Institutions: Private lending may trigger a prolonged economic recession, supporting higher gold prices.

2026-03-12 14:33:17

Against the backdrop of escalating global economic uncertainty, the potential risks in the private credit market are becoming a new concern for the financial system.

Laks Ganapathi, CEO of Unicus Research, has made it clear that investors should not expect a significant pullback in gold prices in the short term. She believes that as vulnerabilities in the private credit market continue to rise, this risk could spill over into the broader global economy, thereby boosting gold demand again.

She suggested that investors turn to gold, commodities, and other hard assets to protect themselves from the slow and prolonged economic recession she anticipates. She added that gold is offering new stability amid weakening credit market confidence amid persistent inflation and rising global debt.

Laks Ganapathi points out that since 2022, central banks have been purchasing nearly a thousand tons of gold annually. She states, "When the institutions that control the global monetary system begin to accumulate large amounts of gold, that in itself indicates which direction the world is heading."

She warned that one of the biggest risks facing the financial system is the rapid expansion of the private lending market over the past two decades. This sector has grown from approximately $40 billion in 2000 to nearly $2 trillion today, and has largely operated outside the framework of traditional banking regulation and stress testing.

Following the 2008 financial crisis, banks were forced to strengthen their balance sheets, while the rise of private lending (sometimes referred to as shadow banking) created a new layer of risk that has yet to be tested by a major recession.

Laks Ganapathi stated, "Private lending has not undergone stress testing mechanisms."

The shadow banking system, which developed after 2008, has expanded significantly, with many operations lacking the transparency common in public markets. She added that this market structure makes it difficult for investors to accurately assess risk, as many loans in private credit portfolios are unrated, and asset pricing relies on internal valuation models rather than market prices.

She further pointed out that many private lending funds are deeply interconnected with the traditional financial system, including banks that provide credit lines to lending instruments such as business development companies. She said, "These loans are priced by internal models rather than by the market, and the trigger for a crisis may not be realized losses, but simply a loss of confidence."

She emphasized that the risks are no longer limited to corporate loans. Private credit is rapidly entering the consumer finance sector, including commercial real estate, auto loans, payday loans, and "buy now, pay later" programs. She stated, "This is where systemic vulnerability stems; once one part of the system comes under pressure, it will spread rapidly through overlapping loan portfolios and borrowers."

She also specifically mentioned the increasing participation of retail investors in the market. Products such as non-trading business development companies and retirement target funds allow individual investors to access private credit, assets that are often illiquid and difficult to value.

She believes that this combination of opacity, high leverage, and retail exposure will significantly amplify instability should economic conditions deteriorate.

Laks Ganapathi believes that the next recession will not be a sudden and complete collapse like the one in 2008.

She stated, "It won't be like 2008 where everything collapsed at once. It will be slower, possibly lasting from 2025 to 2027, and could be more painful in the long run."

She added that her company expects the global economy to face a scenario of weak growth and persistent inflation in the coming years, similar to stagflation. She said, "We anticipate stagnation and a resurgence of inflation around 2026."

Laks Ganapathi advises investors to focus on capital preservation rather than chasing high yields on complex credit products. She states, "Gold doesn't generate returns, but in a world of persistent government deficits and monetized debt, it serves as a store of value."

She revealed that Unicus Research is exploring the launch of a hedge fund strategy focused on shorting vulnerable credit assets to address rising market risks. At the same time, she cautioned that many investors may not fully understand their exposure to retirement products and other collective investment vehicles. She added, "People should understand exactly what's in their retirement funds and ask their financial advisor line by line what assets are included in their portfolio."

Overall , Laks Ganapathi's analysis highlights the structural risks in the private credit market, which have become a potential trigger for a global economic recession.

Central bank gold purchases, debt expansion, and the lack of transparency in the shadow banking system are collectively reinforcing gold's status as a safe-haven and store-of-value asset. In an anticipated environment of slow stagflation, gold's downside potential in the short term is limited, and it may even see a new wave of demand-driven growth.

Investors need to be wary of the spillover effects of private credit and carefully examine their asset allocation, especially the hidden exposure in retirement funds. Shifting towards hard assets such as gold may be a better way to cope with upcoming economic uncertainties and systemic pressures. In the coming years, if the private credit crisis gradually emerges, gold, as the ultimate safe-haven asset with "no counterparty risk," will further highlight its strategic value.

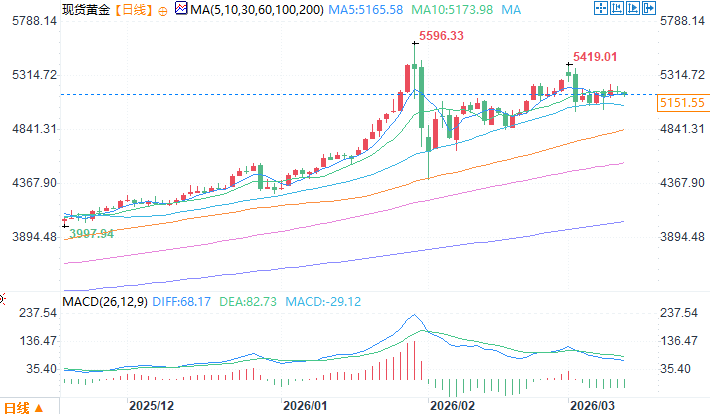

Spot gold daily chart source: EasyForex

At 14:33 Beijing time on March 12, spot gold was trading at $5160.55 per ounce.

Laks Ganapathi, CEO of Unicus Research, has made it clear that investors should not expect a significant pullback in gold prices in the short term. She believes that as vulnerabilities in the private credit market continue to rise, this risk could spill over into the broader global economy, thereby boosting gold demand again.

She suggested that investors turn to gold, commodities, and other hard assets to protect themselves from the slow and prolonged economic recession she anticipates. She added that gold is offering new stability amid weakening credit market confidence amid persistent inflation and rising global debt.

Central bank gold purchases signal a shift in the global monetary system.

Laks Ganapathi points out that since 2022, central banks have been purchasing nearly a thousand tons of gold annually. She states, "When the institutions that control the global monetary system begin to accumulate large amounts of gold, that in itself indicates which direction the world is heading."

She warned that one of the biggest risks facing the financial system is the rapid expansion of the private lending market over the past two decades. This sector has grown from approximately $40 billion in 2000 to nearly $2 trillion today, and has largely operated outside the framework of traditional banking regulation and stress testing.

Following the 2008 financial crisis, banks were forced to strengthen their balance sheets, while the rise of private lending (sometimes referred to as shadow banking) created a new layer of risk that has yet to be tested by a major recession.

The lack of transparency and stress testing in private lending may have triggered a crisis stemming from a collapse in confidence.

Laks Ganapathi stated, "Private lending has not undergone stress testing mechanisms."

The shadow banking system, which developed after 2008, has expanded significantly, with many operations lacking the transparency common in public markets. She added that this market structure makes it difficult for investors to accurately assess risk, as many loans in private credit portfolios are unrated, and asset pricing relies on internal valuation models rather than market prices.

She further pointed out that many private lending funds are deeply interconnected with the traditional financial system, including banks that provide credit lines to lending instruments such as business development companies. She said, "These loans are priced by internal models rather than by the market, and the trigger for a crisis may not be realized losses, but simply a loss of confidence."

The risks have expanded from corporate loans to consumer finance, and retail investor exposure has increased.

She emphasized that the risks are no longer limited to corporate loans. Private credit is rapidly entering the consumer finance sector, including commercial real estate, auto loans, payday loans, and "buy now, pay later" programs. She stated, "This is where systemic vulnerability stems; once one part of the system comes under pressure, it will spread rapidly through overlapping loan portfolios and borrowers."

She also specifically mentioned the increasing participation of retail investors in the market. Products such as non-trading business development companies and retirement target funds allow individual investors to access private credit, assets that are often illiquid and difficult to value.

She believes that this combination of opacity, high leverage, and retail exposure will significantly amplify instability should economic conditions deteriorate.

The recession will spread slowly, not a sudden collapse like in 2008, and the risk of stagflation will reappear.

Laks Ganapathi believes that the next recession will not be a sudden and complete collapse like the one in 2008.

She stated, "It won't be like 2008 where everything collapsed at once. It will be slower, possibly lasting from 2025 to 2027, and could be more painful in the long run."

She added that her company expects the global economy to face a scenario of weak growth and persistent inflation in the coming years, similar to stagflation. She said, "We anticipate stagnation and a resurgence of inflation around 2026."

As a tool for preserving capital, investors should prioritize defense over pursuing high returns when investing in gold.

Laks Ganapathi advises investors to focus on capital preservation rather than chasing high yields on complex credit products. She states, "Gold doesn't generate returns, but in a world of persistent government deficits and monetized debt, it serves as a store of value."

She revealed that Unicus Research is exploring the launch of a hedge fund strategy focused on shorting vulnerable credit assets to address rising market risks. At the same time, she cautioned that many investors may not fully understand their exposure to retirement products and other collective investment vehicles. She added, "People should understand exactly what's in their retirement funds and ask their financial advisor line by line what assets are included in their portfolio."

Overall , Laks Ganapathi's analysis highlights the structural risks in the private credit market, which have become a potential trigger for a global economic recession.

Central bank gold purchases, debt expansion, and the lack of transparency in the shadow banking system are collectively reinforcing gold's status as a safe-haven and store-of-value asset. In an anticipated environment of slow stagflation, gold's downside potential in the short term is limited, and it may even see a new wave of demand-driven growth.

Investors need to be wary of the spillover effects of private credit and carefully examine their asset allocation, especially the hidden exposure in retirement funds. Shifting towards hard assets such as gold may be a better way to cope with upcoming economic uncertainties and systemic pressures. In the coming years, if the private credit crisis gradually emerges, gold, as the ultimate safe-haven asset with "no counterparty risk," will further highlight its strategic value.

Spot gold daily chart source: EasyForex

At 14:33 Beijing time on March 12, spot gold was trading at $5160.55 per ounce.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.