A chart: The Baltic Dry Index has retreated from a two-year high, but still recorded a weekly gain.

2026-05-08 22:56:52

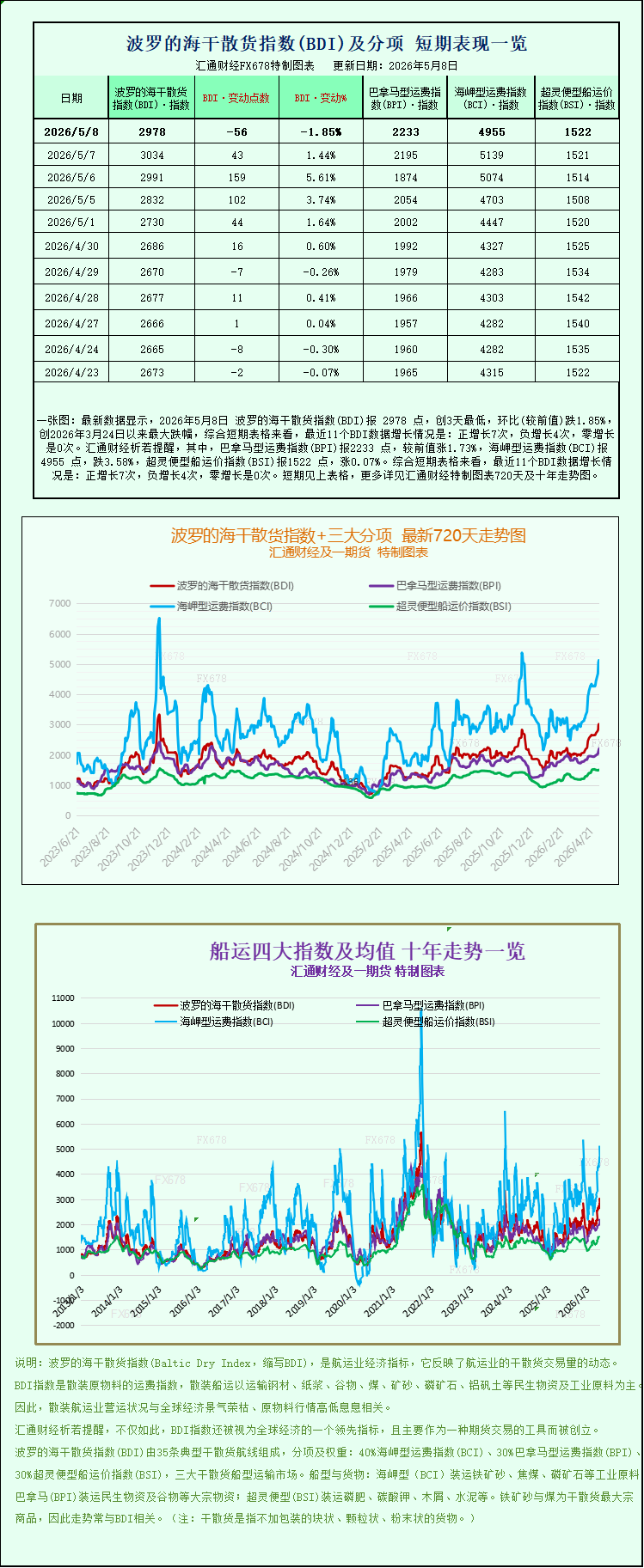

Latest data shows that on May 8, 2026, the Baltic Dry Index (BDI) was 2978 points, a three-day low, down 1.85% from the previous day, the largest drop since March 24, 2026. Looking at the short-term charts, the BDI has seen positive growth 7 times, negative growth 4 times, and zero growth 0 times in the last 11 BDI data points. Specifically, the Panamax Freight Index (BPI) was 2233 points, up 1.73% from the previous day; the Capesize Freight Index (BCI) was 4955 points, down 3.58%; and the Supramax Freight Index (BSI) was 1522 points, up 0.07%. For detailed 720-day and 10-year trend charts of the Baltic Dry Index and its three main sub-indices, please refer to the specially designed charts.

The Baltic Dry Index (BDI), a key indicator tracking global dry bulk shipping rates, saw a slight decline on Friday, officially retreating from its more than two-year high reached in the previous trading day. However, thanks to its strong performance in the first four trading days of the week, the index still recorded a significant weekly gain, continuing the overall upward trend since April and reflecting the resilience of the global dry bulk shipping market recovery. As a core indicator measuring the cost of shipping key dry bulk commodities such as iron ore, coal, and grains globally, the fluctuations in the Baltic Dry Index directly reflect the dynamics of global dry bulk trading volume and are closely related to global economic conditions and raw material prices.

Specifically, the Baltic Dry Index, which tracks freight rates for the three major bulk carrier categories—Capesize, Panamax, and Supramax—fell 56 points, or 1.9%, to close at 2978. Notably, the index had climbed to its highest point since March 2024 on Thursday, reaching its peak in over two years, demonstrating the strong recovery momentum in the dry bulk market recently. Looking at the weekly performance, despite a slight pullback on Friday, the index still rose 9.1% this week, marking two consecutive weeks of gains and further consolidating the market recovery. This also continues the two-month upward trend since the index bottomed out in early March, with a cumulative increase exceeding 40%.

Among the various vessel types, the Capesize sector was the main drag on the day's correction. The Capesize index fell sharply by 184 points, a drop of 3.6%, closing at 4955 points, a significant decline from the five-month high reached on Thursday, ending a four-day winning streak. However, the sector's overall performance this week was still strong, with a cumulative increase of 11.4%, becoming one of the important forces driving the overall index's weekly rise. As the mainstay of global dry bulk shipping, Capesize vessels primarily carry 150,000 tons of industrial bulk raw materials such as iron ore and coal, and their freight rates are highly correlated with the activity of global iron ore trade.

In a recent market report, Maria Bertzeletou, Senior Market Analyst at Signal Group, clearly stated: "The market performance in the first week of May further confirmed the strong upward momentum in the Atlantic Capesize bulk carrier freight market in April. Freight rates on this route have now successfully exceeded $35 per tonne and even climbed to an annual peak of $37 per tonne, setting a new high for the year. In particular, Australia and Brazil, the two major global iron ore exporting countries, maintained strong iron ore export activity throughout April. The continuous demand for cargo transportation provided strong support for the sustained rise in Capesize freight rates, which is also the core driving force behind the recent sharp increase in the Capesize index."

Affected by the correction in the Capesize index, the average daily revenue of corresponding vessels also declined. Data shows that Capesize vessels carrying 150,000 tons of cargo (mainly industrial raw materials such as iron ore and coal) saw their average daily revenue fall by $1,669, ultimately dropping to $41,438. Industry analysts stated that this decline in average daily revenue is closely related to the volatility in the iron ore futures market. Although iron ore futures have maintained an overall upward trend supported by stable downstream demand, short-term price fluctuations still had a certain suppressive effect on Capesize freight rates and average daily revenue, echoing the correction in the Capesize index on that day.

In the iron ore futures market, prices fell slightly on the day, mainly pressured by increased shipments of iron ore from Brazil and Simandou in Guinea. As a major global source of iron ore exports, Brazil has recently seen a continuous recovery in iron ore shipments. Meanwhile, the Simandou mine, the world's largest undeveloped high-quality mine, has been gradually increasing its shipments since it officially began operations in December 2025, further increasing supply pressure in the global iron ore market. At the same time, global pig iron production has reached a peak, and downstream steel industry demand for iron ore has largely stabilized. This means that there is limited room for further growth in future iron ore demand, indirectly constraining the upward momentum of iron ore futures prices and consequently dragging down Capesize freight rates.

In stark contrast to the correction in the Capesize sector, the Panamax sector performed strongly, becoming a key force supporting the overall index. The Panamax index rose slightly by 38 points, or 1.7%, to close at 2233 points, successfully reaching a new high in over two years and continuing its recent upward trend. Looking at the weekly performance, the index rose by 11.5% this week, slightly higher than the Capesize index, demonstrating the strong recovery of the Panamax market. As the mainstay vessel type for medium- and long-haul dry bulk trade, Panamax vessels are strictly sized to meet the navigation requirements of the Panama Canal. They primarily carry 60,000 to 70,000 tons of coal or grain, as well as other consumer goods and industrial raw materials, combining route flexibility with large cargo capacity.

As the Panamax index rose, the average daily revenue of the corresponding vessels also increased. Data shows that the average daily revenue of Panamax vessels increased by $341, reaching $20,099, a significant improvement compared to the same period last month. This growth is closely related to the recovery in global demand for the transportation of bulk commodities such as coal and grain. Recently, temperatures have gradually risen in many parts of the world, and coal demand has entered a seasonal recovery phase. At the same time, increased activity in global grain trade has further boosted the transportation demand for Panamax vessels, supporting the continued rise in freight rates and average daily revenue.

In the smaller tonnage vessel sector, the Very Large Vessel Index remained stable throughout the day, experiencing only minor fluctuations. The index rose by 1 point, or 0.1%, closing at 1522 points, essentially remaining within its recent trading range. Very large vessels primarily handle small-volume dry bulk cargo transport, including non-ferrous metal ores and minor agricultural products. Their freight rates are relatively stable and less affected by short-term market fluctuations. Industry insiders stated that although the Very Large Vessel Index saw a limited increase on the day, its overall stable performance reflects the stability of the global small-volume dry bulk shipping market, providing some support for the recovery of the entire dry bulk market.

In addition, geopolitical factors have also had a certain impact on the dry bulk market recently. The continued volatility in the Middle East has acted as a "volatility-driven catalyst," amplifying fluctuations in freight rates and, to some extent, boosting market sentiment. Although the Gulf region accounts for only about 4% of global dry bulk shipping, its impact on shipping routes has been significantly amplified. Currently, the volume of bulk carriers passing through the Strait of Hormuz is down by about 90% compared to normal levels, and regional disturbances have already had spillover effects on the global shipping network. However, with the recent proximity of the US and Iran to reaching a ceasefire memorandum of understanding, the situation in the Middle East is expected to ease, which may further stabilize expectations in the dry bulk shipping market.

The Baltic Dry Index (BDI), a key indicator tracking global dry bulk shipping rates, saw a slight decline on Friday, officially retreating from its more than two-year high reached in the previous trading day. However, thanks to its strong performance in the first four trading days of the week, the index still recorded a significant weekly gain, continuing the overall upward trend since April and reflecting the resilience of the global dry bulk shipping market recovery. As a core indicator measuring the cost of shipping key dry bulk commodities such as iron ore, coal, and grains globally, the fluctuations in the Baltic Dry Index directly reflect the dynamics of global dry bulk trading volume and are closely related to global economic conditions and raw material prices.

Specifically, the Baltic Dry Index, which tracks freight rates for the three major bulk carrier categories—Capesize, Panamax, and Supramax—fell 56 points, or 1.9%, to close at 2978. Notably, the index had climbed to its highest point since March 2024 on Thursday, reaching its peak in over two years, demonstrating the strong recovery momentum in the dry bulk market recently. Looking at the weekly performance, despite a slight pullback on Friday, the index still rose 9.1% this week, marking two consecutive weeks of gains and further consolidating the market recovery. This also continues the two-month upward trend since the index bottomed out in early March, with a cumulative increase exceeding 40%.

Among the various vessel types, the Capesize sector was the main drag on the day's correction. The Capesize index fell sharply by 184 points, a drop of 3.6%, closing at 4955 points, a significant decline from the five-month high reached on Thursday, ending a four-day winning streak. However, the sector's overall performance this week was still strong, with a cumulative increase of 11.4%, becoming one of the important forces driving the overall index's weekly rise. As the mainstay of global dry bulk shipping, Capesize vessels primarily carry 150,000 tons of industrial bulk raw materials such as iron ore and coal, and their freight rates are highly correlated with the activity of global iron ore trade.

In a recent market report, Maria Bertzeletou, Senior Market Analyst at Signal Group, clearly stated: "The market performance in the first week of May further confirmed the strong upward momentum in the Atlantic Capesize bulk carrier freight market in April. Freight rates on this route have now successfully exceeded $35 per tonne and even climbed to an annual peak of $37 per tonne, setting a new high for the year. In particular, Australia and Brazil, the two major global iron ore exporting countries, maintained strong iron ore export activity throughout April. The continuous demand for cargo transportation provided strong support for the sustained rise in Capesize freight rates, which is also the core driving force behind the recent sharp increase in the Capesize index."

Affected by the correction in the Capesize index, the average daily revenue of corresponding vessels also declined. Data shows that Capesize vessels carrying 150,000 tons of cargo (mainly industrial raw materials such as iron ore and coal) saw their average daily revenue fall by $1,669, ultimately dropping to $41,438. Industry analysts stated that this decline in average daily revenue is closely related to the volatility in the iron ore futures market. Although iron ore futures have maintained an overall upward trend supported by stable downstream demand, short-term price fluctuations still had a certain suppressive effect on Capesize freight rates and average daily revenue, echoing the correction in the Capesize index on that day.

In the iron ore futures market, prices fell slightly on the day, mainly pressured by increased shipments of iron ore from Brazil and Simandou in Guinea. As a major global source of iron ore exports, Brazil has recently seen a continuous recovery in iron ore shipments. Meanwhile, the Simandou mine, the world's largest undeveloped high-quality mine, has been gradually increasing its shipments since it officially began operations in December 2025, further increasing supply pressure in the global iron ore market. At the same time, global pig iron production has reached a peak, and downstream steel industry demand for iron ore has largely stabilized. This means that there is limited room for further growth in future iron ore demand, indirectly constraining the upward momentum of iron ore futures prices and consequently dragging down Capesize freight rates.

In stark contrast to the correction in the Capesize sector, the Panamax sector performed strongly, becoming a key force supporting the overall index. The Panamax index rose slightly by 38 points, or 1.7%, to close at 2233 points, successfully reaching a new high in over two years and continuing its recent upward trend. Looking at the weekly performance, the index rose by 11.5% this week, slightly higher than the Capesize index, demonstrating the strong recovery of the Panamax market. As the mainstay vessel type for medium- and long-haul dry bulk trade, Panamax vessels are strictly sized to meet the navigation requirements of the Panama Canal. They primarily carry 60,000 to 70,000 tons of coal or grain, as well as other consumer goods and industrial raw materials, combining route flexibility with large cargo capacity.

As the Panamax index rose, the average daily revenue of the corresponding vessels also increased. Data shows that the average daily revenue of Panamax vessels increased by $341, reaching $20,099, a significant improvement compared to the same period last month. This growth is closely related to the recovery in global demand for the transportation of bulk commodities such as coal and grain. Recently, temperatures have gradually risen in many parts of the world, and coal demand has entered a seasonal recovery phase. At the same time, increased activity in global grain trade has further boosted the transportation demand for Panamax vessels, supporting the continued rise in freight rates and average daily revenue.

In the smaller tonnage vessel sector, the Very Large Vessel Index remained stable throughout the day, experiencing only minor fluctuations. The index rose by 1 point, or 0.1%, closing at 1522 points, essentially remaining within its recent trading range. Very large vessels primarily handle small-volume dry bulk cargo transport, including non-ferrous metal ores and minor agricultural products. Their freight rates are relatively stable and less affected by short-term market fluctuations. Industry insiders stated that although the Very Large Vessel Index saw a limited increase on the day, its overall stable performance reflects the stability of the global small-volume dry bulk shipping market, providing some support for the recovery of the entire dry bulk market.

In addition, geopolitical factors have also had a certain impact on the dry bulk market recently. The continued volatility in the Middle East has acted as a "volatility-driven catalyst," amplifying fluctuations in freight rates and, to some extent, boosting market sentiment. Although the Gulf region accounts for only about 4% of global dry bulk shipping, its impact on shipping routes has been significantly amplified. Currently, the volume of bulk carriers passing through the Strait of Hormuz is down by about 90% compared to normal levels, and regional disturbances have already had spillover effects on the global shipping network. However, with the recent proximity of the US and Iran to reaching a ceasefire memorandum of understanding, the situation in the Middle East is expected to ease, which may further stabilize expectations in the dry bulk shipping market.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.