Structural Imbalances Coupled with Geopolitical Shocks: March Non-Farm Payrolls, the Threshold for Recession under the SAM Rule

2026-04-03 16:00:52

March 2026 US Non-Farm Payrolls Outlook: Employment Illusions in a Wartime Economy, SAM Rules Red Line Hanging High

On April 3, 2026, Eastern Time, the U.S. Bureau of Labor Statistics will officially release the March non-farm payroll data. The mainstream market expectation is that 60,000 new jobs will be added and the unemployment rate will remain stable at 4.4%.

This non-farm payroll report is the first employment report since the escalation of geopolitical conflicts in the Middle East, and it deserves attention.

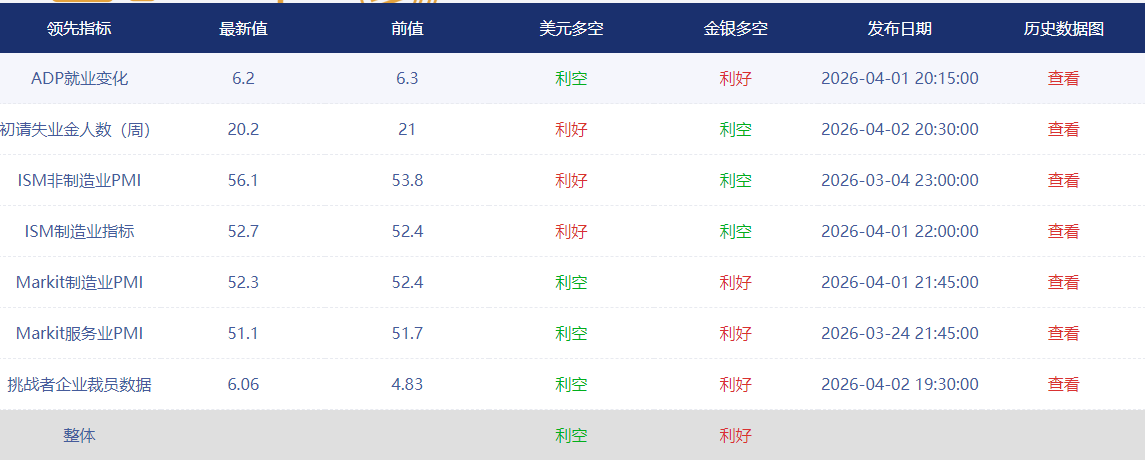

This is compounded by key variables such as the unhealthy reliance on healthcare in the employment structure, the hiring rate falling to a 15-year low, the continued wage-inflation spiral, and significant downward revisions to historical data. Furthermore, the 4.5% unemployment rate is a critical threshold for determining an economic recession under the SAM rule. The overall picture of the data will directly determine the Fed's interest rate path and expectations for a soft landing of the US economy.

First wartime non-farm payrolls report: Delayed impacts of geopolitical conflict become apparent; military-driven growth and energy sector backlash create a tug-of-war between bulls and bears.

Healthcare sector is the sole pillar of the economy: Excluding the healthcare sector, private non-farm payrolls may face substantial negative growth, leading to an extremely unbalanced employment structure.

Hiring rate freezes: The hiring rate of 3.1% is the lowest in 15 years, with companies hoarding labor and employment mobility completely exhausted.

Wage inflation spiral: The bizarre coexistence of low hiring and high wages continues to drive up inflation and locks up the Federal Reserve's room for interest rate cuts.

Historical data has been adjusted to remove inflated figures: a total of 167,000 jobs were revised downwards in January and February, and the negative non-farm payroll growth in February may worsen further.

The Sam Rule's threshold for recession: A 0.5 percentage point increase in the 3-month moving average of the unemployment rate from the low of the previous 12 months triggers a recession signal; 4.5% is the critical threshold.

Meanwhile, the previous non-farm payroll data was as follows:

(Non-farm payroll data comparison chart, source: subsidiary EasyForex)

Here is an in-depth analysis of the key points:

As the first non-farm payroll report following the escalation of tensions in the Middle East, the March data represents the first direct confrontation between geopolitical storms and economic resilience—it is not just a simple employment figure, but a crucial litmus test for predicting future economic trends.

The transmission logic of geopolitical shocks contains a hidden "time lag code": the military and defense manufacturing sectors may release a temporary warming of recruitment by supplementing emergency orders, becoming a "short-term boost" to the employment side; but on the other hand, the cost tsunami caused by soaring oil prices has quietly spread, and transportation, retail, and small and medium-sized manufacturing enterprises are facing the "invisible shackles" of profit squeeze, their willingness to expand has cooled rapidly, and they dare not easily increase recruitment.

It is worth noting that there is a natural "wait-and-see period" in corporate decision-making: companies will not rashly lay off employees in the early stages of a conflict, but will immediately tighten the gates on recruitment, and the real wave of layoffs will most likely be concentrated in April and May.

Therefore, the March non-farm payrolls report will not see extreme scenarios of "wartime surge" or "collapse-like decline." Its core value lies in capturing "early signs of shock"—if industries such as transportation and retail have already experienced employment contraction, it indicates that the economy's ability to withstand risks is weaker than expected; if the military industry's driving effect exceeds expectations and employment on the consumer side stabilizes, it confirms the economy's resilience.

The current US job market is severely structurally unbalanced. March ADP data shows that the healthcare industry contributed 93% of new jobs in the private sector, becoming the "only lifeline" in the job market.

While healthcare jobs are counter-cyclical, when the economic engines—manufacturing, technology, and trade—all stall, relying solely on healthcare to sustain the economy means that job growth has lost its sustainability. Coupled with the return of 30,000 jobs after the end of the Kaiser Permanente strike, this could further embellish the figures and mask the true weakness.

Meanwhile, the hiring rate of 3.1% returned to the 2011 level, hitting a 15-year low.

Businesses did not lay off employees on a large scale, but instead chose to "stockpile labor" due to concerns about staffing. However, they completely stopped expanding recruitment, and the job market fell into a "great standstill".

While the job market remains relatively stable for those already employed, job seekers face the most challenging employment environment in 15 years. The depletion of job mobility is a typical sign of an impending labor market collapse.

Even with a significant slowdown in recruitment activity, average hourly wages in March are still expected to maintain a high growth rate of 3.7%-3.8% year-on-year.

In a high-inflation environment, union wage negotiations and adjustments in the cost of living force rigid wage increases, creating a stagflation pattern of "shrinking employment + high wage growth".

This is the scenario the Federal Reserve fears most: a weakening labor market should support interest rate cuts, but wages are pushing up inflation, leaving the central bank in a policy deadlock where it wants to ease monetary policy but dares not, and the interest rate cut cycle is likely to be further delayed.

The U.S. Bureau of Labor Statistics has been continuously "squeezing out the inflated" employment data recently, with the combined non-farm payrolls figures for December and January revised down by 167,000 jobs. January's new jobs were cut from 353,000 to 229,000, and December's figure was even revised from positive growth to negative growth.

Market confidence in the initial data has decreased significantly. If the March data is strong, but the negative growth of 92,000 in February is further revised downward, it will confirm the conclusion that the US job market has already entered a recession and that statistical models are lagging behind reality.

The SAM rule, proposed by a former Federal Reserve economist, is a highly accurate indicator for predicting economic recessions: when the 3-month moving average of the unemployment rate rises by 0.5 percentage points or more from its 12-month low, it signals that the economy has entered a recession. Currently, the market expects the unemployment rate to remain stable at 4.4%. If the March figure rises to 4.5%, it will trigger recession signals and significantly strengthen the market's pricing in a hard landing for the US economy.

Optimistic Scenario (Goldilocks Market): 50,000-80,000 new jobs, a moderate decline in healthcare employment, a month-on-month wage growth rate of 0.2%, rising expectations of a soft landing for the economy, and stronger risk assets.

Pessimistic scenario (signs of a hard landing): New job creation falls below 30,000 or even turns negative, and February data is significantly revised downwards, coupled with the unemployment rate hitting the 4.5% red line, triggering a full-blown recession trade.

Stagflation scenario (worst-case scenario): sluggish job growth, but wages rise by more than 0.5% month-on-month; the Fed's policy is completely locked down; stocks and bonds suffer a double blow; and the dollar strengthens temporarily.

Key takeaway: Don't be misled by the total number of new jobs; focus on employment performance excluding the healthcare sector. Unless the healthcare sector experiences widespread negative growth, this non-farm payroll report would be confirmation of a US economic recession.

(A summary of leading indicators for non-farm payrolls, sourced from FX678's subsidiary, EasyForex)

On April 3, 2026, Eastern Time, the U.S. Bureau of Labor Statistics will officially release the March non-farm payroll data. The mainstream market expectation is that 60,000 new jobs will be added and the unemployment rate will remain stable at 4.4%.

This non-farm payroll report is the first employment report since the escalation of geopolitical conflicts in the Middle East, and it deserves attention.

This is compounded by key variables such as the unhealthy reliance on healthcare in the employment structure, the hiring rate falling to a 15-year low, the continued wage-inflation spiral, and significant downward revisions to historical data. Furthermore, the 4.5% unemployment rate is a critical threshold for determining an economic recession under the SAM rule. The overall picture of the data will directly determine the Fed's interest rate path and expectations for a soft landing of the US economy.

Key highlights at a glance

First wartime non-farm payrolls report: Delayed impacts of geopolitical conflict become apparent; military-driven growth and energy sector backlash create a tug-of-war between bulls and bears.

Healthcare sector is the sole pillar of the economy: Excluding the healthcare sector, private non-farm payrolls may face substantial negative growth, leading to an extremely unbalanced employment structure.

Hiring rate freezes: The hiring rate of 3.1% is the lowest in 15 years, with companies hoarding labor and employment mobility completely exhausted.

Wage inflation spiral: The bizarre coexistence of low hiring and high wages continues to drive up inflation and locks up the Federal Reserve's room for interest rate cuts.

Historical data has been adjusted to remove inflated figures: a total of 167,000 jobs were revised downwards in January and February, and the negative non-farm payroll growth in February may worsen further.

The Sam Rule's threshold for recession: A 0.5 percentage point increase in the 3-month moving average of the unemployment rate from the low of the previous 12 months triggers a recession signal; 4.5% is the critical threshold.

Meanwhile, the previous non-farm payroll data was as follows:

(Non-farm payroll data comparison chart, source: subsidiary EasyForex)

Here is an in-depth analysis of the key points:

First wartime non-farm payrolls: A lagged game of geopolitical shocks

As the first non-farm payroll report following the escalation of tensions in the Middle East, the March data represents the first direct confrontation between geopolitical storms and economic resilience—it is not just a simple employment figure, but a crucial litmus test for predicting future economic trends.

The transmission logic of geopolitical shocks contains a hidden "time lag code": the military and defense manufacturing sectors may release a temporary warming of recruitment by supplementing emergency orders, becoming a "short-term boost" to the employment side; but on the other hand, the cost tsunami caused by soaring oil prices has quietly spread, and transportation, retail, and small and medium-sized manufacturing enterprises are facing the "invisible shackles" of profit squeeze, their willingness to expand has cooled rapidly, and they dare not easily increase recruitment.

It is worth noting that there is a natural "wait-and-see period" in corporate decision-making: companies will not rashly lay off employees in the early stages of a conflict, but will immediately tighten the gates on recruitment, and the real wave of layoffs will most likely be concentrated in April and May.

Therefore, the March non-farm payrolls report will not see extreme scenarios of "wartime surge" or "collapse-like decline." Its core value lies in capturing "early signs of shock"—if industries such as transportation and retail have already experienced employment contraction, it indicates that the economy's ability to withstand risks is weaker than expected; if the military industry's driving effect exceeds expectations and employment on the consumer side stabilizes, it confirms the economy's resilience.

Healthcare sector alone supports the workforce, recruitment rate freezes: morbid employment structure

The current US job market is severely structurally unbalanced. March ADP data shows that the healthcare industry contributed 93% of new jobs in the private sector, becoming the "only lifeline" in the job market.

While healthcare jobs are counter-cyclical, when the economic engines—manufacturing, technology, and trade—all stall, relying solely on healthcare to sustain the economy means that job growth has lost its sustainability. Coupled with the return of 30,000 jobs after the end of the Kaiser Permanente strike, this could further embellish the figures and mask the true weakness.

Meanwhile, the hiring rate of 3.1% returned to the 2011 level, hitting a 15-year low.

Businesses did not lay off employees on a large scale, but instead chose to "stockpile labor" due to concerns about staffing. However, they completely stopped expanding recruitment, and the job market fell into a "great standstill".

While the job market remains relatively stable for those already employed, job seekers face the most challenging employment environment in 15 years. The depletion of job mobility is a typical sign of an impending labor market collapse.

Wage-Inflation Spiral: Room for Interest Rate Cuts Completely Closed

Even with a significant slowdown in recruitment activity, average hourly wages in March are still expected to maintain a high growth rate of 3.7%-3.8% year-on-year.

In a high-inflation environment, union wage negotiations and adjustments in the cost of living force rigid wage increases, creating a stagflation pattern of "shrinking employment + high wage growth".

This is the scenario the Federal Reserve fears most: a weakening labor market should support interest rate cuts, but wages are pushing up inflation, leaving the central bank in a policy deadlock where it wants to ease monetary policy but dares not, and the interest rate cut cycle is likely to be further delayed.

Historical data revision: The false prosperity at the statistical level has been exposed.

The U.S. Bureau of Labor Statistics has been continuously "squeezing out the inflated" employment data recently, with the combined non-farm payrolls figures for December and January revised down by 167,000 jobs. January's new jobs were cut from 353,000 to 229,000, and December's figure was even revised from positive growth to negative growth.

Market confidence in the initial data has decreased significantly. If the March data is strong, but the negative growth of 92,000 in February is further revised downward, it will confirm the conclusion that the US job market has already entered a recession and that statistical models are lagging behind reality.

Sam's Rule: 4.5% unemployment rate is the threshold for recession survival.

The SAM rule, proposed by a former Federal Reserve economist, is a highly accurate indicator for predicting economic recessions: when the 3-month moving average of the unemployment rate rises by 0.5 percentage points or more from its 12-month low, it signals that the economy has entered a recession. Currently, the market expects the unemployment rate to remain stable at 4.4%. If the March figure rises to 4.5%, it will trigger recession signals and significantly strengthen the market's pricing in a hard landing for the US economy.

Data Scenario and Market Interpretation

Optimistic Scenario (Goldilocks Market): 50,000-80,000 new jobs, a moderate decline in healthcare employment, a month-on-month wage growth rate of 0.2%, rising expectations of a soft landing for the economy, and stronger risk assets.

Pessimistic scenario (signs of a hard landing): New job creation falls below 30,000 or even turns negative, and February data is significantly revised downwards, coupled with the unemployment rate hitting the 4.5% red line, triggering a full-blown recession trade.

Stagflation scenario (worst-case scenario): sluggish job growth, but wages rise by more than 0.5% month-on-month; the Fed's policy is completely locked down; stocks and bonds suffer a double blow; and the dollar strengthens temporarily.

Key takeaway: Don't be misled by the total number of new jobs; focus on employment performance excluding the healthcare sector. Unless the healthcare sector experiences widespread negative growth, this non-farm payroll report would be confirmation of a US economic recession.

(A summary of leading indicators for non-farm payrolls, sourced from FX678's subsidiary, EasyForex)

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.