One chart: The Baltic Dry Index hits its highest point in over two years, with all types of vessels seeing increases.

2026-05-08 00:53:17

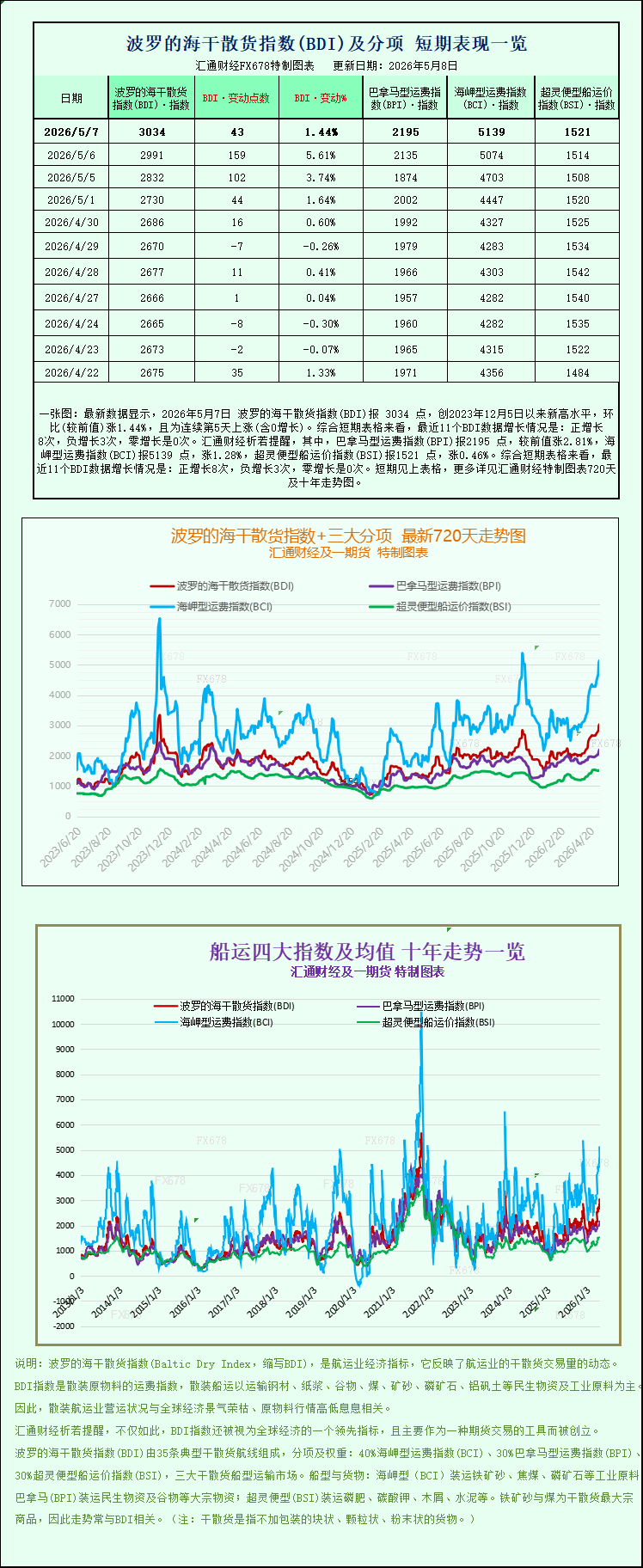

The latest data shows that the Baltic Dry Index (BDI) reached 3034 points on May 7, 2026, a new high since December 5, 2023, up 1.44% month-on-month, marking the fifth consecutive day of increase (including zero growth). Looking at the short-term charts, the recent 11 BDI data points show: 8 positive increases, 3 negative increases, and 0 zero increases. Specifically, the Panamax Freight Index (BPI) was 2195 points, up 2.81% from the previous value; the Capesize Freight Index (BCI) was 5139 points, up 1.28%; and the Supramax Freight Index (BSI) was 1521 points, up 0.46%. For detailed 720-day and 10-year trend charts of the Baltic Dry Index and its three main sub-indices, please refer to the specially designed charts.

The Baltic Dry Index (which monitors freight rates for vessels transporting dry bulk commodities) reached its highest level in more than two years on Thursday, driven by strong demand for all types of vessels.

Specifically, the Baltic Dry Index, which tracks freight rates for Capesize, Panamax, and Supramax vessels, rose 43 points, or 1.44%, to 3034 points, reaching its highest level since early December 2023. It is understood that the index has been trending upwards recently, consistent with the overall trend of the Baltic Dry Index, highlighting the strong recovery momentum in the dry bulk market.

As a core force in the large bulk shipping market, the Capesize vessel sector performed exceptionally well, becoming a key engine driving the overall index upward. Specifically, the Capesize index rose 65 points, or 1.3%, to 5139 points, a new high in over five months, continuing its recent strong upward momentum. It also formed a reasonable price difference with the main Baltic Dry Index, consistent with the market pattern of "a single large vessel type index exceeding the composite index." Analysts at shipping consultancy Intermodal stated that the Capesize market has performed positively recently. Although there are differences in different shipping regions globally, the continued tightness of effective shipping capacity and the steady strengthening of demand for bulk commodity transportation have jointly supported the continued rise in freight rates.

Echoing the rise in the index, the average daily earnings for Capesize bulk carriers increased by $593 to $43,107. These bulk carriers typically transport 150,000 tons of cargo, including iron ore and coal. The continued rise in iron ore futures prices, supported by stable demand, has driven sustained strong demand for iron ore transportation, thereby pushing up freight rates and daily earnings for Capesize vessels.

Besides Capesize vessels, the Panamax sector also performed strongly, becoming a significant force supporting the overall index. The Panamax index rose slightly by 60 points, or 2.8%, to 2195 points, reaching its highest level in over two years and the highest level since late March 2024. This vessel type is sized to meet the navigation requirements of the Panama Canal, with a deadweight tonnage between 60,000 and 80,000 tons. It combines route flexibility with cargo capacity advantages, making it the mainstay of medium- and long-haul dry bulk trade, primarily handling the transportation of 60,000 to 70,000 tons of bulk commodities such as coal or grain.

Benefiting from the continued release of market demand, the average daily earnings of Panamax vessels (typically carrying 60,000 to 70,000 tons of coal or grain) increased by US$542 to US$19,758, demonstrating the resilience of demand in niche transportation markets such as grain and coal. It is understood that Southeast Asian demand for imported coal is accelerating, while South American grain cargoes are steadily increasing. The combined effect of these two core cargoes has directly driven up daily charter rates and freight rates for this vessel type, further activating the turnover efficiency of the Far East dry bulk shipping market.

Strong growth in coal shipping demand has been one of the core drivers of rising Panamax freight rates. Data shows that in April, coal shipments to the EU, Japan, and South Korea boosted global coal ton-mile demand by 8% year-on-year. In a report, Filipe Guvia, shipping analysis manager at the Baltic Chamber of International Shipping (BIMCO), noted that Panamax vessels are the primary type of vessel transporting coal to these markets, accounting for 58% of total shipments, while Capesize vessels account for 31%.

Among smaller vessels, the Very Large Vessel (VLS) index increased by 7 points, or 0.5%, to 1521 points, moving in tandem with Capesize and Panamax vessels, further confirming the overall recovery momentum of the dry bulk market. These vessels primarily handle short-haul transportation of small dry bulk cargoes, and their freight rate rebound is mainly attributed to the gradual recovery in regional short-haul transportation demand. Simultaneously, driven by the overall positive market sentiment, they have achieved a synchronized increase, resulting in a comprehensive rise in freight rates for all tonnages of bulk carriers.

Industry analysts point out that the Baltic Dry Index's recent surge to a more than two-year high is primarily driven by strong demand for all types of vessels. On the demand side, robust demand for core dry bulk commodities such as iron ore and coal is supporting rising freight rates across all ship types. On the supply side, although bulk carrier deliveries are projected to reach 41.2 million deadweight tons in 2026, a new high since 2018, limited capacity release in the short term, coupled with some vessels being stranded due to geopolitical factors, has led to a tight supply of effective shipping capacity, further pushing up freight rates. Looking ahead, the dry bulk market is expected to maintain a positive trend in the short term, but in the long term, close attention needs to be paid to the progress of new ship deliveries, the pace of global industrial demand recovery, and changes in the geopolitical situation.

The Baltic Dry Index (which monitors freight rates for vessels transporting dry bulk commodities) reached its highest level in more than two years on Thursday, driven by strong demand for all types of vessels.

Specifically, the Baltic Dry Index, which tracks freight rates for Capesize, Panamax, and Supramax vessels, rose 43 points, or 1.44%, to 3034 points, reaching its highest level since early December 2023. It is understood that the index has been trending upwards recently, consistent with the overall trend of the Baltic Dry Index, highlighting the strong recovery momentum in the dry bulk market.

As a core force in the large bulk shipping market, the Capesize vessel sector performed exceptionally well, becoming a key engine driving the overall index upward. Specifically, the Capesize index rose 65 points, or 1.3%, to 5139 points, a new high in over five months, continuing its recent strong upward momentum. It also formed a reasonable price difference with the main Baltic Dry Index, consistent with the market pattern of "a single large vessel type index exceeding the composite index." Analysts at shipping consultancy Intermodal stated that the Capesize market has performed positively recently. Although there are differences in different shipping regions globally, the continued tightness of effective shipping capacity and the steady strengthening of demand for bulk commodity transportation have jointly supported the continued rise in freight rates.

Echoing the rise in the index, the average daily earnings for Capesize bulk carriers increased by $593 to $43,107. These bulk carriers typically transport 150,000 tons of cargo, including iron ore and coal. The continued rise in iron ore futures prices, supported by stable demand, has driven sustained strong demand for iron ore transportation, thereby pushing up freight rates and daily earnings for Capesize vessels.

Besides Capesize vessels, the Panamax sector also performed strongly, becoming a significant force supporting the overall index. The Panamax index rose slightly by 60 points, or 2.8%, to 2195 points, reaching its highest level in over two years and the highest level since late March 2024. This vessel type is sized to meet the navigation requirements of the Panama Canal, with a deadweight tonnage between 60,000 and 80,000 tons. It combines route flexibility with cargo capacity advantages, making it the mainstay of medium- and long-haul dry bulk trade, primarily handling the transportation of 60,000 to 70,000 tons of bulk commodities such as coal or grain.

Benefiting from the continued release of market demand, the average daily earnings of Panamax vessels (typically carrying 60,000 to 70,000 tons of coal or grain) increased by US$542 to US$19,758, demonstrating the resilience of demand in niche transportation markets such as grain and coal. It is understood that Southeast Asian demand for imported coal is accelerating, while South American grain cargoes are steadily increasing. The combined effect of these two core cargoes has directly driven up daily charter rates and freight rates for this vessel type, further activating the turnover efficiency of the Far East dry bulk shipping market.

Strong growth in coal shipping demand has been one of the core drivers of rising Panamax freight rates. Data shows that in April, coal shipments to the EU, Japan, and South Korea boosted global coal ton-mile demand by 8% year-on-year. In a report, Filipe Guvia, shipping analysis manager at the Baltic Chamber of International Shipping (BIMCO), noted that Panamax vessels are the primary type of vessel transporting coal to these markets, accounting for 58% of total shipments, while Capesize vessels account for 31%.

Among smaller vessels, the Very Large Vessel (VLS) index increased by 7 points, or 0.5%, to 1521 points, moving in tandem with Capesize and Panamax vessels, further confirming the overall recovery momentum of the dry bulk market. These vessels primarily handle short-haul transportation of small dry bulk cargoes, and their freight rate rebound is mainly attributed to the gradual recovery in regional short-haul transportation demand. Simultaneously, driven by the overall positive market sentiment, they have achieved a synchronized increase, resulting in a comprehensive rise in freight rates for all tonnages of bulk carriers.

Industry analysts point out that the Baltic Dry Index's recent surge to a more than two-year high is primarily driven by strong demand for all types of vessels. On the demand side, robust demand for core dry bulk commodities such as iron ore and coal is supporting rising freight rates across all ship types. On the supply side, although bulk carrier deliveries are projected to reach 41.2 million deadweight tons in 2026, a new high since 2018, limited capacity release in the short term, coupled with some vessels being stranded due to geopolitical factors, has led to a tight supply of effective shipping capacity, further pushing up freight rates. Looking ahead, the dry bulk market is expected to maintain a positive trend in the short term, but in the long term, close attention needs to be paid to the progress of new ship deliveries, the pace of global industrial demand recovery, and changes in the geopolitical situation.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.