Out-of-control interest rates led to gold weakness; two key turning points to watch.

2026-05-20 16:17:12

Spot gold continued to lack positive momentum on Wednesday (Asian and European sessions), failing to rebound significantly after a full day of one-sided declines, and is currently trading around 4477.

Recently, multiple factors in the market have been unfavorable to gold prices. From geopolitics to holding costs and the pricing of gold in relation to the US dollar index, all have released news that is not good for gold. However, as the saying goes, opportunities arise from declines and risks arise from rises. The market is waiting for a new opportunity to position itself in gold.

Recently, US President Trump optimistically declared at the White House that "the war with Iran will end very quickly" and insisted that Iran is tired of the war and "eager to reach an agreement".

However, the true story behind the negotiations was chilling.

Even more dangerously, the aborted ceasefire is accompanied by a substantial escalation of the conflict. Last weekend, a drone from Iraq struck a generator at the Barakah nuclear power plant in the UAE, sparking strong condemnation from the region. In the past 48 hours, the UAE has intercepted six more drones.

Faced with Iran's pressure tactics of blocking the Strait of Hormuz and frequently harassing the Persian Gulf with drones and missiles, a military counterattack by the United States and Israel is imminent.

According to mediators and US officials familiar with the matter, Iran's position in the US-Iran negotiations has not changed substantially. It not only insists on ending hostilities, obtaining huge amounts of financial aid and war reparations, but also seeks to gain control of the monitoring in the Strait of Hormuz.

The differences between the two sides on their nuclear programs are like a chasm, and there is much skepticism about whether a solution can be reached.

Sources familiar with the matter revealed that the US and Israel had been preparing to launch a new attack on Iran within days, possibly as early as next week. Trump publicly warned, "We may have to give them another big blow," and Vice President Vance also expressed reservations about the prospects of the agreement.

However, the root cause of gold's recent lack of luster, besides the slow progress of the US-Iran peace talks and the possibility of another major war, lies in the persistently high yields on government bonds, the "stabilizing force" of the global financial market, which have exerted strong downward pressure on gold prices.

Currently, a sell-off storm, the worst in decades, is unfolding in the global secondary market.

Not only did government bond yields in the United States, Japan, and the United Kingdom surge, but global corporate bond yields also saw a simultaneous sharp rise, indicating a concentrated sell-off of various bonds.

As we know from common financial knowledge, bond yields are inversely proportional to prices. The collective surge in yields is essentially a direct result of global funds voting with their feet in the secondary market and frantically selling bonds at a loss.

Why are investors so determined to flee the bond market? This is intertwined with changes in macroeconomic policies and a deep-seated credit crisis.

First, the attack on the Baraka nuclear power plant and the crisis of a complete blockade of the Strait of Hormuz directly ignited the engine of soaring prices for commodities such as crude oil, and persistently high inflation has once again become a nightmare for all fixed-income assets.

With core inflation rising again due to the energy crisis, market concerns about "prolonged inflation" have become a reality.

More importantly, the Federal Reserve has just experienced a "change of government." New Fed Chairman Kevin Warsh came to power with great difficulty in a historically divided vote, and he faces an extremely perilous economic environment: on the one hand, the task of double-dip inflation fueled by geopolitical crises is far from over, and on the other hand, there is enormous political pressure to cut interest rates.

How can the new head rebuild the Federal Reserve's credibility with the promise of "regime change"?

This significant uncertainty surrounding monetary policy has led secondary market traders to sell off their holdings, pushing up overall interest rates.

Delving into the debt structure, this sell-off resembles a "credit trial" targeting both the nation and the company:

For nations: a systemic decline in the ability of borrowing countries to repay their debts.

Whether it's the massive debt accumulated by the United States due to years of war and fiscal deficits, or the fiscal holes in various European countries, the market has seen through the rogue game of sovereign states—they are unlikely to default directly, but they will most likely be forced to maintain high inflation by printing money excessively and using "worthless" bills with severely diminished future purchasing power to repay previous loans.

To combat this implicit default (inflation tax), investors have no choice but to frantically sell off government bonds, demanding a higher risk premium.

For companies: direct default and cash flow panic. Unlike the government, which can print money, companies must use profits to pay off debts.

With the sharp drop in corporate bond prices and soaring yields in the secondary market, the financial trick of "borrowing new to repay old" is no longer viable for companies in such a high-interest-rate environment.

Nowadays, companies that want to issue new bonds to extend their maturities must pay extremely high, or even unbearable, interest costs. This not only directly threatens the company's cash flow security, but also reflects the market's extreme concern about whether its subsequent profitability can cover the high interest rates.

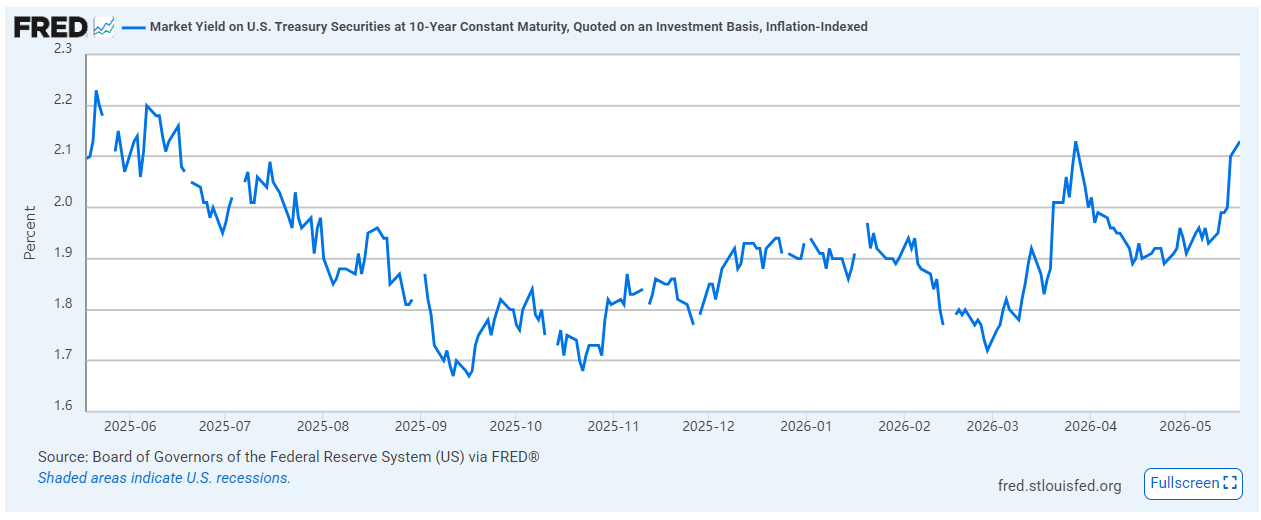

Returning to the pricing logic of gold, as a non-dividend-paying asset, the biggest opportunity cost of gold is the real interest rate (nominal interest rate minus inflation expectations). The real interest rate has long been severely negatively correlated with gold, and the TIPS rate basically reflects the real interest rate in the market. Recently, this rate has risen rapidly.

(Chart showing the yield trend of 10-year TIPS (Treasury Inflation Protected Securities), Source: Federal Reserve)

The massive amounts of money fleeing the secondary bond market after suffering losses are now pouring into money market funds or ultra-short-term US Treasury bonds to lock in risk-free returns of over 5%, thus creating a temporary "vampire effect" on gold.

This is the fundamental reason why gold has remained weak even in the face of traditionally bullish factors such as the attack on the Barakah nuclear power plant and the breakdown of Middle East peace talks.

However, as mentioned in the first half of the article, the underlying logic behind the surge in government bond yields is the market's desperate protest against the government's policy of "diluting debt and maintaining high inflation."

This means that the current bond market sell-off is constantly undermining the credit of fiat currency. Once the Federal Reserve under Warsh's leadership shows its willingness to compromise on interest rate hikes in the face of war and inflation, or if a wave of corporate bond defaults truly breaks out and triggers a systemic liquidity crisis, then these huge amounts of funds that have been waiting and watching in the short term with high-interest instruments will instantly realize that only "hard currencies" such as gold can save them.

Currently, the lack of petrodollar revenue in the Gulf countries has forced them to buy dollars, and some are even selling gold to exchange for dollars. The sharp rebound in the dollar price has directly suppressed gold prices.

Meanwhile, high inflation and high global interest rate pressures make it difficult for gold prices to rise. However, as US Treasury yields continue to rise, it will be very difficult for the US government to issue bonds to achieve its goals, which will ultimately limit the president's military operations. This means that there is a limit to the rise in interest rates. Once the Straits of Hormuz reopens, Middle Eastern countries that have obtained petrodollars will reduce their exchange of dollars and are likely to redeem their gold.

Therefore, it is still necessary to closely monitor the marginal changes in navigation in the Strait of Hormuz and the actions of the Federal Reserve. Good investment opportunities are like springs; the tighter they are stretched, the more violently they bounce back.

From a technical perspective, gold prices have recently broken out of their downward trend, with resistance near the 5-day moving average and the middle line of the descending channel.

(Spot gold daily chart, source:)

At 16:06 Beijing time, spot gold was trading at $4,480 per ounce.

Recently, multiple factors in the market have been unfavorable to gold prices. From geopolitics to holding costs and the pricing of gold in relation to the US dollar index, all have released news that is not good for gold. However, as the saying goes, opportunities arise from declines and risks arise from rises. The market is waiting for a new opportunity to position itself in gold.

Recently, US President Trump optimistically declared at the White House that "the war with Iran will end very quickly" and insisted that Iran is tired of the war and "eager to reach an agreement".

However, the true story behind the negotiations was chilling.

Even more dangerously, the aborted ceasefire is accompanied by a substantial escalation of the conflict. Last weekend, a drone from Iraq struck a generator at the Barakah nuclear power plant in the UAE, sparking strong condemnation from the region. In the past 48 hours, the UAE has intercepted six more drones.

Faced with Iran's pressure tactics of blocking the Strait of Hormuz and frequently harassing the Persian Gulf with drones and missiles, a military counterattack by the United States and Israel is imminent.

According to mediators and US officials familiar with the matter, Iran's position in the US-Iran negotiations has not changed substantially. It not only insists on ending hostilities, obtaining huge amounts of financial aid and war reparations, but also seeks to gain control of the monitoring in the Strait of Hormuz.

The differences between the two sides on their nuclear programs are like a chasm, and there is much skepticism about whether a solution can be reached.

Sources familiar with the matter revealed that the US and Israel had been preparing to launch a new attack on Iran within days, possibly as early as next week. Trump publicly warned, "We may have to give them another big blow," and Vice President Vance also expressed reservations about the prospects of the agreement.

However, the root cause of gold's recent lack of luster, besides the slow progress of the US-Iran peace talks and the possibility of another major war, lies in the persistently high yields on government bonds, the "stabilizing force" of the global financial market, which have exerted strong downward pressure on gold prices.

A global sell-off in bond markets

Currently, a sell-off storm, the worst in decades, is unfolding in the global secondary market.

Not only did government bond yields in the United States, Japan, and the United Kingdom surge, but global corporate bond yields also saw a simultaneous sharp rise, indicating a concentrated sell-off of various bonds.

As we know from common financial knowledge, bond yields are inversely proportional to prices. The collective surge in yields is essentially a direct result of global funds voting with their feet in the secondary market and frantically selling bonds at a loss.

Why are investors so determined to flee the bond market? This is intertwined with changes in macroeconomic policies and a deep-seated credit crisis.

The specter of inflation and the perilous environment of the new Fed chief

First, the attack on the Baraka nuclear power plant and the crisis of a complete blockade of the Strait of Hormuz directly ignited the engine of soaring prices for commodities such as crude oil, and persistently high inflation has once again become a nightmare for all fixed-income assets.

With core inflation rising again due to the energy crisis, market concerns about "prolonged inflation" have become a reality.

More importantly, the Federal Reserve has just experienced a "change of government." New Fed Chairman Kevin Warsh came to power with great difficulty in a historically divided vote, and he faces an extremely perilous economic environment: on the one hand, the task of double-dip inflation fueled by geopolitical crises is far from over, and on the other hand, there is enormous political pressure to cut interest rates.

How can the new head rebuild the Federal Reserve's credibility with the promise of "regime change"?

This significant uncertainty surrounding monetary policy has led secondary market traders to sell off their holdings, pushing up overall interest rates.

Devaluation of national credit and the survival crisis of enterprises

Delving into the debt structure, this sell-off resembles a "credit trial" targeting both the nation and the company:

For nations: a systemic decline in the ability of borrowing countries to repay their debts.

Whether it's the massive debt accumulated by the United States due to years of war and fiscal deficits, or the fiscal holes in various European countries, the market has seen through the rogue game of sovereign states—they are unlikely to default directly, but they will most likely be forced to maintain high inflation by printing money excessively and using "worthless" bills with severely diminished future purchasing power to repay previous loans.

To combat this implicit default (inflation tax), investors have no choice but to frantically sell off government bonds, demanding a higher risk premium.

For companies: direct default and cash flow panic. Unlike the government, which can print money, companies must use profits to pay off debts.

With the sharp drop in corporate bond prices and soaring yields in the secondary market, the financial trick of "borrowing new to repay old" is no longer viable for companies in such a high-interest-rate environment.

Nowadays, companies that want to issue new bonds to extend their maturities must pay extremely high, or even unbearable, interest costs. This not only directly threatens the company's cash flow security, but also reflects the market's extreme concern about whether its subsequent profitability can cover the high interest rates.

The ultimate link between gold and the bond market

Returning to the pricing logic of gold, as a non-dividend-paying asset, the biggest opportunity cost of gold is the real interest rate (nominal interest rate minus inflation expectations). The real interest rate has long been severely negatively correlated with gold, and the TIPS rate basically reflects the real interest rate in the market. Recently, this rate has risen rapidly.

(Chart showing the yield trend of 10-year TIPS (Treasury Inflation Protected Securities), Source: Federal Reserve)

The massive amounts of money fleeing the secondary bond market after suffering losses are now pouring into money market funds or ultra-short-term US Treasury bonds to lock in risk-free returns of over 5%, thus creating a temporary "vampire effect" on gold.

This is the fundamental reason why gold has remained weak even in the face of traditionally bullish factors such as the attack on the Barakah nuclear power plant and the breakdown of Middle East peace talks.

However, as mentioned in the first half of the article, the underlying logic behind the surge in government bond yields is the market's desperate protest against the government's policy of "diluting debt and maintaining high inflation."

This means that the current bond market sell-off is constantly undermining the credit of fiat currency. Once the Federal Reserve under Warsh's leadership shows its willingness to compromise on interest rate hikes in the face of war and inflation, or if a wave of corporate bond defaults truly breaks out and triggers a systemic liquidity crisis, then these huge amounts of funds that have been waiting and watching in the short term with high-interest instruments will instantly realize that only "hard currencies" such as gold can save them.

Summary and Technical Analysis:

Currently, the lack of petrodollar revenue in the Gulf countries has forced them to buy dollars, and some are even selling gold to exchange for dollars. The sharp rebound in the dollar price has directly suppressed gold prices.

Meanwhile, high inflation and high global interest rate pressures make it difficult for gold prices to rise. However, as US Treasury yields continue to rise, it will be very difficult for the US government to issue bonds to achieve its goals, which will ultimately limit the president's military operations. This means that there is a limit to the rise in interest rates. Once the Straits of Hormuz reopens, Middle Eastern countries that have obtained petrodollars will reduce their exchange of dollars and are likely to redeem their gold.

Therefore, it is still necessary to closely monitor the marginal changes in navigation in the Strait of Hormuz and the actions of the Federal Reserve. Good investment opportunities are like springs; the tighter they are stretched, the more violently they bounce back.

From a technical perspective, gold prices have recently broken out of their downward trend, with resistance near the 5-day moving average and the middle line of the descending channel.

(Spot gold daily chart, source:)

At 16:06 Beijing time, spot gold was trading at $4,480 per ounce.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.