A chart shows the Baltic Dry Index has fallen for six consecutive days, hitting a new low in more than two months.

2026-06-30 00:49:19

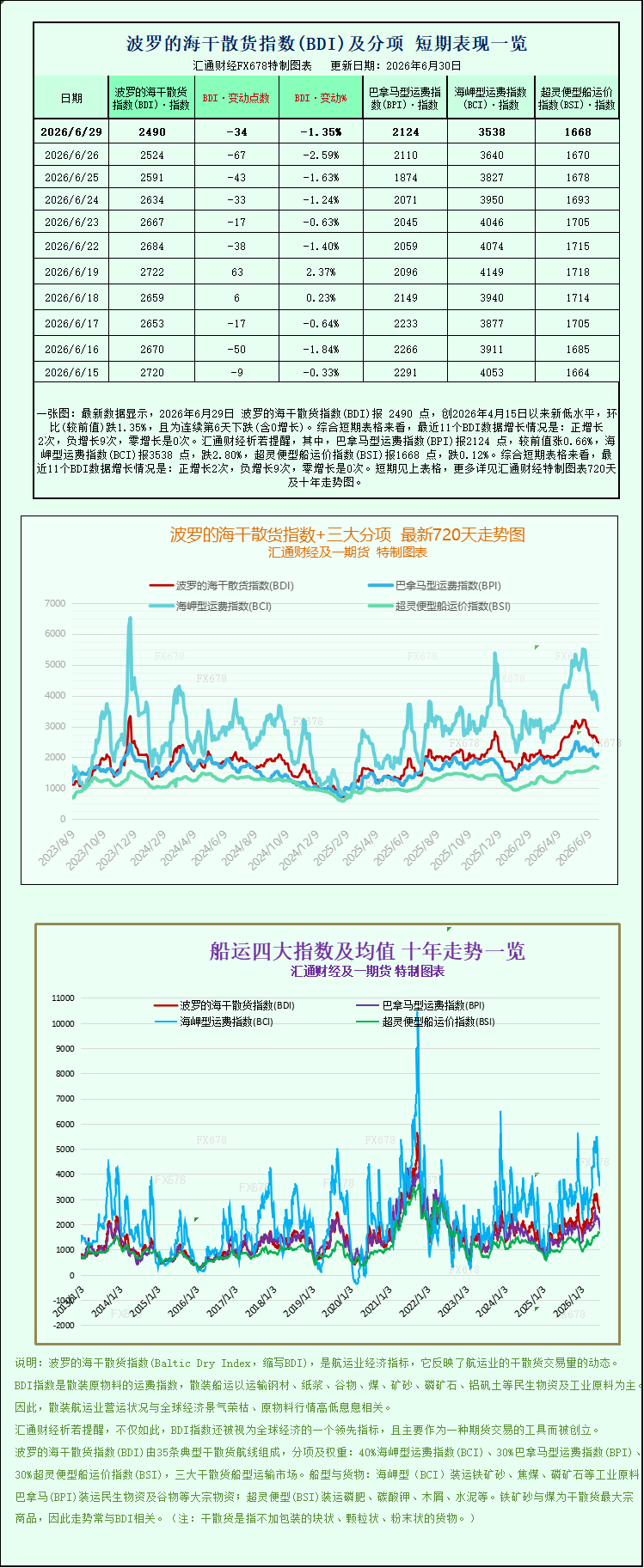

Latest data shows that the Baltic Dry Index (BDI) was at 2490 points on June 29, 2026, a new low since April 15, 2026, down 1.35% month-on-month, marking the sixth consecutive day of decline (including zero growth). Looking at the short-term charts, the recent 11 BDI data points show: 2 positive increases, 9 negative increases, and 0 zero increases. Specifically, the Panamax Freight Index (BPI) was at 2124 points, up 0.66% from the previous value; the Capesize Freight Index (BCI) was at 3538 points, down 2.80%; and the Supramax Freight Index (BSI) was at 1668 points, down 0.12%. For detailed 720-day and 10-year trend charts of the Baltic Dry Index and its three main sub-indices, please refer to the specially designed charts.

On Monday, the international dry bulk shipping market continued its weak trend, with the Baltic Dry Index (BDI) declining again, marking its sixth consecutive day of losses. It ultimately closed at 2490 points, the lowest level in over two months since April 15th. This decline was mainly driven by a sharp drop in Capesize freight rates, while Supramax vessels also faced slight pressure. Only Panamax vessels bucked the trend with a slight increase. The overall market exhibited a clear structural divergence, reflecting a phased adjustment in global commodity shipping demand.

As a core indicator of the global dry bulk shipping market, the Baltic Dry Index (.BADI) comprehensively reflects the spot freight rates of mainstream international dry bulk vessels, covering the three main vessel types: Capesize, Panamax, and Supramax. It is an important indicator for measuring the activity of global industrial raw material and agricultural product shipping and the health of international trade. On that day, the core index .BADI fell sharply by 34 points, a single-day drop of 1.4%, ending its previous period of stability and continuing to hit new recent lows. Industry analysts pointed out that this round of index declines is not a short-term market fluctuation, but rather the result of multiple factors, including weak demand, commodity price speculation, and a loose market capacity structure.

Capesize vessels, the mainstay of large-scale ocean shipping, became the core drag on the index decline, with a particularly significant market cooling trend. Data shows that the Capesize vessel-specific index plummeted 102 points that day, a drop of 2.8%, closing at 3538 points, with freight rates falling far more sharply than other vessel types. Correspondingly, vessel operating revenue shrank significantly. Capesize vessels primarily engaged in the ocean shipping of 150,000-ton iron ore, coal, and other industrial raw materials saw their average daily revenue decrease by $923, ultimately falling to $28,588, resulting in a continued narrowing of shipowners' profit margins.

The core reason for the sharp decline in Capesize freight rates is the seasonal demand adjustment and market expectation game in China's steel industry chain. Entering the end of June, downstream steel-consuming industries such as construction and machinery manufacturing entered the traditional off-season, resulting in continued sluggish end-user steel consumption. Steel mills accumulated finished product inventories and their production profits continued to shrink. Most steel mills proactively reduced blast furnace operating rates and slowed down the pace of iron ore import replenishment. The number of long-haul iron ore cargoes that previously supported ocean shipping demand decreased significantly, and the increase in orders on mainstream iron ore shipping routes from Brazil and Australia to China was insufficient, directly suppressing large Capesize vessel freight rates.

Meanwhile, the iron ore futures market saw intensified competition between bulls and bears, resulting in volatile and unclear price movements, further exacerbating the wait-and-see sentiment in the shipping market. The iron ore market exhibited a clear balance between bulls and bears: on the one hand, some domestic steel mills maintained stable pig iron production to sustain basic operations, providing some support for iron ore prices from the perspective of basic needs, and raw material import demand had not completely collapsed; on the other hand, the market generally expected steel mills to continue reducing production, coupled with the continued narrowing of profit margins in the steel industry, leading to a pessimistic outlook on long-term iron ore demand and a strong wait-and-see attitude among investors. The offsetting forces of bulls and bears resulted in a lack of clear upward momentum in iron ore prices, failing to provide positive support for the Capesize shipping market, and the industry's recovery continued to slow. In addition, the slowdown in overseas metallurgical coal procurement at the end of the second quarter and insufficient growth in long-haul coal freight orders in the Atlantic region further dragged down the overall prosperity of the Capesize shipping market.

The market for small and medium-sized vessels also showed a divergent trend, with the overall weak pattern remaining unchanged. Supramax vessels continued their slight downward trend, with the dedicated index falling 2 points, a decrease of 0.1%, to close at 1668 points, a new low in nearly half a month since June 15th. Supramax vessels mainly carry small and medium-sized industrial raw materials, building materials, and small batches of grain. The slight decline in freight rates reflects the overall weak global demand for small and medium-sized bulk cargo shipping and a cooling of regional trade activity. Coupled with the earlier recovery in shipping conditions leading to the resumption of some idle capacity, the overall market capacity supply is marginally loose, further compressing the room for freight rate increases for small and medium-sized vessels.

Amid a generally weak market, Panamax vessels emerged as the sole positive growth driver, exhibiting an independent upward trend. Data shows that the Panamax index rose 14 points, or 0.7%, to close at 2124 points; correspondingly, the average daily revenue per vessel increased by $127 to $19,117. This vessel type primarily transports 60,000 to 70,000 tons of bulk commodities such as coal and grain, mainly serving regional trade in global food and energy. The core reason for its counter-trend rise lies in the stable global demand for seaborne grain. The continued release of summer grain circulation and cross-border grain trade orders provided solid demand support for Panamax vessels, offsetting the negative impact of weak demand for seaborne industrial raw materials. This highlights the current structural characteristic of the dry bulk market: "weak demand for industrial raw materials and strong demand for agricultural products."

Considering the current state of the industry, the dry bulk shipping market is currently in a period of adjustment. On the demand side, there is a divergence between cooling industrial raw material demand and resilient agricultural demand. The seasonal off-season in China's steel industry chain is suppressing freight rates for large vessels, while global grain trade is supporting the market for medium-sized vessels. On the supply side, overall market capacity is relatively ample, coupled with weak sentiment in the commodity market, making it difficult for the overall downward pressure on dry bulk freight rates to reverse quickly in the short term.

Industry analysts say the future trend of the index will be highly dependent on the pace of recovery in China's steel industry and changes in global commodity trade. If domestic policies to stabilize growth are introduced and steel mill profits recover, iron ore restocking demand will rebound, potentially causing Capesize freight rates to bottom out and drive the index higher. However, if end-user demand remains weak, and seaborne demand for industrial raw materials contracts further, the index may continue its low-level fluctuations. Meanwhile, the ongoing peak season for global grain transportation will continue to provide a safety net for Panamax and other medium-sized vessel freight rates, and the structural differentiation in the market is likely to persist.

On Monday, the international dry bulk shipping market continued its weak trend, with the Baltic Dry Index (BDI) declining again, marking its sixth consecutive day of losses. It ultimately closed at 2490 points, the lowest level in over two months since April 15th. This decline was mainly driven by a sharp drop in Capesize freight rates, while Supramax vessels also faced slight pressure. Only Panamax vessels bucked the trend with a slight increase. The overall market exhibited a clear structural divergence, reflecting a phased adjustment in global commodity shipping demand.

As a core indicator of the global dry bulk shipping market, the Baltic Dry Index (.BADI) comprehensively reflects the spot freight rates of mainstream international dry bulk vessels, covering the three main vessel types: Capesize, Panamax, and Supramax. It is an important indicator for measuring the activity of global industrial raw material and agricultural product shipping and the health of international trade. On that day, the core index .BADI fell sharply by 34 points, a single-day drop of 1.4%, ending its previous period of stability and continuing to hit new recent lows. Industry analysts pointed out that this round of index declines is not a short-term market fluctuation, but rather the result of multiple factors, including weak demand, commodity price speculation, and a loose market capacity structure.

Capesize vessels, the mainstay of large-scale ocean shipping, became the core drag on the index decline, with a particularly significant market cooling trend. Data shows that the Capesize vessel-specific index plummeted 102 points that day, a drop of 2.8%, closing at 3538 points, with freight rates falling far more sharply than other vessel types. Correspondingly, vessel operating revenue shrank significantly. Capesize vessels primarily engaged in the ocean shipping of 150,000-ton iron ore, coal, and other industrial raw materials saw their average daily revenue decrease by $923, ultimately falling to $28,588, resulting in a continued narrowing of shipowners' profit margins.

The core reason for the sharp decline in Capesize freight rates is the seasonal demand adjustment and market expectation game in China's steel industry chain. Entering the end of June, downstream steel-consuming industries such as construction and machinery manufacturing entered the traditional off-season, resulting in continued sluggish end-user steel consumption. Steel mills accumulated finished product inventories and their production profits continued to shrink. Most steel mills proactively reduced blast furnace operating rates and slowed down the pace of iron ore import replenishment. The number of long-haul iron ore cargoes that previously supported ocean shipping demand decreased significantly, and the increase in orders on mainstream iron ore shipping routes from Brazil and Australia to China was insufficient, directly suppressing large Capesize vessel freight rates.

Meanwhile, the iron ore futures market saw intensified competition between bulls and bears, resulting in volatile and unclear price movements, further exacerbating the wait-and-see sentiment in the shipping market. The iron ore market exhibited a clear balance between bulls and bears: on the one hand, some domestic steel mills maintained stable pig iron production to sustain basic operations, providing some support for iron ore prices from the perspective of basic needs, and raw material import demand had not completely collapsed; on the other hand, the market generally expected steel mills to continue reducing production, coupled with the continued narrowing of profit margins in the steel industry, leading to a pessimistic outlook on long-term iron ore demand and a strong wait-and-see attitude among investors. The offsetting forces of bulls and bears resulted in a lack of clear upward momentum in iron ore prices, failing to provide positive support for the Capesize shipping market, and the industry's recovery continued to slow. In addition, the slowdown in overseas metallurgical coal procurement at the end of the second quarter and insufficient growth in long-haul coal freight orders in the Atlantic region further dragged down the overall prosperity of the Capesize shipping market.

The market for small and medium-sized vessels also showed a divergent trend, with the overall weak pattern remaining unchanged. Supramax vessels continued their slight downward trend, with the dedicated index falling 2 points, a decrease of 0.1%, to close at 1668 points, a new low in nearly half a month since June 15th. Supramax vessels mainly carry small and medium-sized industrial raw materials, building materials, and small batches of grain. The slight decline in freight rates reflects the overall weak global demand for small and medium-sized bulk cargo shipping and a cooling of regional trade activity. Coupled with the earlier recovery in shipping conditions leading to the resumption of some idle capacity, the overall market capacity supply is marginally loose, further compressing the room for freight rate increases for small and medium-sized vessels.

Amid a generally weak market, Panamax vessels emerged as the sole positive growth driver, exhibiting an independent upward trend. Data shows that the Panamax index rose 14 points, or 0.7%, to close at 2124 points; correspondingly, the average daily revenue per vessel increased by $127 to $19,117. This vessel type primarily transports 60,000 to 70,000 tons of bulk commodities such as coal and grain, mainly serving regional trade in global food and energy. The core reason for its counter-trend rise lies in the stable global demand for seaborne grain. The continued release of summer grain circulation and cross-border grain trade orders provided solid demand support for Panamax vessels, offsetting the negative impact of weak demand for seaborne industrial raw materials. This highlights the current structural characteristic of the dry bulk market: "weak demand for industrial raw materials and strong demand for agricultural products."

Considering the current state of the industry, the dry bulk shipping market is currently in a period of adjustment. On the demand side, there is a divergence between cooling industrial raw material demand and resilient agricultural demand. The seasonal off-season in China's steel industry chain is suppressing freight rates for large vessels, while global grain trade is supporting the market for medium-sized vessels. On the supply side, overall market capacity is relatively ample, coupled with weak sentiment in the commodity market, making it difficult for the overall downward pressure on dry bulk freight rates to reverse quickly in the short term.

Industry analysts say the future trend of the index will be highly dependent on the pace of recovery in China's steel industry and changes in global commodity trade. If domestic policies to stabilize growth are introduced and steel mill profits recover, iron ore restocking demand will rebound, potentially causing Capesize freight rates to bottom out and drive the index higher. However, if end-user demand remains weak, and seaborne demand for industrial raw materials contracts further, the index may continue its low-level fluctuations. Meanwhile, the ongoing peak season for global grain transportation will continue to provide a safety net for Panamax and other medium-sized vessel freight rates, and the structural differentiation in the market is likely to persist.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.