A chart shows that the Baltic Dry Index is rising, with freight rates for different vessel types showing a divergent upward trend.

2026-04-01 22:47:49

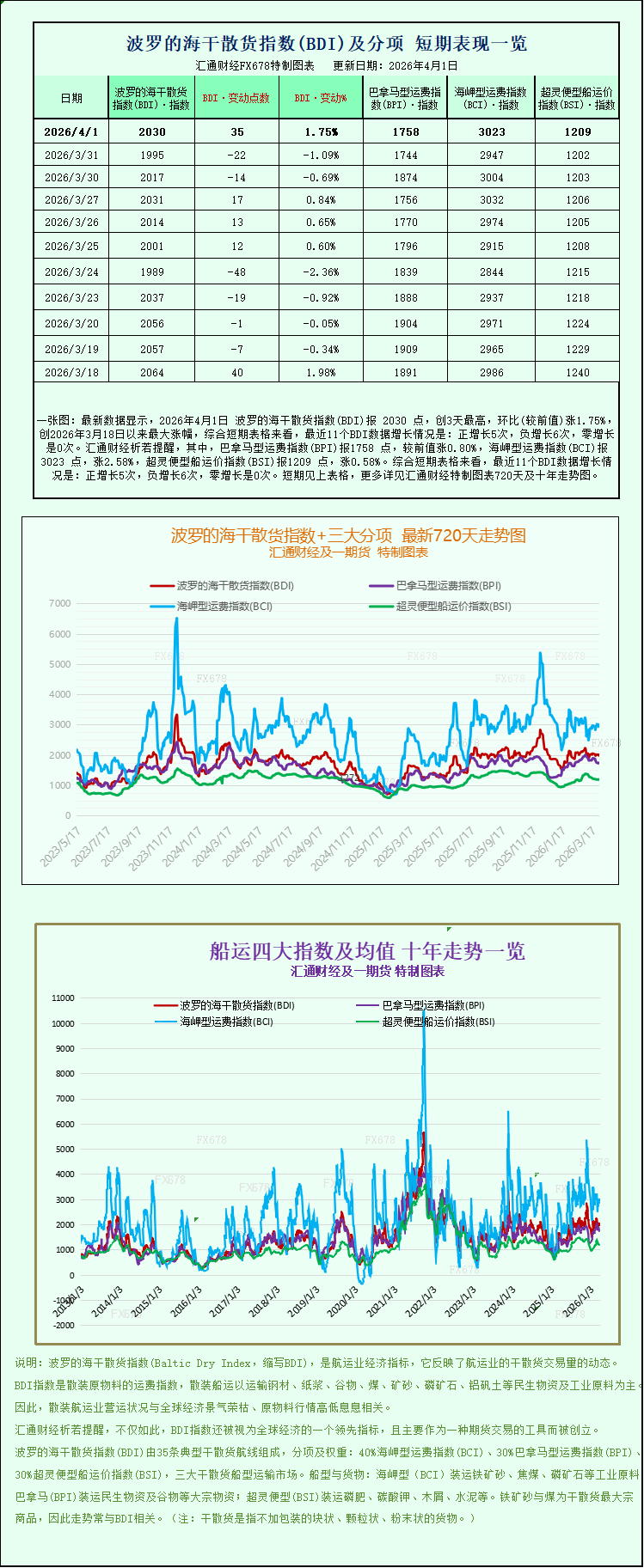

Latest data shows that the Baltic Dry Index (BDI) reached 2030 points on April 1, 2026, a three-day high, up 1.75% month-on-month (compared to the previous value), marking the largest increase since March 18, 2026. Looking at the short-term charts, the recent 11 BDI data points show: 5 positive increases, 6 negative increases, and 0 zero increases. Specifically, the Panamax Freight Index (BPI) was 1758 points, up 0.80% from the previous value; the Capesize Freight Index (BCI) was 3023 points, up 2.58%; and the Supramax Freight Index (BSI) was 1209 points, up 0.58%. For detailed 720-day and 10-year trend charts of the Baltic Dry Index and its three main sub-indices, please refer to the specially designed charts.

Recently, the international dry bulk shipping market has seen a significant recovery, with the Baltic Dry Index (BDI) rising markedly. The core driver was the simultaneous increase in freight rates for all major vessel types, breaking the downward trend since March and injecting new vitality into the global dry bulk trade market. This also reflects the complex impact of current global commodity demand and geopolitical situation.

The Baltic Dry Index (BDI), a core indicator of the global dry bulk shipping market, primarily monitors changes in spot freight rates for vessels transporting dry bulk commodities such as iron ore, coal, and grains worldwide. Its fluctuations directly reflect the activity of global commodity trade and the market's supply and demand dynamics. On Wednesday, the index saw a significant rise. Specifically, the core index, which tracks freight rates for the three major vessel types—Capesize, Panamax, and Supramax—rose by 35 points, a gain of 1.8%, ultimately closing at 2030 points. It is worth noting that this index experienced a nearly 7% decline in March; this rise signals a positive sign that the market is beginning to bottom out and rebound, reflecting a gradual recovery in demand in the dry bulk shipping market.

Looking at different ship types, performance varied somewhat, but overall, the trend was upward, with Capesize vessels (also known as Good Hope sizes) being the main driver of the index increase. Capesize vessels, large ships in dry bulk shipping, typically have a deadweight tonnage between 120,000 and 200,000 tons. They are mainly used for long-distance transport of core industrial materials such as iron ore and coal. Named for their size limitations requiring them to circumnavigate the Cape of Good Hope and Cape Horn, they are a core carrier of global industrial raw material transportation. On that day, the Capesize index rose 76 points, an increase of approximately 2.6%, closing at 3023 points, significantly higher than the overall index. However, in contrast, the average daily earnings of Capesize vessels saw a slight decline, decreasing by $697 from the previous day to $23,918. This short-term divergence between the index and daily earnings is mainly due to a temporary misalignment between ship capacity scheduling and short-term supply and demand fluctuations, and does not change the overall upward trend in freight rates for this ship type.

The rise in the Capesize freight rate index is closely related to the recovery in the iron ore market. On Wednesday, iron ore futures prices saw a significant increase, supported by two main factors: first, optimistic factory data from major global economies reflected a recovery in industrial production, leading to increased expectations for demand for industrial raw materials such as iron ore; second, the market widely anticipates that China, the world's largest iron ore consumer, will introduce stimulus measures to further boost iron ore demand. Previously, five departments, including the Ministry of Industry and Information Technology, jointly issued the "Work Plan for Stabilizing Growth in the Steel Industry (2025-2026)," proposing measures such as stabilizing raw material supply and stimulating the consumption potential of the steel industry, which also provided long-term support for iron ore demand, indirectly driving up the transportation demand for Capesize vessels and pushing up their freight rate index.

Besides Capesize vessels, Panamax vessels also saw a simultaneous increase in both freight rates and daily revenue. Panamax vessels are medium-sized ships in dry bulk shipping, with a deadweight tonnage between 55,000 and 85,000 tons. Named for their ability to pass fully loaded through the Panama Canal, they primarily handle the transport of 60,000 to 70,000 tons of coal, grain, and other goods, playing a crucial role in global food and energy transportation. Their freight rates are closely linked to global food trade and coal demand. On that day, the Panamax index rose 14 points, or 0.8%, to reach 1758 points; correspondingly, the average daily revenue per vessel increased by $133 to $15,825, reflecting a steady increase in global demand for food and coal transportation, and benefiting from the recent recovery in international coal demand and the gradual recovery of the food transportation market.

Unlike the other two major ship types, Supramax bulk carriers saw a slight pullback on the day. Supramax bulk carriers have a deadweight tonnage between 50,000 and 65,000 tons, are equipped with cranes and loading/unloading equipment, and are suitable for small-volume bulk cargo transportation between ports with less favorable conditions, mainly transporting products such as grains, fertilizers, and cement. On that day, the Supramax bulk carrier index fell 7 points, a decrease of 0.6%, closing at 1209 points, becoming the only one of the three major ship types to experience a decline. This fluctuation mainly stemmed from a temporary decline in short-term demand for small-volume bulk cargo transportation and a slight increase in market capacity supply, which is a normal fluctuation within the industry and did not affect the overall recovery trend of the dry bulk market.

While the dry bulk shipping market recovered, the international crude oil market exhibited a starkly different trend, a shift closely linked to the current complex geopolitical situation in the Middle East. On that day, oil prices initially rose in the morning session but subsequently gave back all gains. The core reason was the continued uncertainty surrounding the Middle East situation, which unsettled the market, with investors worried that escalating regional conflict would impact global oil supplies. Meanwhile, US President Trump reiterated his suggestion that the US-Israel war against Iran might be nearing its end, further exacerbating market uncertainty and causing oil prices to rise and then fall.

More concerning is the escalating tensions between the United States and its NATO allies caused by the changing situation in the Middle East. The Strait of Hormuz, a strategic waterway connecting the Persian Gulf and the Indian Ocean, carries a significant portion of global maritime crude oil trade, and its security directly impacts global energy supply. Recently, due to the refusal of European member states to send vessels to participate in the clearing of the Strait of Hormuz, Trump stated in an interview that he was considering withdrawing the United States from NATO to pressure European allies to intervene in the Strait of Hormuz issue. This statement not only exacerbated the differences between the United States and its NATO allies but also further increased global geopolitical uncertainty, thus having a ripple effect on international shipping and energy markets. War risk insurance costs for shipping companies are rising continuously, and some companies have begun to cautiously manage their shipping operations in the relevant waters.

Overall, the recent rise in the Baltic Dry Index (BDI) directly reflects the gradual recovery in global dry bulk demand. The divergent performance of the three main vessel types reflects the differences in demand for transporting different categories of bulk commodities. Looking ahead, with the implementation of China's stimulus measures and the continued recovery of global industrial production, the dry bulk shipping market is expected to maintain its upward trend. However, it is also necessary to pay attention to the potential impact of Middle East geopolitical tensions, international oil price fluctuations, and global economic uncertainties. These factors will continue to influence the trend of the dry bulk freight index and the operational performance of various vessel types.

Recently, the international dry bulk shipping market has seen a significant recovery, with the Baltic Dry Index (BDI) rising markedly. The core driver was the simultaneous increase in freight rates for all major vessel types, breaking the downward trend since March and injecting new vitality into the global dry bulk trade market. This also reflects the complex impact of current global commodity demand and geopolitical situation.

The Baltic Dry Index (BDI), a core indicator of the global dry bulk shipping market, primarily monitors changes in spot freight rates for vessels transporting dry bulk commodities such as iron ore, coal, and grains worldwide. Its fluctuations directly reflect the activity of global commodity trade and the market's supply and demand dynamics. On Wednesday, the index saw a significant rise. Specifically, the core index, which tracks freight rates for the three major vessel types—Capesize, Panamax, and Supramax—rose by 35 points, a gain of 1.8%, ultimately closing at 2030 points. It is worth noting that this index experienced a nearly 7% decline in March; this rise signals a positive sign that the market is beginning to bottom out and rebound, reflecting a gradual recovery in demand in the dry bulk shipping market.

Looking at different ship types, performance varied somewhat, but overall, the trend was upward, with Capesize vessels (also known as Good Hope sizes) being the main driver of the index increase. Capesize vessels, large ships in dry bulk shipping, typically have a deadweight tonnage between 120,000 and 200,000 tons. They are mainly used for long-distance transport of core industrial materials such as iron ore and coal. Named for their size limitations requiring them to circumnavigate the Cape of Good Hope and Cape Horn, they are a core carrier of global industrial raw material transportation. On that day, the Capesize index rose 76 points, an increase of approximately 2.6%, closing at 3023 points, significantly higher than the overall index. However, in contrast, the average daily earnings of Capesize vessels saw a slight decline, decreasing by $697 from the previous day to $23,918. This short-term divergence between the index and daily earnings is mainly due to a temporary misalignment between ship capacity scheduling and short-term supply and demand fluctuations, and does not change the overall upward trend in freight rates for this ship type.

The rise in the Capesize freight rate index is closely related to the recovery in the iron ore market. On Wednesday, iron ore futures prices saw a significant increase, supported by two main factors: first, optimistic factory data from major global economies reflected a recovery in industrial production, leading to increased expectations for demand for industrial raw materials such as iron ore; second, the market widely anticipates that China, the world's largest iron ore consumer, will introduce stimulus measures to further boost iron ore demand. Previously, five departments, including the Ministry of Industry and Information Technology, jointly issued the "Work Plan for Stabilizing Growth in the Steel Industry (2025-2026)," proposing measures such as stabilizing raw material supply and stimulating the consumption potential of the steel industry, which also provided long-term support for iron ore demand, indirectly driving up the transportation demand for Capesize vessels and pushing up their freight rate index.

Besides Capesize vessels, Panamax vessels also saw a simultaneous increase in both freight rates and daily revenue. Panamax vessels are medium-sized ships in dry bulk shipping, with a deadweight tonnage between 55,000 and 85,000 tons. Named for their ability to pass fully loaded through the Panama Canal, they primarily handle the transport of 60,000 to 70,000 tons of coal, grain, and other goods, playing a crucial role in global food and energy transportation. Their freight rates are closely linked to global food trade and coal demand. On that day, the Panamax index rose 14 points, or 0.8%, to reach 1758 points; correspondingly, the average daily revenue per vessel increased by $133 to $15,825, reflecting a steady increase in global demand for food and coal transportation, and benefiting from the recent recovery in international coal demand and the gradual recovery of the food transportation market.

Unlike the other two major ship types, Supramax bulk carriers saw a slight pullback on the day. Supramax bulk carriers have a deadweight tonnage between 50,000 and 65,000 tons, are equipped with cranes and loading/unloading equipment, and are suitable for small-volume bulk cargo transportation between ports with less favorable conditions, mainly transporting products such as grains, fertilizers, and cement. On that day, the Supramax bulk carrier index fell 7 points, a decrease of 0.6%, closing at 1209 points, becoming the only one of the three major ship types to experience a decline. This fluctuation mainly stemmed from a temporary decline in short-term demand for small-volume bulk cargo transportation and a slight increase in market capacity supply, which is a normal fluctuation within the industry and did not affect the overall recovery trend of the dry bulk market.

While the dry bulk shipping market recovered, the international crude oil market exhibited a starkly different trend, a shift closely linked to the current complex geopolitical situation in the Middle East. On that day, oil prices initially rose in the morning session but subsequently gave back all gains. The core reason was the continued uncertainty surrounding the Middle East situation, which unsettled the market, with investors worried that escalating regional conflict would impact global oil supplies. Meanwhile, US President Trump reiterated his suggestion that the US-Israel war against Iran might be nearing its end, further exacerbating market uncertainty and causing oil prices to rise and then fall.

More concerning is the escalating tensions between the United States and its NATO allies caused by the changing situation in the Middle East. The Strait of Hormuz, a strategic waterway connecting the Persian Gulf and the Indian Ocean, carries a significant portion of global maritime crude oil trade, and its security directly impacts global energy supply. Recently, due to the refusal of European member states to send vessels to participate in the clearing of the Strait of Hormuz, Trump stated in an interview that he was considering withdrawing the United States from NATO to pressure European allies to intervene in the Strait of Hormuz issue. This statement not only exacerbated the differences between the United States and its NATO allies but also further increased global geopolitical uncertainty, thus having a ripple effect on international shipping and energy markets. War risk insurance costs for shipping companies are rising continuously, and some companies have begun to cautiously manage their shipping operations in the relevant waters.

Overall, the recent rise in the Baltic Dry Index (BDI) directly reflects the gradual recovery in global dry bulk demand. The divergent performance of the three main vessel types reflects the differences in demand for transporting different categories of bulk commodities. Looking ahead, with the implementation of China's stimulus measures and the continued recovery of global industrial production, the dry bulk shipping market is expected to maintain its upward trend. However, it is also necessary to pay attention to the potential impact of Middle East geopolitical tensions, international oil price fluctuations, and global economic uncertainties. These factors will continue to influence the trend of the dry bulk freight index and the operational performance of various vessel types.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.