A chart shows that the Baltic Dry Index is softening, with freight rates declining across all ship types.

2026-03-30 22:46:39

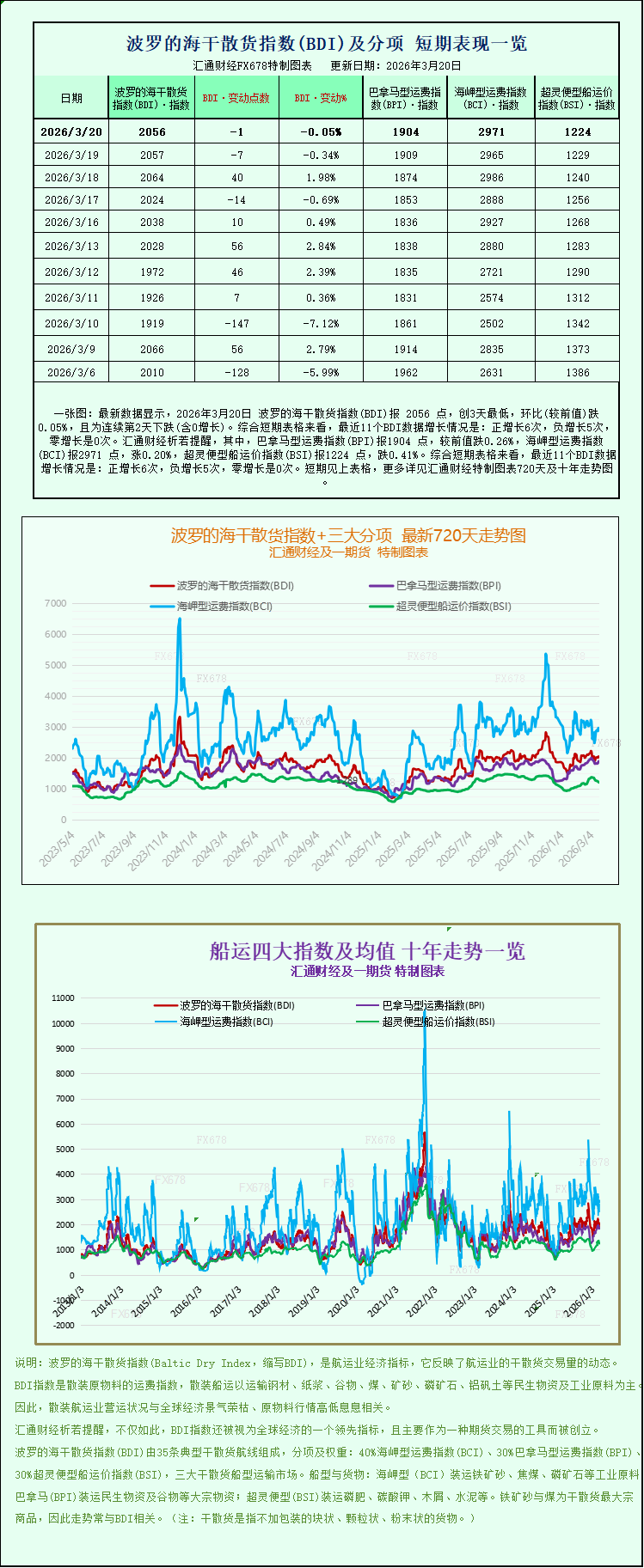

The latest data shows that on March 30, 2026, the Baltic Dry Index (BDI) was 2017 points, a decrease of 0.69% compared to the previous period, marking the largest drop in four days. Looking at the short-term charts, the BDI saw positive growth 5 times, negative growth 6 times, and zero growth 0 times in the last 11 BDI data points. Specifically, the Panamax Freight Index (BPI) was 1742 points, down 0.80% from the previous period; the Capesize Freight Index (BCI) was 3004 points, down 0.92%; and the Supramax Freight Index (BSI) was 1203 points, down 0.25%. For detailed 720-day and 10-year trend charts of the Baltic Dry Index and its three main sub-indices, please refer to the specially designed charts.

Recently, the Baltic Dry Index (BDI) has shown a significant weakening trend, with freight rates across all vessel types declining to varying degrees, ending a two-day winning streak and reflecting a short-term adjustment in the dry bulk shipping market. As a core indicator of the global dry bulk shipping market, the BDI primarily monitors freight rates for vessels transporting dry bulk commodities such as coal, iron ore, and grain. Its fluctuations directly reflect the dynamic changes in global dry bulk shipping demand and supply, attracting widespread attention from the shipping industry, commodity traders, and investors.

Specifically, on Monday, the Baltic Dry Index, which tracks freight rates for the three main vessel types—Capesize, Panamax, and Supramax—fell, down 14 points, or 0.7%, from the previous trading day, closing at 2017 points. While this decline wasn't significant, it broke the recent pattern of slight increases, highlighting the market's cautious short-term sentiment regarding dry bulk shipping demand.

The Capesize vessel index (primarily corresponding to Capesize vessels) saw a more pronounced decline, falling 28 points, or approximately 0.9%, to close at 3004 points. It's worth noting that this index had climbed to a three-week high last Friday, and this pullback indicates a temporary cooling in the Capesize shipping market. Capesize vessels, as large ships in dry bulk shipping, are typically used to transport 150,000 tons of bulk commodities, primarily iron ore and coal. Their freight rates are closely linked to global steel industry demand and coal energy consumption. Affected by the index decline, the average daily earnings of Capesize vessels also saw a slight decrease, falling by $249 to $23,745 per day.

Echoing the decline in Capesize freight rates, global iron ore futures prices have recently traded within a narrow range, without forming a clear upward or downward trend. Currently, investors are focusing on assessing the combined impact of multiple factors on the iron ore market. On the one hand, high energy prices are putting upward pressure on transportation and production costs; on the other hand, there are expectations of a recovery in demand from China's steel industry. Meanwhile, the current high levels of iron ore inventory at ports are also exerting downward pressure on iron ore prices, indirectly affecting iron ore transportation demand and dragging down Capesize freight rates.

Besides Capesize vessels, the Panamax index also fell, dropping 14 points, or 0.8%, to close at 1742 points, near its lowest point in seven weeks, indicating a weak market for this vessel type. Panamax vessels are medium-sized dry bulk carriers, typically carrying 60,000 to 70,000 tons of cargo, mainly coal and grain. Their freight rates are closely linked to global grain trade and coal import/export demand. Along with the index decline, the average daily earnings of Panamax vessels also decreased, falling by $118 to $15,682 per day, reflecting insufficient demand for medium-sized dry bulk shipping.

Although the Supramax bulk carrier index saw a relatively smaller decline, it also showed a downward trend, falling 3 points, or 0.3%, to close at 1203 points. Supramax bulk carriers, with their flexible navigation advantages, are mainly used to transport small batches of dry bulk cargo and cover a wider range of routes, resulting in relatively stable freight rate fluctuations. However, they were not spared this time, further confirming the current softening trend in the overall dry bulk shipping market.

From the perspective of the overall shipping market environment, the changes in the international geopolitical situation on Monday also had a certain indirect impact on the shipping market. On that day, Iran responded to the US proposal to end the conflict, deeming it unrealistic, illogical, and excessive, and launched a new round of missiles at Israel. Meanwhile, since the Houthi rebels intervened in the conflict in Yemen, global oil prices have further increased. This price surge not only increases fuel costs for shipping but also further threatens already disrupted global shipping routes. Currently, the Strait of Hormuz is effectively closed, preventing oil from flowing through the crucial Suez Canal via the Red Sea. While this shipping bottleneck primarily affects oil transport, it has also had a ripple effect on overall confidence and capacity allocation in the global shipping market, indirectly impacting expectations in the dry bulk shipping market.

Overall, the recent softening of the Baltic Dry Index (BDI) is a result of simultaneous declines in freight rates across all vessel types. This is related to market demand and price fluctuations in core dry bulk commodities, as well as indirect influences from global shipping costs and geopolitical situations. Going forward, the BDI and freight rates for various vessel types may experience further fluctuations as global commodity demand changes, energy price trends shift, and shipping lanes become more precarious.

Recently, the Baltic Dry Index (BDI) has shown a significant weakening trend, with freight rates across all vessel types declining to varying degrees, ending a two-day winning streak and reflecting a short-term adjustment in the dry bulk shipping market. As a core indicator of the global dry bulk shipping market, the BDI primarily monitors freight rates for vessels transporting dry bulk commodities such as coal, iron ore, and grain. Its fluctuations directly reflect the dynamic changes in global dry bulk shipping demand and supply, attracting widespread attention from the shipping industry, commodity traders, and investors.

Specifically, on Monday, the Baltic Dry Index, which tracks freight rates for the three main vessel types—Capesize, Panamax, and Supramax—fell, down 14 points, or 0.7%, from the previous trading day, closing at 2017 points. While this decline wasn't significant, it broke the recent pattern of slight increases, highlighting the market's cautious short-term sentiment regarding dry bulk shipping demand.

The Capesize vessel index (primarily corresponding to Capesize vessels) saw a more pronounced decline, falling 28 points, or approximately 0.9%, to close at 3004 points. It's worth noting that this index had climbed to a three-week high last Friday, and this pullback indicates a temporary cooling in the Capesize shipping market. Capesize vessels, as large ships in dry bulk shipping, are typically used to transport 150,000 tons of bulk commodities, primarily iron ore and coal. Their freight rates are closely linked to global steel industry demand and coal energy consumption. Affected by the index decline, the average daily earnings of Capesize vessels also saw a slight decrease, falling by $249 to $23,745 per day.

Echoing the decline in Capesize freight rates, global iron ore futures prices have recently traded within a narrow range, without forming a clear upward or downward trend. Currently, investors are focusing on assessing the combined impact of multiple factors on the iron ore market. On the one hand, high energy prices are putting upward pressure on transportation and production costs; on the other hand, there are expectations of a recovery in demand from China's steel industry. Meanwhile, the current high levels of iron ore inventory at ports are also exerting downward pressure on iron ore prices, indirectly affecting iron ore transportation demand and dragging down Capesize freight rates.

Besides Capesize vessels, the Panamax index also fell, dropping 14 points, or 0.8%, to close at 1742 points, near its lowest point in seven weeks, indicating a weak market for this vessel type. Panamax vessels are medium-sized dry bulk carriers, typically carrying 60,000 to 70,000 tons of cargo, mainly coal and grain. Their freight rates are closely linked to global grain trade and coal import/export demand. Along with the index decline, the average daily earnings of Panamax vessels also decreased, falling by $118 to $15,682 per day, reflecting insufficient demand for medium-sized dry bulk shipping.

Although the Supramax bulk carrier index saw a relatively smaller decline, it also showed a downward trend, falling 3 points, or 0.3%, to close at 1203 points. Supramax bulk carriers, with their flexible navigation advantages, are mainly used to transport small batches of dry bulk cargo and cover a wider range of routes, resulting in relatively stable freight rate fluctuations. However, they were not spared this time, further confirming the current softening trend in the overall dry bulk shipping market.

From the perspective of the overall shipping market environment, the changes in the international geopolitical situation on Monday also had a certain indirect impact on the shipping market. On that day, Iran responded to the US proposal to end the conflict, deeming it unrealistic, illogical, and excessive, and launched a new round of missiles at Israel. Meanwhile, since the Houthi rebels intervened in the conflict in Yemen, global oil prices have further increased. This price surge not only increases fuel costs for shipping but also further threatens already disrupted global shipping routes. Currently, the Strait of Hormuz is effectively closed, preventing oil from flowing through the crucial Suez Canal via the Red Sea. While this shipping bottleneck primarily affects oil transport, it has also had a ripple effect on overall confidence and capacity allocation in the global shipping market, indirectly impacting expectations in the dry bulk shipping market.

Overall, the recent softening of the Baltic Dry Index (BDI) is a result of simultaneous declines in freight rates across all vessel types. This is related to market demand and price fluctuations in core dry bulk commodities, as well as indirect influences from global shipping costs and geopolitical situations. Going forward, the BDI and freight rates for various vessel types may experience further fluctuations as global commodity demand changes, energy price trends shift, and shipping lanes become more precarious.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.