With the Federal Reserve's interest rate decision approaching, the dot plot is becoming the focus of attention.

2026-03-18 16:47:23

According to APP, Daniel Lavney, head of fixed income at Mediolanum International Fund Management, stated that the market had already anticipated the Federal Reserve would keep interest rates unchanged at this week's meeting, even before the escalation of the Gulf situation, and this is now a foregone conclusion. Recent economic data showed continued slowing inflation and a deteriorating labor market, leading the firm to initially expect a dovish stance. However, this is no longer the case. The Fed is now expected to convey a cautious wait-and-see attitude. The policy statement is likely to mention conflict risks and add two-sided language to its description of the future path of interest rates, emphasizing both the upside risks to inflation and the downside risks to the labor market.

Bei Chen Lin , senior investment strategist at Russell Investments , stated that the fundamentals of the US economy remain solid, meaning the threshold for further interest rate cuts by the Federal Reserve is likely high. He anticipates only one rate cut in the second half of this year, or even none until 2027. Given that even if energy prices temporarily push up inflation, a balanced labor market and subdued housing inflation cap the upside potential, a rate hike this year is unlikely. He expects the Fed to keep rates unchanged this time, and any hints from Powell regarding the future path of interest rates will be crucial.

Phil Newhart, head of markets and economics research at First Citizens , said investors and markets will be paying particular attention to the median forecast for the federal funds rate at the end of 2026. This is difficult to predict, but we believe the median will continue to indicate only one rate cut for the remainder of the year. In addition to the Federal Open Market Committee's forecasts, the tone of Powell 's press conference will be a key variable influencing the market, especially how he will address the contradiction between the recent surge in oil prices and weak labor market data.

The latest CME FedWatch data shows that the probability of maintaining the 3.50%-3.75% interest rate range at the March 18 meeting is as high as 99.9%. The expectation of a rate cut in 2026 has been reduced from two at the beginning of the year to only one, with the first rate cut expected to be postponed to the second half of the year.

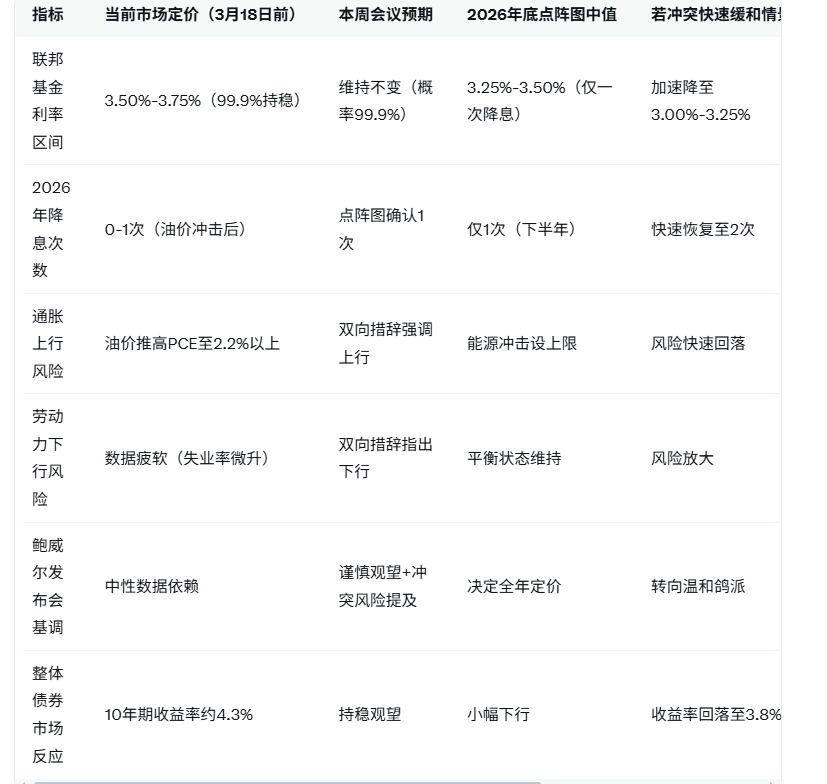

To clearly compare the expected path with its multi-dimensional impacts, the following table presents key indicators (including pricing evolution, dot plot midpoint, inflation and labor risk transmission, conflict scenario assumptions, and the core views of three experts):

From an in-depth analysis perspective, the Middle East conflict directly amplifies the uncertainty of imported inflation through oil prices. Daniel Lavney explicitly pointed out that the originally expected dovish stance has shifted to a cautious wait-and-see approach, and the addition of two-way language in the policy statement is precisely to balance the risks of rising inflation and declining labor market. BeiChen Lin further emphasized that the fundamentals of the US economy are solid, and the balanced labor market and suppressed housing inflation set a natural ceiling for inflation. Therefore, the probability of a rate hike throughout the year is close to zero, but the threshold for a rate cut has been significantly raised. Phil Newhart focused on the midpoint of the dot plot at the end of 2026, believing that it will continue to anchor to a path of only one rate cut, and how Powell responds to the contradiction of "soaring oil prices vs. weak labor market" will be the core of market pricing. It is reasonable to speculate that if the conflict eases in mid-to-late April, the market can repric an additional rate cut within a few days after the dot plot, pushing long-term bond yields down by 20-30 basis points; conversely, continued oil price pressure will force the Fed to maintain a "higher and longer" stance, significantly amplifying bond volatility.

On the other hand, the resilience of the US economy provides a buffer, and housing and wage data have mitigated the risk of an inflationary spiral. The consensus among the three experts indicates that while the meeting maintained interest rates unchanged, the communication strategy shifted from "dovish expectations" to "data-dependent + geopolitical caution," leaving room for gradual easing while avoiding premature easing that could lead to market misjudgments.

Editor's Summary : While the Middle East conflict has increased inflation uncertainty, the Federal Reserve maintained interest rates this week and conveyed a cautious wait-and-see approach through its dot plot and two-way wording, reflecting a prudent framework that balances a solid economic foundation with risks. The future path depends on the evolution of the conflict and data validation; market participants should closely monitor the midpoint of the dot plot and the tone of the press conference.

Frequently Asked Questions

Q1: Why is it a foregone conclusion that the Federal Reserve will keep interest rates unchanged this week, and why has the previously expected dovish stance changed?

A: Daniel Lavney points out that the market had already priced in stability before the conflict escalated, but the surge in oil prices directly complicated the inflation outlook, causing dovish expectations to be replaced by cautious wait-and-see. CME data shows a 99.9% probability of maintaining the 3.50%-3.75% level, and the policy statement will add wording regarding two-way risks, both to guard against rising inflation and to take into account declining labor costs, avoiding any unilateral signals that could mislead the market.

Q2: Why is the midpoint of the dot plot at the end of 2026 expected to show only one interest rate cut? How was the threshold for interest rate cuts raised?

A: BeiChen Lin emphasized that the fundamentals of the US economy are solid, and that a balanced labor force and subdued housing inflation limit the upside potential for inflation. Therefore, the number of rate cuts this year will be reduced to one or even fewer. Phil Newhart added that investors will pay particular attention to this median; maintaining a one-time rate cut path will solidify the "higher and longer" framework and raise the threshold for further easing.

Q3: How will the tone of Powell's press conference affect the market, especially when addressing the conflict between oil prices and labor?

A: All three experts agree that this is a key variable influencing the market. Phil Newhart points out that Powell needs to balance the inflationary risks from rising oil prices with the downward pressure from a weak labor market. Any indication that he ignores supply shocks could trigger a bond market rebound, while conversely, it would reinforce hawkish pricing, leading to higher yields.

Q4: If the conflict in the Middle East eases rapidly, how will the expectation of interest rate cuts be repriced and what will be the impact on the bond market?

A: Daniel Lavney clearly stated that the anticipated rate cuts will quickly resume, and the market may make up for an additional rate cut within 1-2 weeks after the dot plot, pushing the 10-year Treasury yield down to around 3.8%, which is beneficial for fixed-income assets. However, given the current oil price shock, a clear easing signal is needed to trigger this rebound.

Bei Chen Lin , senior investment strategist at Russell Investments , stated that the fundamentals of the US economy remain solid, meaning the threshold for further interest rate cuts by the Federal Reserve is likely high. He anticipates only one rate cut in the second half of this year, or even none until 2027. Given that even if energy prices temporarily push up inflation, a balanced labor market and subdued housing inflation cap the upside potential, a rate hike this year is unlikely. He expects the Fed to keep rates unchanged this time, and any hints from Powell regarding the future path of interest rates will be crucial.

Phil Newhart, head of markets and economics research at First Citizens , said investors and markets will be paying particular attention to the median forecast for the federal funds rate at the end of 2026. This is difficult to predict, but we believe the median will continue to indicate only one rate cut for the remainder of the year. In addition to the Federal Open Market Committee's forecasts, the tone of Powell 's press conference will be a key variable influencing the market, especially how he will address the contradiction between the recent surge in oil prices and weak labor market data.

The latest CME FedWatch data shows that the probability of maintaining the 3.50%-3.75% interest rate range at the March 18 meeting is as high as 99.9%. The expectation of a rate cut in 2026 has been reduced from two at the beginning of the year to only one, with the first rate cut expected to be postponed to the second half of the year.

To clearly compare the expected path with its multi-dimensional impacts, the following table presents key indicators (including pricing evolution, dot plot midpoint, inflation and labor risk transmission, conflict scenario assumptions, and the core views of three experts):

From an in-depth analysis perspective, the Middle East conflict directly amplifies the uncertainty of imported inflation through oil prices. Daniel Lavney explicitly pointed out that the originally expected dovish stance has shifted to a cautious wait-and-see approach, and the addition of two-way language in the policy statement is precisely to balance the risks of rising inflation and declining labor market. BeiChen Lin further emphasized that the fundamentals of the US economy are solid, and the balanced labor market and suppressed housing inflation set a natural ceiling for inflation. Therefore, the probability of a rate hike throughout the year is close to zero, but the threshold for a rate cut has been significantly raised. Phil Newhart focused on the midpoint of the dot plot at the end of 2026, believing that it will continue to anchor to a path of only one rate cut, and how Powell responds to the contradiction of "soaring oil prices vs. weak labor market" will be the core of market pricing. It is reasonable to speculate that if the conflict eases in mid-to-late April, the market can repric an additional rate cut within a few days after the dot plot, pushing long-term bond yields down by 20-30 basis points; conversely, continued oil price pressure will force the Fed to maintain a "higher and longer" stance, significantly amplifying bond volatility.

On the other hand, the resilience of the US economy provides a buffer, and housing and wage data have mitigated the risk of an inflationary spiral. The consensus among the three experts indicates that while the meeting maintained interest rates unchanged, the communication strategy shifted from "dovish expectations" to "data-dependent + geopolitical caution," leaving room for gradual easing while avoiding premature easing that could lead to market misjudgments.

Editor's Summary : While the Middle East conflict has increased inflation uncertainty, the Federal Reserve maintained interest rates this week and conveyed a cautious wait-and-see approach through its dot plot and two-way wording, reflecting a prudent framework that balances a solid economic foundation with risks. The future path depends on the evolution of the conflict and data validation; market participants should closely monitor the midpoint of the dot plot and the tone of the press conference.

Frequently Asked Questions

Q1: Why is it a foregone conclusion that the Federal Reserve will keep interest rates unchanged this week, and why has the previously expected dovish stance changed?

A: Daniel Lavney points out that the market had already priced in stability before the conflict escalated, but the surge in oil prices directly complicated the inflation outlook, causing dovish expectations to be replaced by cautious wait-and-see. CME data shows a 99.9% probability of maintaining the 3.50%-3.75% level, and the policy statement will add wording regarding two-way risks, both to guard against rising inflation and to take into account declining labor costs, avoiding any unilateral signals that could mislead the market.

Q2: Why is the midpoint of the dot plot at the end of 2026 expected to show only one interest rate cut? How was the threshold for interest rate cuts raised?

A: BeiChen Lin emphasized that the fundamentals of the US economy are solid, and that a balanced labor force and subdued housing inflation limit the upside potential for inflation. Therefore, the number of rate cuts this year will be reduced to one or even fewer. Phil Newhart added that investors will pay particular attention to this median; maintaining a one-time rate cut path will solidify the "higher and longer" framework and raise the threshold for further easing.

Q3: How will the tone of Powell's press conference affect the market, especially when addressing the conflict between oil prices and labor?

A: All three experts agree that this is a key variable influencing the market. Phil Newhart points out that Powell needs to balance the inflationary risks from rising oil prices with the downward pressure from a weak labor market. Any indication that he ignores supply shocks could trigger a bond market rebound, while conversely, it would reinforce hawkish pricing, leading to higher yields.

Q4: If the conflict in the Middle East eases rapidly, how will the expectation of interest rate cuts be repriced and what will be the impact on the bond market?

A: Daniel Lavney clearly stated that the anticipated rate cuts will quickly resume, and the market may make up for an additional rate cut within 1-2 weeks after the dot plot, pushing the 10-year Treasury yield down to around 3.8%, which is beneficial for fixed-income assets. However, given the current oil price shock, a clear easing signal is needed to trigger this rebound.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.