The BRICS nations' massive gold hoarding has swelled to 17.4% of global reserves, posing an unprecedented crisis to the dollar's hegemony.

2026-04-08 09:56:55

A global wave of central bank gold purchases is reshaping the international financial landscape. The BRICS countries' share of gold reserves has surged from 11.2% in 2019 to 17.4% currently, while the US dollar's share of global reserves has fallen to its lowest level since 1994. This structural shift not only reflects emerging economies' strategic adjustments to the traditional monetary system but also highlights the unique appeal of gold as a safe-haven asset.

According to a recent analysis report by Michael Harris, a technical analyst at EBC Financial Group, this trend is accelerating at a pace that exceeds market expectations.

In an analysis report released on Tuesday (April 7), Michael Harris pointed out that global central banks have purchased more gold in the past three years than at any other time in modern history, with BRICS members playing a central role in this process. Currently, the BRICS countries collectively hold over 6,000 tons of gold, accounting for approximately 17.4% of global central bank reserves. Russia leads with 2,336 tons, followed by a major Asian power with 2,298 tons, and India with 880 tons. Russia and the major Asian power together account for approximately 74% of the group's total gold holdings.

He stated that in the first nine months of 2025, BRICS countries collectively increased their gold reserves by 663 tons, worth approximately $91 billion. Brazil also added 16 tons in September 2025, marking its first gold purchase since 2021. He emphasized that this buying activity is unidirectional and price-insensitive; sovereign buyers will continue to absorb supply regardless of whether the gold price is $4,000 or $5,000.

In 2025, central bank gold purchases exceeded the total annual mine production of several medium-sized gold-producing countries. This was not driven by speculative demand, but by clear policy. Russia, major Asian powers, India, Turkey, and Poland led this trend, with more than 40 central banks participating throughout the year.

Michael Harris specifically points out that 2022 was a key turning point in this trend. At that time, following sanctions imposed on Russia by the United States and its allies, approximately $300 billion of Russia's foreign exchange reserves were frozen. This event sent a clear warning to all central banks worldwide holding dollar assets: reserves stored in other countries' financial systems could face the risk of seizure.

Subsequently, global central bank gold purchases surged from approximately 500 tons per year before 2022 to over 1,000 tons per year for the following three years.

Michael Harris argues that the fact that gold stored in national vaults cannot be frozen or confiscated through the SWIFT system makes it the most reliable reserve asset option for central banks in the current geopolitical environment. From 2020 to 2024, central banks of BRICS member countries accounted for more than 50% of global sovereign gold purchases, demonstrating their dominant role in strategic adjustments.

In stark contrast to the rapid growth of gold reserves, the share of the US dollar in global reserves has been declining. Michael Harris, citing IMF COFER data, notes that the dollar's share has fallen from 71% in 1999 to approximately 57% by the end of 2025, marking its lowest level since 1994. While the actual holdings of dollar assets by foreign central banks have remained stable since 2014, the faster growth of reserves in the euro, yen, gold, and other non-traditional currencies has led to a continued dilution of the dollar's share.

The World Gold Council’s 2025 survey further confirms this trend: 73% of the central banks surveyed believe that the share of dollar reserves will decline further in the next five years, and 43% of central banks plan to increase their gold holdings, both of which are at record highs.

Michael Harris stated that while the decline in the dollar's share has been gradual, gold's share of official reserve assets has more than doubled from less than 10% in 2015 to over 23% currently, a trend that is clear and irreversible.

In this global transformation, Saudi Arabia, the largest economy in the Persian Gulf region, has become the most noteworthy uncertainty. Currently, Saudi Arabia holds approximately 323 tons of gold, representing only 2.6% of its total reserves.

Michael Harris points out that this proportion is significantly low for a country with over $500 billion in reserves. If Saudi Arabia were to increase its gold allocation to 5%, its required purchases would be equivalent to the total global central bank gold demand in 2026, all done by a single buyer.

While Saudi Arabia has not publicly announced specific plans to increase its gold holdings, its BRICS membership suggests a strategic repositioning. Michael Harris believes a significant increase in gold reserves is highly likely.

Michael Harris's analysis suggests that by early April 2026, gold prices will have reached nearly $4,660 per ounce, representing a more than 60% increase for the entire year of 2025. This surge has prompted several institutions to significantly raise their price forecasts, with Deutsche Bank setting a target price of $6,000, JPMorgan Chase at $6,300, Goldman Sachs at $5,400, while Société Générale considers $6,000 to be conservative.

The World Gold Council projects that central bank gold purchases will reach 750 to 850 tons in 2026, far exceeding the historical average.

He emphasized that this purchase volume accounts for approximately 20% of the global annual mine supply and exhibits a one-way, continuous inflow characteristic. Regardless of price levels, it is absorbed by sovereign buyers, thus constructing a solid structural bottom for gold prices, making each pullback more moderate than the last. Simultaneously, inflows into gold ETFs are accelerating, and insurance companies in major Asian countries have also been granted pilot quotas for gold allocation. When sovereign, institutional, and retail buyers act in unison, the supply-demand relationship will tighten rapidly in ways that are difficult to predict using traditional models.

Michael Harris further proposed three potential developments that could accelerate sovereign nations' shift away from the dollar and towards gold: First, if major Asian powers increase transparency in their gold purchases and disclose holdings exceeding expectations, it will be a direct catalyst; second, if Saudi Arabia or the UAE formally announces an increase in their gold allocations, it will confirm that new BRICS members are following the strategic path of Russia and other major Asian powers; and third, attention should be paid to whether the share of dollar reserves in the next IMF COFER report will decline further, as each decline will reinforce the global narrative driving sovereign gold demand.

Overall , the shift from dollar reserves to gold reserves is no longer a prediction, but an established trend fully supported by data. Since 2022, over 3,000 tons of gold have flowed into sovereign treasuries, with more than 40 central banks participating. While the dollar remains dominant, central banks are accumulating an asset that foreign governments cannot freeze at an unprecedented rate. The gold price of $4,660 per ounce in early April directly reflects this reality, while price forecasts above $5,000 clearly indicate the market's judgment on future trends.

The rapid growth of gold reserves in BRICS countries is profoundly changing the global financial landscape, and the impact of this process on the international monetary system and asset allocation logic will continue to manifest in the coming years.

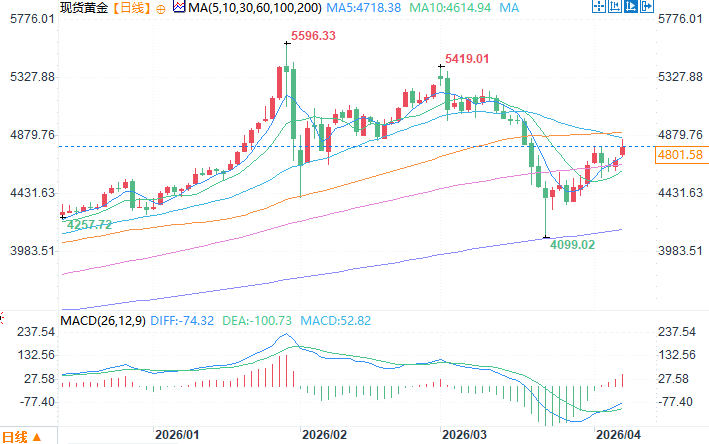

Spot gold daily chart source: EasyForex

At 9:56 AM Beijing time on April 8, spot gold was trading at $4810.58 per ounce.

According to a recent analysis report by Michael Harris, a technical analyst at EBC Financial Group, this trend is accelerating at a pace that exceeds market expectations.

The concentration of gold reserves among BRICS countries has surged rapidly.

In an analysis report released on Tuesday (April 7), Michael Harris pointed out that global central banks have purchased more gold in the past three years than at any other time in modern history, with BRICS members playing a central role in this process. Currently, the BRICS countries collectively hold over 6,000 tons of gold, accounting for approximately 17.4% of global central bank reserves. Russia leads with 2,336 tons, followed by a major Asian power with 2,298 tons, and India with 880 tons. Russia and the major Asian power together account for approximately 74% of the group's total gold holdings.

He stated that in the first nine months of 2025, BRICS countries collectively increased their gold reserves by 663 tons, worth approximately $91 billion. Brazil also added 16 tons in September 2025, marking its first gold purchase since 2021. He emphasized that this buying activity is unidirectional and price-insensitive; sovereign buyers will continue to absorb supply regardless of whether the gold price is $4,000 or $5,000.

In 2025, central bank gold purchases exceeded the total annual mine production of several medium-sized gold-producing countries. This was not driven by speculative demand, but by clear policy. Russia, major Asian powers, India, Turkey, and Poland led this trend, with more than 40 central banks participating throughout the year.

2022 became a historic turning point.

Michael Harris specifically points out that 2022 was a key turning point in this trend. At that time, following sanctions imposed on Russia by the United States and its allies, approximately $300 billion of Russia's foreign exchange reserves were frozen. This event sent a clear warning to all central banks worldwide holding dollar assets: reserves stored in other countries' financial systems could face the risk of seizure.

Subsequently, global central bank gold purchases surged from approximately 500 tons per year before 2022 to over 1,000 tons per year for the following three years.

Michael Harris argues that the fact that gold stored in national vaults cannot be frozen or confiscated through the SWIFT system makes it the most reliable reserve asset option for central banks in the current geopolitical environment. From 2020 to 2024, central banks of BRICS member countries accounted for more than 50% of global sovereign gold purchases, demonstrating their dominant role in strategic adjustments.

The share of US dollar reserves continues to decline

In stark contrast to the rapid growth of gold reserves, the share of the US dollar in global reserves has been declining. Michael Harris, citing IMF COFER data, notes that the dollar's share has fallen from 71% in 1999 to approximately 57% by the end of 2025, marking its lowest level since 1994. While the actual holdings of dollar assets by foreign central banks have remained stable since 2014, the faster growth of reserves in the euro, yen, gold, and other non-traditional currencies has led to a continued dilution of the dollar's share.

The World Gold Council’s 2025 survey further confirms this trend: 73% of the central banks surveyed believe that the share of dollar reserves will decline further in the next five years, and 43% of central banks plan to increase their gold holdings, both of which are at record highs.

Michael Harris stated that while the decline in the dollar's share has been gradual, gold's share of official reserve assets has more than doubled from less than 10% in 2015 to over 23% currently, a trend that is clear and irreversible.

Saudi Arabia becomes the biggest potential variable

In this global transformation, Saudi Arabia, the largest economy in the Persian Gulf region, has become the most noteworthy uncertainty. Currently, Saudi Arabia holds approximately 323 tons of gold, representing only 2.6% of its total reserves.

Michael Harris points out that this proportion is significantly low for a country with over $500 billion in reserves. If Saudi Arabia were to increase its gold allocation to 5%, its required purchases would be equivalent to the total global central bank gold demand in 2026, all done by a single buyer.

While Saudi Arabia has not publicly announced specific plans to increase its gold holdings, its BRICS membership suggests a strategic repositioning. Michael Harris believes a significant increase in gold reserves is highly likely.

The gold market has formed a structural bottom.

Michael Harris's analysis suggests that by early April 2026, gold prices will have reached nearly $4,660 per ounce, representing a more than 60% increase for the entire year of 2025. This surge has prompted several institutions to significantly raise their price forecasts, with Deutsche Bank setting a target price of $6,000, JPMorgan Chase at $6,300, Goldman Sachs at $5,400, while Société Générale considers $6,000 to be conservative.

The World Gold Council projects that central bank gold purchases will reach 750 to 850 tons in 2026, far exceeding the historical average.

He emphasized that this purchase volume accounts for approximately 20% of the global annual mine supply and exhibits a one-way, continuous inflow characteristic. Regardless of price levels, it is absorbed by sovereign buyers, thus constructing a solid structural bottom for gold prices, making each pullback more moderate than the last. Simultaneously, inflows into gold ETFs are accelerating, and insurance companies in major Asian countries have also been granted pilot quotas for gold allocation. When sovereign, institutional, and retail buyers act in unison, the supply-demand relationship will tighten rapidly in ways that are difficult to predict using traditional models.

Three catalysts may accelerate the transformation process

Michael Harris further proposed three potential developments that could accelerate sovereign nations' shift away from the dollar and towards gold: First, if major Asian powers increase transparency in their gold purchases and disclose holdings exceeding expectations, it will be a direct catalyst; second, if Saudi Arabia or the UAE formally announces an increase in their gold allocations, it will confirm that new BRICS members are following the strategic path of Russia and other major Asian powers; and third, attention should be paid to whether the share of dollar reserves in the next IMF COFER report will decline further, as each decline will reinforce the global narrative driving sovereign gold demand.

Overall , the shift from dollar reserves to gold reserves is no longer a prediction, but an established trend fully supported by data. Since 2022, over 3,000 tons of gold have flowed into sovereign treasuries, with more than 40 central banks participating. While the dollar remains dominant, central banks are accumulating an asset that foreign governments cannot freeze at an unprecedented rate. The gold price of $4,660 per ounce in early April directly reflects this reality, while price forecasts above $5,000 clearly indicate the market's judgment on future trends.

The rapid growth of gold reserves in BRICS countries is profoundly changing the global financial landscape, and the impact of this process on the international monetary system and asset allocation logic will continue to manifest in the coming years.

Spot gold daily chart source: EasyForex

At 9:56 AM Beijing time on April 8, spot gold was trading at $4810.58 per ounce.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.