The Bank of Japan faces a policy dilemma: the dual threats of Middle East geopolitical conflict and weak wages.

2026-03-16 13:16:25

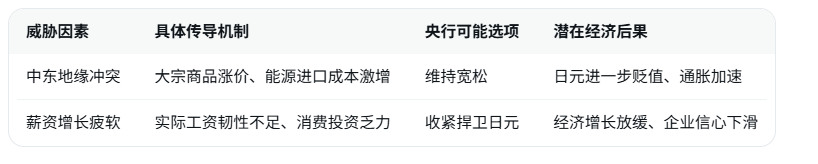

According to APP, Moody's Analytics analyst Stefan Anglick points out that Middle East geopolitical conflicts and persistently weak wage data pose a double threat to the Japanese economy. The conflicts have led to soaring commodity prices, pushing up the country's energy import spending, weakening the trade balance, and impacting the yen's exchange rate. This is a double blow to households and businesses. Despite record wage increases, the latest official data shows that real wage growth has not yet shown sufficient resilience. Stefan Anglick recently stated explicitly on this topic: "While strong wage negotiation results are likely again this year, this has not translated into wage growth across the entire economy as it has in the past. All of this disrupts the Bank of Japan 's policy path."

The central bank faces a dilemma: maintaining an accommodative monetary policy to buffer the economic slowdown, but potentially exacerbating the yen's depreciation and imported inflation; or tightening policy to defend the yen's exchange rate and curb prices, but further damaging already fragile consumption and investment. Latest trade data shows that Japan's energy imports have increased by more than 15% year-on-year due to rising prices, the current account surplus is narrowing at a faster pace, and the yen's exchange rate is under pressure to near-recent lows. While the spring wage negotiations yielded promising results, actual compliance rates among SMEs remain low, household purchasing power has not improved significantly, and corporate investment intentions remain weak.

The transmission mechanism of this dual threat is clear: geopolitical conflicts directly erode the trade balance through energy and raw material costs, while the depreciation of the yen further amplifies import inflation; weak wages suppress domestic demand from the demand side, creating a compound effect of supply shocks and weak demand. The Bank of Japan's previous gradual normalization path has been forced to reassess, and the market expects its policy rate adjustments to be more cautious.

The following is a comparison of the key impacts and central bank options under the dual threats to the Japanese economy (based on the latest official data and institutional scenario simulations):

Stefan Angeric's analysis highlights a structural challenge: even if wage negotiations reach new highs, if this fails to effectively transmit to the entire economy, the Bank of Japan will continue to face the dilemma of balancing "easing to boost growth but hurting the exchange rate" versus "tightening to stabilize the exchange rate but hurting growth." In the short term, pressure on real household income and rising business costs will jointly drag down GDP growth expectations, while in the medium to long term, the ability of structural reforms to mitigate external shocks will be tested.

Overall, the current geopolitical conflict in the Middle East , coupled with weak domestic wages, has pushed the Japanese economy into a policy dilemma. While the central bank has some buffer space, rising exchange rate and inflation risks will force policy decisions to rely more heavily on data evolution. Investors should closely monitor spring wage data, the monthly trade balance report, and central bank communications to proactively position themselves in yen assets and related hedging strategies.

Editor's Summary : The Japanese economy is facing a rare confluence of external supply shocks and weak domestic demand. Geopolitical conflicts in the Middle East are amplifying energy cost pressures, while sluggish wage transmission is further weakening the resilience of domestic demand. The central bank's policy path has been forced to shift from gradual normalization to a highly data-dependent approach, with short-term exchange rate fluctuations and inflation risks dominating market pricing. In the long term, structural wage reforms and energy diversification will be key to recovery. Global investors should dynamically adjust their Japanese asset allocations, using conflict easing and wage compliance rates as leading indicators.

Frequently Asked Questions

1. How exactly do Middle East geopolitical conflicts impact Japan's trade balance and the yen?

The conflict has led to a surge in prices for commodities such as crude oil and natural gas. As a major energy importer, Japan's import bills have increased by more than 15% year-on-year, directly worsening its current account. The depreciation of the yen has further amplified import costs, creating a vicious cycle. The latest exchange rate has come under pressure to a recent low, and the trade balance is narrowing at an accelerated pace.

2. Why is wage growth, despite record increases, still lacking resilience?

Nominal wages were strong due to spring negotiations, but actual implementation rates among small and medium-sized enterprises (SMEs) were low, and real wage growth, adjusted for inflation, was weak. Latest data indicates that the transmission of economic activity across the entire economy is ineffective, household purchasing power has not improved significantly, and consumption and investment cannot be effectively stimulated.

3. What policy dilemmas does the Bank of Japan face?

Maintaining loose monetary policy could buffer the slowdown in growth, but it would exacerbate the depreciation of the yen and imported inflation; while tightening policy could stabilize the exchange rate and control prices, it would further damage already fragile economic demand. Stefan Angelik points out that this has completely disrupted the original path of gradual normalization.

4. What does this double whammy mean for families and businesses?

Households are facing the dual pressures of shrinking real income and rising living costs, leading to a decline in their willingness to consume; businesses, on the other hand, are suffering from rising raw material costs and weak domestic demand, resulting in the postponement of investment plans and creating simultaneous pressure on both the demand and supply sides.

The central bank faces a dilemma: maintaining an accommodative monetary policy to buffer the economic slowdown, but potentially exacerbating the yen's depreciation and imported inflation; or tightening policy to defend the yen's exchange rate and curb prices, but further damaging already fragile consumption and investment. Latest trade data shows that Japan's energy imports have increased by more than 15% year-on-year due to rising prices, the current account surplus is narrowing at a faster pace, and the yen's exchange rate is under pressure to near-recent lows. While the spring wage negotiations yielded promising results, actual compliance rates among SMEs remain low, household purchasing power has not improved significantly, and corporate investment intentions remain weak.

The transmission mechanism of this dual threat is clear: geopolitical conflicts directly erode the trade balance through energy and raw material costs, while the depreciation of the yen further amplifies import inflation; weak wages suppress domestic demand from the demand side, creating a compound effect of supply shocks and weak demand. The Bank of Japan's previous gradual normalization path has been forced to reassess, and the market expects its policy rate adjustments to be more cautious.

The following is a comparison of the key impacts and central bank options under the dual threats to the Japanese economy (based on the latest official data and institutional scenario simulations):

Stefan Angeric's analysis highlights a structural challenge: even if wage negotiations reach new highs, if this fails to effectively transmit to the entire economy, the Bank of Japan will continue to face the dilemma of balancing "easing to boost growth but hurting the exchange rate" versus "tightening to stabilize the exchange rate but hurting growth." In the short term, pressure on real household income and rising business costs will jointly drag down GDP growth expectations, while in the medium to long term, the ability of structural reforms to mitigate external shocks will be tested.

Overall, the current geopolitical conflict in the Middle East , coupled with weak domestic wages, has pushed the Japanese economy into a policy dilemma. While the central bank has some buffer space, rising exchange rate and inflation risks will force policy decisions to rely more heavily on data evolution. Investors should closely monitor spring wage data, the monthly trade balance report, and central bank communications to proactively position themselves in yen assets and related hedging strategies.

Editor's Summary : The Japanese economy is facing a rare confluence of external supply shocks and weak domestic demand. Geopolitical conflicts in the Middle East are amplifying energy cost pressures, while sluggish wage transmission is further weakening the resilience of domestic demand. The central bank's policy path has been forced to shift from gradual normalization to a highly data-dependent approach, with short-term exchange rate fluctuations and inflation risks dominating market pricing. In the long term, structural wage reforms and energy diversification will be key to recovery. Global investors should dynamically adjust their Japanese asset allocations, using conflict easing and wage compliance rates as leading indicators.

Frequently Asked Questions

1. How exactly do Middle East geopolitical conflicts impact Japan's trade balance and the yen?

The conflict has led to a surge in prices for commodities such as crude oil and natural gas. As a major energy importer, Japan's import bills have increased by more than 15% year-on-year, directly worsening its current account. The depreciation of the yen has further amplified import costs, creating a vicious cycle. The latest exchange rate has come under pressure to a recent low, and the trade balance is narrowing at an accelerated pace.

2. Why is wage growth, despite record increases, still lacking resilience?

Nominal wages were strong due to spring negotiations, but actual implementation rates among small and medium-sized enterprises (SMEs) were low, and real wage growth, adjusted for inflation, was weak. Latest data indicates that the transmission of economic activity across the entire economy is ineffective, household purchasing power has not improved significantly, and consumption and investment cannot be effectively stimulated.

3. What policy dilemmas does the Bank of Japan face?

Maintaining loose monetary policy could buffer the slowdown in growth, but it would exacerbate the depreciation of the yen and imported inflation; while tightening policy could stabilize the exchange rate and control prices, it would further damage already fragile economic demand. Stefan Angelik points out that this has completely disrupted the original path of gradual normalization.

4. What does this double whammy mean for families and businesses?

Households are facing the dual pressures of shrinking real income and rising living costs, leading to a decline in their willingness to consume; businesses, on the other hand, are suffering from rising raw material costs and weak domestic demand, resulting in the postponement of investment plans and creating simultaneous pressure on both the demand and supply sides.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.