One chart: Baltic Dry Index strengthens, with major vessel types leading the weekly gains.

2026-05-02 00:32:19

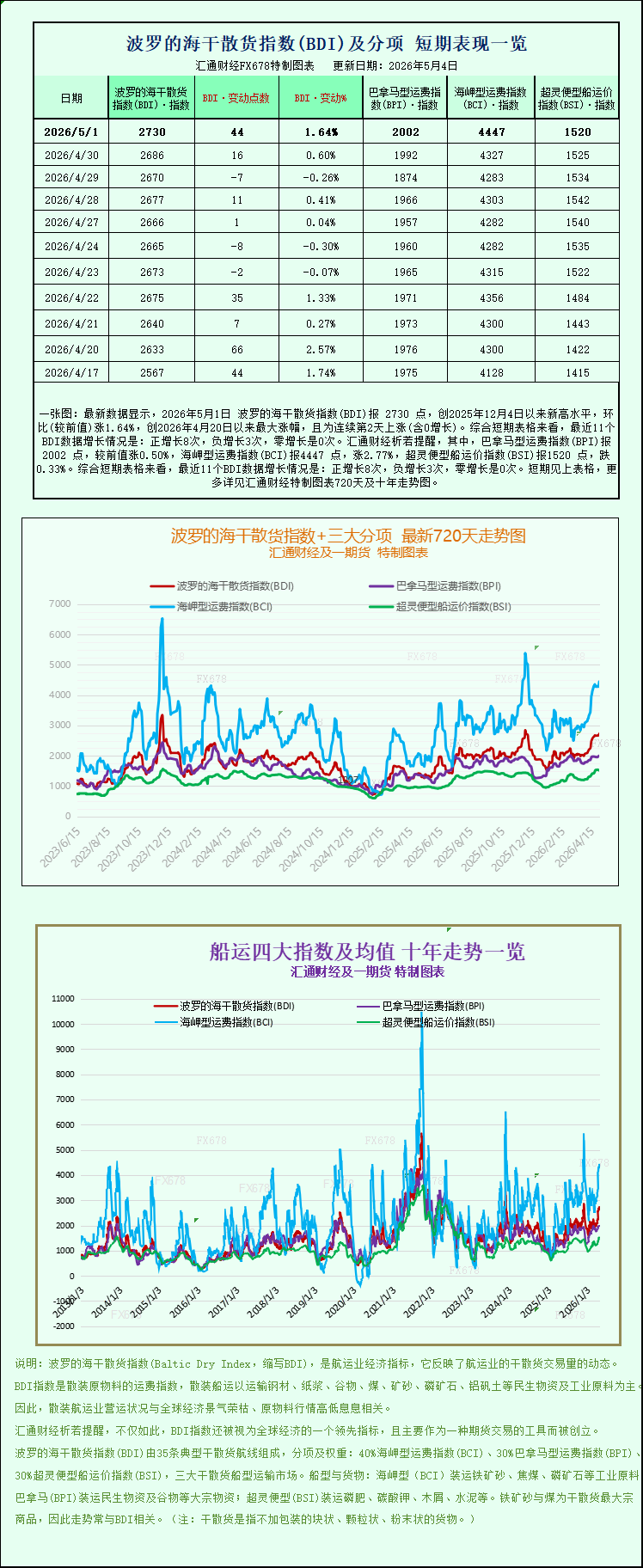

Latest data shows that the Baltic Dry Index (BDI) reached 2730 points on May 1, 2026, a new high since December 4, 2025, up 1.64% month-on-month, the largest increase since April 20, 2026, and marking the second consecutive day of increase (including zero growth). Looking at the short-term charts, the recent 11 BDI data points show: 8 positive increases, 3 negative increases, and 0 zero increases. Specifically, the Panamax Freight Index (BPI) was 2002 points, up 0.50% from the previous value; the Capesize Freight Index (BCI) was 4447 points, up 2.77%; and the Supramax Freight Index (BSI) was 1520 points, down 0.33%. For detailed 720-day and 10-year trend charts of the Baltic Dry Index and its three main sub-indices, please refer to the specially designed charts.

The Baltic Dry Index (BDI), which monitors freight rates for various vessels transporting dry bulk commodities such as iron ore, coal, and grain globally in real time and is a key indicator of the global dry bulk shipping market's health, closed higher on Friday and has continued its upward trend this week. This positive performance is mainly attributed to the simultaneous rise in the two major vessel sectors, Capesize and Panamax, which effectively offset the slight downward pressure from the smaller vessel sector, driving a moderate recovery in the overall market.

Specifically, the Baltic Dry Index, which tracks freight rates for the three major dry bulk shipping types—Capesize, Panamax, and Supramax—rose 44 points, or 1.6%, to close at 2730 points. On a weekly basis, the index rose 2.4%, continuing its upward trend since the end of April and reaching a high point not seen since December 2025, highlighting a moderate recovery in overall demand in the global dry bulk shipping market.

As the "giant" of the dry bulk shipping market, the Capesize sector performed particularly well, becoming the core force driving the overall index up. On that day, the Capesize index surged 120 points, a gain of 2.8%, closing at 4447 points, maintaining an upward trend for several consecutive trading days. From a weekly perspective, the index rose 3.9% cumulatively this week, significantly higher than the overall index, demonstrating a strong recovery momentum. Capesize vessels primarily undertake transoceanic transportation of large dry bulk cargoes, typically with a carrying capacity of around 150,000 tons. Their core transported cargoes include basic industrial raw materials such as iron ore and coal, serving as a crucial guarantee for the smooth operation of the global industrial supply chain.

Matching the index's rise, Capesize vessel freight revenue also increased significantly. Data shows that the average daily revenue of Capesize vessels carrying 150,000 tons of cargo (mainly covering core industrial raw materials such as iron ore and coal) increased by $1,087 that day, ultimately reaching $36,828. This increase in revenue directly reflects the increased global demand for large dry bulk shipping, especially the recovery in demand for industrial raw material transportation. This, coupled with the capacity constraints caused by longer shipping distances, has provided clear support for the Capesize vessel sector.

Besides the Capesize sector, the Panamax sector also showed a steady upward trend, further consolidating the overall index's upward momentum. The Panamax index rose 10 points, or 0.5%, to close at 2002 points, continuing its recent moderate upward trend; this week, the index has risen a cumulative 2.1%, demonstrating solid performance. Panamax vessels are built to meet the size restrictions for passage through the Panama Canal. Their carrying capacity falls between Capesize and Supramax, typically carrying 60,000 to 70,000 tons of cargo. Core cargo categories include coal and grain, making them important carriers for inter-regional dry bulk shipping.

Along with the rise in the Panamax index, freight revenue also increased accordingly. Data shows that the average daily revenue of Panamax vessels (typically carrying 60,000 to 70,000 tons of coal or grain) increased by $88 to $18,018. This growth was mainly due to a steady increase in global demand for the transportation of agricultural products such as grain and coal, as well as energy-related dry bulk cargoes, particularly increased inter-regional transportation activity. This, coupled with capacity constraints caused by detours on some routes, provided stable demand support for the Panamax sector.

It's worth noting that while the two major shipping sectors saw strong gains, the small vessel sector experienced a slight decline, failing to follow the overall market trend. Within the small vessel sector, the Very Large Bulk Carrier (VLCC) index fell 5 points, a 0.3% drop, closing at 1520 points. Looking at weekly performance, the index has seen a cumulative decline of approximately 1% this week. Analysts believe that small vessels primarily handle dry bulk cargo transportation in near-sea or coastal areas, and their performance is more influenced by regional market supply and demand. This slight decline may be related to short-term fluctuations in transportation demand and relatively ample capacity supply in some regions, but the overall decline is limited and has not had a significant impact on the overall market.

Overall, the rise in the Baltic Dry Index this week was mainly supported by demand from the two main vessel types, Capesize and Panamax, reflecting a moderate recovery in global dry bulk trade, particularly a rebound in demand for industrial raw materials and agricultural products, as well as the combined effects of route detours and capacity constraints. Looking ahead, as global commodity trade progresses, changes in the flow of key shipping routes and the supply and demand dynamics of various vessel types will continue to influence the Baltic Dry Index's trajectory.

The Baltic Dry Index (BDI), which monitors freight rates for various vessels transporting dry bulk commodities such as iron ore, coal, and grain globally in real time and is a key indicator of the global dry bulk shipping market's health, closed higher on Friday and has continued its upward trend this week. This positive performance is mainly attributed to the simultaneous rise in the two major vessel sectors, Capesize and Panamax, which effectively offset the slight downward pressure from the smaller vessel sector, driving a moderate recovery in the overall market.

Specifically, the Baltic Dry Index, which tracks freight rates for the three major dry bulk shipping types—Capesize, Panamax, and Supramax—rose 44 points, or 1.6%, to close at 2730 points. On a weekly basis, the index rose 2.4%, continuing its upward trend since the end of April and reaching a high point not seen since December 2025, highlighting a moderate recovery in overall demand in the global dry bulk shipping market.

As the "giant" of the dry bulk shipping market, the Capesize sector performed particularly well, becoming the core force driving the overall index up. On that day, the Capesize index surged 120 points, a gain of 2.8%, closing at 4447 points, maintaining an upward trend for several consecutive trading days. From a weekly perspective, the index rose 3.9% cumulatively this week, significantly higher than the overall index, demonstrating a strong recovery momentum. Capesize vessels primarily undertake transoceanic transportation of large dry bulk cargoes, typically with a carrying capacity of around 150,000 tons. Their core transported cargoes include basic industrial raw materials such as iron ore and coal, serving as a crucial guarantee for the smooth operation of the global industrial supply chain.

Matching the index's rise, Capesize vessel freight revenue also increased significantly. Data shows that the average daily revenue of Capesize vessels carrying 150,000 tons of cargo (mainly covering core industrial raw materials such as iron ore and coal) increased by $1,087 that day, ultimately reaching $36,828. This increase in revenue directly reflects the increased global demand for large dry bulk shipping, especially the recovery in demand for industrial raw material transportation. This, coupled with the capacity constraints caused by longer shipping distances, has provided clear support for the Capesize vessel sector.

Besides the Capesize sector, the Panamax sector also showed a steady upward trend, further consolidating the overall index's upward momentum. The Panamax index rose 10 points, or 0.5%, to close at 2002 points, continuing its recent moderate upward trend; this week, the index has risen a cumulative 2.1%, demonstrating solid performance. Panamax vessels are built to meet the size restrictions for passage through the Panama Canal. Their carrying capacity falls between Capesize and Supramax, typically carrying 60,000 to 70,000 tons of cargo. Core cargo categories include coal and grain, making them important carriers for inter-regional dry bulk shipping.

Along with the rise in the Panamax index, freight revenue also increased accordingly. Data shows that the average daily revenue of Panamax vessels (typically carrying 60,000 to 70,000 tons of coal or grain) increased by $88 to $18,018. This growth was mainly due to a steady increase in global demand for the transportation of agricultural products such as grain and coal, as well as energy-related dry bulk cargoes, particularly increased inter-regional transportation activity. This, coupled with capacity constraints caused by detours on some routes, provided stable demand support for the Panamax sector.

It's worth noting that while the two major shipping sectors saw strong gains, the small vessel sector experienced a slight decline, failing to follow the overall market trend. Within the small vessel sector, the Very Large Bulk Carrier (VLCC) index fell 5 points, a 0.3% drop, closing at 1520 points. Looking at weekly performance, the index has seen a cumulative decline of approximately 1% this week. Analysts believe that small vessels primarily handle dry bulk cargo transportation in near-sea or coastal areas, and their performance is more influenced by regional market supply and demand. This slight decline may be related to short-term fluctuations in transportation demand and relatively ample capacity supply in some regions, but the overall decline is limited and has not had a significant impact on the overall market.

Overall, the rise in the Baltic Dry Index this week was mainly supported by demand from the two main vessel types, Capesize and Panamax, reflecting a moderate recovery in global dry bulk trade, particularly a rebound in demand for industrial raw materials and agricultural products, as well as the combined effects of route detours and capacity constraints. Looking ahead, as global commodity trade progresses, changes in the flow of key shipping routes and the supply and demand dynamics of various vessel types will continue to influence the Baltic Dry Index's trajectory.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.