The situation in the Middle East is shaking up global energy markets, and the oil landscape may be permanently reshaped.

2026-04-28 14:14:45

Currently, various risk warnings are increasing. Affected by both the Middle East geopolitical situation and the Russia-Ukraine conflict, global oil supply is experiencing a severe shock, and traditional oil consumption and demand patterns may undergo profound and long-term adjustments. The longer the conflict lasts, the larger the scale of crude oil supply disruptions will be, and the higher the probability of a qualitative change in the energy consumption structure will continue to rise.

According to publicly available information from financial media, the current global oil supply gap is approaching 1 billion barrels, a dire situation that is almost a foregone conclusion, with shrinking oil demand already evident in Asia. This demand decline is not a localized phenomenon but is slowly and steadily spreading globally. Countries' crude oil reserves, intended to offset reduced Middle Eastern oil supply and stabilize market prices, are now nearing depletion, and the buffer space in the global energy market is rapidly shrinking.

International Energy Agency Executive Director Fatih Birol publicly stated this month that global daily crude oil supply is currently shrinking by 13 million barrels, and supply disruptions are occurring in various key commodities for both consumer and industrial use. In his view, the world is facing the most severe energy security threat in history. He reiterated this view in a subsequent interview, pointing out that many countries' economies are overly reliant on hydrocarbon energy, posing significant development risks.

Birol has long advocated for the world to break free from dependence on oil and gas and to comprehensively promote the transformation to clean energy sources such as wind power and photovoltaics.

This oil crisis has further propelled the global energy transition. Birol's analysis suggests that countries will comprehensively update their understanding of energy security and stability, leading to a re-planning of their energy development strategies. Renewable energy and nuclear power industries will experience rapid growth, and social production and daily life will accelerate towards electrification, ultimately resulting in a permanent decline in oil demand.

While the notion of a permanent decline in oil demand remains controversial within the industry, the massive oil supply gap will force major oil-importing countries to proactively address energy shortages and increase their investment in new energy sources. Currently, the global energy system is still dominated by traditional energy sources such as coal and oil and gas. New energy sources, limited by technological and stability shortcomings, are unlikely to achieve a dominant position in the short term.

Amidst significant energy price fluctuations, coal has emerged as an unusual beneficiary of the current crisis. Many countries, unable to afford the high costs of liquefied natural gas (LNG), have turned to increasing their coal consumption. Coal's advantages, including low price, abundant reserves, and wide availability, have made it a compromise for many nations. Developed economies like Japan and South Korea have increased their reliance on coal-fired power generation, while major Asian countries, India, Bangladesh, and many Southeast Asian nations have further deepened their dependence on coal due to natural gas shortages and price increases.

Adjustments to the energy structure will directly suppress demand for natural gas and liquefied natural gas, while potentially promoting electrification in the transportation sector. However, widespread electrification is still constrained by energy costs and is unlikely to be implemented in the short term.

Tight oil supplies have dealt a heavy blow to the petrochemical industry, whose raw materials cover multiple sectors including industrial manufacturing and new energy. The production of electric vehicles and wind and solar power infrastructure all rely heavily on petrochemical products. Rising crude oil prices will be transmitted through the industrial chain, increasing the production costs of various products such as new energy equipment and power cables, causing clean energy alternatives to lose their price advantage, and ultimately suppressing overall energy consumption demand.

Cuneyt Kazokoglu, head of an energy industry analysis firm, pointed out that Western countries, by failing to confront the obvious energy shortage crisis, have ignored potential risks and viewed only the slight increase in oil prices as the sole impact. In fact, the global demand contraction is arriving in stages, with Asia being the first to be affected, followed by Africa, and Europe already experiencing fuel shortages and rising prices.

Market analysts point out that if supply and demand were to be balanced solely by market forces, oil prices would need to surge dramatically to achieve demand control, potentially reaching $250 per barrel. Several financial institution executives also predict that international oil prices breaking through $200 is a realistic possibility, as energy supply shortages will drive commodity prices up rapidly.

Currently, Brent crude oil futures prices are just over $100, while West Texas Intermediate (WTI) crude oil prices are still below $100. However, futures prices do not reflect the true situation in the spot market. Due to rising additional costs such as freight and insurance, physical crude oil trading prices exhibit a high premium.

Overall, a contraction in global oil demand is an inevitable trend, and a profound transformation of the energy market has begun. The scope and intensity of the energy recession's impact, as well as whether it will fundamentally and permanently alter oil demand patterns, remain to be seen and will require long-term market observation.

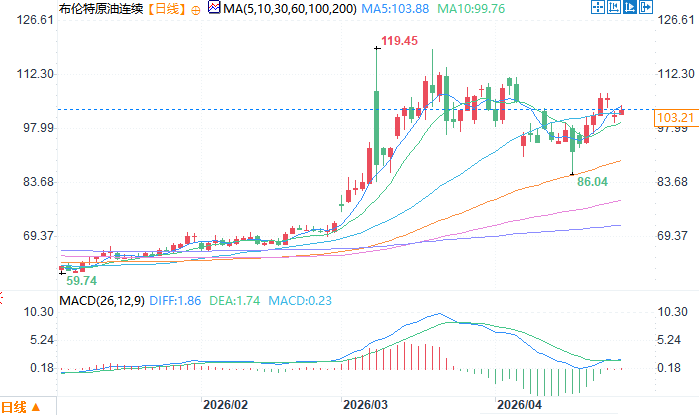

Brent crude oil daily chart source: EasyForex

At 14:07 Beijing time on April 28, Brent crude oil futures were trading at $103.11 per barrel.

According to publicly available information from financial media, the current global oil supply gap is approaching 1 billion barrels, a dire situation that is almost a foregone conclusion, with shrinking oil demand already evident in Asia. This demand decline is not a localized phenomenon but is slowly and steadily spreading globally. Countries' crude oil reserves, intended to offset reduced Middle Eastern oil supply and stabilize market prices, are now nearing depletion, and the buffer space in the global energy market is rapidly shrinking.

Authoritative agencies warn of risks, highlighting the need to accelerate energy transition.

International Energy Agency Executive Director Fatih Birol publicly stated this month that global daily crude oil supply is currently shrinking by 13 million barrels, and supply disruptions are occurring in various key commodities for both consumer and industrial use. In his view, the world is facing the most severe energy security threat in history. He reiterated this view in a subsequent interview, pointing out that many countries' economies are overly reliant on hydrocarbon energy, posing significant development risks.

Birol has long advocated for the world to break free from dependence on oil and gas and to comprehensively promote the transformation to clean energy sources such as wind power and photovoltaics.

This oil crisis has further propelled the global energy transition. Birol's analysis suggests that countries will comprehensively update their understanding of energy security and stability, leading to a re-planning of their energy development strategies. Renewable energy and nuclear power industries will experience rapid growth, and social production and daily life will accelerate towards electrification, ultimately resulting in a permanent decline in oil demand.

The shift in energy substitution patterns has unexpectedly made coal a beneficiary of the crisis.

While the notion of a permanent decline in oil demand remains controversial within the industry, the massive oil supply gap will force major oil-importing countries to proactively address energy shortages and increase their investment in new energy sources. Currently, the global energy system is still dominated by traditional energy sources such as coal and oil and gas. New energy sources, limited by technological and stability shortcomings, are unlikely to achieve a dominant position in the short term.

Amidst significant energy price fluctuations, coal has emerged as an unusual beneficiary of the current crisis. Many countries, unable to afford the high costs of liquefied natural gas (LNG), have turned to increasing their coal consumption. Coal's advantages, including low price, abundant reserves, and wide availability, have made it a compromise for many nations. Developed economies like Japan and South Korea have increased their reliance on coal-fired power generation, while major Asian countries, India, Bangladesh, and many Southeast Asian nations have further deepened their dependence on coal due to natural gas shortages and price increases.

Adjustments to the energy structure will directly suppress demand for natural gas and liquefied natural gas, while potentially promoting electrification in the transportation sector. However, widespread electrification is still constrained by energy costs and is unlikely to be implemented in the short term.

The chain reaction in the industrial chain is becoming apparent, with energy costs being passed on to the entire industry.

Tight oil supplies have dealt a heavy blow to the petrochemical industry, whose raw materials cover multiple sectors including industrial manufacturing and new energy. The production of electric vehicles and wind and solar power infrastructure all rely heavily on petrochemical products. Rising crude oil prices will be transmitted through the industrial chain, increasing the production costs of various products such as new energy equipment and power cables, causing clean energy alternatives to lose their price advantage, and ultimately suppressing overall energy consumption demand.

Cuneyt Kazokoglu, head of an energy industry analysis firm, pointed out that Western countries, by failing to confront the obvious energy shortage crisis, have ignored potential risks and viewed only the slight increase in oil prices as the sole impact. In fact, the global demand contraction is arriving in stages, with Asia being the first to be affected, followed by Africa, and Europe already experiencing fuel shortages and rising prices.

Oil price expectations are diverging, and future market trends remain uncertain.

Market analysts point out that if supply and demand were to be balanced solely by market forces, oil prices would need to surge dramatically to achieve demand control, potentially reaching $250 per barrel. Several financial institution executives also predict that international oil prices breaking through $200 is a realistic possibility, as energy supply shortages will drive commodity prices up rapidly.

Currently, Brent crude oil futures prices are just over $100, while West Texas Intermediate (WTI) crude oil prices are still below $100. However, futures prices do not reflect the true situation in the spot market. Due to rising additional costs such as freight and insurance, physical crude oil trading prices exhibit a high premium.

Summarize

Overall, a contraction in global oil demand is an inevitable trend, and a profound transformation of the energy market has begun. The scope and intensity of the energy recession's impact, as well as whether it will fundamentally and permanently alter oil demand patterns, remain to be seen and will require long-term market observation.

Brent crude oil daily chart source: EasyForex

At 14:07 Beijing time on April 28, Brent crude oil futures were trading at $103.11 per barrel.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.