A chart: Baltic Dry Index declines and related market dynamics

2026-04-23 23:57:03

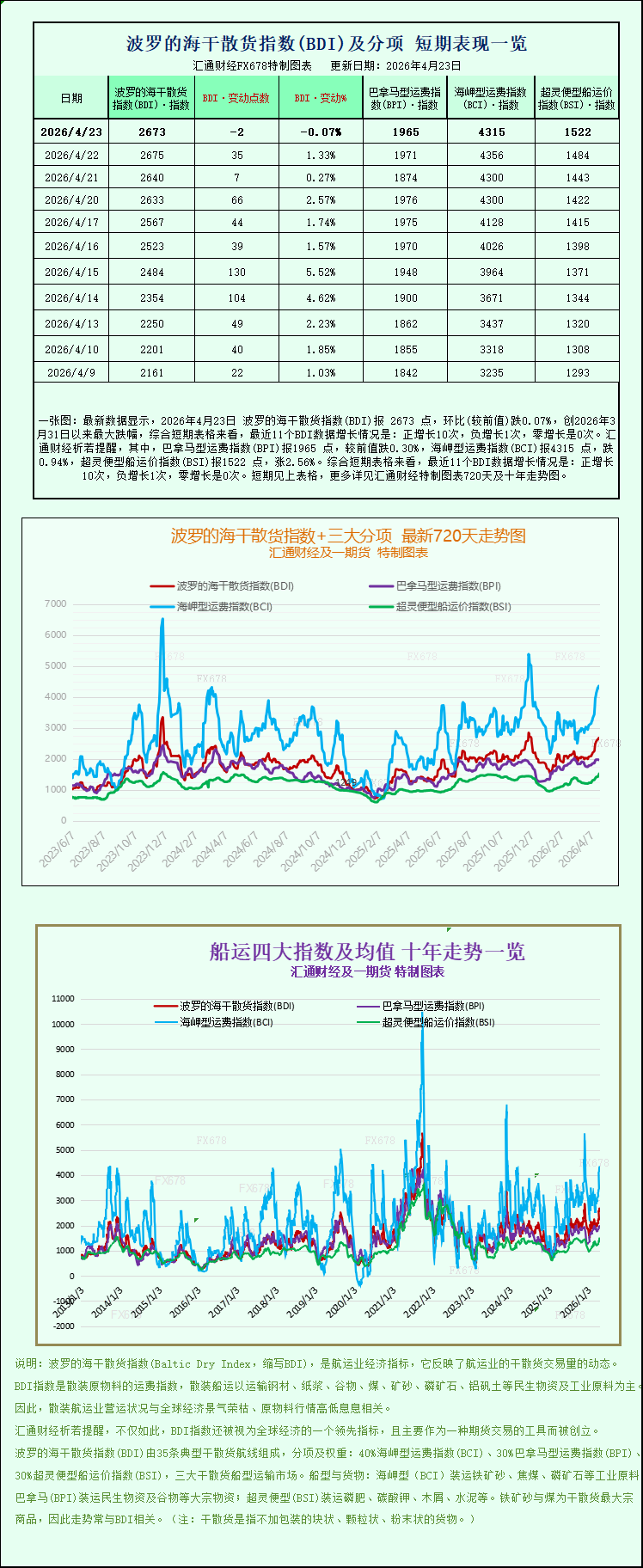

The latest data shows that on April 23, 2026, the Baltic Dry Index (BDI) was 2673 points, a decrease of 0.07% compared to the previous period, marking the largest drop since March 31, 2026. Looking at the short-term charts, the recent 11 BDI data points show: 10 positive increases, 1 negative increase, and 0 zero increases. Specifically, the Panamax Freight Index (BPI) was 1965 points, down 0.30% from the previous period; the Capesize Freight Index (BCI) was 4315 points, down 0.94%; and the Supramax Freight Index (BSI) was 1522 points, up 2.56%. For detailed 720-day and 10-year trend charts of the Baltic Dry Index and its three main sub-indices, please refer to the specially designed charts.

Directly affected by the continued decline in Capesize and Panamax bulk carrier freight rates, the Baltic Dry Index (BDI), which had been climbing steadily recently, has seen a slight pullback from its high level in more than four months, ending a period of strong growth and highlighting the structural differentiation in the current dry bulk shipping market.

Specifically, the Baltic Dry Index (BDI) released by the Baltic Exchange (which mainly monitors the freight rates of various types of vessels transporting dry bulk commodities globally and is a core indicator reflecting the prosperity of the dry bulk shipping market) fell slightly on the day, officially ending its previous 14-day upward trend. The simultaneous decline in freight rates for Capesize and Supramax vessels was the core reason driving the index's correction, which is also closely related to the subtle changes in the current supply and demand pattern of the dry bulk market.

The Baltic Dry Index, which tracks freight rates for the three major bulk carrier categories—Capesize, Panamax, and Supramax—showed lackluster performance, falling slightly by 2 points, or only 0.1%, to close at 2673. It's worth noting that the index reached its highest level in over four months on Wednesday, and this slight pullback does not alter its recent overall bullish trend; it is merely a temporary adjustment after reaching a high point.

As the "giant" of the dry bulk shipping market, the Capesize market was the main drag on the index's recent correction. The Capesize index fell 41 points, a drop of 0.9%, closing at 4315 points, continuing its recent downward trend. Capesize vessels primarily handle transoceanic transport of large dry bulk cargoes, typically with a carrying capacity of up to 150,000 tons. Core cargoes include key industrial raw materials such as iron ore and coal, and their freight rate fluctuations are directly linked to global industrial demand.

Correspondingly, the average daily earnings of Capesize vessels carrying 150,000 tons of cargo (including iron ore and coal) also declined, falling by $368 on the day to $35,634. This change echoed the trend in iron ore prices that day, which saw a significant drop on Thursday. Market investors were carefully weighing the prospects for increased supply of key steelmaking raw materials against the pros and cons of rising shipping costs due to the ongoing conflict with Iran. This uncertainty also indirectly affected the demand for Capesize vessels and freight rates.

Besides Capesize vessels, the Panamax bulk carrier market also showed weakness. The Panamax index fell 6 points, or approximately 0.3%, to close at 1965 points, continuing its previous mild downward trend. Panamax vessels have a carrying capacity between Capesize and Supramax, typically carrying 60,000 to 70,000 tons of dry bulk cargo such as coal or grain. They mainly undertake short- to medium-haul transoceanic transport missions, and their freight rates are closely related to the activity of global food and coal trade.

Affected by the decline in freight rates, the average daily earnings of Panamax vessels also declined slightly, falling by $62 to close at $17,682. Industry analysts believe that the slight decline in global seaborne coal demand and the phased adjustment in grain trade are the main reasons for the pressure on Panamax vessel freight rates, which is also related to the current structural supply and demand imbalance in the global dry bulk market.

In stark contrast to the sluggish Capesize and Panamax markets, the Supramax bulk carrier market performed exceptionally well, becoming a major highlight of the dry bulk shipping market that day. The Supramax bulk carrier index rose 38 points, or 2.6%, to close at 1522 points, reaching its highest level since early December 2023, demonstrating a strong recovery momentum. This also alleviated some of the downward pressure on the overall index, highlighting the divergence between different ship type markets.

Meanwhile, changes in the international geopolitical situation have added uncertainty to the dry bulk shipping market. On Thursday, Iranian officials released a video clearly showing their commandos storming a giant cargo ship, a move intended to showcase Iran's further strengthened control over the Strait of Hormuz. The Strait of Hormuz is one of the world's most important shipping routes, through which approximately one-fifth of the world's oil and gas supply passes, and its navigation status directly affects global shipping costs and trade flows.

Previously, Washington had attempted to open this crucial shipping route through peaceful negotiations to ease tensions in the global energy and shipping markets, but the talks ultimately broke down without any substantial consensus. Just as Iran demonstrated its control over the Strait of Hormuz, US President Trump explicitly vowed to further strengthen the US blockade of Iranian maritime trade. This statement will undoubtedly exacerbate geopolitical tensions in the Middle East and may have a profound impact on the future trajectory of the global dry bulk shipping market.

Directly affected by the continued decline in Capesize and Panamax bulk carrier freight rates, the Baltic Dry Index (BDI), which had been climbing steadily recently, has seen a slight pullback from its high level in more than four months, ending a period of strong growth and highlighting the structural differentiation in the current dry bulk shipping market.

Specifically, the Baltic Dry Index (BDI) released by the Baltic Exchange (which mainly monitors the freight rates of various types of vessels transporting dry bulk commodities globally and is a core indicator reflecting the prosperity of the dry bulk shipping market) fell slightly on the day, officially ending its previous 14-day upward trend. The simultaneous decline in freight rates for Capesize and Supramax vessels was the core reason driving the index's correction, which is also closely related to the subtle changes in the current supply and demand pattern of the dry bulk market.

The Baltic Dry Index, which tracks freight rates for the three major bulk carrier categories—Capesize, Panamax, and Supramax—showed lackluster performance, falling slightly by 2 points, or only 0.1%, to close at 2673. It's worth noting that the index reached its highest level in over four months on Wednesday, and this slight pullback does not alter its recent overall bullish trend; it is merely a temporary adjustment after reaching a high point.

As the "giant" of the dry bulk shipping market, the Capesize market was the main drag on the index's recent correction. The Capesize index fell 41 points, a drop of 0.9%, closing at 4315 points, continuing its recent downward trend. Capesize vessels primarily handle transoceanic transport of large dry bulk cargoes, typically with a carrying capacity of up to 150,000 tons. Core cargoes include key industrial raw materials such as iron ore and coal, and their freight rate fluctuations are directly linked to global industrial demand.

Correspondingly, the average daily earnings of Capesize vessels carrying 150,000 tons of cargo (including iron ore and coal) also declined, falling by $368 on the day to $35,634. This change echoed the trend in iron ore prices that day, which saw a significant drop on Thursday. Market investors were carefully weighing the prospects for increased supply of key steelmaking raw materials against the pros and cons of rising shipping costs due to the ongoing conflict with Iran. This uncertainty also indirectly affected the demand for Capesize vessels and freight rates.

Besides Capesize vessels, the Panamax bulk carrier market also showed weakness. The Panamax index fell 6 points, or approximately 0.3%, to close at 1965 points, continuing its previous mild downward trend. Panamax vessels have a carrying capacity between Capesize and Supramax, typically carrying 60,000 to 70,000 tons of dry bulk cargo such as coal or grain. They mainly undertake short- to medium-haul transoceanic transport missions, and their freight rates are closely related to the activity of global food and coal trade.

Affected by the decline in freight rates, the average daily earnings of Panamax vessels also declined slightly, falling by $62 to close at $17,682. Industry analysts believe that the slight decline in global seaborne coal demand and the phased adjustment in grain trade are the main reasons for the pressure on Panamax vessel freight rates, which is also related to the current structural supply and demand imbalance in the global dry bulk market.

In stark contrast to the sluggish Capesize and Panamax markets, the Supramax bulk carrier market performed exceptionally well, becoming a major highlight of the dry bulk shipping market that day. The Supramax bulk carrier index rose 38 points, or 2.6%, to close at 1522 points, reaching its highest level since early December 2023, demonstrating a strong recovery momentum. This also alleviated some of the downward pressure on the overall index, highlighting the divergence between different ship type markets.

Meanwhile, changes in the international geopolitical situation have added uncertainty to the dry bulk shipping market. On Thursday, Iranian officials released a video clearly showing their commandos storming a giant cargo ship, a move intended to showcase Iran's further strengthened control over the Strait of Hormuz. The Strait of Hormuz is one of the world's most important shipping routes, through which approximately one-fifth of the world's oil and gas supply passes, and its navigation status directly affects global shipping costs and trade flows.

Previously, Washington had attempted to open this crucial shipping route through peaceful negotiations to ease tensions in the global energy and shipping markets, but the talks ultimately broke down without any substantial consensus. Just as Iran demonstrated its control over the Strait of Hormuz, US President Trump explicitly vowed to further strengthen the US blockade of Iranian maritime trade. This statement will undoubtedly exacerbate geopolitical tensions in the Middle East and may have a profound impact on the future trajectory of the global dry bulk shipping market.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.