Yen Analysis: Rumors of GPIF repatriation coupled with intervention logic reshape the yen's short-term strength.

2026-07-10 19:22:57

On Friday (July 10), the USD/JPY pair exhibited typical news-driven price action, opening at 162.37 and trending downwards throughout the day. The pair reached a high of 162.42 and a low of 161.27, with a decline of over 0.6% by the end of the daytime trading session. The exchange rate steadily declined, while the yen strengthened accordingly.

The Finance Minister's policy signals boosted both the yen and Japanese government bonds.

Japanese Finance Minister Satsuki Katayama made a public statement that day, clarifying that the Bank of Japan has independent authority to adjust monetary policy, which strengthened market expectations for flexible policy adjustments by the central bank. On the other hand, he released a key signal that he would guide the GPIF (Government Pension Investment Fund of Japan) to adjust its asset allocation and increase its domestic asset investment, which triggered market speculation about a large-scale return of overseas funds to Japan. This directly led to a short-term rise in the yen and a simultaneous strengthening of Japanese bonds, forming a pattern of linked increases in both asset classes.

From a practical perspective, GPIF currently maintains a balanced allocation structure with domestic stocks, overseas stocks, domestic bonds, and overseas bonds divided equally. Large-scale portfolio adjustments involve complex processes and lengthy implementation cycles, making it difficult to achieve substantial capital inflows in the short term. Therefore, the market generally interprets the Finance Minister's recent remarks as typical expectation management, with the core purpose of providing sentiment and confidence support for the yen exchange rate and the Japanese bond market through policy statements, rather than immediate actual portfolio adjustments. The Japanese authorities are currently more focused on stabilizing market expectations through signals and will not hastily implement substantive interventions or portfolio adjustments.

Japanese Finance Minister Satsuki Katayama made a public statement that day, clarifying that the Bank of Japan possesses independent authority to adjust monetary policy, reinforcing market expectations of flexible policy adjustments by the central bank. He also released a key signal that the Bank of Japan's GPIF (Government Pension Investment Fund of Japan) will adjust its asset allocation and increase its domestic asset investment, sparking speculation about a large-scale repatriation of overseas funds. Stimulated by this news, the yen rose rapidly in the short term, and Japanese government bonds strengthened in tandem, creating a pattern of simultaneous increases in both asset classes.

The core logic of intervention: the rate of decline takes precedence over the absolute exchange rate level.

Carmignac fixed income fund manager Mari-Anne Allier argues that the core trigger for yen intervention is the speed of depreciation, rather than the absolute exchange rate level previously closely watched by the market. Currently, the yen's depreciation is gradual and without a sudden collapse, therefore, there is no immediate need for emergency market intervention by the authorities. Previously, the market unanimously bet on the 160 level as Japan's intervention threshold, but the yen's continued weakness and active short selling demonstrate that a single exchange rate level is no longer sufficient to deter short sellers.

At the same time, she emphasized the risks of intervention, stating that a failed, tentative intervention would not only fail to reverse the depreciation trend but would also exacerbate downward pressure on the yen, cause official financial losses, and damage policy credibility. This also means that if Japan were to intervene, it would inevitably follow the principles of large-scale and unexpected intervention, and would not easily resort to small-scale trials.

According to Aliyah, the core reason for the current weakness of the yen is the market's widespread expectation that the Japanese government will constrain the central bank's interest rate hikes. This expectation has continuously suppressed the yen's valuation recovery. Compared to passive foreign exchange market intervention, tightening monetary policy is the fundamental solution to stabilizing the yen's exchange rate. If the Bank of Japan raises interest rates as expected in September, it can directly correct market expectations and reverse the yen's weakness, and there is a high probability that there will be no need for actual foreign exchange market intervention.

Regarding potential intervention methods, she predicted that if the Japanese authorities intervene in the market to stabilize it, they will raise funds by selling overseas foreign currency assets. In order to avoid disturbing the global long-term yield curve and impacting the mainstream US Treasury market, they will prioritize selling short-term US Treasury bonds and avoid 10-year long-term US Treasury bonds, so as to minimize the spillover negative impact of intervention.

Key risk: Be wary of cross-market contagion effects.

While the market largely focuses on the direct impact of intervention on the US Treasury market, Alier pointed out that the real risk of yen volatility stems from cross-market contagion effects. As a core global low-cost carry trade currency, a sudden and significant appreciation of the yen would trigger a concentrated unwinding of global carry trades, and this chain reaction of rebalancing would quickly spread to various cross-asset and cross-regional assets. She used the Mexican peso as an example, explaining that yen fluctuations often impact seemingly unrelated emerging market assets. This implicit, global transmission risk is far more worthy of market vigilance than short-term fluctuations in US Treasury bonds.

Technical Analysis

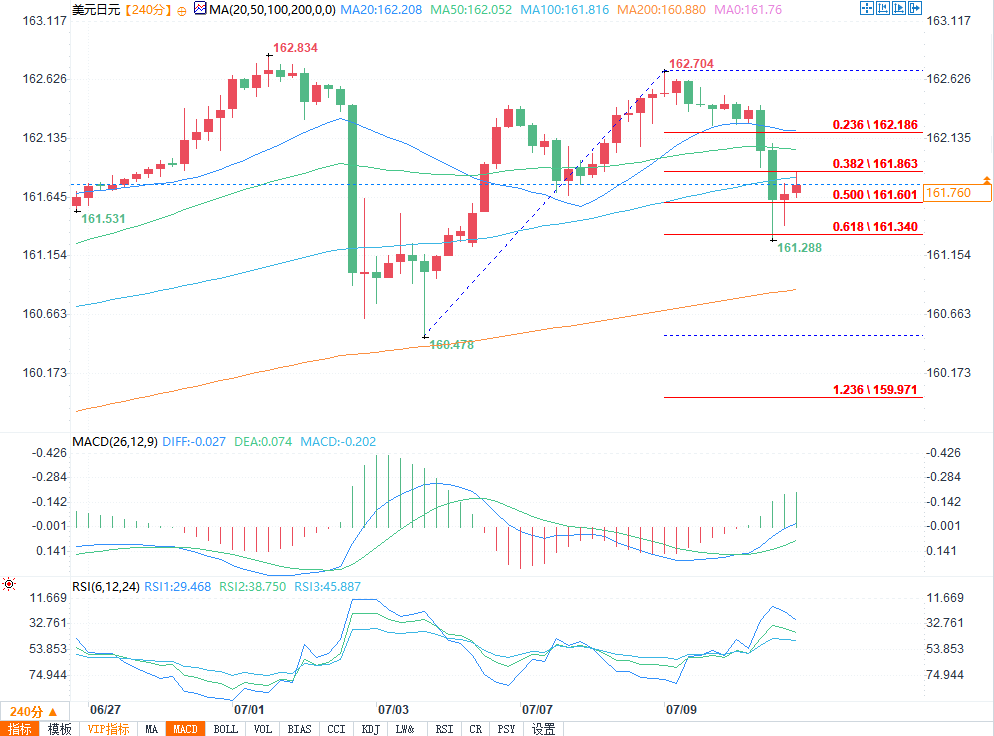

(USD/JPY 4-hour chart source: EasyForex)

From the 4-hour chart, the USD/JPY pair has recently rebounded from its lows, but the overall trend remains suppressed by multiple moving averages. The chart shows a short-term high formed around 161.28, indicating significant resistance above.

The current price is below the 100-period simple moving average, indicating that downward pressure remains in the medium term. If it can effectively break through 161.28 and further test the 161.60-161.88 area, the bullish momentum may strengthen again, and the exchange rate is expected to continue its attack on the resistance near 163.40.

On the downside, if the exchange rate fails to break through 161.28 and instead falls back, the first support level to watch is around 160.80, followed by the psychological level of 160.20-160.00. If the closing price falls below 160.00, the rebound structure may fail, and the exchange rate may retest the lows around 158.80.

Overall, the USD/JPY pair is currently in a weak rebound phase. The key criterion is whether it can effectively break through 161.28 and hold above 161.60. If the breakout is successful, the price may rise further; if it continues to fall under pressure, the 160.00 level will become an important support level.

At 19:20 Beijing time, the USD/JPY exchange rate was 161.774/783, down 0.35%.

The Finance Minister's policy signals boosted both the yen and Japanese government bonds.

Japanese Finance Minister Satsuki Katayama made a public statement that day, clarifying that the Bank of Japan has independent authority to adjust monetary policy, which strengthened market expectations for flexible policy adjustments by the central bank. On the other hand, he released a key signal that he would guide the GPIF (Government Pension Investment Fund of Japan) to adjust its asset allocation and increase its domestic asset investment, which triggered market speculation about a large-scale return of overseas funds to Japan. This directly led to a short-term rise in the yen and a simultaneous strengthening of Japanese bonds, forming a pattern of linked increases in both asset classes.

From a practical perspective, GPIF currently maintains a balanced allocation structure with domestic stocks, overseas stocks, domestic bonds, and overseas bonds divided equally. Large-scale portfolio adjustments involve complex processes and lengthy implementation cycles, making it difficult to achieve substantial capital inflows in the short term. Therefore, the market generally interprets the Finance Minister's recent remarks as typical expectation management, with the core purpose of providing sentiment and confidence support for the yen exchange rate and the Japanese bond market through policy statements, rather than immediate actual portfolio adjustments. The Japanese authorities are currently more focused on stabilizing market expectations through signals and will not hastily implement substantive interventions or portfolio adjustments.

Japanese Finance Minister Satsuki Katayama made a public statement that day, clarifying that the Bank of Japan possesses independent authority to adjust monetary policy, reinforcing market expectations of flexible policy adjustments by the central bank. He also released a key signal that the Bank of Japan's GPIF (Government Pension Investment Fund of Japan) will adjust its asset allocation and increase its domestic asset investment, sparking speculation about a large-scale repatriation of overseas funds. Stimulated by this news, the yen rose rapidly in the short term, and Japanese government bonds strengthened in tandem, creating a pattern of simultaneous increases in both asset classes.

The core logic of intervention: the rate of decline takes precedence over the absolute exchange rate level.

Carmignac fixed income fund manager Mari-Anne Allier argues that the core trigger for yen intervention is the speed of depreciation, rather than the absolute exchange rate level previously closely watched by the market. Currently, the yen's depreciation is gradual and without a sudden collapse, therefore, there is no immediate need for emergency market intervention by the authorities. Previously, the market unanimously bet on the 160 level as Japan's intervention threshold, but the yen's continued weakness and active short selling demonstrate that a single exchange rate level is no longer sufficient to deter short sellers.

At the same time, she emphasized the risks of intervention, stating that a failed, tentative intervention would not only fail to reverse the depreciation trend but would also exacerbate downward pressure on the yen, cause official financial losses, and damage policy credibility. This also means that if Japan were to intervene, it would inevitably follow the principles of large-scale and unexpected intervention, and would not easily resort to small-scale trials.

According to Aliyah, the core reason for the current weakness of the yen is the market's widespread expectation that the Japanese government will constrain the central bank's interest rate hikes. This expectation has continuously suppressed the yen's valuation recovery. Compared to passive foreign exchange market intervention, tightening monetary policy is the fundamental solution to stabilizing the yen's exchange rate. If the Bank of Japan raises interest rates as expected in September, it can directly correct market expectations and reverse the yen's weakness, and there is a high probability that there will be no need for actual foreign exchange market intervention.

Regarding potential intervention methods, she predicted that if the Japanese authorities intervene in the market to stabilize it, they will raise funds by selling overseas foreign currency assets. In order to avoid disturbing the global long-term yield curve and impacting the mainstream US Treasury market, they will prioritize selling short-term US Treasury bonds and avoid 10-year long-term US Treasury bonds, so as to minimize the spillover negative impact of intervention.

Key risk: Be wary of cross-market contagion effects.

While the market largely focuses on the direct impact of intervention on the US Treasury market, Alier pointed out that the real risk of yen volatility stems from cross-market contagion effects. As a core global low-cost carry trade currency, a sudden and significant appreciation of the yen would trigger a concentrated unwinding of global carry trades, and this chain reaction of rebalancing would quickly spread to various cross-asset and cross-regional assets. She used the Mexican peso as an example, explaining that yen fluctuations often impact seemingly unrelated emerging market assets. This implicit, global transmission risk is far more worthy of market vigilance than short-term fluctuations in US Treasury bonds.

Technical Analysis

(USD/JPY 4-hour chart source: EasyForex)

From the 4-hour chart, the USD/JPY pair has recently rebounded from its lows, but the overall trend remains suppressed by multiple moving averages. The chart shows a short-term high formed around 161.28, indicating significant resistance above.

The current price is below the 100-period simple moving average, indicating that downward pressure remains in the medium term. If it can effectively break through 161.28 and further test the 161.60-161.88 area, the bullish momentum may strengthen again, and the exchange rate is expected to continue its attack on the resistance near 163.40.

On the downside, if the exchange rate fails to break through 161.28 and instead falls back, the first support level to watch is around 160.80, followed by the psychological level of 160.20-160.00. If the closing price falls below 160.00, the rebound structure may fail, and the exchange rate may retest the lows around 158.80.

Overall, the USD/JPY pair is currently in a weak rebound phase. The key criterion is whether it can effectively break through 161.28 and hold above 161.60. If the breakout is successful, the price may rise further; if it continues to fall under pressure, the 160.00 level will become an important support level.

At 19:20 Beijing time, the USD/JPY exchange rate was 161.774/783, down 0.35%.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.