Resilient US domestic demand and global risk aversion are driving a short-term strengthening of the US dollar.

2026-05-14 21:57:16

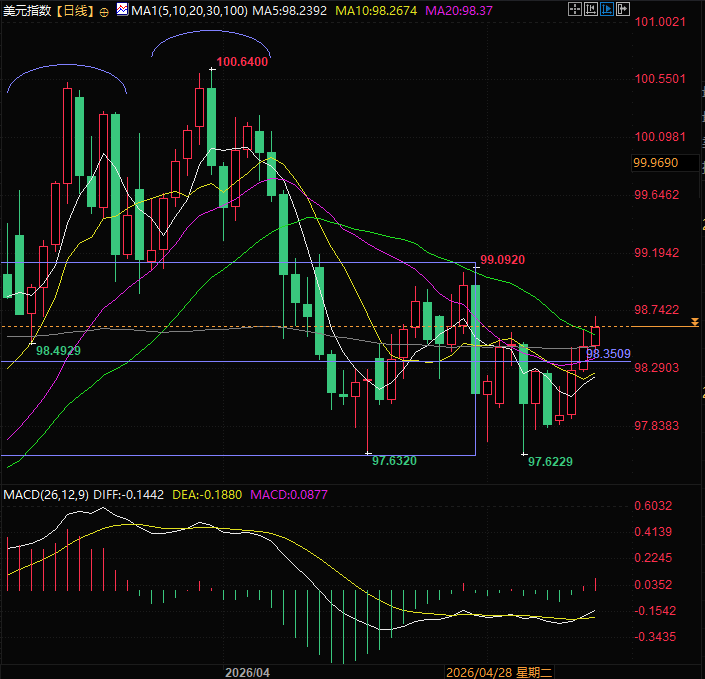

On Thursday (May 14), during the European and American trading sessions, the US dollar index remained strong during Trump's visit to China. After the data release, it began to rise slightly, but then suddenly fluctuated sharply. It is currently trading around 98.63. Traders can pay attention to whether there will be any important news affecting the US dollar index.

In April 2026, the US economy presented a complex picture of "strong consumption and weakening employment." The divergence in core data highlighted the resilience of domestic demand but also exposed concerns about growth momentum. Coupled with the interplay of geopolitical and market factors, this added uncertainty to subsequent policies and asset trends.

U.S. retail sales rose 0.5% month-over-month in April, in line with market expectations. Core retail sales (excluding volatile items such as automobiles and gasoline), which better reflect real consumer momentum, performed even better, recording a 0.7% month-over-month increase, slightly exceeding expectations by 0.1 percentage points, and firmly standing within the historical average monthly growth range of 0.3%-0.5%, highlighting the "stabilizing force" of consumption on the economy.

From a long-term perspective, the 4.9% year-on-year increase continues the core driver of GDP growth through consumption, but some details in the data reveal hidden concerns: March retail sales growth was revised down from 1.7% to 1.6% month-on-month, suggesting that growth momentum at the end of the first quarter was slightly weaker than initially expected.

This surge in consumption is not simply an endogenous recovery, but rather the result of a confluence of multiple external factors: amid the global energy crisis, American consumers stockpiled energy-related products in advance, directly driving up sales.

The continued strength of US stocks in April stimulated consumer spending through the wealth effect. Data shows that for every dollar increase in stock wealth, personal consumption increased by an average of nearly 5 cents, further amplifying the strength of retail data.

Labor Department data shows that in the week ending May 9, initial jobless claims jumped from 199,000 to 211,000, exceeding market expectations and reaching a new high for the period; continuing jobless claims also climbed to 1.782 million, indicating that it is becoming more difficult for the unemployed to find new jobs and that the "friction" in the job market is increasing.

The four-week moving average, which eliminates weekly fluctuations, rose to 203,750, further confirming that the slowdown in employment is not a short-term surprise, but rather an emerging trend.

This sluggishness was confirmed in the non-farm payroll data: although the U.S. added 115,000 non-farm jobs in April, there was a clear divergence among industries—healthcare, transportation and warehousing continued to see hiring activity, but employment in the federal government and information technology sectors continued to decline. Within the retail trade sector, there was a coexistence of department store layoffs and commodity retailers expanding hiring, reflecting companies' cautious attitude towards the economic outlook.

The current strength of the US dollar index is not only due to the boost from the US visit to China, but also because the index stabilized above 98.50 after the data release and subsequently strengthened significantly.

On the one hand, the better-than-expected core retail sales confirm the resilience of domestic demand, alleviate concerns about an economic recession, weaken the necessity for the Federal Reserve to cut interest rates in the short term, and provide fundamental support for the US dollar.

On the other hand, the escalating global geopolitical uncertainty, coupled with high energy prices, has driven risk aversion and led to a return of funds to dollar assets, reinforcing their safe-haven attributes.

The weakness in the job market is limiting the dollar's gains: if initial jobless claims continue to rise and non-farm payroll growth slows further, it could trigger a repricing of the economic outlook, thereby suppressing the dollar's upside potential.

In the short term, the US dollar index is expected to maintain a "conflicted" but slightly strong fluctuation, with its trend closely tied to the sustainability of retail consumption and the degree of deterioration in the job market. Energy price fluctuations and changes in the geopolitical situation will be key disruptive variables.

(US Dollar Index Daily Chart, Source: FX678)

At 21:54 Beijing time, the US dollar index is currently at 98.63.

In April 2026, the US economy presented a complex picture of "strong consumption and weakening employment." The divergence in core data highlighted the resilience of domestic demand but also exposed concerns about growth momentum. Coupled with the interplay of geopolitical and market factors, this added uncertainty to subsequent policies and asset trends.

Data performance: Overall up to standard, but quality is questionable.

U.S. retail sales rose 0.5% month-over-month in April, in line with market expectations. Core retail sales (excluding volatile items such as automobiles and gasoline), which better reflect real consumer momentum, performed even better, recording a 0.7% month-over-month increase, slightly exceeding expectations by 0.1 percentage points, and firmly standing within the historical average monthly growth range of 0.3%-0.5%, highlighting the "stabilizing force" of consumption on the economy.

From a long-term perspective, the 4.9% year-on-year increase continues the core driver of GDP growth through consumption, but some details in the data reveal hidden concerns: March retail sales growth was revised down from 1.7% to 1.6% month-on-month, suggesting that growth momentum at the end of the first quarter was slightly weaker than initially expected.

This surge in consumption is not simply an endogenous recovery, but rather the result of a confluence of multiple external factors: amid the global energy crisis, American consumers stockpiled energy-related products in advance, directly driving up sales.

The continued strength of US stocks in April stimulated consumer spending through the wealth effect. Data shows that for every dollar increase in stock wealth, personal consumption increased by an average of nearly 5 cents, further amplifying the strength of retail data.

Job Market: Cracks Emerge, Non-Farm Payrolls Confirm Weakness

Labor Department data shows that in the week ending May 9, initial jobless claims jumped from 199,000 to 211,000, exceeding market expectations and reaching a new high for the period; continuing jobless claims also climbed to 1.782 million, indicating that it is becoming more difficult for the unemployed to find new jobs and that the "friction" in the job market is increasing.

The four-week moving average, which eliminates weekly fluctuations, rose to 203,750, further confirming that the slowdown in employment is not a short-term surprise, but rather an emerging trend.

This sluggishness was confirmed in the non-farm payroll data: although the U.S. added 115,000 non-farm jobs in April, there was a clear divergence among industries—healthcare, transportation and warehousing continued to see hiring activity, but employment in the federal government and information technology sectors continued to decline. Within the retail trade sector, there was a coexistence of department store layoffs and commodity retailers expanding hiring, reflecting companies' cautious attitude towards the economic outlook.

The US Dollar Index Under Data Interaction: Fluctuating with a Slightly Stronger Bias Amidst Divergence

The current strength of the US dollar index is not only due to the boost from the US visit to China, but also because the index stabilized above 98.50 after the data release and subsequently strengthened significantly.

On the one hand, the better-than-expected core retail sales confirm the resilience of domestic demand, alleviate concerns about an economic recession, weaken the necessity for the Federal Reserve to cut interest rates in the short term, and provide fundamental support for the US dollar.

On the other hand, the escalating global geopolitical uncertainty, coupled with high energy prices, has driven risk aversion and led to a return of funds to dollar assets, reinforcing their safe-haven attributes.

The weakness in the job market is limiting the dollar's gains: if initial jobless claims continue to rise and non-farm payroll growth slows further, it could trigger a repricing of the economic outlook, thereby suppressing the dollar's upside potential.

In the short term, the US dollar index is expected to maintain a "conflicted" but slightly strong fluctuation, with its trend closely tied to the sustainability of retail consumption and the degree of deterioration in the job market. Energy price fluctuations and changes in the geopolitical situation will be key disruptive variables.

(US Dollar Index Daily Chart, Source: FX678)

At 21:54 Beijing time, the US dollar index is currently at 98.63.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.