One chart: The Baltic Dry Index rises to a more than one-month high, with all sectors rising.

2026-04-10 02:10:08

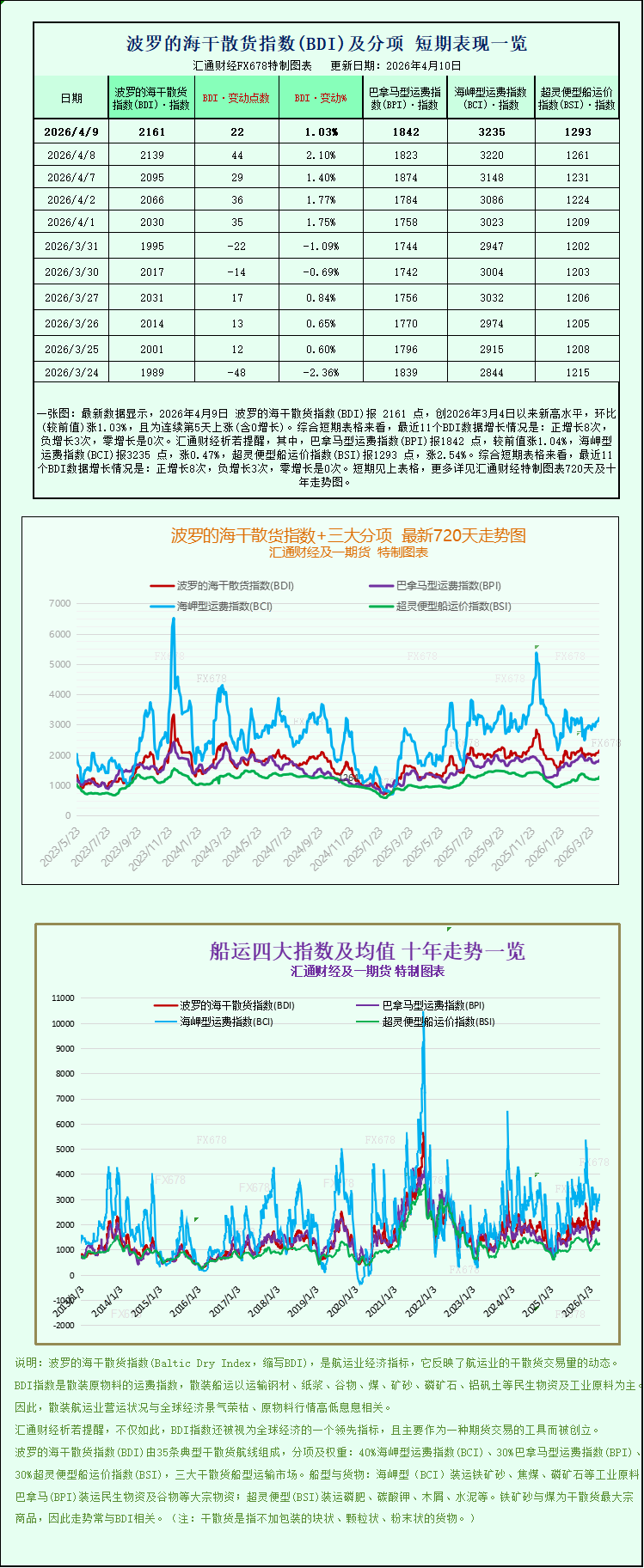

The latest data shows that the Baltic Dry Index (BDI) reached 2161 points on April 9, 2026, a new high since March 4, 2026, up 1.03% month-on-month, marking the fifth consecutive day of increase (including zero growth). Looking at the short-term charts, the recent 11 BDI data points show: 8 positive increases, 3 negative increases, and 0 zero increases. Specifically, the Panamax Freight Index (BPI) reached 1842 points, up 1.04% from the previous value; the Capesize Freight Index (BCI) reached 3235 points, up 0.47%; and the Supramax Freight Index (BSI) reached 1293 points, up 2.54%. For detailed 720-day and 10-year trend charts of the Baltic Dry Index and its three main sub-indices, please refer to the specially designed charts.

The Baltic Dry Index (BDI) released by the London Baltic Exchange saw a significant surge on Thursday, breaking through its previous trading range and reaching its highest level since March 5th. This marks the first time in over a month that all sectors of the index have risen simultaneously, highlighting a phase of recovery in the global dry bulk shipping market. As a core indicator of the global dry bulk shipping market, the index directly monitors fluctuations in freight rates for ships transporting dry bulk commodities such as iron ore, coal, grain, and bauxite worldwide. Its trends closely reflect the activity of global commodity trade and the supply and demand dynamics of the shipping market. This comprehensive increase is seen by the industry as an important signal of the dry bulk market's recovery.

Specifically, the Baltic Dry Index, which tracks freight rates for the world's three major dry bulk carrier types—Capesize, Panamax, and Supramax—performed strongly, rising 22 points, or 1%, to close at 2161 points, precisely hitting its peak since March 5th. While this increase wasn't dramatic, considering the recent market volatility, it reflects the dual support of a steady recovery in dry bulk shipping demand and a temporary tightness in shipping capacity. This broke the previous stalemate between bulls and bears and confirmed the market's cautiously optimistic expectations for the dry bulk trade outlook.

Among the various vessel types, the Capesize vessel index, a "juggernaut" in dry bulk shipping, performed steadily. Specifically, the Capesize index rose 15 points, or approximately 0.5%, to close at 3235 points, also reaching its highest point in over a month, continuing its recent upward trend. The average daily revenue of Capesize vessels also climbed, increasing by $133 to $25,835. These vessels primarily handle the long-distance transport of 150,000-tonnage bulk commodities, with core cargoes including basic industrial raw materials such as iron ore and coal. The increase in freight rates and revenue is mainly attributed to a surge in demand on the West Africa-China route—China's continued increase in imports of bauxite and iron ore from Guinea and other West African countries has driven up demand for Capesize vessel capacity. Simultaneously, loading delays at Guinean ports have also tied up some capacity, further pushing up freight rates.

It is worth noting that, in stark contrast to the recovery in demand for Capesize shipping, global iron ore prices declined significantly on the same day. Driven by increased global iron ore supply and concerns about the demand outlook in the world's largest iron ore consumer due to persistently low profit margins of Chinese steel companies, iron ore prices fell to their lowest point in over a month. According to data from the Dalian Commodity Exchange, iron ore futures contract prices have been under continuous pressure recently, remaining at low levels for several days since April. While this trend represents a short-term divergence from the rise in Capesize shipping rates, it also reflects the structural differentiation within the dry bulk market, where the transportation demand for different types of cargo exhibits varying characteristics due to industry cycles.

Besides Capesize vessels, the Panamax sector also saw steady growth, becoming a significant driver of the overall index's rise. The Panamax index rose 19 points, or about 1%, to close at 1842 points, continuing the upward trend since early April. The corresponding average daily earnings for Panamax vessels increased by $173 to $16,582. These vessels, with a deadweight between Capesize and Supramax, typically carry 60,000 to 70,000 tons of commodities such as coal or grain. The increase in freight rates mainly benefited from the seasonal recovery in global grain trade and the steady release of demand for coal transportation, especially the increased activity on the South America-China soybean shipping route, providing stable demand support for Panamax vessels.

Among the three major ship types, the Very Large Bulk Carrier (VLCC) sector performed the best, becoming the sub-sector with the highest increase on the day. The VLCC index rose 32 points, or 2.5%, to close at 1293 points, significantly higher than the Capesize and Panamax ship indices. These vessels, with their flexible route adaptability, mainly undertake small-volume dry bulk cargo transportation tasks, covering a variety of industrial raw materials and agricultural products. Their significant increase reflects a substantial increase in the activity of global small- and medium-volume dry bulk trade. Industry analysts point out that the recent general rise in second-hand Supramax ship prices and the shift in market demand towards older vessels have further supported the stable upward trend in freight rates for this ship type. At the same time, the seasonal growth in global agricultural trade has also provided additional demand momentum.

From an overall market perspective, the recent surge in the Baltic Dry Index across all sectors directly reflects the phased recovery in global dry bulk shipping demand and is closely related to changes in the current global dry bulk trade landscape. With the steady recovery of China's logistics industry, the China Logistics Industry Prosperity Index rebounded to 50.2% in March. The orderly resumption of work and production across the supply chain and upstream and downstream sectors of logistics demand has provided stable support for dry bulk import demand. Meanwhile, the rise of West African bauxite and iron ore trade is reshaping global dry bulk shipping flows. Increased resource exports from West African countries such as Guinea have driven up demand for large dry bulk vessels, injecting long-term momentum into freight rate increases.

However, industry analysts also caution that the dry bulk market still faces multiple uncertainties. On the one hand, the profit margins of Chinese steel companies are narrow, and their profits are expected to remain weak in April, potentially suppressing import demand for dry bulk commodities such as iron ore. On the other hand, global geopolitical uncertainties and increased fuel costs due to rising oil prices may also constrain dry bulk freight rates. Nevertheless, the recovery trend in the dry bulk market is expected to continue in the short term, especially with the sustained release of demand for resource transportation from West Africa, which is likely to further support the Baltic Dry Index remaining at a high level.

The Baltic Dry Index (BDI) released by the London Baltic Exchange saw a significant surge on Thursday, breaking through its previous trading range and reaching its highest level since March 5th. This marks the first time in over a month that all sectors of the index have risen simultaneously, highlighting a phase of recovery in the global dry bulk shipping market. As a core indicator of the global dry bulk shipping market, the index directly monitors fluctuations in freight rates for ships transporting dry bulk commodities such as iron ore, coal, grain, and bauxite worldwide. Its trends closely reflect the activity of global commodity trade and the supply and demand dynamics of the shipping market. This comprehensive increase is seen by the industry as an important signal of the dry bulk market's recovery.

Specifically, the Baltic Dry Index, which tracks freight rates for the world's three major dry bulk carrier types—Capesize, Panamax, and Supramax—performed strongly, rising 22 points, or 1%, to close at 2161 points, precisely hitting its peak since March 5th. While this increase wasn't dramatic, considering the recent market volatility, it reflects the dual support of a steady recovery in dry bulk shipping demand and a temporary tightness in shipping capacity. This broke the previous stalemate between bulls and bears and confirmed the market's cautiously optimistic expectations for the dry bulk trade outlook.

Among the various vessel types, the Capesize vessel index, a "juggernaut" in dry bulk shipping, performed steadily. Specifically, the Capesize index rose 15 points, or approximately 0.5%, to close at 3235 points, also reaching its highest point in over a month, continuing its recent upward trend. The average daily revenue of Capesize vessels also climbed, increasing by $133 to $25,835. These vessels primarily handle the long-distance transport of 150,000-tonnage bulk commodities, with core cargoes including basic industrial raw materials such as iron ore and coal. The increase in freight rates and revenue is mainly attributed to a surge in demand on the West Africa-China route—China's continued increase in imports of bauxite and iron ore from Guinea and other West African countries has driven up demand for Capesize vessel capacity. Simultaneously, loading delays at Guinean ports have also tied up some capacity, further pushing up freight rates.

It is worth noting that, in stark contrast to the recovery in demand for Capesize shipping, global iron ore prices declined significantly on the same day. Driven by increased global iron ore supply and concerns about the demand outlook in the world's largest iron ore consumer due to persistently low profit margins of Chinese steel companies, iron ore prices fell to their lowest point in over a month. According to data from the Dalian Commodity Exchange, iron ore futures contract prices have been under continuous pressure recently, remaining at low levels for several days since April. While this trend represents a short-term divergence from the rise in Capesize shipping rates, it also reflects the structural differentiation within the dry bulk market, where the transportation demand for different types of cargo exhibits varying characteristics due to industry cycles.

Besides Capesize vessels, the Panamax sector also saw steady growth, becoming a significant driver of the overall index's rise. The Panamax index rose 19 points, or about 1%, to close at 1842 points, continuing the upward trend since early April. The corresponding average daily earnings for Panamax vessels increased by $173 to $16,582. These vessels, with a deadweight between Capesize and Supramax, typically carry 60,000 to 70,000 tons of commodities such as coal or grain. The increase in freight rates mainly benefited from the seasonal recovery in global grain trade and the steady release of demand for coal transportation, especially the increased activity on the South America-China soybean shipping route, providing stable demand support for Panamax vessels.

Among the three major ship types, the Very Large Bulk Carrier (VLCC) sector performed the best, becoming the sub-sector with the highest increase on the day. The VLCC index rose 32 points, or 2.5%, to close at 1293 points, significantly higher than the Capesize and Panamax ship indices. These vessels, with their flexible route adaptability, mainly undertake small-volume dry bulk cargo transportation tasks, covering a variety of industrial raw materials and agricultural products. Their significant increase reflects a substantial increase in the activity of global small- and medium-volume dry bulk trade. Industry analysts point out that the recent general rise in second-hand Supramax ship prices and the shift in market demand towards older vessels have further supported the stable upward trend in freight rates for this ship type. At the same time, the seasonal growth in global agricultural trade has also provided additional demand momentum.

From an overall market perspective, the recent surge in the Baltic Dry Index across all sectors directly reflects the phased recovery in global dry bulk shipping demand and is closely related to changes in the current global dry bulk trade landscape. With the steady recovery of China's logistics industry, the China Logistics Industry Prosperity Index rebounded to 50.2% in March. The orderly resumption of work and production across the supply chain and upstream and downstream sectors of logistics demand has provided stable support for dry bulk import demand. Meanwhile, the rise of West African bauxite and iron ore trade is reshaping global dry bulk shipping flows. Increased resource exports from West African countries such as Guinea have driven up demand for large dry bulk vessels, injecting long-term momentum into freight rate increases.

However, industry analysts also caution that the dry bulk market still faces multiple uncertainties. On the one hand, the profit margins of Chinese steel companies are narrow, and their profits are expected to remain weak in April, potentially suppressing import demand for dry bulk commodities such as iron ore. On the other hand, global geopolitical uncertainties and increased fuel costs due to rising oil prices may also constrain dry bulk freight rates. Nevertheless, the recovery trend in the dry bulk market is expected to continue in the short term, especially with the sustained release of demand for resource transportation from West Africa, which is likely to further support the Baltic Dry Index remaining at a high level.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.