US stocks face a major test at record highs: will they rise even with weaker non-farm payroll data? The real risk is actually strong data.

2026-05-08 11:08:13

Currently, the S&P 500, Nasdaq 100, and Dow Jones indices are all at historical highs, with the semiconductor sector leading the gains. Crude oil prices have fallen below $100, and the inflationary pressures facing the Federal Reserve have eased somewhat. Market logic has shifted back to "bad news is good news"—weak non-farm payroll data will boost expectations of interest rate cuts, further driving up the stock market. The real risk is not weak data, but strong data.

I. Analysis of Preliminary Data: ADP Exceeds Expectations, But Caution is Needed

April's ADP private sector employment rose by 109,000, exceeding the expected 84,000-99,000 and rebounding sharply from the revised 61,000 in March. JPMorgan Chase pointed out that ADP has historically underestimated the initial BLS figure, and this growth was mainly concentrated in the leisure and hospitality industry—sectors most sensitive to weak consumer spending.

Initial jobless claims totaled 189,000, but the data was distorted by the Easter holiday. Job openings at JOLTS rebounded somewhat, but the hiring rate remained at only 3.3%, the lowest level since 2014 (excluding the pandemic period). Furthermore, the one-off factor of approximately 31,000 new nonfarm payroll jobs in March due to Kaiser Permanente employees returning to work will turn into a drag in April.

Note: Kaiser Permanente is one of the largest healthcare organizations in the United States.

Scenario 1: Exceeding Expectations (>100,000): The market will repric the interest rate path, the two-year US Treasury yield will surge, the financial sector (XLF) will outperform, and long-duration technology stocks (QQQ) and semiconductors (SMH) will pause. If wages remain moderate, bargain hunters may quickly enter the market.

Scenario 2: As Expected (60,000-80,000): The smoothest path for the market, and current prices have already priced in this scenario. The unemployment rate remains stable at 4.3%, the Federal Reserve maintains its flexibility, and semiconductor leaders (NVDA, AMD, TSM) continue their upward trend.

Scenario 3: Weak (<50,000): Most favorable for the current market. Falling oil prices and diminishing inflation risks will fuel expectations of interest rate cuts. QQQ and SMH will lead the gains, and small-cap stocks (IWM) are expected to attract interest rate-sensitive funds after months of underperformance. If the unemployment rate rises above 4.5%, SAM rule concerns may temporarily suppress the market, but the narrative of interest rate cuts will typically dominate intraday.

Wages (AHE): A month-on-month increase of ≤0.20% will strengthen the bullish logic, regardless of the non-farm payroll data.

Unemployment rate: Below 4.4% is still considered "bad is good," while above 4.5% will turn into recession fears.

Semiconductors (SMH): If semiconductors are in high demand within 30 minutes of the data release, the upward trend will continue.

The threat posed by the April non-farm payrolls report to the current bull market is asymmetrical: weak or in line-of-expectations data will continue the "melt-up" rally; only strong employment and wages could temporarily halt the upward trend—and even then, pullbacks could be seen as buying opportunities by the market.

"If the employment data is significantly stronger than expected, it could reignite bets on interest rate hikes," noted the head of research at FXTM. Analysts cautioned that even with weak data, investors may not be willing to make large-scale bets on rate cuts until the situation in Iran becomes clearer.

Institutional forecasts diverge, scenario simulations and trading strategies

I. Analysis of Preliminary Data: ADP Exceeds Expectations, But Caution is Needed

April's ADP private sector employment rose by 109,000, exceeding the expected 84,000-99,000 and rebounding sharply from the revised 61,000 in March. JPMorgan Chase pointed out that ADP has historically underestimated the initial BLS figure, and this growth was mainly concentrated in the leisure and hospitality industry—sectors most sensitive to weak consumer spending.

Initial jobless claims totaled 189,000, but the data was distorted by the Easter holiday. Job openings at JOLTS rebounded somewhat, but the hiring rate remained at only 3.3%, the lowest level since 2014 (excluding the pandemic period). Furthermore, the one-off factor of approximately 31,000 new nonfarm payroll jobs in March due to Kaiser Permanente employees returning to work will turn into a drag in April.

Note: Kaiser Permanente is one of the largest healthcare organizations in the United States.

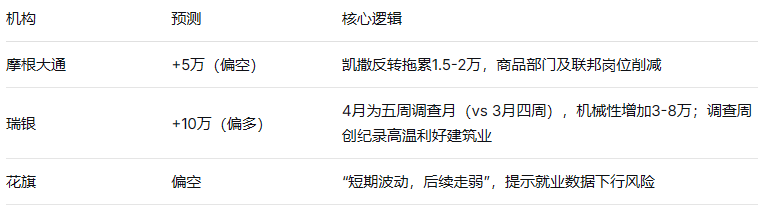

II. Institutional Disagreements: From +50,000 to +100,000

III. Three Scenario Deductions

Scenario 1: Exceeding Expectations (>100,000): The market will repric the interest rate path, the two-year US Treasury yield will surge, the financial sector (XLF) will outperform, and long-duration technology stocks (QQQ) and semiconductors (SMH) will pause. If wages remain moderate, bargain hunters may quickly enter the market.

Scenario 2: As Expected (60,000-80,000): The smoothest path for the market, and current prices have already priced in this scenario. The unemployment rate remains stable at 4.3%, the Federal Reserve maintains its flexibility, and semiconductor leaders (NVDA, AMD, TSM) continue their upward trend.

Scenario 3: Weak (<50,000): Most favorable for the current market. Falling oil prices and diminishing inflation risks will fuel expectations of interest rate cuts. QQQ and SMH will lead the gains, and small-cap stocks (IWM) are expected to attract interest rate-sensitive funds after months of underperformance. If the unemployment rate rises above 4.5%, SAM rule concerns may temporarily suppress the market, but the narrative of interest rate cuts will typically dominate intraday.

IV. Key Cross Variables

Wages (AHE): A month-on-month increase of ≤0.20% will strengthen the bullish logic, regardless of the non-farm payroll data.

Unemployment rate: Below 4.4% is still considered "bad is good," while above 4.5% will turn into recession fears.

Semiconductors (SMH): If semiconductors are in high demand within 30 minutes of the data release, the upward trend will continue.

Friday's threshold – a low or high threshold is a positive sign, a strong threshold is a risk.

The threat posed by the April non-farm payrolls report to the current bull market is asymmetrical: weak or in line-of-expectations data will continue the "melt-up" rally; only strong employment and wages could temporarily halt the upward trend—and even then, pullbacks could be seen as buying opportunities by the market.

"If the employment data is significantly stronger than expected, it could reignite bets on interest rate hikes," noted the head of research at FXTM. Analysts cautioned that even with weak data, investors may not be willing to make large-scale bets on rate cuts until the situation in Iran becomes clearer.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.