron ore in a concentrated manner. This has led to a surge in ocean shipping orders, continuously supporting Capesize vessel charter rates, and iron ore futures have risen in tandem, creating a positive correlation between upstream and downstream markets. The Panamax market remained relatively stable, with the Panamax index rising slightly by 1 point to close at 2251 points. This vessel type has a deadweight range of 60,000 to 70,000 tons and is mainly responsible for transoceanic coal and grain transportation, suitable for multiple grain and coal trade routes from Central America, Australia to Asia, and South America to Asia. Freight rate data shows that the average daily charter rate for Panamax vessels increased by $6, reaching $20,260 per day. Compared to the significant increase in Capesize vessels, the increase in Panamax vessels was moderate. This is mainly because the global supply and demand for grain transportation remained balanced, with stable shipments from grain exporting countries. Sufficient capacity on some routes also prevented a sharp rise in freight rates. However, the continued stable purchasing demand from downstream power plants and feed companies maintained the bottom of freight rates, resulting in a steady upward trend. The small vessel sector also saw a market recovery, with the Supramax index rising 3 points, or 0.2%, to close at 1710 points, the highest level since June 22nd. Supramax vessels, with their shallower drafts, are well-suited for loading and unloading operations in small and medium-sized ports. Their routes cover short-haul bulk cargo transportation, and trade in small and medium-tonnage coal, fertilizer, and grain within the region. Increased activity in regional shipping trade has driven a sustained recovery in this segment. Although the price increase per vessel is not as significant as that of large ocean-going vessels, the continuous small increases over several days reflect a simultaneous improvement in demand in the small and medium-sized short-haul shipping market. The market recovery is gradually spreading from mainline ocean shipping to regional feeder routes, forming a comprehensive recovery pattern. Industry analysts point out that the simultaneous rise in the Baltic Dry Index across all vessel types signifies that the dry bulk shipping market has broken free from its previous prolonged slump and entered a period of overall recovery. In the short term, the possibility of continued escalation of geopolitical conflicts in the Strait of Hormuz remains, and the risk premium for commodity shipping will continue to support freight rates. Strikes at Australian ports are disrupting iron ore export supply, coupled with continued raw material restocking by domestic steel mills, providing a basis for upward movement in Capesize vessel freight rates. In the medium to long term, global coal trade demand remains rigid, and with the peak electricity season approaching in the Northern Hemisphere, thermal power plants will increase their overseas coal purchases, which is expected to continue to support Panamax shipping demand. The global grain trade cycle is stable, with the peak export season for grains from South America and the Black Sea gradually beginning, which will also continue to provide stable order support for small and medium-sized vessels. However, the market also faces potential suppressive factors that require close monitoring. On the one hand, the pace of global manufacturing recovery is diverging, and the recovery in overseas industrial demand is weaker than expected. If subsequent bulk commodity purchases decline, it may weaken forward chartering demand. On the other hand, the continuous delivery of new dry bulk vessels in recent years means that long-term shipping capacity is still in an expansion cycle. If the recovery in demand is not as strong as the growth rate of shipping capacity, the upside potential for freight rates will be significantly constrained. From the perspective of supply chain transmission, the continued rise in the Baltic Dry Index will have multiple market impacts. For shipping companies, the increase in average daily charter rates directly boosts their revenue and profits, improving the performance expectations of listed dry bulk shipping companies. For commodity traders, rising shipping costs will increase the overall cost of raw material imports, which may indirectly affect downstream steel, electricity, and grain and oil end products. For international trade, the recovery in freight rates indirectly confirms the increased activity in global physical commodity trade, which is an important signal of the recovery in real economic and commercial activities.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.