A chart shows that the Baltic Dry Index has hit a near-month high, with freight rates rising for multiple vessel types.

2026-04-02 23:19:12

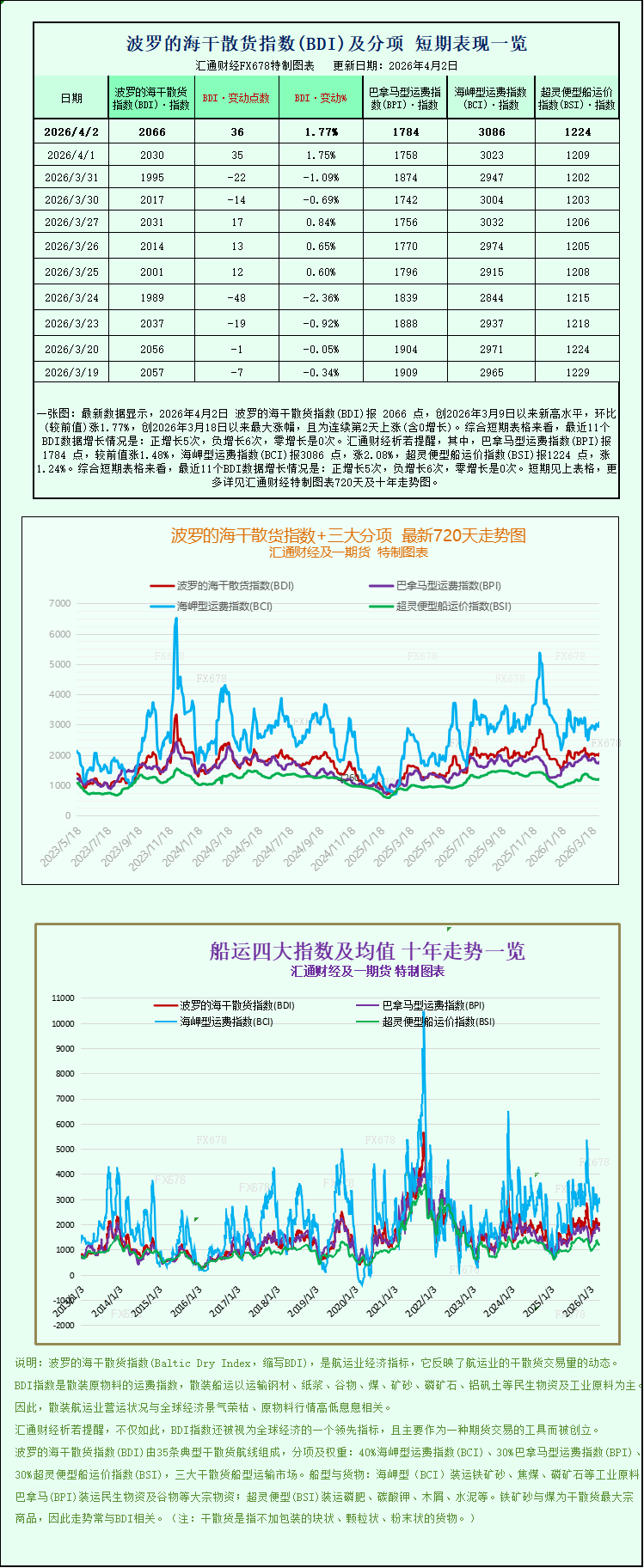

Latest data shows that the Baltic Dry Index (BDI) reached 2066 points on April 2, 2026, a new high since March 9, 2026, up 1.77% month-on-month, the largest increase since March 18, 2026, and the second consecutive day of increase (including zero growth). Looking at the short-term charts, the recent 11 BDI data points show: 5 positive increases, 6 negative increases, and 0 zero increases. Specifically, the Panamax Freight Index (BPI) reached 1784 points, up 1.48% from the previous value; the Capesize Freight Index (BCI) reached 3086 points, up 2.08%; and the Supramax Freight Index (BSI) reached 1224 points, up 1.24%. For detailed 720-day and 10-year trend charts of the Baltic Dry Index and its three main sub-indices, please refer to the specially designed charts.

The global dry bulk shipping market has recently shown a significant recovery trend. Driven by the comprehensive increase in freight rates for all types of vessels, the Baltic Dry Index has continued to climb, successfully reaching its highest level in nearly a month. This has become a key point of interest in the current global commodity shipping market and reflects the short-term changes in the global dry bulk trade pattern.

Specifically, the Baltic Dry Index (BDI), a core indicator for monitoring freight rates for dry bulk cargo vessels globally, covering major dry bulk shipping routes, saw a significant rise on Thursday, successfully climbing to its highest level in nearly a month. The main driving force was the simultaneous increase in freight rates for major vessel types such as Capesize, Panamax, and Supramax, which combined to push the index upward and break the previous period of fluctuation.

The Baltic Dry Index (BDI), a core benchmark for measuring global dry bulk freight rates and tracking freight rates for the three major vessel types—Capesize, Panamax, and Supramax—rose 36 points, or 1.8%, to close at 2066 points. This is the highest level since March 5th, indicating that the dry bulk shipping market has resumed its upward trend after a brief adjustment. Industry analysts point out that this increase was not driven by a single factor, but rather by the combined effect of supply and demand. On the one hand, global demand for some dry bulk cargo categories is steadily recovering; on the other hand, vessel capacity supply is experiencing a temporary tightness. These two factors combined have led to a comprehensive rise in freight rates.

Looking at specific vessel types, Capesize vessels performed particularly well, with their corresponding index rising 63 points, or approximately 2.1%, to close at 3086 points, a new high in over four weeks, becoming the core driving force behind the overall index increase. Capesize vessels, as the "juggernauts" of global dry bulk shipping, typically handle the transport of 150,000 tons of bulk commodities, with core cargoes including basic industrial raw materials such as iron ore and coal. Their freight rate fluctuations are closely related to the pace of global industrial production. Along with this index increase, the average daily earnings of Capesize vessels also rose, increasing by $570 to $24,488. This increase reflects a phased recovery in global demand for industrial raw material transportation, especially the recent explosive growth in demand for Capesize shipping on the West Africa-China route. China's increased imports of bauxite and iron ore from Guinea and other West African countries have further driven up demand and freight rates for this vessel type.

It is worth noting that while the dry bulk shipping market is recovering and Capesize freight rates are rising, the iron ore futures market is showing the opposite trend. Affected by the continued narrowing of profit margins in the domestic steel industry and the temporary weakness in demand in China, the world's largest iron ore consumer, after completing its pre-holiday restocking tasks, iron ore futures prices have continued to decline, eventually falling to their lowest point in nearly three weeks. Data from the Tonghuashun financial database shows that as of April 2nd, the closing price of the main iron ore futures contract was 805 yuan/ton, a significant drop from the previous high. This divergence between "hot shipping and cold futures" reflects the current phase of supply-demand imbalance in the iron ore market—the increase in shipping demand is largely due to short-term adjustments in transportation schedules, while weak end-consumer demand directly suppresses iron ore futures prices.

Besides Capesize vessels, Panamax vessels also showed a positive upward trend. The Panamax index rose 26 points, or 1.5%, to close at 1784 points, continuing its recent upward trend. Panamax vessels have a deadweight between Capesize and Supramax, typically carrying 60,000 to 70,000 tons of cargo, with core commodities including coal and grain. The increase in freight rates reflects the steady recovery in global energy and food trade transportation demand. Correspondingly, the average daily revenue of Panamax vessels also increased by $231 to $16,056, further confirming the improved market conditions for this vessel type. From a market perspective, since the beginning of 2026, the overall valuation of second-hand dry bulk carriers has continued to rise, with smaller vessels showing more significant increases. Panamax freight rates have maintained a year-on-year increase of approximately 40%, demonstrating the resilience of this vessel type market.

The Supramax bulk carrier index also rose, increasing by 15 points, or 1.2%, to close at 1224 points. While the increase was less than that of Capesize and Panamax vessels, it continued the overall market recovery trend, becoming an important supplement to the rise in the Baltic Dry Index. Supramax bulk carriers, with their flexible route adaptability, mainly undertake small-volume dry bulk cargo transportation tasks, covering a variety of industrial raw materials and agricultural products. Their freight rate increase reflects the increased activity in global small- and medium-volume dry bulk trade. It is understood that since the beginning of 2026, second-hand prices for Supramax vessels have generally increased by 7%–15%, with market demand shifting towards older vessels, further supporting the stable upward trend in freight rates for this type of vessel.

Meanwhile, the global energy market experienced sharp fluctuations on Thursday, further exacerbating uncertainty in the global commodities market. US President Trump publicly vowed to launch a more aggressive strike against Iran, a statement that shattered market expectations for a swift end to the Middle East conflict, causing a sharp resurgence in global oil prices and severely impacting global consumers and related industries. According to Xinhua News Agency, the ongoing escalation of the Middle East conflict has severely hampered navigation on key oil transport routes such as the Strait of Hormuz and the Bab el-Mandeb Strait. Market concerns that shipping disruptions will further exacerbate energy supply shortages are growing, and Trump's tough stance further fueled market panic, causing London Brent crude futures prices to rise by as much as 4.8% to $106.04 per barrel, while US West Texas Intermediate crude futures prices also rose by 4.2%.

Industry analysts believe that the recent rise in the Baltic Dry Index reflects both a temporary recovery in global dry bulk shipping demand and a temporary tightness in shipping capacity. The escalating situation in the Middle East and the sharp rise in oil prices may further impact the cost and demand structure of the global dry bulk shipping market—rising oil prices will increase ship fuel costs, potentially indirectly affecting dry bulk freight rates, while the uncertainty in the Middle East may also influence the pace of global commodity trade. However, some analysts point out that the volume of Gulf trade in global dry bulk trade is limited, and its systemic impact on global freight rates is limited in the short term. But if the conflict prolongs and triggers an energy crisis, it could drag down the global economy, thus putting medium- to long-term downward pressure on commodity demand, freight rates, and ship prices.

The global dry bulk shipping market has recently shown a significant recovery trend. Driven by the comprehensive increase in freight rates for all types of vessels, the Baltic Dry Index has continued to climb, successfully reaching its highest level in nearly a month. This has become a key point of interest in the current global commodity shipping market and reflects the short-term changes in the global dry bulk trade pattern.

Specifically, the Baltic Dry Index (BDI), a core indicator for monitoring freight rates for dry bulk cargo vessels globally, covering major dry bulk shipping routes, saw a significant rise on Thursday, successfully climbing to its highest level in nearly a month. The main driving force was the simultaneous increase in freight rates for major vessel types such as Capesize, Panamax, and Supramax, which combined to push the index upward and break the previous period of fluctuation.

The Baltic Dry Index (BDI), a core benchmark for measuring global dry bulk freight rates and tracking freight rates for the three major vessel types—Capesize, Panamax, and Supramax—rose 36 points, or 1.8%, to close at 2066 points. This is the highest level since March 5th, indicating that the dry bulk shipping market has resumed its upward trend after a brief adjustment. Industry analysts point out that this increase was not driven by a single factor, but rather by the combined effect of supply and demand. On the one hand, global demand for some dry bulk cargo categories is steadily recovering; on the other hand, vessel capacity supply is experiencing a temporary tightness. These two factors combined have led to a comprehensive rise in freight rates.

Looking at specific vessel types, Capesize vessels performed particularly well, with their corresponding index rising 63 points, or approximately 2.1%, to close at 3086 points, a new high in over four weeks, becoming the core driving force behind the overall index increase. Capesize vessels, as the "juggernauts" of global dry bulk shipping, typically handle the transport of 150,000 tons of bulk commodities, with core cargoes including basic industrial raw materials such as iron ore and coal. Their freight rate fluctuations are closely related to the pace of global industrial production. Along with this index increase, the average daily earnings of Capesize vessels also rose, increasing by $570 to $24,488. This increase reflects a phased recovery in global demand for industrial raw material transportation, especially the recent explosive growth in demand for Capesize shipping on the West Africa-China route. China's increased imports of bauxite and iron ore from Guinea and other West African countries have further driven up demand and freight rates for this vessel type.

It is worth noting that while the dry bulk shipping market is recovering and Capesize freight rates are rising, the iron ore futures market is showing the opposite trend. Affected by the continued narrowing of profit margins in the domestic steel industry and the temporary weakness in demand in China, the world's largest iron ore consumer, after completing its pre-holiday restocking tasks, iron ore futures prices have continued to decline, eventually falling to their lowest point in nearly three weeks. Data from the Tonghuashun financial database shows that as of April 2nd, the closing price of the main iron ore futures contract was 805 yuan/ton, a significant drop from the previous high. This divergence between "hot shipping and cold futures" reflects the current phase of supply-demand imbalance in the iron ore market—the increase in shipping demand is largely due to short-term adjustments in transportation schedules, while weak end-consumer demand directly suppresses iron ore futures prices.

Besides Capesize vessels, Panamax vessels also showed a positive upward trend. The Panamax index rose 26 points, or 1.5%, to close at 1784 points, continuing its recent upward trend. Panamax vessels have a deadweight between Capesize and Supramax, typically carrying 60,000 to 70,000 tons of cargo, with core commodities including coal and grain. The increase in freight rates reflects the steady recovery in global energy and food trade transportation demand. Correspondingly, the average daily revenue of Panamax vessels also increased by $231 to $16,056, further confirming the improved market conditions for this vessel type. From a market perspective, since the beginning of 2026, the overall valuation of second-hand dry bulk carriers has continued to rise, with smaller vessels showing more significant increases. Panamax freight rates have maintained a year-on-year increase of approximately 40%, demonstrating the resilience of this vessel type market.

The Supramax bulk carrier index also rose, increasing by 15 points, or 1.2%, to close at 1224 points. While the increase was less than that of Capesize and Panamax vessels, it continued the overall market recovery trend, becoming an important supplement to the rise in the Baltic Dry Index. Supramax bulk carriers, with their flexible route adaptability, mainly undertake small-volume dry bulk cargo transportation tasks, covering a variety of industrial raw materials and agricultural products. Their freight rate increase reflects the increased activity in global small- and medium-volume dry bulk trade. It is understood that since the beginning of 2026, second-hand prices for Supramax vessels have generally increased by 7%–15%, with market demand shifting towards older vessels, further supporting the stable upward trend in freight rates for this type of vessel.

Meanwhile, the global energy market experienced sharp fluctuations on Thursday, further exacerbating uncertainty in the global commodities market. US President Trump publicly vowed to launch a more aggressive strike against Iran, a statement that shattered market expectations for a swift end to the Middle East conflict, causing a sharp resurgence in global oil prices and severely impacting global consumers and related industries. According to Xinhua News Agency, the ongoing escalation of the Middle East conflict has severely hampered navigation on key oil transport routes such as the Strait of Hormuz and the Bab el-Mandeb Strait. Market concerns that shipping disruptions will further exacerbate energy supply shortages are growing, and Trump's tough stance further fueled market panic, causing London Brent crude futures prices to rise by as much as 4.8% to $106.04 per barrel, while US West Texas Intermediate crude futures prices also rose by 4.2%.

Industry analysts believe that the recent rise in the Baltic Dry Index reflects both a temporary recovery in global dry bulk shipping demand and a temporary tightness in shipping capacity. The escalating situation in the Middle East and the sharp rise in oil prices may further impact the cost and demand structure of the global dry bulk shipping market—rising oil prices will increase ship fuel costs, potentially indirectly affecting dry bulk freight rates, while the uncertainty in the Middle East may also influence the pace of global commodity trade. However, some analysts point out that the volume of Gulf trade in global dry bulk trade is limited, and its systemic impact on global freight rates is limited in the short term. But if the conflict prolongs and triggers an energy crisis, it could drag down the global economy, thus putting medium- to long-term downward pressure on commodity demand, freight rates, and ship prices.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.