A chart: The Baltic Dry Index rises due to stronger Capesize freight rates.

2026-03-12 23:24:42

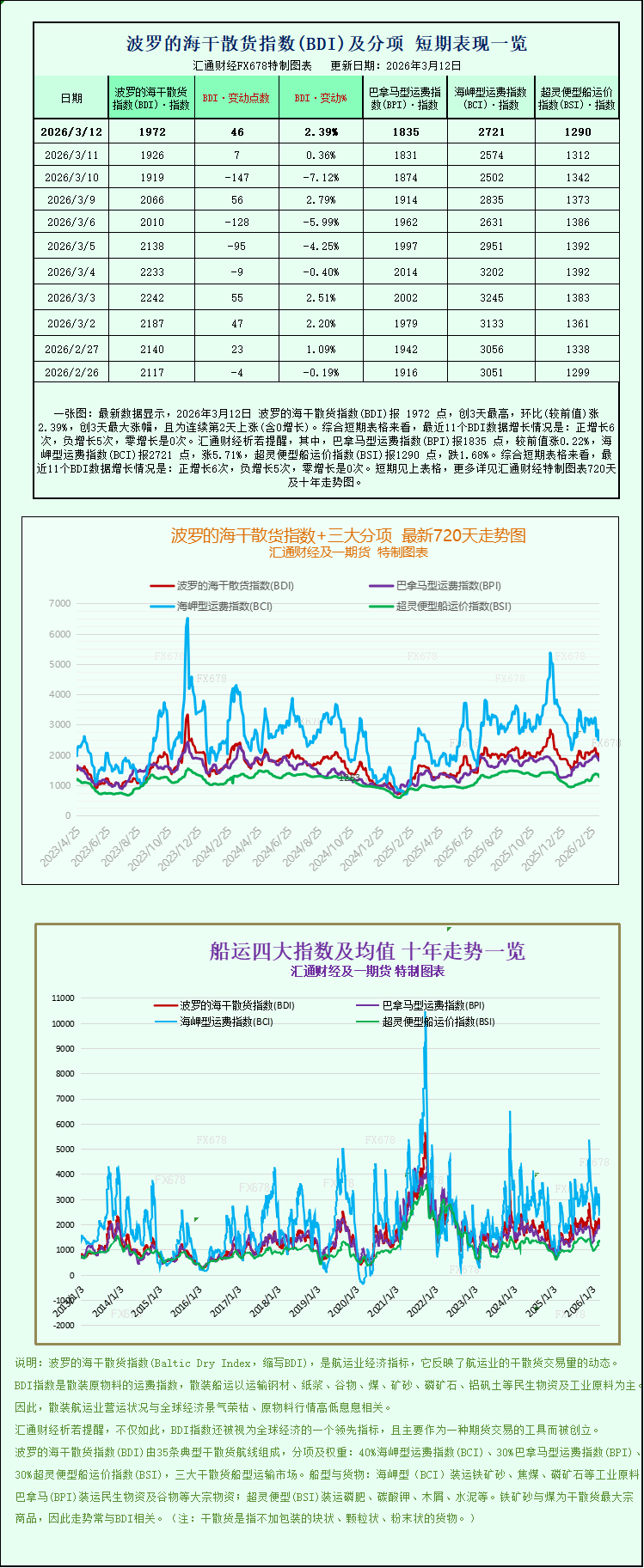

Latest data shows that on March 12, 2026, the Baltic Dry Index (BDI) reached 1972 points, the highest level in three days, up 2.39% compared to the previous trading day. This also marks the largest single-day increase in three days, and the second consecutive day of increase (including zero-growth instances), indicating a clear short-term rebound. Looking at the short-term monitoring data, the BDI has shown a slightly upward trend over the past 11 trading days, with 6 positive increases, 5 negative increases, and 0 zero increases. Overall, the balance between bulls and bears has been relatively mild, without any extreme one-sided movements. Among the three core sub-indices of the Baltic Dry Index (BDI), the Panamax Index (BPI) closed at 1835 points, a slight increase of 0.22% from the previous value, showing a relatively stable trend. The Capesize Index (BCI) performed strongly, closing at 2721 points, a significant increase of 5.71%, becoming the core driver of the BDI's rise. The Supramax Index (BSI), however, was weak, closing at 1290 points, a decrease of 1.68%, making it the only sub-indice to decline. Detailed data, including the latest 720-day trend chart and ten-year long-term trend chart for the Baltic Dry Index and its three sub-indices, can be found in specially designed charts, which visually reflect recent and long-term market fluctuations.

Strongly supported by a significant increase in Capesize vessel freight rates, the Baltic Dry Index (BDI), which monitors fluctuations in freight rates for dry bulk commodities globally and is a key indicator of the dry bulk shipping market's health, saw a substantial rise on Thursday (March 12, 2026), continuing the upward trend of the previous trading day. As a core indicator of the global dry bulk shipping market, the BDI directly reflects the relationship between global demand and supply for bulk commodities such as iron ore, coal, and grain. This increase was primarily driven by the strong rise in Capesize vessel freight rates, offsetting the drag from the decline in Supramax vessel freight rates and highlighting the divergent market structure across different vessel types.

Specifically, the Baltic Dry Index (BDI), which tracks freight rates for Capesize, Panamax, and Supramax dry bulk carriers, rose 46 points, or 2.4%, to close at 1972 points, consistent with the latest BDI data and further confirming the market's recovery. In the short term, the index has gradually rebounded since bottoming out on March 10th, accumulating a gain of over 3% in just two trading days. Market confidence has been somewhat restored, which is closely related to the continued warming of the Capesize shipping market and reflects a structural recovery in the global dry bulk shipping market.

Among them, the Capesize Index (BCI) performed the best, rising 147 points, or 5.7%, to reach 2721 points, becoming a key force driving the rise in the Baltic Dry Index (BDI). Capesize vessels, as large vessels in dry bulk shipping, have a deadweight tonnage between 160,000 and 21,000 tons and mainly carry bulk commodities such as iron ore and coal. They particularly dominate the iron ore shipping route from Western Australia to China, and their freight rate fluctuations are directly linked to global iron ore demand. This significant increase fully reflects the current strong demand for iron ore transportation.

Correspondingly, Capesize vessels transporting 150,000-tonnage cargoes such as iron ore and coal also saw an increase in average daily revenue, rising by $1,330 to reach $21,173, resulting in a significant increase in captains' earnings. This revenue growth rate is largely in line with the BCI's increase, indicating that the freight rate hike has effectively benefited shipowners, improving the operational efficiency of large dry bulk vessels and further stimulating their operational enthusiasm.

“The impact of the Middle East conflict on the dry bulk shipping sector is clearly much milder than on the tanker sector, but it certainly has an impact,” said Rico Luhmann, a transport and shipping economist at ING Research. As a veteran analyst in the shipping industry, Luhmann has long focused on the impact of geopolitics on the shipping market, and his views reflect the subtle role the current Middle East situation plays in the dry bulk shipping market—it has not caused large-scale capacity disruptions, but it has brought about certain structural effects.

“One percent of global shipping capacity is tied up in the Persian Gulf, particularly for fertilizers and aluminum, a major production area in the region. This consumes capacity that cannot be deployed elsewhere, disrupting trade routes and driving up freight and charter rates in the short term,” Luhmann added. It is understood that the Persian Gulf region is a major global fertilizer and aluminum production area, and Supramax and Handysize vessels account for a very high proportion of dry bulk trade in the region. Approximately 40% of dry bulk trade in the Persian Gulf is carried by Handysize vessels. The 1% global capacity tie-up directly leads to capacity shortages on some routes, thereby driving up freight rates for related vessel types. This is also a significant indirect factor contributing to the recent strength in Capesize vessel freight rates.

Iran's newly appointed Supreme Leader, Mojtaba Khamenei, said on Thursday that the Strait of Hormuz should remain closed to put pressure on his opposition. The Strait of Hormuz is a vital global shipping route, handling a large volume of oil and dry bulk cargo. The anticipated closure has further exacerbated market concerns about capacity constraints. While it has not yet caused substantial, large-scale disruptions to dry bulk shipping, it has already impacted market expectations in the short term, indirectly driving up freight rates.

On Thursday, iron ore futures prices rose as the market anticipated increased iron ore production following the completion of regulatory inspections at steel mills in Hebei's steel hub. Hebei is a core region for iron ore production and consumption in my country, and the production dynamics of large steel mills like Hebei Iron and Steel Group directly influence iron ore demand. With the completion of these inspections, the market generally expects production to gradually resume, further increasing iron ore demand and consequently boosting iron ore transportation demand, providing solid demand support for rising Capesize shipping rates. According to data from the China Economic Information Network, Hebei's recent iron ore production has remained above 34 million tons, providing a stable supply base. The anticipated resumption of steel mill production further amplifies the positive signals on the demand side.

The Panamax index performed relatively modestly, rising slightly by 4 points, or 0.2%, to close at 1835 points, showing little change compared to the previous trading day and exhibiting an overall stable trend. Panamax vessels, with a deadweight tonnage between 50,000 and 80,000 tons, can pass smoothly through the Panama Canal and are mainly used to transport bulk commodities such as coal and grain. Their freight rates have remained relatively stable, partly due to stable global demand for coal and grain transportation, and partly due to relatively ample market capacity, preventing a significant price increase like that seen with Capesize vessels.

Correspondingly, the average daily earnings of Panamax vessels (typically carrying 60,000 to 70,000 tons of coal or grain) also increased slightly by $37 to $16,516, resulting in a modest improvement in profitability. Although the increase was limited, this growth trend aligns with the stable performance of the Panamax index, reflecting a relatively balanced supply and demand in the market for this vessel type, without any significant imbalance, thus providing some support for the stable recovery of the BDI.

The Very Large Bulk Carrier Index (BSI) was weak, falling 22 points, or 1.7%, to close at 1290 points, making it the only one of the three sub-indices to decline. Supramax vessels, with a deadweight tonnage between 45,000 and 70,000 tons, transport a diverse range of cargoes, including not only bulk commodities like coal and grain but also various smaller bulk commodities. The decline in freight rates was mainly due to weak demand for smaller bulk cargo transportation, coupled with some capacity returning from other routes, leading to a relative oversupply in the market. This dragged down the index's performance and, to some extent, offset the positive impact of rising Capesize vessel freight rates.

Strongly supported by a significant increase in Capesize vessel freight rates, the Baltic Dry Index (BDI), which monitors fluctuations in freight rates for dry bulk commodities globally and is a key indicator of the dry bulk shipping market's health, saw a substantial rise on Thursday (March 12, 2026), continuing the upward trend of the previous trading day. As a core indicator of the global dry bulk shipping market, the BDI directly reflects the relationship between global demand and supply for bulk commodities such as iron ore, coal, and grain. This increase was primarily driven by the strong rise in Capesize vessel freight rates, offsetting the drag from the decline in Supramax vessel freight rates and highlighting the divergent market structure across different vessel types.

Specifically, the Baltic Dry Index (BDI), which tracks freight rates for Capesize, Panamax, and Supramax dry bulk carriers, rose 46 points, or 2.4%, to close at 1972 points, consistent with the latest BDI data and further confirming the market's recovery. In the short term, the index has gradually rebounded since bottoming out on March 10th, accumulating a gain of over 3% in just two trading days. Market confidence has been somewhat restored, which is closely related to the continued warming of the Capesize shipping market and reflects a structural recovery in the global dry bulk shipping market.

Among them, the Capesize Index (BCI) performed the best, rising 147 points, or 5.7%, to reach 2721 points, becoming a key force driving the rise in the Baltic Dry Index (BDI). Capesize vessels, as large vessels in dry bulk shipping, have a deadweight tonnage between 160,000 and 21,000 tons and mainly carry bulk commodities such as iron ore and coal. They particularly dominate the iron ore shipping route from Western Australia to China, and their freight rate fluctuations are directly linked to global iron ore demand. This significant increase fully reflects the current strong demand for iron ore transportation.

Correspondingly, Capesize vessels transporting 150,000-tonnage cargoes such as iron ore and coal also saw an increase in average daily revenue, rising by $1,330 to reach $21,173, resulting in a significant increase in captains' earnings. This revenue growth rate is largely in line with the BCI's increase, indicating that the freight rate hike has effectively benefited shipowners, improving the operational efficiency of large dry bulk vessels and further stimulating their operational enthusiasm.

“The impact of the Middle East conflict on the dry bulk shipping sector is clearly much milder than on the tanker sector, but it certainly has an impact,” said Rico Luhmann, a transport and shipping economist at ING Research. As a veteran analyst in the shipping industry, Luhmann has long focused on the impact of geopolitics on the shipping market, and his views reflect the subtle role the current Middle East situation plays in the dry bulk shipping market—it has not caused large-scale capacity disruptions, but it has brought about certain structural effects.

“One percent of global shipping capacity is tied up in the Persian Gulf, particularly for fertilizers and aluminum, a major production area in the region. This consumes capacity that cannot be deployed elsewhere, disrupting trade routes and driving up freight and charter rates in the short term,” Luhmann added. It is understood that the Persian Gulf region is a major global fertilizer and aluminum production area, and Supramax and Handysize vessels account for a very high proportion of dry bulk trade in the region. Approximately 40% of dry bulk trade in the Persian Gulf is carried by Handysize vessels. The 1% global capacity tie-up directly leads to capacity shortages on some routes, thereby driving up freight rates for related vessel types. This is also a significant indirect factor contributing to the recent strength in Capesize vessel freight rates.

Iran's newly appointed Supreme Leader, Mojtaba Khamenei, said on Thursday that the Strait of Hormuz should remain closed to put pressure on his opposition. The Strait of Hormuz is a vital global shipping route, handling a large volume of oil and dry bulk cargo. The anticipated closure has further exacerbated market concerns about capacity constraints. While it has not yet caused substantial, large-scale disruptions to dry bulk shipping, it has already impacted market expectations in the short term, indirectly driving up freight rates.

On Thursday, iron ore futures prices rose as the market anticipated increased iron ore production following the completion of regulatory inspections at steel mills in Hebei's steel hub. Hebei is a core region for iron ore production and consumption in my country, and the production dynamics of large steel mills like Hebei Iron and Steel Group directly influence iron ore demand. With the completion of these inspections, the market generally expects production to gradually resume, further increasing iron ore demand and consequently boosting iron ore transportation demand, providing solid demand support for rising Capesize shipping rates. According to data from the China Economic Information Network, Hebei's recent iron ore production has remained above 34 million tons, providing a stable supply base. The anticipated resumption of steel mill production further amplifies the positive signals on the demand side.

The Panamax index performed relatively modestly, rising slightly by 4 points, or 0.2%, to close at 1835 points, showing little change compared to the previous trading day and exhibiting an overall stable trend. Panamax vessels, with a deadweight tonnage between 50,000 and 80,000 tons, can pass smoothly through the Panama Canal and are mainly used to transport bulk commodities such as coal and grain. Their freight rates have remained relatively stable, partly due to stable global demand for coal and grain transportation, and partly due to relatively ample market capacity, preventing a significant price increase like that seen with Capesize vessels.

Correspondingly, the average daily earnings of Panamax vessels (typically carrying 60,000 to 70,000 tons of coal or grain) also increased slightly by $37 to $16,516, resulting in a modest improvement in profitability. Although the increase was limited, this growth trend aligns with the stable performance of the Panamax index, reflecting a relatively balanced supply and demand in the market for this vessel type, without any significant imbalance, thus providing some support for the stable recovery of the BDI.

The Very Large Bulk Carrier Index (BSI) was weak, falling 22 points, or 1.7%, to close at 1290 points, making it the only one of the three sub-indices to decline. Supramax vessels, with a deadweight tonnage between 45,000 and 70,000 tons, transport a diverse range of cargoes, including not only bulk commodities like coal and grain but also various smaller bulk commodities. The decline in freight rates was mainly due to weak demand for smaller bulk cargo transportation, coupled with some capacity returning from other routes, leading to a relative oversupply in the market. This dragged down the index's performance and, to some extent, offset the positive impact of rising Capesize vessel freight rates.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.