Institutional analysis of this year's commodity market: The overall bull market continues, with gold prices facing short-term pressure but the long-term upward trend remains unchanged.

2026-06-02 13:26:34

UBS's latest commodities research report points out that the trajectory of the US-Iran rivalry is the core driving force in the short-term commodity market. Various geopolitical disturbances have increased market volatility, leading to a significant overall rise in commodities this year. While gold is facing short-term downward pressure due to high interest rates and a strong dollar, with prices consolidating, crude oil and base metals are supported by strong supply-demand gaps.

Institutions have clearly stated their continued optimism about the value of commodities in 2026, arguing that they can hedge against inflation and energy supply risks. They also recommend that investors optimize their asset structure, shifting from a single heavy position in gold to a diversified portfolio of commodities.

In a recent research report released on Monday (June 1), UBS commodities analyst Giovanni Staunovo stated that the ongoing geopolitical tensions in the Middle East have continued to increase volatility in commodity markets, while simultaneously driving significant gains across all asset classes.

Market data shows that Brent crude oil hit a four-year high of $126 per barrel on April 30, before subsequently retreating, and is currently trading around $94 per barrel. Gold prices are relatively weak, down about 16% from their record closing high in January of this year, mainly due to rising market expectations of interest rate hikes, which continue to suppress market sentiment and buying momentum for gold.

According to UBS CMCI Composite Total Return US Dollar Index, the overall price of all commodities has risen by more than 20% since the beginning of this year, and the overall bull market trend is stable.

Analysts say that even if geopolitical risk premiums gradually subside, the fundamentals of crude oil, gold, and base metals remain solid, sufficient to support steady price movements. Currently, refined oil inventories in many countries continue to decline, and during the inventory replenishment cycle, oil prices may further rise to adjust market demand, making a rapid reversal of the tight supply-demand balance unlikely.

Affected by high US Treasury yields and a continued strengthening of the US dollar, UBS lowered its year-end target price for gold last week, from $5,900 per ounce to $5,500.

UBS analysts Dominic Schnider and Wayne Gordon stated that the market is currently highly focused on the opportunity cost of capital, gold's attractiveness as a zero-interest asset has declined, demand for gold ETFs and futures trading has cooled significantly, short-term capital inflows are weak, and it is unlikely to replicate the upward trend seen at the beginning of the year.

However, institutions did not deny the long-term bullish trend in gold, but merely advised investors to patiently wait for market correction, noting that gold prices still have room to rise by thousands of dollars by the end of the year. Institutions predict that global monetary policy is likely to become neutral in 2027, and the strengthening of the US dollar may reverse, at which point gold's attractiveness as an asset allocation will rise again. Looking back at historical trends, whether it was the Russia-Ukraine conflict in 2022, or the Gulf War and the Iraq War, gold has consistently exhibited a pattern of "rising prices at the beginning of the conflict and falling back during the interest rate hike cycle," a pattern highly consistent with the current market trend.

Giovanni Stanovo added that in the medium to long term, high global debt pressure, the persistent US fiscal deficit, and the diversification of foreign exchange reserves by various countries will continue to benefit gold prices. Meanwhile, the widening supply-demand gap in base metals such as copper and aluminum, coupled with long-term industrial support from the global electrification transition, provides ample upward momentum for prices.

Based on this, UBS advises investors to adjust their portfolio allocation strategy and avoid placing too much emphasis on gold.

For investors holding substantial gold positions and accumulating considerable unrealized profits, it is advisable to moderately increase allocations to commodities such as copper, aluminum, and agricultural products to diversify income sources and mitigate investment risks. For ordinary investors, a small portion of gold can be allocated to a diversified asset portfolio to hedge against systemic risks arising from geopolitical conflicts and high inflation. Furthermore, continued gold purchases by central banks worldwide and increased gold jewelry consumption in Asia will further solidify underlying demand for gold, providing strong support for market trends.

Overall, the overall bullish trend in commodities remains unchanged in 2026. In the short term, gold is under pressure from macroeconomic factors and is undergoing a period of consolidation, while crude oil and base metals are maintaining their strength due to supply and demand gaps. The long-tail effect of geopolitical conflicts, inflationary pressures, and industrial upgrading together form the long-term positive foundation for the commodity market.

Against the backdrop of increasing global economic uncertainty, proactive management and diversified investment in commodities remain a high-quality strategy for hedging market risks and enhancing investment returns.

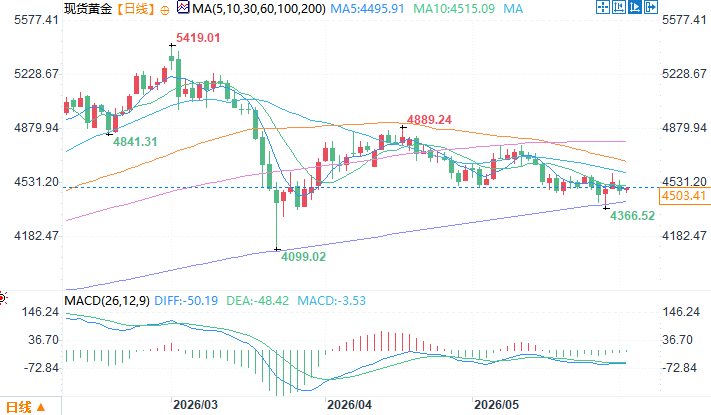

Spot gold daily chart source: EasyForex

At 13:26 Beijing time on June 2, spot gold was trading at $4517.41 per ounce.

Institutions have clearly stated their continued optimism about the value of commodities in 2026, arguing that they can hedge against inflation and energy supply risks. They also recommend that investors optimize their asset structure, shifting from a single heavy position in gold to a diversified portfolio of commodities.

Geopolitical disturbances dominated the market, and commodities saw considerable overall gains.

In a recent research report released on Monday (June 1), UBS commodities analyst Giovanni Staunovo stated that the ongoing geopolitical tensions in the Middle East have continued to increase volatility in commodity markets, while simultaneously driving significant gains across all asset classes.

Market data shows that Brent crude oil hit a four-year high of $126 per barrel on April 30, before subsequently retreating, and is currently trading around $94 per barrel. Gold prices are relatively weak, down about 16% from their record closing high in January of this year, mainly due to rising market expectations of interest rate hikes, which continue to suppress market sentiment and buying momentum for gold.

According to UBS CMCI Composite Total Return US Dollar Index, the overall price of all commodities has risen by more than 20% since the beginning of this year, and the overall bull market trend is stable.

Analysts say that even if geopolitical risk premiums gradually subside, the fundamentals of crude oil, gold, and base metals remain solid, sufficient to support steady price movements. Currently, refined oil inventories in many countries continue to decline, and during the inventory replenishment cycle, oil prices may further rise to adjust market demand, making a rapid reversal of the tight supply-demand balance unlikely.

Gold price expectations have been slightly lowered, but the long-term bull market logic has not ended.

Affected by high US Treasury yields and a continued strengthening of the US dollar, UBS lowered its year-end target price for gold last week, from $5,900 per ounce to $5,500.

UBS analysts Dominic Schnider and Wayne Gordon stated that the market is currently highly focused on the opportunity cost of capital, gold's attractiveness as a zero-interest asset has declined, demand for gold ETFs and futures trading has cooled significantly, short-term capital inflows are weak, and it is unlikely to replicate the upward trend seen at the beginning of the year.

However, institutions did not deny the long-term bullish trend in gold, but merely advised investors to patiently wait for market correction, noting that gold prices still have room to rise by thousands of dollars by the end of the year. Institutions predict that global monetary policy is likely to become neutral in 2027, and the strengthening of the US dollar may reverse, at which point gold's attractiveness as an asset allocation will rise again. Looking back at historical trends, whether it was the Russia-Ukraine conflict in 2022, or the Gulf War and the Iraq War, gold has consistently exhibited a pattern of "rising prices at the beginning of the conflict and falling back during the interest rate hike cycle," a pattern highly consistent with the current market trend.

The value of diversified commodities is becoming more apparent, leading to an optimization of asset allocation strategies.

Giovanni Stanovo added that in the medium to long term, high global debt pressure, the persistent US fiscal deficit, and the diversification of foreign exchange reserves by various countries will continue to benefit gold prices. Meanwhile, the widening supply-demand gap in base metals such as copper and aluminum, coupled with long-term industrial support from the global electrification transition, provides ample upward momentum for prices.

Based on this, UBS advises investors to adjust their portfolio allocation strategy and avoid placing too much emphasis on gold.

For investors holding substantial gold positions and accumulating considerable unrealized profits, it is advisable to moderately increase allocations to commodities such as copper, aluminum, and agricultural products to diversify income sources and mitigate investment risks. For ordinary investors, a small portion of gold can be allocated to a diversified asset portfolio to hedge against systemic risks arising from geopolitical conflicts and high inflation. Furthermore, continued gold purchases by central banks worldwide and increased gold jewelry consumption in Asia will further solidify underlying demand for gold, providing strong support for market trends.

Summarize

Overall, the overall bullish trend in commodities remains unchanged in 2026. In the short term, gold is under pressure from macroeconomic factors and is undergoing a period of consolidation, while crude oil and base metals are maintaining their strength due to supply and demand gaps. The long-tail effect of geopolitical conflicts, inflationary pressures, and industrial upgrading together form the long-term positive foundation for the commodity market.

Against the backdrop of increasing global economic uncertainty, proactive management and diversified investment in commodities remain a high-quality strategy for hedging market risks and enhancing investment returns.

Spot gold daily chart source: EasyForex

At 13:26 Beijing time on June 2, spot gold was trading at $4517.41 per ounce.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.