Breaking News! Warsh's debut saw the abolition of forward guidance, and nine officials predicting a 2026 rate hike triggered a double whammy in stocks and bonds.

2026-06-18 07:02:26

On June 17, Eastern Time (2:00 AM Beijing Time on Thursday, June 18), the Federal Open Market Committee (FOMC) of the Federal Reserve announced its latest interest rate decision, with all members unanimously voting to maintain the target range for the federal funds rate at 3.50% to 3.75%. This marks the fourth consecutive time the Fed has kept interest rates unchanged since December 2025.

This meeting marked the first policy meeting since Kevin Warsh took over as the new chairman of the Federal Reserve last month. Warsh quickly made his first appearance, drastically reducing the policy statement from over 300 words to approximately 130 words—a 62% reduction. The statement removed all previous wording hinting at "further adjustments to interest rates" and eliminated any forward guidance on near-term policy actions, signifying a return to the concise style of communication characteristic of former Chairman Greenspan.

The statement's description of the economic situation also reflects Warsh's policy focus, noting "strong productivity growth and capital investment," while acknowledging that inflation is "above the Committee's 2 percent target," attributing part of the reason to "supply shocks that have driven up prices in certain sectors, including energy."

At the post-meeting press conference, Warsh made it clear that forward guidance is "not suitable" for the current economic environment. "I can't tell you what we're going to do next," he said. "The good news is that we'll be meeting again in six weeks."

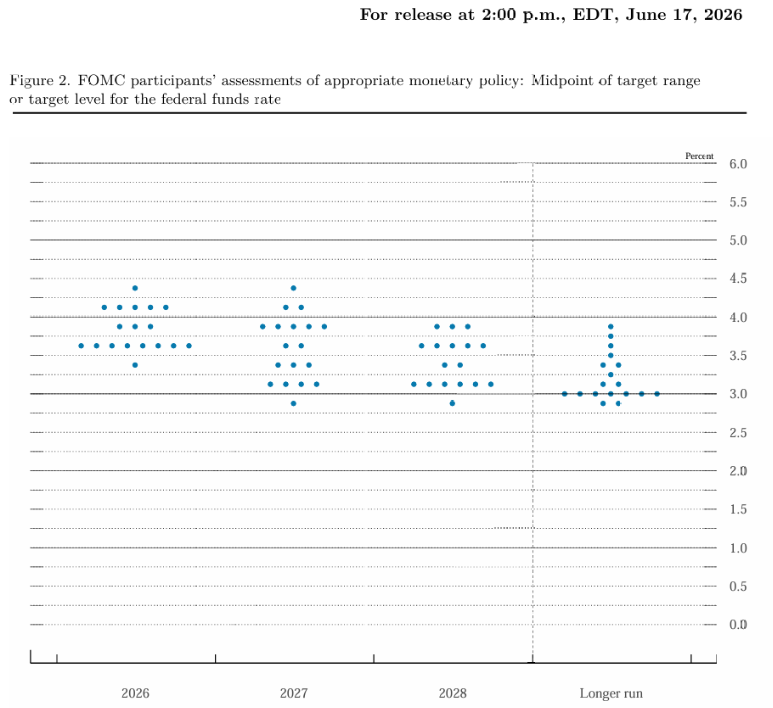

Although the interest rate decision itself was in line with market expectations, the latest quarterly forecasts (dot plot) released a strong hawkish signal, becoming the core variable that triggered sharp market fluctuations.

The median interest rate in the dot plot was 3.8%, a significant upward revision from the 3.4% forecast in March. Of the 19 Federal Reserve officials, only 18 submitted dot plot projections—Wash himself confirmed that he did not provide any projections, stating that "providing a dot plot does not help with policy implementation." Of the 18 officials who submitted projections:

One person predicts a cumulative interest rate hike of 75 basis points over the remainder of 2026.

Five people predict a cumulative interest rate hike of 50 basis points.

Three people predict a cumulative interest rate hike of 25 basis points.

Eight people expect interest rates to remain unchanged.

One person predicts a cumulative interest rate cut of 25 basis points.

A total of 9 people support raising interest rates in 2026, 8 people prefer to keep rates unchanged, and only 1 person insists on cutting interest rates.

At the press conference, Walsh attempted to downplay the importance of the dot plot, saying that the forecasts were submitted with "pencils with big erasers," and added that policymakers "did not feel constrained by their own dot plot forecasts."

The Summary of Economic Projections (SEP) simultaneously and significantly raised its inflation forecasts. The median PCE inflation forecast for 2026 was revised upward to 3.6% from 2.7% in March, with a further decline to 2.3% in 2027 and 2.0% in 2028. Core PCE inflation is projected to rise to 3.3% in 2026, significantly higher than the 2.7% forecast in March. Regarding economic growth, the median real GDP growth rate for 2026 was revised downward to 2.2% (from 2.4% in March), while the median unemployment rate was slightly adjusted to 4.3% (from 4.4% in March).

The hawkish shift in the dot plot immediately triggered violent turmoil in the financial markets.

Stock Market: U.S. stocks plunged after the decision was announced. The S&P 500 closed down 1.19%, and the Nasdaq Composite closed down 1.32%.

Bond Market: The yield on the two-year U.S. Treasury note surged 17 basis points to 4.216%, the highest since February 2025; the benchmark 10-year yield rose 7 basis points to 4.495%.

Currency Market: The US dollar index rose 0.8% to 100.38. Non-US currencies generally came under pressure.

Interest rate futures: The market's probability of a Fed rate hike before October has risen to 72%, fully priced in the expectation of a 25 basis point rate hike before the end of the year.

Spot gold: Spot gold fell 1.7% to $4,257.60 per ounce on Thursday.

Thomas Simons, chief U.S. economist at Jefferies, noted: "The changes to the policy statement are profound. The word count has been significantly reduced, and the few remaining forward guidance points to the two-way risks in the policy direction. After the global financial crisis, the statement became lengthy, and now it is returning to a communication style closer to that of the Greenspan era."

Uto Shinohara, senior investment strategist at Mesirow Currency Management, said: “Although the Fed held rates steady as expected, the hawkish revision of the dot plot led to a rise in both the dollar and yields. With 12 votes in favor, 0 against, and no dovish dissent, market expectations for a Fed rate hike before the end of the year jumped from 20 basis points before the statement to 30 basis points after the statement.”

Michael Pearce, chief U.S. economist at Oxford Economics, analyzed: "The key message from the Fed's significantly streamlined communications is that about half of the members now expect interest rate hikes this year, reflecting persistent concerns about inflation. The committee is roughly divided into two groups: nine policymakers expect one or more rate hikes this year, while a similar number expect rate cuts by the end of 2027."

Beyond interest rate decisions, Warsh announced a far-reaching reform plan at the press conference—a comprehensive review of how the Federal Reserve operates in several key policy areas.

Walsh will establish five special task forces, each responsible for:

Federal Reserve Communication – Reforming the Expression and Disclosure Mechanisms of Policy Statements

Balance Sheet – Examining the Current Balance Sheet Reduction Path and the Size of the Long-Term Balance Sheet

Data Sources – Exploring More Open Data Collection Methods and Statistical Indicator Systems

Productivity and Employment: Reassessing Economic Growth Potential and Labor Market Indicators

Inflation Framework – Reviewing the Path and Policy Tools for Achieving the 2% Inflation Target

These areas are all key points of criticism Warsh has consistently drawn since leaving the Federal Reserve more than a decade ago, reflecting his desire to reshape the Fed into a leaner, less transparent institution. During the press conference, Warsh repeatedly emphasized that he would not provide any forward guidance and avoided all questions regarding the future path of interest rates. Overall, the core message of Warsh's first press conference was: reduce policy guidance to the market, downplay pre-commitments to the interest rate path, and focus more on reforming the Fed's systems, data infrastructure, and communication framework.

Against the backdrop of synchronized tightening by central banks worldwide, the Federal Reserve's hawkish shift is not an isolated event. On June 16, the Bank of Japan announced an increase in its policy rate from 0.75% to 1.0%, the highest level in nearly 31 years. Following the European Central Bank's rate hike on June 11, the Danish central bank followed suit with a 25 basis point increase, and the Reserve Bank of Australia also raised rates consecutively during this period.

The June 2026 FOMC meeting marks the official start of the "Wash era" at the Federal Reserve. While maintaining interest rates at 3.50%-3.75% was in line with expectations, the dot plot showed nine officials supporting a rate hike this year, inflation expectations were significantly revised upward to 3.6%, and the policy statement was reduced by more than 60% and all forward guidance was removed. These three signals combined strongly confirm a policy turning point. The market responded with a "double whammy" of falling stocks and bonds—the S&P 500 fell 1.19%, the two-year Treasury yield surged 17 basis points to 4.216%, and interest rate futures fully priced in a rate hike before the end of the year. Warsh also launched five comprehensive reforms covering communication, the balance sheet, data sources, productivity and employment, and the inflation framework, indicating a profound reshaping of the Fed's operating model. Against the backdrop of synchronized tightening by global central banks (the Bank of Japan raised rates to 1.0%, and the ECB followed suit), the hawks within the Fed have gained the upper hand, and the next policy direction will heavily depend on subsequent inflation and employment data.

Question 1: Why did the market plummet despite the Federal Reserve keeping interest rates unchanged this time?

The interest rate decision itself was in line with market expectations—pre-meeting interest rate futures data showed a 99.6% probability of maintaining the current rate. What truly triggered a sharp market reaction was the hawkish shift in the dot plot: nine officials projected a rate hike in 2026, with the median dot plot revised significantly upward from 3.4% to 3.8%. While the market had previously anticipated an increased probability of a rate hike, it had not fully priced in a rate increase before the end of the year. Interest rate futures fully priced in the expectation of a 25 basis point rate hike before the end of the year after the decision, and this expectation gap led to a "double whammy" of declines in both stocks and bonds.

Question 2: Why did Warsh refuse to submit his personal interest rate forecast? Is the dot plot still of any value?

Warsh has long criticized the forward guidance system, arguing that over-committing to future interest rate paths restricts policy flexibility. At a press conference, he stated that "providing a dot plot does not help with policy implementation," and used the analogy of a "pencil with a large eraser" to emphasize the variability of forecasts. Although Warsh himself withdrew from submitting the dot plot, the forecasts of the remaining 18 officials remain of significant value—reflecting the distribution of policy inclinations within the FOMC and serving as a key basis for the market to judge policy direction.

Question 3: What does it mean that the policy statement has been reduced from more than 300 words to 130 words?

The statement was shrunk by 62%, removing all phrases about "further adjustments to interest rates," marking a shift in the Federal Reserve's communication style from the detailed guidance of former Chairman Powell's era back to the concise expressions of the Greenspan era. Warsh believes that forward guidance is "unsuitable" in the current economic environment and prefers to use vague language instead of clear guidance, changing the communication from "guiding expectations" to "explaining risks." This means that the market will find it more difficult to glean clear policy path signals from the statement.

Question 4: What practical impact will the Federal Reserve's reform plan have?

Warsh announced the formation of five special task forces, each responsible for reforming communications, the balance sheet, data sources, productivity and employment, and the inflation framework. These reforms could bring about changes such as: adjustments to the balance sheet reduction path, changes in how economic data is collected, a reassessment of the path to achieving the inflation target, and a reduction in the frequency and content of policy communications. Former Federal Reserve Vice Chairman Richard Clarida stated that the market needs weeks or even months to assess the new policy framework and communication mechanisms.

Question 5: Other central banks around the world are also raising interest rates. What impact will this have on the Federal Reserve?

Since June, the Bank of Japan has raised interest rates to 1.0% (a near 31-year high), while the European Central Bank, the Danish central bank, and the Reserve Bank of Australia have followed suit. This synchronized tightening by global central banks provides external support for a hawkish shift in the Federal Reserve – if other major central banks continue to raise rates while the Fed remains on hold, it could exacerbate pressure on the dollar's depreciation and the risk of capital outflows. Analysts point out that with the Bank of Japan and the European Central Bank raising rates, hawks within the FOMC are feeling some pressure, which is one of the external driving factors behind the hawkish revision of the dot plot.

This meeting marked the first policy meeting since Kevin Warsh took over as the new chairman of the Federal Reserve last month. Warsh quickly made his first appearance, drastically reducing the policy statement from over 300 words to approximately 130 words—a 62% reduction. The statement removed all previous wording hinting at "further adjustments to interest rates" and eliminated any forward guidance on near-term policy actions, signifying a return to the concise style of communication characteristic of former Chairman Greenspan.

The statement's description of the economic situation also reflects Warsh's policy focus, noting "strong productivity growth and capital investment," while acknowledging that inflation is "above the Committee's 2 percent target," attributing part of the reason to "supply shocks that have driven up prices in certain sectors, including energy."

At the post-meeting press conference, Warsh made it clear that forward guidance is "not suitable" for the current economic environment. "I can't tell you what we're going to do next," he said. "The good news is that we'll be meeting again in six weeks."

Dot plot shifts hawkish: Nine officials support rate hike this year, Warsh refuses to submit personal forecast.

Although the interest rate decision itself was in line with market expectations, the latest quarterly forecasts (dot plot) released a strong hawkish signal, becoming the core variable that triggered sharp market fluctuations.

The median interest rate in the dot plot was 3.8%, a significant upward revision from the 3.4% forecast in March. Of the 19 Federal Reserve officials, only 18 submitted dot plot projections—Wash himself confirmed that he did not provide any projections, stating that "providing a dot plot does not help with policy implementation." Of the 18 officials who submitted projections:

One person predicts a cumulative interest rate hike of 75 basis points over the remainder of 2026.

Five people predict a cumulative interest rate hike of 50 basis points.

Three people predict a cumulative interest rate hike of 25 basis points.

Eight people expect interest rates to remain unchanged.

One person predicts a cumulative interest rate cut of 25 basis points.

A total of 9 people support raising interest rates in 2026, 8 people prefer to keep rates unchanged, and only 1 person insists on cutting interest rates.

At the press conference, Walsh attempted to downplay the importance of the dot plot, saying that the forecasts were submitted with "pencils with big erasers," and added that policymakers "did not feel constrained by their own dot plot forecasts."

The Summary of Economic Projections (SEP) simultaneously and significantly raised its inflation forecasts. The median PCE inflation forecast for 2026 was revised upward to 3.6% from 2.7% in March, with a further decline to 2.3% in 2027 and 2.0% in 2028. Core PCE inflation is projected to rise to 3.3% in 2026, significantly higher than the 2.7% forecast in March. Regarding economic growth, the median real GDP growth rate for 2026 was revised downward to 2.2% (from 2.4% in March), while the median unemployment rate was slightly adjusted to 4.3% (from 4.4% in March).

Market reaction: Stocks and bonds suffer a "double whammy," the dollar surges, and interest rate futures fully price in a rate hike before the end of the year.

The hawkish shift in the dot plot immediately triggered violent turmoil in the financial markets.

Stock Market: U.S. stocks plunged after the decision was announced. The S&P 500 closed down 1.19%, and the Nasdaq Composite closed down 1.32%.

Bond Market: The yield on the two-year U.S. Treasury note surged 17 basis points to 4.216%, the highest since February 2025; the benchmark 10-year yield rose 7 basis points to 4.495%.

Currency Market: The US dollar index rose 0.8% to 100.38. Non-US currencies generally came under pressure.

Interest rate futures: The market's probability of a Fed rate hike before October has risen to 72%, fully priced in the expectation of a 25 basis point rate hike before the end of the year.

Spot gold: Spot gold fell 1.7% to $4,257.60 per ounce on Thursday.

Thomas Simons, chief U.S. economist at Jefferies, noted: "The changes to the policy statement are profound. The word count has been significantly reduced, and the few remaining forward guidance points to the two-way risks in the policy direction. After the global financial crisis, the statement became lengthy, and now it is returning to a communication style closer to that of the Greenspan era."

Uto Shinohara, senior investment strategist at Mesirow Currency Management, said: “Although the Fed held rates steady as expected, the hawkish revision of the dot plot led to a rise in both the dollar and yields. With 12 votes in favor, 0 against, and no dovish dissent, market expectations for a Fed rate hike before the end of the year jumped from 20 basis points before the statement to 30 basis points after the statement.”

Michael Pearce, chief U.S. economist at Oxford Economics, analyzed: "The key message from the Fed's significantly streamlined communications is that about half of the members now expect interest rate hikes this year, reflecting persistent concerns about inflation. The committee is roughly divided into two groups: nine policymakers expect one or more rate hikes this year, while a similar number expect rate cuts by the end of 2027."

Reform Agenda: Five Special Task Forces Established, Warsh Reshapes the Fed's Operating Model

Beyond interest rate decisions, Warsh announced a far-reaching reform plan at the press conference—a comprehensive review of how the Federal Reserve operates in several key policy areas.

Walsh will establish five special task forces, each responsible for:

Federal Reserve Communication – Reforming the Expression and Disclosure Mechanisms of Policy Statements

Balance Sheet – Examining the Current Balance Sheet Reduction Path and the Size of the Long-Term Balance Sheet

Data Sources – Exploring More Open Data Collection Methods and Statistical Indicator Systems

Productivity and Employment: Reassessing Economic Growth Potential and Labor Market Indicators

Inflation Framework – Reviewing the Path and Policy Tools for Achieving the 2% Inflation Target

These areas are all key points of criticism Warsh has consistently drawn since leaving the Federal Reserve more than a decade ago, reflecting his desire to reshape the Fed into a leaner, less transparent institution. During the press conference, Warsh repeatedly emphasized that he would not provide any forward guidance and avoided all questions regarding the future path of interest rates. Overall, the core message of Warsh's first press conference was: reduce policy guidance to the market, downplay pre-commitments to the interest rate path, and focus more on reforming the Fed's systems, data infrastructure, and communication framework.

Against the backdrop of synchronized tightening by central banks worldwide, the Federal Reserve's hawkish shift is not an isolated event. On June 16, the Bank of Japan announced an increase in its policy rate from 0.75% to 1.0%, the highest level in nearly 31 years. Following the European Central Bank's rate hike on June 11, the Danish central bank followed suit with a 25 basis point increase, and the Reserve Bank of Australia also raised rates consecutively during this period.

Editor's Summary

The June 2026 FOMC meeting marks the official start of the "Wash era" at the Federal Reserve. While maintaining interest rates at 3.50%-3.75% was in line with expectations, the dot plot showed nine officials supporting a rate hike this year, inflation expectations were significantly revised upward to 3.6%, and the policy statement was reduced by more than 60% and all forward guidance was removed. These three signals combined strongly confirm a policy turning point. The market responded with a "double whammy" of falling stocks and bonds—the S&P 500 fell 1.19%, the two-year Treasury yield surged 17 basis points to 4.216%, and interest rate futures fully priced in a rate hike before the end of the year. Warsh also launched five comprehensive reforms covering communication, the balance sheet, data sources, productivity and employment, and the inflation framework, indicating a profound reshaping of the Fed's operating model. Against the backdrop of synchronized tightening by global central banks (the Bank of Japan raised rates to 1.0%, and the ECB followed suit), the hawks within the Fed have gained the upper hand, and the next policy direction will heavily depend on subsequent inflation and employment data.

Frequently Asked Questions

Question 1: Why did the market plummet despite the Federal Reserve keeping interest rates unchanged this time?

The interest rate decision itself was in line with market expectations—pre-meeting interest rate futures data showed a 99.6% probability of maintaining the current rate. What truly triggered a sharp market reaction was the hawkish shift in the dot plot: nine officials projected a rate hike in 2026, with the median dot plot revised significantly upward from 3.4% to 3.8%. While the market had previously anticipated an increased probability of a rate hike, it had not fully priced in a rate increase before the end of the year. Interest rate futures fully priced in the expectation of a 25 basis point rate hike before the end of the year after the decision, and this expectation gap led to a "double whammy" of declines in both stocks and bonds.

Question 2: Why did Warsh refuse to submit his personal interest rate forecast? Is the dot plot still of any value?

Warsh has long criticized the forward guidance system, arguing that over-committing to future interest rate paths restricts policy flexibility. At a press conference, he stated that "providing a dot plot does not help with policy implementation," and used the analogy of a "pencil with a large eraser" to emphasize the variability of forecasts. Although Warsh himself withdrew from submitting the dot plot, the forecasts of the remaining 18 officials remain of significant value—reflecting the distribution of policy inclinations within the FOMC and serving as a key basis for the market to judge policy direction.

Question 3: What does it mean that the policy statement has been reduced from more than 300 words to 130 words?

The statement was shrunk by 62%, removing all phrases about "further adjustments to interest rates," marking a shift in the Federal Reserve's communication style from the detailed guidance of former Chairman Powell's era back to the concise expressions of the Greenspan era. Warsh believes that forward guidance is "unsuitable" in the current economic environment and prefers to use vague language instead of clear guidance, changing the communication from "guiding expectations" to "explaining risks." This means that the market will find it more difficult to glean clear policy path signals from the statement.

Question 4: What practical impact will the Federal Reserve's reform plan have?

Warsh announced the formation of five special task forces, each responsible for reforming communications, the balance sheet, data sources, productivity and employment, and the inflation framework. These reforms could bring about changes such as: adjustments to the balance sheet reduction path, changes in how economic data is collected, a reassessment of the path to achieving the inflation target, and a reduction in the frequency and content of policy communications. Former Federal Reserve Vice Chairman Richard Clarida stated that the market needs weeks or even months to assess the new policy framework and communication mechanisms.

Question 5: Other central banks around the world are also raising interest rates. What impact will this have on the Federal Reserve?

Since June, the Bank of Japan has raised interest rates to 1.0% (a near 31-year high), while the European Central Bank, the Danish central bank, and the Reserve Bank of Australia have followed suit. This synchronized tightening by global central banks provides external support for a hawkish shift in the Federal Reserve – if other major central banks continue to raise rates while the Fed remains on hold, it could exacerbate pressure on the dollar's depreciation and the risk of capital outflows. Analysts point out that with the Bank of Japan and the European Central Bank raising rates, hawks within the FOMC are feeling some pressure, which is one of the external driving factors behind the hawkish revision of the dot plot.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.