The decisive battle at dawn! A breakdown of the three-tier market trend.

2026-04-29 20:34:18

On Wednesday, April 29th, before the US market opened, the Federal Reserve's monetary policy meeting entered a crucial phase, with traders closely watching Fed Chairman Jerome Powell's press conference early Thursday morning. Previously, stock index futures trading volume had rebounded significantly, but open interest remained relatively stable, reflecting that traders were actively adjusting positions rather than establishing new directional bets. Meanwhile, the geopolitical situation in the Middle East remained deadlocked, causing oil prices to continue climbing into triple-digit ranges, and the risk of supply disruptions pushed up global inflationary pressures. Against this backdrop, the US dollar exhibited its safe-haven characteristics, non-US currencies generally declined, and prices of precious metals such as gold saw a correction.

The latest CME stock index futures data shows that trading volume rebounded sharply on April 28 to 5.92 million contracts, an increase of approximately 25% from the previous trading day's 4.72 million contracts. However, open interest has remained stable at around 5.27 million to 5.31 million contracts over the past few trading sessions. This divergence between volume and open interest has a clear signal for traders: trading volume reflects the actual trading size of the day, while open interest reflects the number of open contracts across different maturities. When trading volume jumps but open interest does not expand significantly in tandem, it usually indicates that the market is mainly engaged in hedging operations and rollovers, rather than injecting new large-scale long or short directional bets.

In the current environment, this dynamic indicates that traders remain highly vigilant about rising energy costs driven by geopolitical factors, but have not yet collectively shifted to a clearly bullish or bearish stance. On the eve of the Federal Reserve policy meeting, this "busy but restrained" trading behavior further reinforces the market's wait-and-see attitude, as investors weigh labor data against rising energy prices to avoid locking in positions prematurely. Similar signals are frequently seen during periods of high volatility, often indicating that subsequent policy communication will be a key catalyst for directional price movements.

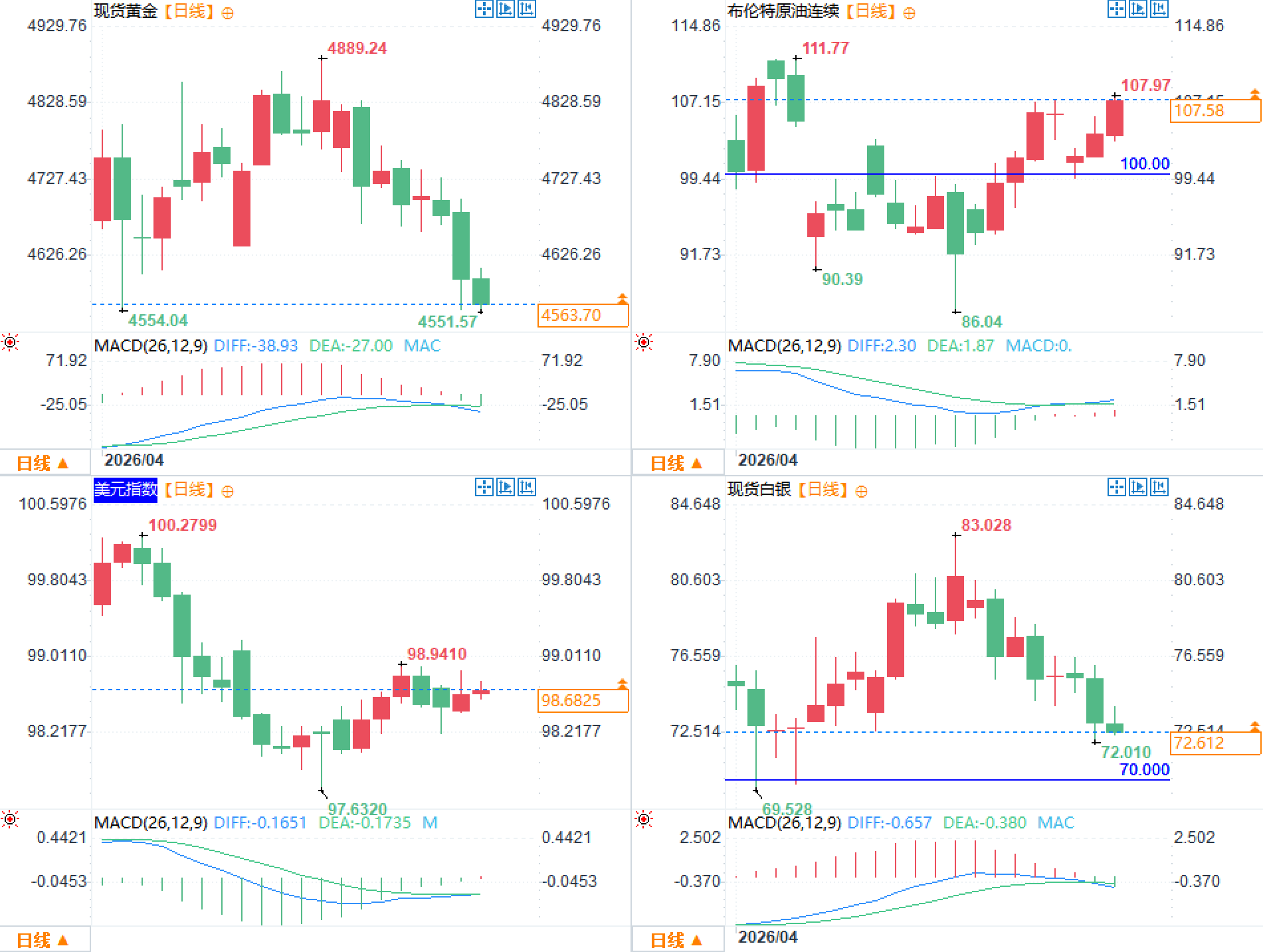

The crude oil market has become the core driver of this round of events. Brent crude oil futures for June delivery rose 3% to $114.59 per barrel, a near one-month high, while the more active July contract rose to $107.43 per barrel; West Texas Intermediate crude oil futures for June delivery rose 3.6% to $103.48 per barrel. This price trend has continued for several days, and the risk of supply disruptions has directly amplified inflation expectations, especially in the areas monitored by the European Central Bank, where consumer confidence has fallen to its lowest point since 2020.

The Federal Reserve is expected to keep interest rates unchanged at this meeting, but Powell needs to provide a neutral assessment of the impact of energy prices on the economy, leaving policy space for his successor. Analysts point out that if supply disruptions persist, inflationary pressures will further solidify the narrative of "higher interest rates for longer"; recent oil price increases have been mainly driven by shipping lane congestion, and if related pressures continue, supply disruptions will worsen and continue to support higher oil prices. This assessment aligns with market consensus: rising energy costs are eroding central bank flexibility, forcing policymakers to prioritize addressing persistent inflation rather than short-term growth fluctuations.

Against this backdrop, the Federal Reserve faces a classic supply-shock dilemma—the labor market remains resilient, but energy-imported inflation has begun to transmit to broader price indices. Traders are focusing on whether Powell hints at the possibility of further tightening this year to determine the anchor for subsequent asset pricing.

The dollar index strengthened moderately, driven by safe-haven demand, while the euro fell 0.1% against the dollar to 1.1701, and the pound also declined 0.1% to 1.3509. The yen hovered below the 160 level, depreciating 0.6% on the day, bringing its cumulative decline to over 2% since escalating geopolitical tensions. The Bank of Japan's previous meeting had hinted at a possible interest rate hike in the coming months, but inflationary pressures from energy imports continued to weigh on the yen. Market data showed that investors' short positions in the yen were at their highest level since July 2024.

As a non-yielding asset, gold's appeal has diminished in a high-interest-rate environment, with spot prices falling 0.6% to $4,567.56 per ounce, and the June contract for US gold futures also declining to $4,580.80 per ounce. Data from the World Gold Council shows that global gold demand rose 2% year-on-year in the first quarter of 2026, with strong growth in gold bar and coin purchases and central bank gold buying offsetting a 23% decline in jewelry demand. However, persistent inflation expectations driven by oil prices are exacerbating uncertainty about the interest rate path, further suppressing gold's short-term performance. OANDA analyst Zain Wafda points out that market sentiment has shifted towards skepticism about potential agreements, reinforcing the high-interest-rate narrative; if geopolitical tensions ease quickly, gold bulls may return to the market.

Spot silver fell 0.2% to $72.92 per ounce, platinum declined 0.8% to $1,924.61 per ounce, and palladium dropped 0.7% to $1,450.46 per ounce. The overall precious metals sector showed divergence, highlighting traders' delicate balancing act between energy inflation and policy expectations.

The rebound in stock index futures trading volume and the stability of open interest highlight position adjustments.

The latest CME stock index futures data shows that trading volume rebounded sharply on April 28 to 5.92 million contracts, an increase of approximately 25% from the previous trading day's 4.72 million contracts. However, open interest has remained stable at around 5.27 million to 5.31 million contracts over the past few trading sessions. This divergence between volume and open interest has a clear signal for traders: trading volume reflects the actual trading size of the day, while open interest reflects the number of open contracts across different maturities. When trading volume jumps but open interest does not expand significantly in tandem, it usually indicates that the market is mainly engaged in hedging operations and rollovers, rather than injecting new large-scale long or short directional bets.

In the current environment, this dynamic indicates that traders remain highly vigilant about rising energy costs driven by geopolitical factors, but have not yet collectively shifted to a clearly bullish or bearish stance. On the eve of the Federal Reserve policy meeting, this "busy but restrained" trading behavior further reinforces the market's wait-and-see attitude, as investors weigh labor data against rising energy prices to avoid locking in positions prematurely. Similar signals are frequently seen during periods of high volatility, often indicating that subsequent policy communication will be a key catalyst for directional price movements.

The continued rise in oil prices has reinforced expectations of high interest rates from the Federal Reserve.

The crude oil market has become the core driver of this round of events. Brent crude oil futures for June delivery rose 3% to $114.59 per barrel, a near one-month high, while the more active July contract rose to $107.43 per barrel; West Texas Intermediate crude oil futures for June delivery rose 3.6% to $103.48 per barrel. This price trend has continued for several days, and the risk of supply disruptions has directly amplified inflation expectations, especially in the areas monitored by the European Central Bank, where consumer confidence has fallen to its lowest point since 2020.

The Federal Reserve is expected to keep interest rates unchanged at this meeting, but Powell needs to provide a neutral assessment of the impact of energy prices on the economy, leaving policy space for his successor. Analysts point out that if supply disruptions persist, inflationary pressures will further solidify the narrative of "higher interest rates for longer"; recent oil price increases have been mainly driven by shipping lane congestion, and if related pressures continue, supply disruptions will worsen and continue to support higher oil prices. This assessment aligns with market consensus: rising energy costs are eroding central bank flexibility, forcing policymakers to prioritize addressing persistent inflation rather than short-term growth fluctuations.

Against this backdrop, the Federal Reserve faces a classic supply-shock dilemma—the labor market remains resilient, but energy-imported inflation has begun to transmit to broader price indices. Traders are focusing on whether Powell hints at the possibility of further tightening this year to determine the anchor for subsequent asset pricing.

The correlation between exchange rates and the precious metals market has diverged.

The dollar index strengthened moderately, driven by safe-haven demand, while the euro fell 0.1% against the dollar to 1.1701, and the pound also declined 0.1% to 1.3509. The yen hovered below the 160 level, depreciating 0.6% on the day, bringing its cumulative decline to over 2% since escalating geopolitical tensions. The Bank of Japan's previous meeting had hinted at a possible interest rate hike in the coming months, but inflationary pressures from energy imports continued to weigh on the yen. Market data showed that investors' short positions in the yen were at their highest level since July 2024.

As a non-yielding asset, gold's appeal has diminished in a high-interest-rate environment, with spot prices falling 0.6% to $4,567.56 per ounce, and the June contract for US gold futures also declining to $4,580.80 per ounce. Data from the World Gold Council shows that global gold demand rose 2% year-on-year in the first quarter of 2026, with strong growth in gold bar and coin purchases and central bank gold buying offsetting a 23% decline in jewelry demand. However, persistent inflation expectations driven by oil prices are exacerbating uncertainty about the interest rate path, further suppressing gold's short-term performance. OANDA analyst Zain Wafda points out that market sentiment has shifted towards skepticism about potential agreements, reinforcing the high-interest-rate narrative; if geopolitical tensions ease quickly, gold bulls may return to the market.

Spot silver fell 0.2% to $72.92 per ounce, platinum declined 0.8% to $1,924.61 per ounce, and palladium dropped 0.7% to $1,450.46 per ounce. The overall precious metals sector showed divergence, highlighting traders' delicate balancing act between energy inflation and policy expectations.

Frequently Asked Questions

Question 1: The sharp rebound in stock index futures trading volume but the stable open interest indicates what kind of market sentiment?

A: This combination of signals indicates increased trader activity, primarily driven by hedging, rollovers, and short-term position adjustments, rather than a collective establishment of new directional bets. The lack of expansion in open interest suggests that the market has not yet formed a consensus of bullish or bearish views, reflecting a cautious wait-and-see attitude amid the combined effects of Fed decisions and geopolitical supply risks.

Question 2: What substantive impact will the return of oil prices to triple digits have on the Fed's interest rate path?

A: Supply disruptions drive up energy costs, directly raising inflation expectations and potentially forcing the Federal Reserve to maintain current interest rates to observe data developments. Powell's press conference will be the focus, as his statements will determine the strength of the market's pricing in the "higher interest rates for longer" narrative, while also leaving room for flexibility in subsequent policy and avoiding premature commitments to a shift.

Question 3: What is the unique significance of Powell's last press conference during his tenure?

A: The market is not only focused on this interest rate decision, but also on its assessment of the economic impact of geopolitical factors, and the potential policy continuity signals from Powell's future role. Some analysts point out that Powell will continue to serve as a governor until 2028, and his statements may hint at whether he retains influence. The high-interest-rate environment has clearly suppressed assets such as gold, and the press conference will be a key window to verify the trade-off between inflation and growth.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.