The IMF warns of an economic recession, yet central banks can only raise interest rates in the opposite direction.

2026-03-20 16:28:09

As geopolitical conflicts in the Middle East continued to escalate on March 20, energy prices soared, prompting the International Monetary Fund (IMF) to issue a series of warnings that global inflation and growth prospects faced significant downward pressure.

At the same time, the US labor market, the core engine of the global economy, continued to cool down, the monetary policies of major central banks diverged rapidly, and the global financial market and exchange rate landscape ushered in a significant turning point.

The International Monetary Fund recently warned that continued rises in energy prices will exacerbate global inflationary pressures and hinder the pace of economic recovery.

The IMF is closely monitoring the conflict in Iran and the disruptions to energy production and maritime logistics. It has noted that the current conflict has severely impacted maritime oil and gas transport, pushing international crude oil prices up by more than 50%, with Brent crude oil stabilizing above $100 per barrel.

IMF spokesperson Julie Kozak stated that the agency has not yet received formal emergency financing requests from member countries, but is prepared to provide support at any time and is maintaining close communication with finance ministers, central bank governors, and regional financial institutions.

She emphasized that the overall economic impact of the conflict depends on its duration, intensity, and scope, and that the assessment will be incorporated into the latest Global Economic Outlook report to be released at the IMF and World Bank Spring Meetings in mid-April.

According to IMF estimates, if energy prices rise by 10% and continue for a year, it will push up global inflation by 40 basis points and cause economic output to fall by 0.1% to 0.2%; if oil prices remain above $100 throughout the year, it will have a significant impact on global inflation and economic growth.

Kozak advised central banks to be highly vigilant and closely monitor whether inflationary pressures spread to non-energy sectors and whether inflation expectations remain stable.

The IMF's initial assessment suggests that this round of conflict will dampen economic growth in the Gulf Cooperation Council countries, with the ultimate impact depending on the countries' ability to resume oil and gas exports.

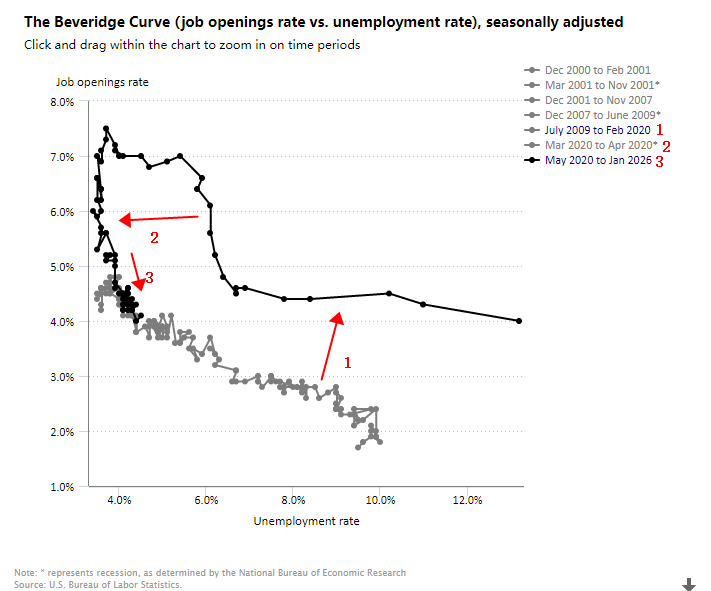

As the core engine of the global economy, the US labor market is showing a clear cooling trend, which can be more clearly revealed by looking at the Beveridge curve.

The Beveridge curve reflects the negative correlation between job vacancy rate and unemployment rate, and changes in the curve can intuitively reflect the tightness of the labor market and matching efficiency.

(Beveridge Curve, Source: U.S. Department of Labor)

As can be seen from the curves, affected by the pandemic, curve 1 deteriorated rapidly towards curve 2. Afterwards, the labor market recovered but remained around curve 3, meaning that at the same unemployment rate, the job vacancy rate continued to decline, reflecting the weakening of labor market matching efficiency.

With no significant improvement in non-farm payrolls, this means that while the unemployment rate appears stable, businesses are showing signs of slowing hiring, the supply of effective jobs is shrinking, and the actual activity in the labor market is declining.

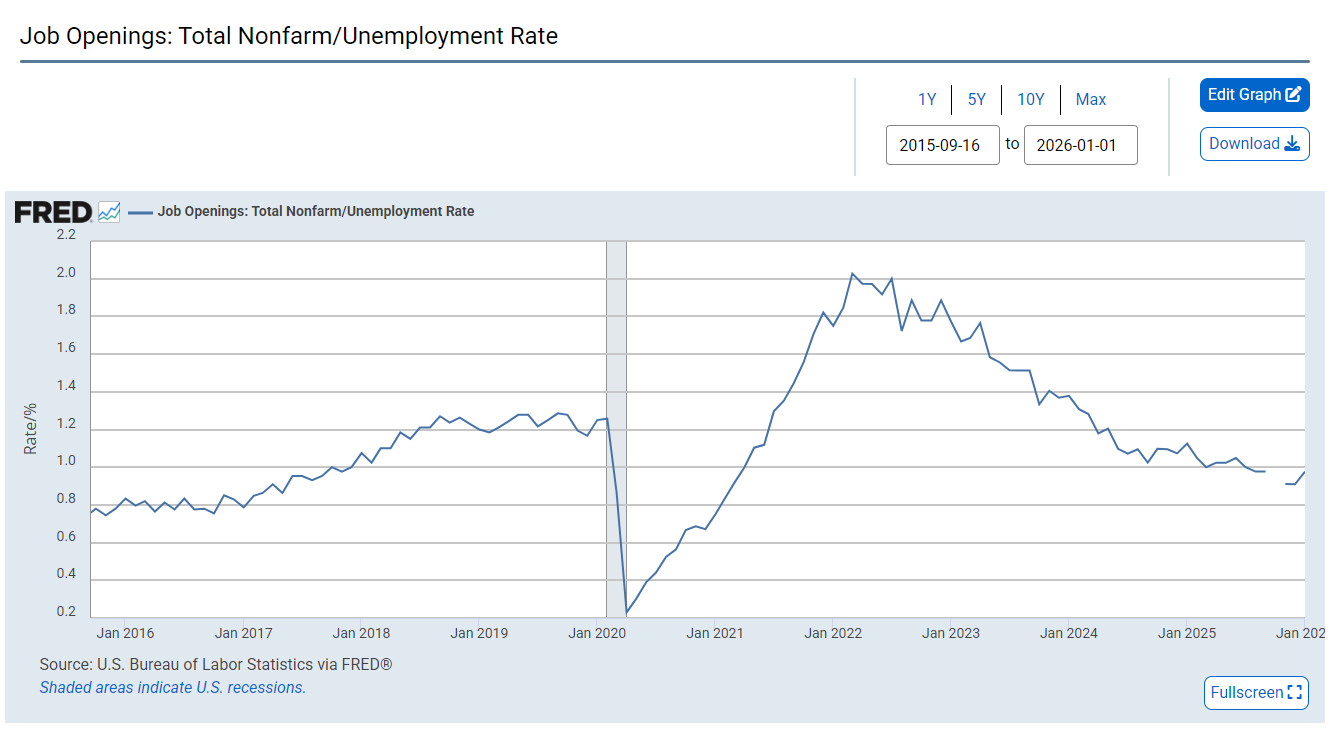

The current US labor market is showing a simultaneous decline in the number of job openings and the number of employed people, with the number of job openings declining at a faster rate. This indicates that companies' willingness to hire has weakened significantly, and the labor market is gradually slowing down from its previous overheated state.

(Ratio of employed persons to unemployment rate, Source: Federal Reserve)

The chart above shows a continued contraction in the labor market, with the gray area representing the period during the pandemic.

The rapid decline in job vacancies and sluggish employment growth indicate weakening household income and consumption momentum, and a decrease in endogenous economic growth. However, due to rising energy prices, the US PPI rose in February ahead of the war, and the Federal Reserve also raised its inflation expectations, making the Fed more cautious in its policy choices and less likely to easily shift to easing.

The surge in energy prices has completely rewritten global interest rate expectations, leading to a significant divergence in the policy stances of major central banks. The Federal Reserve has become the only major central bank this year that is not expected to raise interest rates by the market.

Before the conflict broke out at the end of February, the market generally bet that the Federal Reserve would cut interest rates twice this year. Now, this expectation has cooled down significantly, and even one rate cut this year is considered unlikely.

The Federal Reserve held rates steady this week as expected, with Chairman Powell acknowledging that it is not yet possible to assess the breadth and duration of the economic impact of the conflict.

In stark contrast, other major central banks around the world have rapidly shifted their policy stances to a hawkish one:

The European Central Bank held rates steady on Thursday but warned of inflation risks stemming from energy prices, and policymakers may begin discussions on raising rates next month, with the market already pricing in a rate hike before June.

The Bank of England also kept interest rates unchanged, but sent a strong signal that it could take action at any time, leading to an unusual sell-off in short-term UK bonds. The market has shifted from expecting a rate cut to pricing in an 80 basis point rate hike before the end of the year.

The Bank of Japan hinted on Thursday that it might raise interest rates as early as April, breaking the market consensus that the yen would continue to weaken and directly driving a sharp rebound in the yen.

The Reserve Bank of Australia raised interest rates for the second time in two months, and the market generally expects further rate hikes, supporting the strengthening of the Australian dollar.

The deteriorating US labor market, coupled with the inability to cut interest rates, and the fact that major global economies, including Japan and Australia, have better economic data than the US, are generally shifting towards a hawkish stance, which is likely to impact global economic growth.

Affected by the divergence in global central bank policies, the US dollar retreated from its multi-month high this week, with the dollar index holding steady at 99.46. It is expected to fall by 1% this week, marking its largest weekly decline since the end of January.

The euro, yen, pound, Swiss franc, and Australian dollar all strengthened against the US dollar this week: the euro dipped slightly to 1.1558 in early Asian trading, but rose 1.2% for the week; the yen fell back to around 158, but rose 0.9% for the week; the pound held steady at 1.3408, but rose 1.4% for the week; and the Australian dollar approached the 0.71 mark on Friday, with a weekly gain of 1.5%.

However, most institutions believe that the dollar is unlikely to continue to weaken. Commonwealth Bank of Australia currency strategist Carole Kong said that the longer the conflict lasts, the stronger the dollar is likely to be. On the one hand, the dollar will benefit from the influx of safe-haven funds, and on the other hand, the United States, as an energy exporter, will also directly benefit from high oil prices.

(US Dollar Index Daily Chart, Source: FX678)

International oil prices retreated slightly on Friday after Trump demanded that Israel stop attacking Iranian energy facilities, while Bessant said the U.S. might soon lift sanctions on Iranian oil stranded on tankers and hinted at the possible release of additional crude oil reserves, providing temporary relief to the energy market.

Trump ruled out the possibility of deploying ground troops, and Israel pledged to postpone further strikes against a key Iranian gas field.

However, the mutual attacks between the two sides had already paralyzed a natural gas facility in Qatar. Qatari Energy Minister and CEO of Qatar Energy Company, Saad al-Qabi, said on the 19th that the Iranian attack affected 17% of Qatar's liquefied natural gas export capacity, which is estimated to cause an annual revenue loss of about $20 billion.

Significant uncertainties remain regarding key energy export routes in the Middle East, and high and volatile energy prices will continue to be a core variable affecting the global economy and central bank policies.

At the same time, the US labor market, the core engine of the global economy, continued to cool down, the monetary policies of major central banks diverged rapidly, and the global financial market and exchange rate landscape ushered in a significant turning point.

IMF warns: High energy prices will push up inflation and suppress global growth.

The International Monetary Fund recently warned that continued rises in energy prices will exacerbate global inflationary pressures and hinder the pace of economic recovery.

The IMF is closely monitoring the conflict in Iran and the disruptions to energy production and maritime logistics. It has noted that the current conflict has severely impacted maritime oil and gas transport, pushing international crude oil prices up by more than 50%, with Brent crude oil stabilizing above $100 per barrel.

IMF spokesperson Julie Kozak stated that the agency has not yet received formal emergency financing requests from member countries, but is prepared to provide support at any time and is maintaining close communication with finance ministers, central bank governors, and regional financial institutions.

She emphasized that the overall economic impact of the conflict depends on its duration, intensity, and scope, and that the assessment will be incorporated into the latest Global Economic Outlook report to be released at the IMF and World Bank Spring Meetings in mid-April.

According to IMF estimates, if energy prices rise by 10% and continue for a year, it will push up global inflation by 40 basis points and cause economic output to fall by 0.1% to 0.2%; if oil prices remain above $100 throughout the year, it will have a significant impact on global inflation and economic growth.

Kozak advised central banks to be highly vigilant and closely monitor whether inflationary pressures spread to non-energy sectors and whether inflation expectations remain stable.

The IMF's initial assessment suggests that this round of conflict will dampen economic growth in the Gulf Cooperation Council countries, with the ultimate impact depending on the countries' ability to resume oil and gas exports.

US Labor Market Slows: Weakening Employment Momentum as Seen Through the Beveridge Curve

As the core engine of the global economy, the US labor market is showing a clear cooling trend, which can be more clearly revealed by looking at the Beveridge curve.

The Beveridge curve reflects the negative correlation between job vacancy rate and unemployment rate, and changes in the curve can intuitively reflect the tightness of the labor market and matching efficiency.

(Beveridge Curve, Source: U.S. Department of Labor)

As can be seen from the curves, affected by the pandemic, curve 1 deteriorated rapidly towards curve 2. Afterwards, the labor market recovered but remained around curve 3, meaning that at the same unemployment rate, the job vacancy rate continued to decline, reflecting the weakening of labor market matching efficiency.

With no significant improvement in non-farm payrolls, this means that while the unemployment rate appears stable, businesses are showing signs of slowing hiring, the supply of effective jobs is shrinking, and the actual activity in the labor market is declining.

The current US labor market is showing a simultaneous decline in the number of job openings and the number of employed people, with the number of job openings declining at a faster rate. This indicates that companies' willingness to hire has weakened significantly, and the labor market is gradually slowing down from its previous overheated state.

(Ratio of employed persons to unemployment rate, Source: Federal Reserve)

The chart above shows a continued contraction in the labor market, with the gray area representing the period during the pandemic.

The rapid decline in job vacancies and sluggish employment growth indicate weakening household income and consumption momentum, and a decrease in endogenous economic growth. However, due to rising energy prices, the US PPI rose in February ahead of the war, and the Federal Reserve also raised its inflation expectations, making the Fed more cautious in its policy choices and less likely to easily shift to easing.

Global central bank policy shift: The Federal Reserve remains on the sidelines, while many other countries accelerate their hawkish turn.

The surge in energy prices has completely rewritten global interest rate expectations, leading to a significant divergence in the policy stances of major central banks. The Federal Reserve has become the only major central bank this year that is not expected to raise interest rates by the market.

Before the conflict broke out at the end of February, the market generally bet that the Federal Reserve would cut interest rates twice this year. Now, this expectation has cooled down significantly, and even one rate cut this year is considered unlikely.

The Federal Reserve held rates steady this week as expected, with Chairman Powell acknowledging that it is not yet possible to assess the breadth and duration of the economic impact of the conflict.

In stark contrast, other major central banks around the world have rapidly shifted their policy stances to a hawkish one:

The European Central Bank held rates steady on Thursday but warned of inflation risks stemming from energy prices, and policymakers may begin discussions on raising rates next month, with the market already pricing in a rate hike before June.

The Bank of England also kept interest rates unchanged, but sent a strong signal that it could take action at any time, leading to an unusual sell-off in short-term UK bonds. The market has shifted from expecting a rate cut to pricing in an 80 basis point rate hike before the end of the year.

The Bank of Japan hinted on Thursday that it might raise interest rates as early as April, breaking the market consensus that the yen would continue to weaken and directly driving a sharp rebound in the yen.

The Reserve Bank of Australia raised interest rates for the second time in two months, and the market generally expects further rate hikes, supporting the strengthening of the Australian dollar.

The deteriorating US labor market, coupled with the inability to cut interest rates, and the fact that major global economies, including Japan and Australia, have better economic data than the US, are generally shifting towards a hawkish stance, which is likely to impact global economic growth.

The currency market landscape is shifting: the US dollar is weakening in the short term, but its safe-haven appeal remains.

Affected by the divergence in global central bank policies, the US dollar retreated from its multi-month high this week, with the dollar index holding steady at 99.46. It is expected to fall by 1% this week, marking its largest weekly decline since the end of January.

The euro, yen, pound, Swiss franc, and Australian dollar all strengthened against the US dollar this week: the euro dipped slightly to 1.1558 in early Asian trading, but rose 1.2% for the week; the yen fell back to around 158, but rose 0.9% for the week; the pound held steady at 1.3408, but rose 1.4% for the week; and the Australian dollar approached the 0.71 mark on Friday, with a weekly gain of 1.5%.

However, most institutions believe that the dollar is unlikely to continue to weaken. Commonwealth Bank of Australia currency strategist Carole Kong said that the longer the conflict lasts, the stronger the dollar is likely to be. On the one hand, the dollar will benefit from the influx of safe-haven funds, and on the other hand, the United States, as an energy exporter, will also directly benefit from high oil prices.

(US Dollar Index Daily Chart, Source: FX678)

Geopolitical tensions have eased slightly, but energy volatility continues to impact the global economy.

International oil prices retreated slightly on Friday after Trump demanded that Israel stop attacking Iranian energy facilities, while Bessant said the U.S. might soon lift sanctions on Iranian oil stranded on tankers and hinted at the possible release of additional crude oil reserves, providing temporary relief to the energy market.

Trump ruled out the possibility of deploying ground troops, and Israel pledged to postpone further strikes against a key Iranian gas field.

However, the mutual attacks between the two sides had already paralyzed a natural gas facility in Qatar. Qatari Energy Minister and CEO of Qatar Energy Company, Saad al-Qabi, said on the 19th that the Iranian attack affected 17% of Qatar's liquefied natural gas export capacity, which is estimated to cause an annual revenue loss of about $20 billion.

Significant uncertainties remain regarding key energy export routes in the Middle East, and high and volatile energy prices will continue to be a core variable affecting the global economy and central bank policies.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.