A chart shows the Baltic Dry Index falling to a more than two-month low, with Capesize and Supramax freight rates weakening significantly.

2026-06-27 01:05:32

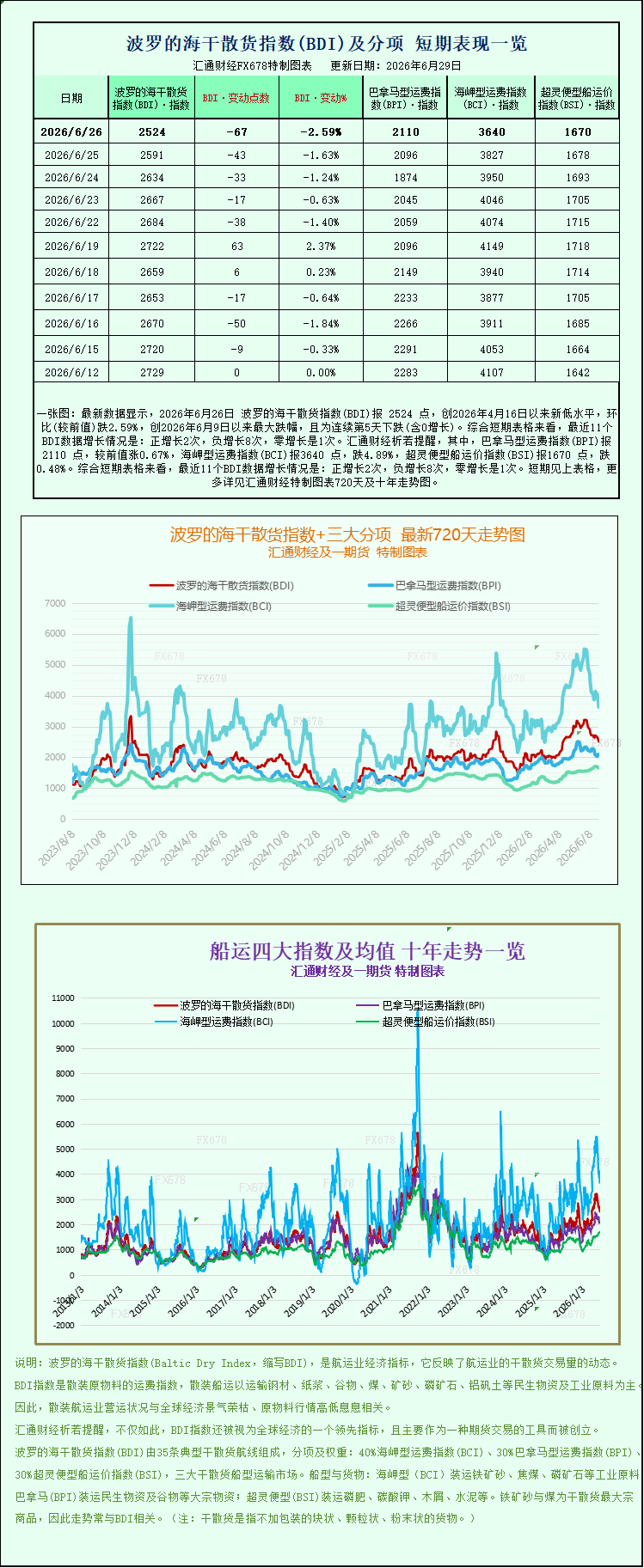

Latest data shows that the Baltic Dry Index (BDI) closed at 2524 points on June 26, 2026, a new low since April 16, 2026, down 2.59% month-on-month, the largest drop since June 9, 2026, and marking the fifth consecutive day of decline (including zero growth). Looking at the short-term charts, the recent 11 BDI data points show: 2 positive increases, 8 negative increases, and 1 zero increase. Specifically, the Panamax Freight Index (BPI) closed at 2110 points, up 0.67% from the previous value; the Capesize Freight Index (BCI) closed at 3640 points, down 4.89%; and the Supramax Freight Index (BSI) closed at 1670 points, down 0.48%. For detailed 720-day and 10-year trend charts of the Baltic Dry Index and its three main sub-indices, please refer to the specially designed charts.

The Baltic Dry Index (BDI) for core dry bulk freight fell sharply on Friday, hitting its lowest closing level in more than two months since April 16. The cumulative decline for the week was significant, clearly indicating a cooling trend in the market. Market divergence was prominent: freight rates for large Capesize vessels carrying iron ore and coal, as well as Supramax vessels suitable for smaller bulk cargoes, both faced downward pressure. Only Panamax vessels, primarily transporting grains and industrial coal, bucked the trend with a slight increase, becoming the only sector supporting the market. This reflects the current structural divergence in global commodity shipping demand.

The Baltic Dry Index (BDI) fell 67 points, or 2.6%, to close at 2524 points, a new low since mid-April. Looking at a longer timeframe, the index fell 7.3% cumulatively over the week, ending its previous recovery and indicating a rapid decline in market bullish sentiment. As a bellwether for the global dry bulk shipping market, the BDI tracks spot charter rates for the three major vessel types: Capesize, Panamax, and Supramax. The continued decline in the index directly reflects a looser supply and demand dynamic in the global ocean shipping of basic commodities such as minerals, energy, and food, while demand for seaborne raw materials for bulk industrial products has weakened temporarily, with only agricultural trade providing some support.

Looking at the breakdown by vessel type, Capesize vessels, being the largest and most sensitive to industrial cycles, were the core force dragging down the overall market. The sub-index representing Capesize vessel freight rates plummeted 187 points in a single day, a drop of 4.9%, closing at 3640 points, the largest decline among all vessel types. 150,000-ton Capesize vessels are the core capacity for transoceanic iron ore, thermal coal, and coking coal transportation, and their spot daily charter rates shrank significantly: average daily revenue on standard routes decreased by $1694 to $29511, resulting in a significant contraction in short-term operating profits for shipowners. Looking at weekly performance, Capesize vessel freight rates fell by a cumulative 12.3% in a single week, a drop far exceeding the market average, indicating a concentrated release of short-term pessimism in the industry.

The sharp adjustment in Capesize freight rates stems primarily from weakening seasonal demand across the East Asian steel supply chain. Entering late June, the domestic construction and machinery manufacturing industries entered their traditional off-season, resulting in persistently sluggish end-user steel transactions. Steel mills faced high finished product inventories and profit pressures, leading to proactive reductions in blast furnace operating rates. This significantly reduced restocking demand for imported iron ore from Brazil and Australia, resulting in a marked decrease in cargo volume on major Pacific mining shipping routes. Simultaneously, overseas metallurgical coal procurement slowed at the end of the second quarter, and long-haul coal freight orders in the Atlantic region saw insufficient growth. A large number of empty vessels remained idle at major loading ports, directly suppressing spot rates due to short-term oversupply. Coupled with a weaker-than-expected recovery in global manufacturing and a simultaneous cooling in demand for industrial coal imports in Europe and the US, these multiple factors amplified the downward pressure on the large bulk carrier market.

In contrast to the across-the-board plunge in Capesize vessels, Panamax vessels bucked the trend, becoming the only bright spot in the sluggish market. The Panamax index rose 14 points, or 0.7%, to close at 2110 points; the average daily earnings for 60,000-70,000 tonne Panamax vessels increased by $125 to $18,990, a slight weekly increase of 0.7%, completely offsetting the downward pressure on the index from larger vessels. This vessel type primarily transports global grains and short-to-medium-haul industrial coal. The current strength is supported by the peak export season for grains from North and South America: Brazilian soybean and corn shipments remain at high levels, US Gulf Coast grain export orders are stable, and Asian buyers continue to replenish grain stocks. Long-distance grain transport is driving up demand per tonne mile, tightening available Panamax vessel capacity to some extent. Furthermore, congestion in the Panama Canal extends vessel turnaround times, further reducing effective market capacity and providing sustained support for grain freight rates, creating a structurally strong performance for this vessel type against the overall market trend.

The small vessel sector continued its overall weakness, with Supramax freight rates also declining. The Supramax index fell 8 points, or 0.5%, to close at 1670 points, a near half-month low since June 15th; the weekly decline was 2.8%, slightly following the correction in Capesize vessels. Supramax vessels are suitable for diverse short-haul, regional bulk cargo transportation such as bauxite, fertilizers, building materials, and small-volume grains. Their route network is flexible, and their response to macroeconomic cycles is relatively lagging. This freight rate decline indicates that the current market adjustment has covered all tonnage classes—large, medium, and small—and is not merely a short-term fluctuation in a single vessel type. The reasons for this are twofold: firstly, global demand for raw materials and agricultural supplies from the manufacturing sector is generally weak, leading to fewer inquiries for short-haul industrial bulk cargo within the region; secondly, a large number of newly delivered small and medium-sized dry bulk vessels have continued to enter the market this year, with the growth rate of small and medium-sized fleet capacity exceeding the growth rate of freight demand, resulting in a loose supply-demand balance that continues to suppress upward pressure on charter rates.

A comparison of the performance of the three vessel types over the entire week further clarifies the market differentiation logic: Capesize vessels, carrying raw materials for the steel industry chain, saw the largest decline, falling 12.3% in a single week; Supramax vessels, covering regional small-volume trade, saw a slight correction of 2.8%; and Panamax vessels, supported by agricultural trade, bucked the trend with a slight increase of 0.7%. This clear divergence in performance fully demonstrates that the current dry bulk market lacks overall recovery momentum, with market trends entirely driven by the trade cycles of specific cargo types. Weak demand for industrial raw materials is the core contradiction suppressing the market, and the peak season for grain exports can only provide partial offsetting, failing to reverse the overall downward trend of the index.

Several shipping brokerage analysts, in interpreting this round of market trends, pointed out that the recent drop in the BDI to a two-month low is a seasonal adjustment at the end of the second quarter, and the downward pressure in the short term has not yet been fully cleared. In the short term, the situation of domestic steel mill maintenance and slowed construction due to the rainy season will continue until early July, making it difficult for iron ore and coal freight volumes to recover quickly. Capesize freight rates are likely to remain low and volatile. Panamax freight rates are highly dependent on the sustainability of South American grain exports; once the pace of shipments from major producing areas slows down, the support will weaken rapidly. Supramax vessels are hampered by the addition of new capacity, limiting their room for recovery.

In the medium to long term, the market faces potential catalysts: the El Niño climate effect will gradually emerge in 2026, with high summer temperatures in Asia potentially boosting demand for imported coal for thermal power generation; a weakening Indian monsoon is also expected to stimulate increased seaborne thermal coal shipments in the Asia-Pacific region. If domestic infrastructure and manufacturing demand stabilizes and recovers in the third quarter, steel mills' iron ore restocking demand will restart, potentially creating a recovery window for Capesize freight rates. Meanwhile, continued congestion in the Panama Canal and the detours around the Cape of Good Hope on some long-haul routes will increase global dry bulk ton-mile demand in the long term, providing a floor for freight rates.

On the supply and demand side, pressure on the industry's supply side remains objectively present. Clarkson data shows that the global dry bulk fleet capacity growth rate will remain at 2.6% in 2026, with high deliveries of new Panamax and Supramax vessels, continuously increasing market capacity in the short term. On the demand side, the growth rate of global dry bulk shipping trade will only remain at 1%-2%, and this mismatch between supply and demand growth will continue to limit the upside potential of freight rates in the second half of the year. Coupled with factors such as international oil price volatility, geopolitical trade policy uncertainties, and profit-taking by long positions in forward freight contracts, the dry bulk market may continue its structural differentiation and overall weak operating pattern in the short term.

The recent sharp decline in the Baltic Dry Index not only directly reflects the cooling global demand for industrial commodities but also sends a clear signal to shipping companies and commodity traders: the profit margins of large mineral transport vessels are shrinking in the short term, increasing operational pressure on shipowners; while grain trade-related shipping businesses offer certain returns in the short term, the profit gap between different vessel types will continue to widen. Market participants will continue to monitor three core indicators: domestic steel production data, North and South American grain exports, and the pace of Australian iron ore shipments, to determine when dry bulk freight rates will end this round of adjustment and begin a new round of recovery.

The Baltic Dry Index (BDI) for core dry bulk freight fell sharply on Friday, hitting its lowest closing level in more than two months since April 16. The cumulative decline for the week was significant, clearly indicating a cooling trend in the market. Market divergence was prominent: freight rates for large Capesize vessels carrying iron ore and coal, as well as Supramax vessels suitable for smaller bulk cargoes, both faced downward pressure. Only Panamax vessels, primarily transporting grains and industrial coal, bucked the trend with a slight increase, becoming the only sector supporting the market. This reflects the current structural divergence in global commodity shipping demand.

The Baltic Dry Index (BDI) fell 67 points, or 2.6%, to close at 2524 points, a new low since mid-April. Looking at a longer timeframe, the index fell 7.3% cumulatively over the week, ending its previous recovery and indicating a rapid decline in market bullish sentiment. As a bellwether for the global dry bulk shipping market, the BDI tracks spot charter rates for the three major vessel types: Capesize, Panamax, and Supramax. The continued decline in the index directly reflects a looser supply and demand dynamic in the global ocean shipping of basic commodities such as minerals, energy, and food, while demand for seaborne raw materials for bulk industrial products has weakened temporarily, with only agricultural trade providing some support.

Looking at the breakdown by vessel type, Capesize vessels, being the largest and most sensitive to industrial cycles, were the core force dragging down the overall market. The sub-index representing Capesize vessel freight rates plummeted 187 points in a single day, a drop of 4.9%, closing at 3640 points, the largest decline among all vessel types. 150,000-ton Capesize vessels are the core capacity for transoceanic iron ore, thermal coal, and coking coal transportation, and their spot daily charter rates shrank significantly: average daily revenue on standard routes decreased by $1694 to $29511, resulting in a significant contraction in short-term operating profits for shipowners. Looking at weekly performance, Capesize vessel freight rates fell by a cumulative 12.3% in a single week, a drop far exceeding the market average, indicating a concentrated release of short-term pessimism in the industry.

The sharp adjustment in Capesize freight rates stems primarily from weakening seasonal demand across the East Asian steel supply chain. Entering late June, the domestic construction and machinery manufacturing industries entered their traditional off-season, resulting in persistently sluggish end-user steel transactions. Steel mills faced high finished product inventories and profit pressures, leading to proactive reductions in blast furnace operating rates. This significantly reduced restocking demand for imported iron ore from Brazil and Australia, resulting in a marked decrease in cargo volume on major Pacific mining shipping routes. Simultaneously, overseas metallurgical coal procurement slowed at the end of the second quarter, and long-haul coal freight orders in the Atlantic region saw insufficient growth. A large number of empty vessels remained idle at major loading ports, directly suppressing spot rates due to short-term oversupply. Coupled with a weaker-than-expected recovery in global manufacturing and a simultaneous cooling in demand for industrial coal imports in Europe and the US, these multiple factors amplified the downward pressure on the large bulk carrier market.

In contrast to the across-the-board plunge in Capesize vessels, Panamax vessels bucked the trend, becoming the only bright spot in the sluggish market. The Panamax index rose 14 points, or 0.7%, to close at 2110 points; the average daily earnings for 60,000-70,000 tonne Panamax vessels increased by $125 to $18,990, a slight weekly increase of 0.7%, completely offsetting the downward pressure on the index from larger vessels. This vessel type primarily transports global grains and short-to-medium-haul industrial coal. The current strength is supported by the peak export season for grains from North and South America: Brazilian soybean and corn shipments remain at high levels, US Gulf Coast grain export orders are stable, and Asian buyers continue to replenish grain stocks. Long-distance grain transport is driving up demand per tonne mile, tightening available Panamax vessel capacity to some extent. Furthermore, congestion in the Panama Canal extends vessel turnaround times, further reducing effective market capacity and providing sustained support for grain freight rates, creating a structurally strong performance for this vessel type against the overall market trend.

The small vessel sector continued its overall weakness, with Supramax freight rates also declining. The Supramax index fell 8 points, or 0.5%, to close at 1670 points, a near half-month low since June 15th; the weekly decline was 2.8%, slightly following the correction in Capesize vessels. Supramax vessels are suitable for diverse short-haul, regional bulk cargo transportation such as bauxite, fertilizers, building materials, and small-volume grains. Their route network is flexible, and their response to macroeconomic cycles is relatively lagging. This freight rate decline indicates that the current market adjustment has covered all tonnage classes—large, medium, and small—and is not merely a short-term fluctuation in a single vessel type. The reasons for this are twofold: firstly, global demand for raw materials and agricultural supplies from the manufacturing sector is generally weak, leading to fewer inquiries for short-haul industrial bulk cargo within the region; secondly, a large number of newly delivered small and medium-sized dry bulk vessels have continued to enter the market this year, with the growth rate of small and medium-sized fleet capacity exceeding the growth rate of freight demand, resulting in a loose supply-demand balance that continues to suppress upward pressure on charter rates.

A comparison of the performance of the three vessel types over the entire week further clarifies the market differentiation logic: Capesize vessels, carrying raw materials for the steel industry chain, saw the largest decline, falling 12.3% in a single week; Supramax vessels, covering regional small-volume trade, saw a slight correction of 2.8%; and Panamax vessels, supported by agricultural trade, bucked the trend with a slight increase of 0.7%. This clear divergence in performance fully demonstrates that the current dry bulk market lacks overall recovery momentum, with market trends entirely driven by the trade cycles of specific cargo types. Weak demand for industrial raw materials is the core contradiction suppressing the market, and the peak season for grain exports can only provide partial offsetting, failing to reverse the overall downward trend of the index.

Several shipping brokerage analysts, in interpreting this round of market trends, pointed out that the recent drop in the BDI to a two-month low is a seasonal adjustment at the end of the second quarter, and the downward pressure in the short term has not yet been fully cleared. In the short term, the situation of domestic steel mill maintenance and slowed construction due to the rainy season will continue until early July, making it difficult for iron ore and coal freight volumes to recover quickly. Capesize freight rates are likely to remain low and volatile. Panamax freight rates are highly dependent on the sustainability of South American grain exports; once the pace of shipments from major producing areas slows down, the support will weaken rapidly. Supramax vessels are hampered by the addition of new capacity, limiting their room for recovery.

In the medium to long term, the market faces potential catalysts: the El Niño climate effect will gradually emerge in 2026, with high summer temperatures in Asia potentially boosting demand for imported coal for thermal power generation; a weakening Indian monsoon is also expected to stimulate increased seaborne thermal coal shipments in the Asia-Pacific region. If domestic infrastructure and manufacturing demand stabilizes and recovers in the third quarter, steel mills' iron ore restocking demand will restart, potentially creating a recovery window for Capesize freight rates. Meanwhile, continued congestion in the Panama Canal and the detours around the Cape of Good Hope on some long-haul routes will increase global dry bulk ton-mile demand in the long term, providing a floor for freight rates.

On the supply and demand side, pressure on the industry's supply side remains objectively present. Clarkson data shows that the global dry bulk fleet capacity growth rate will remain at 2.6% in 2026, with high deliveries of new Panamax and Supramax vessels, continuously increasing market capacity in the short term. On the demand side, the growth rate of global dry bulk shipping trade will only remain at 1%-2%, and this mismatch between supply and demand growth will continue to limit the upside potential of freight rates in the second half of the year. Coupled with factors such as international oil price volatility, geopolitical trade policy uncertainties, and profit-taking by long positions in forward freight contracts, the dry bulk market may continue its structural differentiation and overall weak operating pattern in the short term.

The recent sharp decline in the Baltic Dry Index not only directly reflects the cooling global demand for industrial commodities but also sends a clear signal to shipping companies and commodity traders: the profit margins of large mineral transport vessels are shrinking in the short term, increasing operational pressure on shipowners; while grain trade-related shipping businesses offer certain returns in the short term, the profit gap between different vessel types will continue to widen. Market participants will continue to monitor three core indicators: domestic steel production data, North and South American grain exports, and the pace of Australian iron ore shipments, to determine when dry bulk freight rates will end this round of adjustment and begin a new round of recovery.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.