Analysis of Australian and Japanese Interest Rates: Policy Choices and Market Outlook Based on Differences in National Endowments

2026-06-16 17:33:14

Japan (a raw material importer) and Australia (a raw material exporter) announced their interest rate decisions on the same day, and their monetary policy paths diverged significantly due to differences in trade characteristics, economic fundamentals, and inflation structures.

Institutions are generally optimistic about the medium- to long-term appreciation potential of the Japanese yen, but negative real interest rates in the short term still pose a constraint; the Australian dollar, on the other hand, is suppressed by expectations of a weak economy, and hawkish statements are unlikely to change its weakness.

The Bank of Japan raised interest rates by 25 basis points as expected, bringing the policy rate to 1.0%, a decision based on considerations of economic recovery, rising inflation, and risk balance.

The Bank of Japan clarified that it will flexibly adjust the pace and timing of interest rate hikes based on the economic, price, and financial environment, while also pointing out that the calculation of the neutral interest rate has too high a dispersion and is not of policy reference value.

Despite rising interest rates, the current financial environment remains relatively loose, with real interest rates remaining negative in the short to medium term. If Japanese government bond yields rise sharply, the central bank will use flexible bond market operations to offset the volatility. (Central Bank Intervention)

Furthermore, Governor Kazuo Ueda's short-term hospitalization will not affect the overall direction of monetary policy.

On the inflation front: As a raw material importer, Japan faces a combination of imported inflationary pressures and endogenous inflation. The wage-price transmission mechanism is working smoothly, with the basic wage increase remaining stable at around 3% throughout the year, pushing the price center upward.

The central bank warned that potential inflation could exceed the 2% policy target and accelerate upwards, making stabilizing inflation at around 2% a core objective. This interest rate meeting added a statement regarding the risk of upward inflation, signaling a continued tightening of monetary policy. While the risk of a deep recession triggered by the Middle East conflict has subsided, geopolitical tensions may still be transmitted to domestic prices through foreign exchange and financial markets, requiring continued monitoring.

On the economic front: Japan's economy has achieved a moderate recovery, which is in line with the central bank's benchmark expectations, and the risk of a sharp downside has decreased compared to the previous period; only some sectors are showing weakness, and the recovery prospects of the logistics industry remain uncertain.

Economic fundamentals provide support for the normalization of monetary policy, serving as an important basis for this interest rate hike and subsequent gradual tightening.

The Reserve Bank of Australia opted for a hawkish stance, maintaining the current interest rate level, and did not discuss any rate hikes at the meeting.

The Fed president stated that monthly economic data fluctuates significantly, and more data is needed to verify trends. He indicated that tightening operations will not be implemented at this time, but the possibility of further tightening monetary policy if necessary remains.

The market did not react positively to the hawkish remarks, but instead focused on the expectation of weak economic growth. Short-term swap rates fell in tandem with the Australian dollar, highlighting that the market's threshold for a positive response to hawkish central bank comments has been significantly raised.

On the inflation front: As a raw material exporter, Australia's inflation is closely linked to commodity prices. Current inflation and oil price data are basically in line with the May baseline forecast, but the overall level is still significantly high, and the upside risks have not been eliminated.

The Fed emphasized that low and stable inflation is the foundation for economic growth, and that slowing domestic demand is a necessary condition for inflation to fall. Although the current inflation control environment has improved compared to the previous period, the decline is not as fast as expected, so the Fed is keeping interest rate hikes as an alternative tool.

On the economic front: The Australian economy is not expected to contract this quarter and is maintaining an overall growth trend, but the momentum has clearly weakened, and the market is deeply concerned about downside risks.

The Fed governor stated that it is currently impossible to determine whether the cooling housing market will help lower inflation; while news related to Middle East peace is positive, it is unlikely to reverse the current weak domestic demand. Weak economic growth is the core factor suppressing the Australian dollar and offsetting the positive impact of the central bank's hawkish stance.

Societe Generale believes that the Bank of Japan's rate hike to 1% only touched the lower end of the neutral interest rate range, and the statement regarding upside inflation risks opens up room for continued tightening. The bank predicts that the central bank will raise rates at a pace of 25 basis points per quarter, reaching a terminal interest rate of 2% by the end of 2027; the normalization of monetary policy in the medium to long term will continue to benefit the undervalued yen, driving its steady appreciation.

ING believes that the Reserve Bank of Australia's hawkish stance failed to boost the Australian dollar, with the market's focus entirely shifting to expectations of a weakening economy. The market's threshold for a hawkish stance from the central bank has risen significantly; a strong inflation statement alone is insufficient to support the currency, and economic growth expectations have become the core of exchange rate pricing.

Chris Turner: The Bank of Japan's interest rate hikes are unlikely to reverse the yen's short-term weakness; the loose monetary environment and deep negative real interest rates remain key constraints.

Market expectations are that the next rate hike will be postponed to December, and the USD/JPY exchange rate is likely to test 160.70, or even challenge the 161-162 range, at which point central bank intervention in the foreign exchange market is highly probable. If market volatility declines and carry trades rebound this summer, the yen will continue to face pressure as a major funding currency.

On the surface, Japan, as a raw material importer, experiences a combination of imported and endogenous inflation (rising import costs coupled with wage-price transmission). Economic recovery provides a buffer against interest rate hikes, so the core policy priority is "fighting inflation," and the government will continue to tighten monetary policy even if the real interest rate is negative in the short term.

As a raw material exporter, Australia's economic growth is highly dependent on commodity exports and domestic demand. The current weakening growth momentum has become the primary constraint. Even with high inflation, Australia dares not raise interest rates, and its policy priority has been forced to shift to "maintaining growth".

Realistically, facing government pressure and criticism from the US Treasury Secretary, Japan ultimately chose a more independent approach, aligning itself more closely with the US and even sacrificing economic growth potential by raising interest rates. This was likely due to immense pressure from the US. Australia, on the other hand, normally chose not to raise rates because of a shift in US-Iran relations and the fact that central banks are generally reluctant to do so—the US was unwilling, the UK was unwilling, and the Eurozone had data to support its decision: a robust economy but weak consumption and severe capital outflows.

In the medium to long term, Japan's continued interest rate hike cycle is beneficial to the yen; in the short term, the yen is dragged down by negative real interest rates, and the USD/JPY exchange rate may fluctuate at high levels; the Australian dollar is unlikely to escape the weakness brought about by economic weakness.

From a technical perspective, despite recent intervention by the Bank of Japan, expectations of interest rate hikes, and a weakening US dollar, the USD/JPY pair remains strong. This suggests that USD/JPY may continue to strengthen while the yen continues to depreciate. However, due to the yen's long-term depreciation, the safety margin for going long on the yen is also accumulating.

(USD/JPY daily chart, source: FX678)

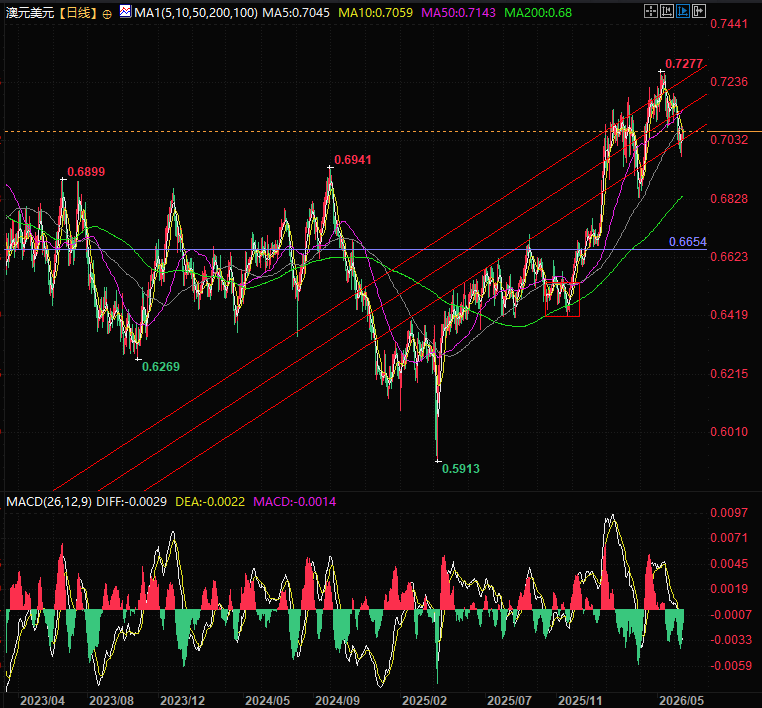

The Australian dollar is currently trading near the lower boundary of its channel against the US dollar, facing the risk of further weakening in the long term, but a short-term rebound is possible.

(AUD/USD daily chart, source: FX678)

At 17:29 Beijing time, the US dollar was trading at 160.30 against the Japanese yen, and the Australian dollar was trading at 0.7066 against the US dollar.

Institutions are generally optimistic about the medium- to long-term appreciation potential of the Japanese yen, but negative real interest rates in the short term still pose a constraint; the Australian dollar, on the other hand, is suppressed by expectations of a weak economy, and hawkish statements are unlikely to change its weakness.

Bank of Japan: Inflation-driven interest rate hikes in raw material importing countries

The Bank of Japan raised interest rates by 25 basis points as expected, bringing the policy rate to 1.0%, a decision based on considerations of economic recovery, rising inflation, and risk balance.

The Bank of Japan clarified that it will flexibly adjust the pace and timing of interest rate hikes based on the economic, price, and financial environment, while also pointing out that the calculation of the neutral interest rate has too high a dispersion and is not of policy reference value.

Despite rising interest rates, the current financial environment remains relatively loose, with real interest rates remaining negative in the short to medium term. If Japanese government bond yields rise sharply, the central bank will use flexible bond market operations to offset the volatility. (Central Bank Intervention)

Furthermore, Governor Kazuo Ueda's short-term hospitalization will not affect the overall direction of monetary policy.

On the inflation front: As a raw material importer, Japan faces a combination of imported inflationary pressures and endogenous inflation. The wage-price transmission mechanism is working smoothly, with the basic wage increase remaining stable at around 3% throughout the year, pushing the price center upward.

The central bank warned that potential inflation could exceed the 2% policy target and accelerate upwards, making stabilizing inflation at around 2% a core objective. This interest rate meeting added a statement regarding the risk of upward inflation, signaling a continued tightening of monetary policy. While the risk of a deep recession triggered by the Middle East conflict has subsided, geopolitical tensions may still be transmitted to domestic prices through foreign exchange and financial markets, requiring continued monitoring.

On the economic front: Japan's economy has achieved a moderate recovery, which is in line with the central bank's benchmark expectations, and the risk of a sharp downside has decreased compared to the previous period; only some sectors are showing weakness, and the recovery prospects of the logistics industry remain uncertain.

Economic fundamentals provide support for the normalization of monetary policy, serving as an important basis for this interest rate hike and subsequent gradual tightening.

Reserve Bank of Australia: Growth constraints in raw material exporting countries lead to price stabilization

The Reserve Bank of Australia opted for a hawkish stance, maintaining the current interest rate level, and did not discuss any rate hikes at the meeting.

The Fed president stated that monthly economic data fluctuates significantly, and more data is needed to verify trends. He indicated that tightening operations will not be implemented at this time, but the possibility of further tightening monetary policy if necessary remains.

The market did not react positively to the hawkish remarks, but instead focused on the expectation of weak economic growth. Short-term swap rates fell in tandem with the Australian dollar, highlighting that the market's threshold for a positive response to hawkish central bank comments has been significantly raised.

On the inflation front: As a raw material exporter, Australia's inflation is closely linked to commodity prices. Current inflation and oil price data are basically in line with the May baseline forecast, but the overall level is still significantly high, and the upside risks have not been eliminated.

The Fed emphasized that low and stable inflation is the foundation for economic growth, and that slowing domestic demand is a necessary condition for inflation to fall. Although the current inflation control environment has improved compared to the previous period, the decline is not as fast as expected, so the Fed is keeping interest rate hikes as an alternative tool.

On the economic front: The Australian economy is not expected to contract this quarter and is maintaining an overall growth trend, but the momentum has clearly weakened, and the market is deeply concerned about downside risks.

The Fed governor stated that it is currently impossible to determine whether the cooling housing market will help lower inflation; while news related to Middle East peace is positive, it is unlikely to reverse the current weak domestic demand. Weak economic growth is the core factor suppressing the Australian dollar and offsetting the positive impact of the central bank's hawkish stance.

Mainstream foreign institutional views

Societe Generale believes that the Bank of Japan's rate hike to 1% only touched the lower end of the neutral interest rate range, and the statement regarding upside inflation risks opens up room for continued tightening. The bank predicts that the central bank will raise rates at a pace of 25 basis points per quarter, reaching a terminal interest rate of 2% by the end of 2027; the normalization of monetary policy in the medium to long term will continue to benefit the undervalued yen, driving its steady appreciation.

ING believes that the Reserve Bank of Australia's hawkish stance failed to boost the Australian dollar, with the market's focus entirely shifting to expectations of a weakening economy. The market's threshold for a hawkish stance from the central bank has risen significantly; a strong inflation statement alone is insufficient to support the currency, and economic growth expectations have become the core of exchange rate pricing.

Chris Turner: The Bank of Japan's interest rate hikes are unlikely to reverse the yen's short-term weakness; the loose monetary environment and deep negative real interest rates remain key constraints.

Market expectations are that the next rate hike will be postponed to December, and the USD/JPY exchange rate is likely to test 160.70, or even challenge the 161-162 range, at which point central bank intervention in the foreign exchange market is highly probable. If market volatility declines and carry trades rebound this summer, the yen will continue to face pressure as a major funding currency.

Summary and Technical Analysis:

On the surface, Japan, as a raw material importer, experiences a combination of imported and endogenous inflation (rising import costs coupled with wage-price transmission). Economic recovery provides a buffer against interest rate hikes, so the core policy priority is "fighting inflation," and the government will continue to tighten monetary policy even if the real interest rate is negative in the short term.

As a raw material exporter, Australia's economic growth is highly dependent on commodity exports and domestic demand. The current weakening growth momentum has become the primary constraint. Even with high inflation, Australia dares not raise interest rates, and its policy priority has been forced to shift to "maintaining growth".

Realistically, facing government pressure and criticism from the US Treasury Secretary, Japan ultimately chose a more independent approach, aligning itself more closely with the US and even sacrificing economic growth potential by raising interest rates. This was likely due to immense pressure from the US. Australia, on the other hand, normally chose not to raise rates because of a shift in US-Iran relations and the fact that central banks are generally reluctant to do so—the US was unwilling, the UK was unwilling, and the Eurozone had data to support its decision: a robust economy but weak consumption and severe capital outflows.

In the medium to long term, Japan's continued interest rate hike cycle is beneficial to the yen; in the short term, the yen is dragged down by negative real interest rates, and the USD/JPY exchange rate may fluctuate at high levels; the Australian dollar is unlikely to escape the weakness brought about by economic weakness.

From a technical perspective, despite recent intervention by the Bank of Japan, expectations of interest rate hikes, and a weakening US dollar, the USD/JPY pair remains strong. This suggests that USD/JPY may continue to strengthen while the yen continues to depreciate. However, due to the yen's long-term depreciation, the safety margin for going long on the yen is also accumulating.

(USD/JPY daily chart, source: FX678)

The Australian dollar is currently trading near the lower boundary of its channel against the US dollar, facing the risk of further weakening in the long term, but a short-term rebound is possible.

(AUD/USD daily chart, source: FX678)

At 17:29 Beijing time, the US dollar was trading at 160.30 against the Japanese yen, and the Australian dollar was trading at 0.7066 against the US dollar.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.