One chart: The Baltic Dry Index hits a multi-month high, with all sectors rising in tandem.

2026-04-14 00:16:58

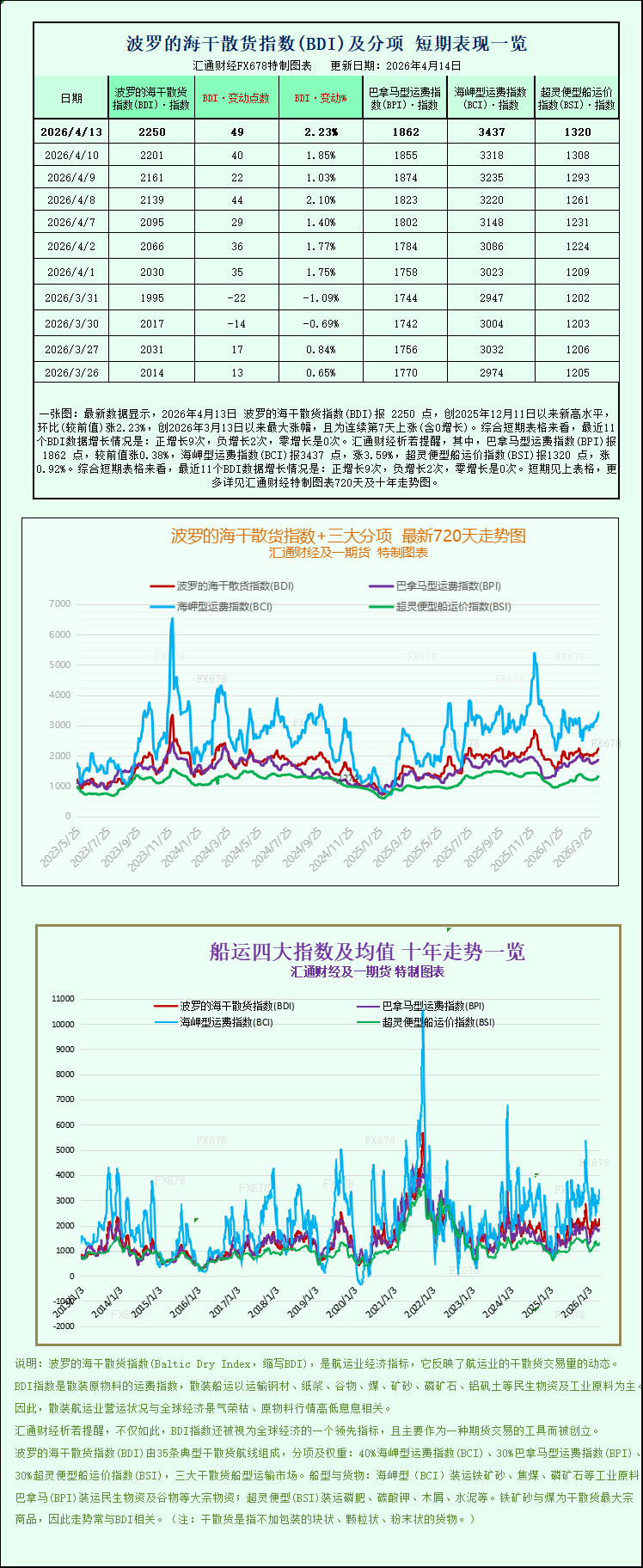

Latest data shows that the Baltic Dry Index (BDI) reached 2250 points on April 13, 2026, a new high since December 11, 2025, up 2.23% month-on-month, the largest increase since March 13, 2026, and marking the 7th consecutive day of increase (including zero growth). Looking at the short-term charts, the recent 11 BDI data points show: 9 positive increases, 2 negative increases, and 0 zero increases. Specifically, the Panamax Freight Index (BPI) was 1862 points, up 0.38% from the previous value; the Capesize Freight Index (BCI) was 3437 points, up 3.59%; and the Supramax Freight Index (BSI) was 1320 points, up 0.92%. For detailed 720-day and 10-year trend charts of the Baltic Dry Index and its three main sub-indices, please refer to the specially designed charts.

The global dry bulk shipping market has seen a significant recovery, with the Baltic Dry Index (BDI) surging on Monday to its highest level in four months. All vessel segments within the index rose steadily, continuing the recent upward trend and becoming an important indicator of the recovery in global commodity trade, reflecting a phased recovery in global dry bulk shipping demand.

As a core indicator for monitoring global dry bulk shipping freight rates, the Baltic Dry Index (BDI) covers freight trends for the three major dry bulk vessel types: Capesize, Panamax, and Supramax. Its fluctuations directly reflect the activity level of global transportation of commodities such as iron ore, coal, and grains. Reportedly, the index surged 49 points on Monday, a 2.2% increase, closing at 2250 points. This figure not only represents the highest level since December 12, 2025, but also continues the strong performance of the previous week—last week saw the index's best weekly gain in two months. The continuous upward trend fully reflects the market's optimistic expectations for the dry bulk shipping industry and confirms the dual support of a steady recovery in global dry bulk shipping demand and a temporary tightness in shipping capacity.

Among the sub-sectors, Capesize vessels, the "juggernauts" of dry bulk shipping, performed the best, becoming the core driving force behind the overall index's rise. The Capesize index surged 119 points, or approximately 3.6%, closing at 3437 points, the highest level since February 2nd, continuing its recent upward trend. As the backbone of long-distance bulk dry bulk shipping, Capesize vessels typically handle 150,000-ton cargoes, primarily transporting core industrial raw materials such as iron ore and coal. Their freight rates and revenues are closely linked to global industrial demand. Driven by this, the average daily revenue of Capesize vessels also climbed, increasing by $1082 to reach $27,667. This increase was mainly due to a surge in demand on the West Africa-China route. China's imports of bauxite and iron ore from Guinea and other West African countries continued to increase, while loading delays at Guinean ports tied up some capacity, further pushing up freight rates and daily revenue.

It is worth noting that the recovery in dry bulk shipping demand and the rebound in upstream raw material markets have created a synergistic effect. On Monday, domestic iron ore futures prices rebounded strongly, successfully ending a six-day losing streak, after previously falling to a one-month low. This rebound in iron ore futures prices was mainly supported by two factors: firstly, the continued surge in international oil prices boosted overall market sentiment in commodities; secondly, the gradual recovery of global industrial production activity led to a sustained increase in demand for industrial raw materials such as iron ore, especially from emerging economies like China, which further boosted iron ore prices and consequently increased shipping demand for core dry bulk vessels such as Capesize vessels.

Besides Capesize vessels, the Panamax sector also saw steady growth, becoming a significant driver of the overall index's rise. The Panamax index rose 7 points, or approximately 0.4%, to close at 1862 points, just shy of its three-week high, continuing the upward trend since early April. Panamax vessels typically have a deadweight tonnage between 60,000 and 70,000 tons, primarily transporting bulk commodities such as coal and grain. They are the mainstay of global short- and medium-haul dry bulk shipping, and their freight rates are closely linked to the activity of global agricultural and energy trade. Driven by the seasonal recovery in global grain trade and the steady release of demand for coal transportation, especially the increased activity on the South America-China soybean shipping route, the average daily revenue of Panamax vessels increased by $61 to $16,757, demonstrating a robust recovery.

The Supramax vessel sector also performed well, achieving steady growth and reaching a new high for the period. The Very Large Bulk Carrier (VLCC) index rose 12 points, or 0.9%, to close at 1320 points, its highest level in a month. Supramax vessels, with a deadweight tonnage between 50,000 and 6,000 tons, possess good route adaptability and cargo compatibility. They are equipped with standard cranes and have self-loading and unloading capabilities, primarily undertaking small-volume dry bulk cargo transportation tasks, covering a variety of industrial raw materials and agricultural products. Their freight rate fluctuations are considered an important indicator of the medium-sized bulk shipping market. This sector's rise reflects a significant increase in the activity of global small- and medium-volume dry bulk trade. Simultaneously, recent increases in Supramax secondhand vessel prices and a shift in market demand towards older vessels have further supported the stable upward trend in freight rates for this vessel type.

Escalating global geopolitical tensions have become a significant variable influencing the dry bulk market and related commodity prices. The US military officially announced on Monday that it would begin a blockade of all ships leaving Iranian ports, further escalating geopolitical tensions in the Middle East. Meanwhile, after weekend peace talks failed to reach an agreement, Iran issued a clear threat of retaliation, stating it would take countermeasures against ports in neighboring Gulf states, further escalating the standoff and creating uncertainty for global shipping and commodity markets.

However, industry analysts point out that although geopolitical tensions have driven up international oil prices, leading to higher marine fuel prices and potentially putting pressure on shipowners' profit margins, the actual impact on most major dry bulk shipping routes is relatively small. The Strait of Hormuz is a core channel for global crude oil transportation, with approximately one-fifth of the world's crude oil and LNG passing through it. However, most major dry bulk shipping routes avoid this area, thus limiting the direct impact. Nevertheless, it is worth noting that continued geopolitical tensions could indirectly suppress global industrial production demand by pushing up energy costs, thereby creating a long-term constraint on dry bulk shipping demand. This is one of the main uncertainties currently facing the market.

Driven directly by geopolitical tensions, international oil prices have surged again, breaking through $102 per barrel by Monday, reaching a new high since 2024. Behind this price surge, in addition to supply concerns stemming from escalating tensions between the US and Iran, factors such as OPEC+ extending its production cut agreement, a weakening dollar, and a recovery in demand driven by the global economic recovery have also played a role. The continued high oil prices will not only increase fuel costs for shipowners but may also further impact the global industrial supply chain, potentially affecting the long-term recovery of the dry bulk market.

Overall, the Baltic Dry Index's recent multi-month high, with all sectors rising simultaneously, is the result of a combination of factors, including a phased recovery in global dry bulk shipping demand, tight shipping capacity, and geopolitical tensions. Despite current challenges such as rising fuel costs and geopolitical uncertainties, the recovery trend in the dry bulk market is expected to continue in the short term, particularly with the sustained release of demand for resource transportation from West Africa, which is likely to further support the Baltic Dry Index at its high levels. Future market trends will require close monitoring of key variables such as changes in global industrial demand, developments in geopolitical situations, and fuel price fluctuations.

The global dry bulk shipping market has seen a significant recovery, with the Baltic Dry Index (BDI) surging on Monday to its highest level in four months. All vessel segments within the index rose steadily, continuing the recent upward trend and becoming an important indicator of the recovery in global commodity trade, reflecting a phased recovery in global dry bulk shipping demand.

As a core indicator for monitoring global dry bulk shipping freight rates, the Baltic Dry Index (BDI) covers freight trends for the three major dry bulk vessel types: Capesize, Panamax, and Supramax. Its fluctuations directly reflect the activity level of global transportation of commodities such as iron ore, coal, and grains. Reportedly, the index surged 49 points on Monday, a 2.2% increase, closing at 2250 points. This figure not only represents the highest level since December 12, 2025, but also continues the strong performance of the previous week—last week saw the index's best weekly gain in two months. The continuous upward trend fully reflects the market's optimistic expectations for the dry bulk shipping industry and confirms the dual support of a steady recovery in global dry bulk shipping demand and a temporary tightness in shipping capacity.

Among the sub-sectors, Capesize vessels, the "juggernauts" of dry bulk shipping, performed the best, becoming the core driving force behind the overall index's rise. The Capesize index surged 119 points, or approximately 3.6%, closing at 3437 points, the highest level since February 2nd, continuing its recent upward trend. As the backbone of long-distance bulk dry bulk shipping, Capesize vessels typically handle 150,000-ton cargoes, primarily transporting core industrial raw materials such as iron ore and coal. Their freight rates and revenues are closely linked to global industrial demand. Driven by this, the average daily revenue of Capesize vessels also climbed, increasing by $1082 to reach $27,667. This increase was mainly due to a surge in demand on the West Africa-China route. China's imports of bauxite and iron ore from Guinea and other West African countries continued to increase, while loading delays at Guinean ports tied up some capacity, further pushing up freight rates and daily revenue.

It is worth noting that the recovery in dry bulk shipping demand and the rebound in upstream raw material markets have created a synergistic effect. On Monday, domestic iron ore futures prices rebounded strongly, successfully ending a six-day losing streak, after previously falling to a one-month low. This rebound in iron ore futures prices was mainly supported by two factors: firstly, the continued surge in international oil prices boosted overall market sentiment in commodities; secondly, the gradual recovery of global industrial production activity led to a sustained increase in demand for industrial raw materials such as iron ore, especially from emerging economies like China, which further boosted iron ore prices and consequently increased shipping demand for core dry bulk vessels such as Capesize vessels.

Besides Capesize vessels, the Panamax sector also saw steady growth, becoming a significant driver of the overall index's rise. The Panamax index rose 7 points, or approximately 0.4%, to close at 1862 points, just shy of its three-week high, continuing the upward trend since early April. Panamax vessels typically have a deadweight tonnage between 60,000 and 70,000 tons, primarily transporting bulk commodities such as coal and grain. They are the mainstay of global short- and medium-haul dry bulk shipping, and their freight rates are closely linked to the activity of global agricultural and energy trade. Driven by the seasonal recovery in global grain trade and the steady release of demand for coal transportation, especially the increased activity on the South America-China soybean shipping route, the average daily revenue of Panamax vessels increased by $61 to $16,757, demonstrating a robust recovery.

The Supramax vessel sector also performed well, achieving steady growth and reaching a new high for the period. The Very Large Bulk Carrier (VLCC) index rose 12 points, or 0.9%, to close at 1320 points, its highest level in a month. Supramax vessels, with a deadweight tonnage between 50,000 and 6,000 tons, possess good route adaptability and cargo compatibility. They are equipped with standard cranes and have self-loading and unloading capabilities, primarily undertaking small-volume dry bulk cargo transportation tasks, covering a variety of industrial raw materials and agricultural products. Their freight rate fluctuations are considered an important indicator of the medium-sized bulk shipping market. This sector's rise reflects a significant increase in the activity of global small- and medium-volume dry bulk trade. Simultaneously, recent increases in Supramax secondhand vessel prices and a shift in market demand towards older vessels have further supported the stable upward trend in freight rates for this vessel type.

Escalating global geopolitical tensions have become a significant variable influencing the dry bulk market and related commodity prices. The US military officially announced on Monday that it would begin a blockade of all ships leaving Iranian ports, further escalating geopolitical tensions in the Middle East. Meanwhile, after weekend peace talks failed to reach an agreement, Iran issued a clear threat of retaliation, stating it would take countermeasures against ports in neighboring Gulf states, further escalating the standoff and creating uncertainty for global shipping and commodity markets.

However, industry analysts point out that although geopolitical tensions have driven up international oil prices, leading to higher marine fuel prices and potentially putting pressure on shipowners' profit margins, the actual impact on most major dry bulk shipping routes is relatively small. The Strait of Hormuz is a core channel for global crude oil transportation, with approximately one-fifth of the world's crude oil and LNG passing through it. However, most major dry bulk shipping routes avoid this area, thus limiting the direct impact. Nevertheless, it is worth noting that continued geopolitical tensions could indirectly suppress global industrial production demand by pushing up energy costs, thereby creating a long-term constraint on dry bulk shipping demand. This is one of the main uncertainties currently facing the market.

Driven directly by geopolitical tensions, international oil prices have surged again, breaking through $102 per barrel by Monday, reaching a new high since 2024. Behind this price surge, in addition to supply concerns stemming from escalating tensions between the US and Iran, factors such as OPEC+ extending its production cut agreement, a weakening dollar, and a recovery in demand driven by the global economic recovery have also played a role. The continued high oil prices will not only increase fuel costs for shipowners but may also further impact the global industrial supply chain, potentially affecting the long-term recovery of the dry bulk market.

Overall, the Baltic Dry Index's recent multi-month high, with all sectors rising simultaneously, is the result of a combination of factors, including a phased recovery in global dry bulk shipping demand, tight shipping capacity, and geopolitical tensions. Despite current challenges such as rising fuel costs and geopolitical uncertainties, the recovery trend in the dry bulk market is expected to continue in the short term, particularly with the sustained release of demand for resource transportation from West Africa, which is likely to further support the Baltic Dry Index at its high levels. Future market trends will require close monitoring of key variables such as changes in global industrial demand, developments in geopolitical situations, and fuel price fluctuations.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.