The geopolitical situation is impacting the foreign exchange market; 12 factors will influence the future direction of the New Zealand dollar.

2026-05-25 12:17:12

The New Zealand dollar has been fluctuating narrowly against the US dollar over the past month, as the situation in Iran continues to disrupt global currency markets.

The New Zealand dollar fluctuated slightly as risk sentiment shifted regarding the possibility of another US military strike against Iran. The market continued to follow US statements, but as the standoff prolonged, the impact of related news on exchange rates gradually weakened.

Latest news on Sunday morning indicates that the US and Iran plan to extend the ceasefire agreement for 60 days, thereby establishing a framework for negotiations on the nuclear issue. The agreement includes the gradual restoration of navigation in the Strait of Hormuz and the unfreezing of Iranian overseas assets. The subsequent situation remains uncertain, and market trends will depend on two main developments. If the new round of talks breaks down and the US resumes military strikes, oil prices will rise, the US dollar will strengthen, and the New Zealand dollar will face downward pressure against the US dollar. Conversely, if the two sides successfully reach a peace agreement, oil prices will fall sharply, the US dollar will weaken, and the New Zealand dollar is expected to break through the 0.6000 level against the US dollar again.

The current situation is at a stalemate, and twelve key factors will influence the New Zealand dollar's exchange rate against the US dollar in the coming months.

First, oil prices are closely linked to the dollar's performance. In the short term, the dollar's movement is deeply tied to oil prices, and the evolving situation has a polarized impact. A sustained rise in oil prices will increase the risk of double-dip inflation in the US, forcing the Federal Reserve to raise interest rates, which in turn benefits the dollar exchange rate; conversely, a sharp drop in oil prices will increase the probability of an interest rate cut this year, dragging down the dollar's performance.

Second, the performance of US economic data. Recently, economic indicators such as employment, retail sales, industrial production, and various purchasing managers' indices have generally performed better than previously expected. The construction of data centers driven by the artificial intelligence industry has effectively boosted corporate investment. However, underlying economic fundamentals harbor hidden risks. This month, the University of Michigan Consumer Sentiment Index fell to 44.8, a record low, the residential construction industry is in deep trouble, and non-farm payroll data is not a reliable indicator. Overall, the US GDP growth rate in 2026 is likely to fall short of expectations, consumption, as the core driver of the economy, remains weak, limiting the potential for further appreciation of the US dollar.

Third, the policy inclinations of the new Federal Reserve Chairman. Trump's governing stance has been inconsistent; he previously publicly criticized the policies of former Fed Chairman Jerome Powell, but after Kevin Warsh was sworn in, he expressed his approval of Warsh's independent decision-making authority. Warsh plans to push forward internal reforms within the Fed, and the market is closely watching whether he will implement interest rate cuts given that inflation is above target. The first press conference after the June 17th policy meeting will be a key juncture in judging his monetary policy bias; a dovish stance would be bearish for the dollar.

Fourth, the Reserve Bank of New Zealand's monetary policy direction. There is disagreement within the industry regarding the central bank's expected interest rate hike tomorrow. Those supporting a rate hike argue that monetary policy transmission takes nine to twelve months, and early intervention can control inflation; delaying intervention will only increase the difficulty of governance. Others argue that the transmission effect of oil price shocks on prices and wages is still unclear, and conditions for a rate hike are not yet in place. Currently, the market generally expects the central bank to maintain interest rates unchanged in the short term, sending a strong signal of price control. If interest rates are raised consecutively over the next three months, it will boost the New Zealand dollar. Currently, the two-year swap rate has risen to 3.57%, indicating that monetary conditions have already tightened.

Fifth, the interest rate differential is gradually changing. For a long time, New Zealand's interest rates have been lower than those of the US and Australia, causing the New Zealand dollar to remain at a cyclical low. This situation is about to change. The market expects New Zealand to begin a rate hike cycle this year, while the US will simultaneously enter a rate-cutting cycle, potentially turning the two-year swap spread between the two countries positive. Interest rate differentials are closely correlated with exchange rates; after the interest rate differential reverses, increased foreign investment demand will drive the New Zealand dollar higher.

Sixth, adjustments in foreign exchange speculative positions. Currently, speculative funds are still maintaining short positions in the New Zealand dollar, as short selling allows them to profit from forward spreads. The Australian dollar previously saw a rapid shift in positions due to a reversal in interest rate differentials, but there are currently no signs of large-scale rebalancing among New Zealand dollar short positions. Once the situation in the Middle East eases and oil prices and the US dollar weaken, funds will flow into long positions in the New Zealand dollar, potentially pushing the exchange rate above 0.6000.

Seventh, New Zealand dollar (NZD) bond issuance is heating up. The attractiveness of NZD bonds issued by overseas institutions has rebounded, indicating a recovery in foreign investors' confidence in the New Zealand economy and currency. After a period of sluggish trading in the bond market over the past two years, new issuance has increased significantly recently. The World Bank and the Asian Development Bank have each issued NZD 1.3 billion in seven-year bonds, and Credit Agricole has expanded its issuance from NZD 300 million to NZD 800 million. Overseas investors need to exchange NZD for bonds; currently, foreign investors hold a quarter of the outstanding bond market, and this issuance boom will continue to drive demand for the currency.

Eighth, exports achieved remarkable results. New Zealand's April trade data broke historical records, with a trade surplus of NZ$1.92 billion, far exceeding market expectations of NZ$900 million, and exports increasing by 12% year-on-year. Even with the global economy under pressure from oil price shocks, the country's commodity export prospects remain solid. First-quarter retail sales increased by 0.9% quarter-on-quarter, indicating strong regional consumer activity, and robust export business is expected to drive Auckland's economic recovery. Strong foreign trade performance reduces the risk of a sovereign rating downgrade. After the release of the fiscal budget this week, debt and deficit planning will further influence market sentiment, and the overall export benefits are positive for the New Zealand dollar.

Ninth, the Bank of Japan's currency intervention. The Bank of Japan has continuously used its foreign exchange reserves to curb the yen's depreciation, successfully holding the USD/JPY level at 160. If falling oil prices lead to a decline in the dollar, and Japanese institutions reduce their holdings of US Treasury bonds and capital flows back to Japan, the yen will appreciate. The New Zealand dollar is strongly correlated with the USD/JPY exchange rate; a stronger yen will also cause the New Zealand dollar to adjust accordingly.

Tenth, many Asian countries have initiated an interest rate hike cycle. Asian countries heavily reliant on Middle Eastern oil imports, such as Malaysia, the Philippines, Thailand, Singapore, and Indonesia, have been severely impacted by energy shortages and rising prices. Central banks in these countries are successively considering raising interest rates to curb inflation, and regional interest rates are gradually catching up with those in the United States, leading to an increase in the value of their currencies. Asian countries possess $1.3 trillion in current account surplus reserves, creating an incentive for funds to flow back to their home countries to obtain higher interest rates. In contrast, oil-exporting countries' surpluses have dwindled to only $300 billion, significantly altering the regional capital flow pattern.

Eleventh, global stock market volatility. Currently, the chip and artificial intelligence technology sectors are driving the stock market upward. Once the market corrects, increased risk aversion will put downward pressure on the New Zealand dollar exchange rate. The probability of a significant short-term correction is relatively limited.

Twelfth, there is a surge in cross-border investment from Australia. With the New Zealand dollar trading at 0.82 against the Australian dollar, New Zealand assets offer a price advantage for Australian capital. Adjustments to Australian domestic tax policies have impacted older homebuyers, prompting private equity firms, real estate companies, and industrial capital to seek investment opportunities in New Zealand. This inflow of cross-border capital will support the New Zealand dollar.

While not all of the factors mentioned above are favorable for the New Zealand dollar, most of them will drive the New Zealand dollar to appreciate against the US dollar and the Australian dollar as the situation in Iran calms down and the impact of oil prices subsides.

Cross-border capital investment data shows that foreign investors have reduced their purchases of US stocks and bonds in recent months, only increasing their holdings of higher-yielding corporate bonds and mortgage-backed securities. With US domestic savings unable to cover the ever-expanding government debt, the slowdown in foreign capital inflows will constrain economic development. Considering all these factors, the medium- to long-term trend of the US dollar is under pressure.

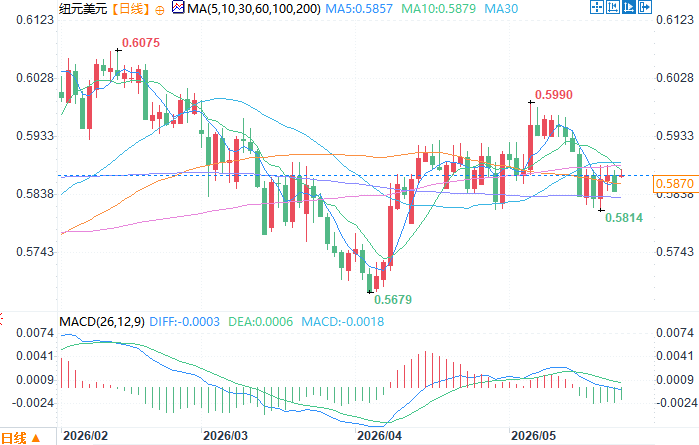

NZD/USD daily chart source: EasyTrade

At 12:16 Beijing time on May 25, the New Zealand dollar was trading at 0.5870/71 against the US dollar.

The New Zealand dollar fluctuated slightly as risk sentiment shifted regarding the possibility of another US military strike against Iran. The market continued to follow US statements, but as the standoff prolonged, the impact of related news on exchange rates gradually weakened.

Latest news on Sunday morning indicates that the US and Iran plan to extend the ceasefire agreement for 60 days, thereby establishing a framework for negotiations on the nuclear issue. The agreement includes the gradual restoration of navigation in the Strait of Hormuz and the unfreezing of Iranian overseas assets. The subsequent situation remains uncertain, and market trends will depend on two main developments. If the new round of talks breaks down and the US resumes military strikes, oil prices will rise, the US dollar will strengthen, and the New Zealand dollar will face downward pressure against the US dollar. Conversely, if the two sides successfully reach a peace agreement, oil prices will fall sharply, the US dollar will weaken, and the New Zealand dollar is expected to break through the 0.6000 level against the US dollar again.

The current situation is at a stalemate, and twelve key factors will influence the New Zealand dollar's exchange rate against the US dollar in the coming months.

First, oil prices are closely linked to the dollar's performance. In the short term, the dollar's movement is deeply tied to oil prices, and the evolving situation has a polarized impact. A sustained rise in oil prices will increase the risk of double-dip inflation in the US, forcing the Federal Reserve to raise interest rates, which in turn benefits the dollar exchange rate; conversely, a sharp drop in oil prices will increase the probability of an interest rate cut this year, dragging down the dollar's performance.

Second, the performance of US economic data. Recently, economic indicators such as employment, retail sales, industrial production, and various purchasing managers' indices have generally performed better than previously expected. The construction of data centers driven by the artificial intelligence industry has effectively boosted corporate investment. However, underlying economic fundamentals harbor hidden risks. This month, the University of Michigan Consumer Sentiment Index fell to 44.8, a record low, the residential construction industry is in deep trouble, and non-farm payroll data is not a reliable indicator. Overall, the US GDP growth rate in 2026 is likely to fall short of expectations, consumption, as the core driver of the economy, remains weak, limiting the potential for further appreciation of the US dollar.

Third, the policy inclinations of the new Federal Reserve Chairman. Trump's governing stance has been inconsistent; he previously publicly criticized the policies of former Fed Chairman Jerome Powell, but after Kevin Warsh was sworn in, he expressed his approval of Warsh's independent decision-making authority. Warsh plans to push forward internal reforms within the Fed, and the market is closely watching whether he will implement interest rate cuts given that inflation is above target. The first press conference after the June 17th policy meeting will be a key juncture in judging his monetary policy bias; a dovish stance would be bearish for the dollar.

Fourth, the Reserve Bank of New Zealand's monetary policy direction. There is disagreement within the industry regarding the central bank's expected interest rate hike tomorrow. Those supporting a rate hike argue that monetary policy transmission takes nine to twelve months, and early intervention can control inflation; delaying intervention will only increase the difficulty of governance. Others argue that the transmission effect of oil price shocks on prices and wages is still unclear, and conditions for a rate hike are not yet in place. Currently, the market generally expects the central bank to maintain interest rates unchanged in the short term, sending a strong signal of price control. If interest rates are raised consecutively over the next three months, it will boost the New Zealand dollar. Currently, the two-year swap rate has risen to 3.57%, indicating that monetary conditions have already tightened.

Fifth, the interest rate differential is gradually changing. For a long time, New Zealand's interest rates have been lower than those of the US and Australia, causing the New Zealand dollar to remain at a cyclical low. This situation is about to change. The market expects New Zealand to begin a rate hike cycle this year, while the US will simultaneously enter a rate-cutting cycle, potentially turning the two-year swap spread between the two countries positive. Interest rate differentials are closely correlated with exchange rates; after the interest rate differential reverses, increased foreign investment demand will drive the New Zealand dollar higher.

Sixth, adjustments in foreign exchange speculative positions. Currently, speculative funds are still maintaining short positions in the New Zealand dollar, as short selling allows them to profit from forward spreads. The Australian dollar previously saw a rapid shift in positions due to a reversal in interest rate differentials, but there are currently no signs of large-scale rebalancing among New Zealand dollar short positions. Once the situation in the Middle East eases and oil prices and the US dollar weaken, funds will flow into long positions in the New Zealand dollar, potentially pushing the exchange rate above 0.6000.

Seventh, New Zealand dollar (NZD) bond issuance is heating up. The attractiveness of NZD bonds issued by overseas institutions has rebounded, indicating a recovery in foreign investors' confidence in the New Zealand economy and currency. After a period of sluggish trading in the bond market over the past two years, new issuance has increased significantly recently. The World Bank and the Asian Development Bank have each issued NZD 1.3 billion in seven-year bonds, and Credit Agricole has expanded its issuance from NZD 300 million to NZD 800 million. Overseas investors need to exchange NZD for bonds; currently, foreign investors hold a quarter of the outstanding bond market, and this issuance boom will continue to drive demand for the currency.

Eighth, exports achieved remarkable results. New Zealand's April trade data broke historical records, with a trade surplus of NZ$1.92 billion, far exceeding market expectations of NZ$900 million, and exports increasing by 12% year-on-year. Even with the global economy under pressure from oil price shocks, the country's commodity export prospects remain solid. First-quarter retail sales increased by 0.9% quarter-on-quarter, indicating strong regional consumer activity, and robust export business is expected to drive Auckland's economic recovery. Strong foreign trade performance reduces the risk of a sovereign rating downgrade. After the release of the fiscal budget this week, debt and deficit planning will further influence market sentiment, and the overall export benefits are positive for the New Zealand dollar.

Ninth, the Bank of Japan's currency intervention. The Bank of Japan has continuously used its foreign exchange reserves to curb the yen's depreciation, successfully holding the USD/JPY level at 160. If falling oil prices lead to a decline in the dollar, and Japanese institutions reduce their holdings of US Treasury bonds and capital flows back to Japan, the yen will appreciate. The New Zealand dollar is strongly correlated with the USD/JPY exchange rate; a stronger yen will also cause the New Zealand dollar to adjust accordingly.

Tenth, many Asian countries have initiated an interest rate hike cycle. Asian countries heavily reliant on Middle Eastern oil imports, such as Malaysia, the Philippines, Thailand, Singapore, and Indonesia, have been severely impacted by energy shortages and rising prices. Central banks in these countries are successively considering raising interest rates to curb inflation, and regional interest rates are gradually catching up with those in the United States, leading to an increase in the value of their currencies. Asian countries possess $1.3 trillion in current account surplus reserves, creating an incentive for funds to flow back to their home countries to obtain higher interest rates. In contrast, oil-exporting countries' surpluses have dwindled to only $300 billion, significantly altering the regional capital flow pattern.

Eleventh, global stock market volatility. Currently, the chip and artificial intelligence technology sectors are driving the stock market upward. Once the market corrects, increased risk aversion will put downward pressure on the New Zealand dollar exchange rate. The probability of a significant short-term correction is relatively limited.

Twelfth, there is a surge in cross-border investment from Australia. With the New Zealand dollar trading at 0.82 against the Australian dollar, New Zealand assets offer a price advantage for Australian capital. Adjustments to Australian domestic tax policies have impacted older homebuyers, prompting private equity firms, real estate companies, and industrial capital to seek investment opportunities in New Zealand. This inflow of cross-border capital will support the New Zealand dollar.

While not all of the factors mentioned above are favorable for the New Zealand dollar, most of them will drive the New Zealand dollar to appreciate against the US dollar and the Australian dollar as the situation in Iran calms down and the impact of oil prices subsides.

Cross-border capital investment data shows that foreign investors have reduced their purchases of US stocks and bonds in recent months, only increasing their holdings of higher-yielding corporate bonds and mortgage-backed securities. With US domestic savings unable to cover the ever-expanding government debt, the slowdown in foreign capital inflows will constrain economic development. Considering all these factors, the medium- to long-term trend of the US dollar is under pressure.

NZD/USD daily chart source: EasyTrade

At 12:16 Beijing time on May 25, the New Zealand dollar was trading at 0.5870/71 against the US dollar.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.