UK GDP unexpectedly rose 0.5% in February and March, exceeding expectations, and the pound continued its rebound against the dollar.

2026-04-16 15:28:47

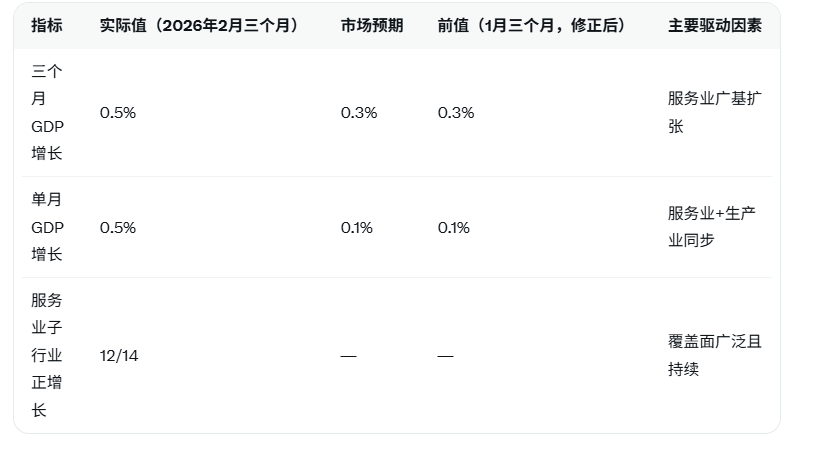

According to APP, market analysts say that UK GDP grew by 0.5% in the three months of February, better than the market consensus of 0.3%, thanks to better-than-expected service sector output data. The service sector is currently performing more optimistically, with output growing for the fourth consecutive month. The good news is that this growth is more widespread, with 12 out of 14 sub-sectors showing positive activity. Overall, the UK economy was performing relatively well before the outbreak of the conflict between the US and Iran. However, because the war will inevitably have an impact, these figures are lagging data and will not have any substantial impact on the economic outlook at present.

Market analysts further pointed out that the GDP data reflects the UK economy had already accumulated some momentum before the conflict. The service sector, as the core engine of the economy, not only saw positive growth for four consecutive months, but also experienced simultaneous expansion across 12 sub-sectors, indicating a relatively solid foundation for domestic demand recovery. The manufacturing and construction sectors also contributed some support, demonstrating an overall economic resilience that exceeded expectations before the external shocks. However, analysts emphasized that these data are essentially "lagging indicators" and cannot capture in real time new variables such as energy price fluctuations, supply chain disruptions, and declining confidence after the outbreak of war. Therefore, their reference value for current policy-making and market expectations is limited.

The latest precise data released by the UK Office for National Statistics (ONS) on April 16, 2026, shows that GDP grew by 0.5% month-on-month in the three months of February, a significant acceleration compared to the revised 0.3% growth in the three months of January; the 0.5% monthly GDP growth also significantly exceeded expectations. The service sector saw a 0.5% increase in output, becoming the main driver, with only two of the 14 sub-sectors contracting, while the remaining 12 recorded positive growth, marking a recent high in the breadth of growth. This contrasts sharply with previous market concerns about an economic slowdown, highlighting the inherent dynamism of the UK economy in terms of consumption and service demand before the conflict.

The table below provides a visual comparison of key GDP indicators to help understand the extent to which the data exceeded expectations:

At a deeper level, despite the strong economic data before the conflict, the rising energy costs and global uncertainty caused by the war have begun to spill over into subsequent months. Analysts believe that while current data provides policymakers with a short-term buffer, it is unlikely to change the downward pressure on the medium- to long-term outlook. The Bank of England will need to weigh lagged data against the immediate shock at its next meeting and carefully assess whether to maintain the current interest rate path.

Editor's Summary : The UK's better-than-expected 0.5% GDP growth in the first three months of February, coupled with broad-based positive performance in the 12/14 sub-sectors of the services sector, clearly demonstrates the inherent resilience of the economy before the conflict. However, as lagging data, its substantive impact on the current outlook is limited; subsequent variables triggered by the geopolitical conflict will become the dominant factor. Investors should closely monitor the latest monthly data and central bank communications, and proactively position themselves for market opportunities arising from energy price volatility and the recovery of confidence.

Market analysts further pointed out that the GDP data reflects the UK economy had already accumulated some momentum before the conflict. The service sector, as the core engine of the economy, not only saw positive growth for four consecutive months, but also experienced simultaneous expansion across 12 sub-sectors, indicating a relatively solid foundation for domestic demand recovery. The manufacturing and construction sectors also contributed some support, demonstrating an overall economic resilience that exceeded expectations before the external shocks. However, analysts emphasized that these data are essentially "lagging indicators" and cannot capture in real time new variables such as energy price fluctuations, supply chain disruptions, and declining confidence after the outbreak of war. Therefore, their reference value for current policy-making and market expectations is limited.

The latest precise data released by the UK Office for National Statistics (ONS) on April 16, 2026, shows that GDP grew by 0.5% month-on-month in the three months of February, a significant acceleration compared to the revised 0.3% growth in the three months of January; the 0.5% monthly GDP growth also significantly exceeded expectations. The service sector saw a 0.5% increase in output, becoming the main driver, with only two of the 14 sub-sectors contracting, while the remaining 12 recorded positive growth, marking a recent high in the breadth of growth. This contrasts sharply with previous market concerns about an economic slowdown, highlighting the inherent dynamism of the UK economy in terms of consumption and service demand before the conflict.

The table below provides a visual comparison of key GDP indicators to help understand the extent to which the data exceeded expectations:

At a deeper level, despite the strong economic data before the conflict, the rising energy costs and global uncertainty caused by the war have begun to spill over into subsequent months. Analysts believe that while current data provides policymakers with a short-term buffer, it is unlikely to change the downward pressure on the medium- to long-term outlook. The Bank of England will need to weigh lagged data against the immediate shock at its next meeting and carefully assess whether to maintain the current interest rate path.

Editor's Summary : The UK's better-than-expected 0.5% GDP growth in the first three months of February, coupled with broad-based positive performance in the 12/14 sub-sectors of the services sector, clearly demonstrates the inherent resilience of the economy before the conflict. However, as lagging data, its substantive impact on the current outlook is limited; subsequent variables triggered by the geopolitical conflict will become the dominant factor. Investors should closely monitor the latest monthly data and central bank communications, and proactively position themselves for market opportunities arising from energy price volatility and the recovery of confidence.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.