The S&P 500 retreated 3%, are traders starting to get nervous?

2026-06-10 20:31:07

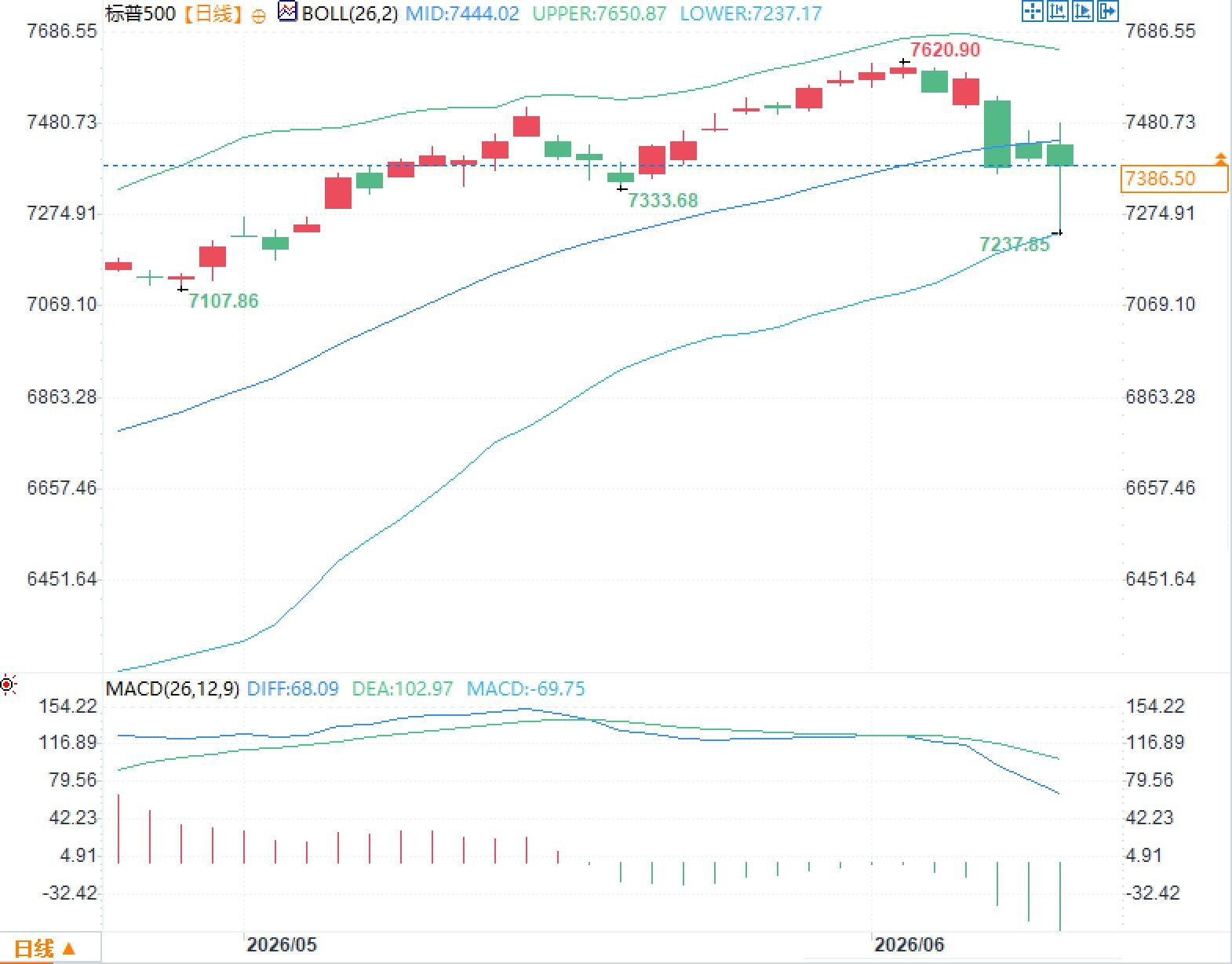

On Wednesday, June 10th, market risk appetite was rapidly cooling. The S&P 500 closed at 7386.50 on June 9th, down approximately 2.9% from its June 2nd closing level of 7609.78; the Nasdaq 100 closed at 29084.50 on June 9th, with a significantly wider daily trading range; the VIX closed around 19.87, having significantly moved away from its previous low volatility range. The market focus was not simply shifting from gains to losses, but rather from "anxiety about missing out on gains" to "risk exposure during downturns." This change was more directly reflected in the options market, where funds did not completely withdraw from strong tech stocks, but instead began to concentrate on buying protection at the index level.

The signals from the options market are sharper than those from the stock index. Data from the options exchange's derivatives intelligence team shows that the S&P 500's one-month skew has risen rapidly from a one-year low to the 72nd percentile, meaning that the relative price of downside protection has been raised again; the proportion of put options opened by retail investors in large-cap tech stocks has also risen from 15% a week ago to 27%. Analysts believe that the market previously lacked hedging against downside risks, and the current reversal at the index level indicates that investors are beginning to assess the possibility of the next decline.

The key issue isn't that investors suddenly abandoned tech leaders, but rather that risk budgets have begun to stratify. On one hand, individual stocks still retain exposure to profit-driven winners; on the other hand, indices are using protective tools to hedge against a synchronized decline. This indicates that the market isn't worried about the fundamentals of a particular company, but rather about the correlational shocks caused by the combined effects of interest rates, inflation, energy prices, and valuations. In other words, as long as macroeconomic factors outweigh individual stock narratives, low correlations can quickly turn into high correlations, and the price of index protection will continue to reflect this tail risk premium.

The Federal Reserve's current target range for the federal funds rate is 3.50% to 3.75%, a range it will maintain after its April meeting. Inflationary pressures remain, with the April CPI rising 0.6% month-on-month and 3.8% year-on-year; core CPI rose 0.4% month-on-month and 2.8% year-on-year.

The constraint on interest rate-sensitive assets lies in the fact that inflation is not solely driven by energy prices. A rise in energy prices will first affect the overall CPI, then be transmitted to core sectors through transportation, food, and service costs. Once core inflation remains near 3%, the Federal Reserve will find it difficult to quickly shift to an easing stance. With non-farm payrolls increasing by 172,000 in May and the unemployment rate remaining at 4.3%, the labor market has not provided a clear reason for policy easing. For highly valued sectors, this means that expectations of a declining discount rate have been weakened, and the earnings narrative must face greater pressure to be validated.

The most noteworthy aspect of this correction is the structural divergence. While the index decline hasn't reached panic levels, technology and semiconductor-related assets have experienced more significant volatility. On June 9th, the Nasdaq Composite Index fell by approximately 1%, and the S&P 500 fell by 0.3%, but the intraday reversal of high-flying AI-related assets was more pronounced, indicating that investors' tolerance for crowded trades is decreasing.

This doesn't mean the technology theme has been completely rejected by the market. On the contrary, many funds still see leading technology companies as the area with the highest profit elasticity, but are simultaneously buying insurance at the index level. Analysts believe that current macro-level stock index protection still has strong risk-reward appeal because the correlation between individual stocks remains low, making index protection "still plausible." The implication is that traders haven't denied the upward momentum of a single strong company, but are instead guarding against macro factors triggering a synchronized revaluation of a basket of assets.

The current market vulnerability lies not in the S&P 500's approximately 3% pullback from its peak, but in the excessively low protective positions and overly optimistic pricing during the previous rally. If energy prices remain high, US Treasury yields may continue to suppress stock valuations, and the correlation between index constituents may increase. At that point, the technology, consumer discretionary, semiconductor, and high-valuation growth sectors may shift from "stock differentiation" to "homogeneous adjustment of risk assets."

It is important to emphasize that this is not a trading judgment on market direction, but rather an observation of risk pricing mechanisms. Increased index skewness, a rise in the proportion of put options, the VIX moving away from its lows, and increased uncertainty surrounding the CPI and the Fed's path all indicate that the market is repricing tail risks.

Demand for index protection is rising, and risk is shifting from individual stocks to the systemic level.

The signals from the options market are sharper than those from the stock index. Data from the options exchange's derivatives intelligence team shows that the S&P 500's one-month skew has risen rapidly from a one-year low to the 72nd percentile, meaning that the relative price of downside protection has been raised again; the proportion of put options opened by retail investors in large-cap tech stocks has also risen from 15% a week ago to 27%. Analysts believe that the market previously lacked hedging against downside risks, and the current reversal at the index level indicates that investors are beginning to assess the possibility of the next decline.

The key issue isn't that investors suddenly abandoned tech leaders, but rather that risk budgets have begun to stratify. On one hand, individual stocks still retain exposure to profit-driven winners; on the other hand, indices are using protective tools to hedge against a synchronized decline. This indicates that the market isn't worried about the fundamentals of a particular company, but rather about the correlational shocks caused by the combined effects of interest rates, inflation, energy prices, and valuations. In other words, as long as macroeconomic factors outweigh individual stock narratives, low correlations can quickly turn into high correlations, and the price of index protection will continue to reflect this tail risk premium.

Inflation and interest rates have once again become the upper limit for valuations.

The Federal Reserve's current target range for the federal funds rate is 3.50% to 3.75%, a range it will maintain after its April meeting. Inflationary pressures remain, with the April CPI rising 0.6% month-on-month and 3.8% year-on-year; core CPI rose 0.4% month-on-month and 2.8% year-on-year.

The constraint on interest rate-sensitive assets lies in the fact that inflation is not solely driven by energy prices. A rise in energy prices will first affect the overall CPI, then be transmitted to core sectors through transportation, food, and service costs. Once core inflation remains near 3%, the Federal Reserve will find it difficult to quickly shift to an easing stance. With non-farm payrolls increasing by 172,000 in May and the unemployment rate remaining at 4.3%, the labor market has not provided a clear reason for policy easing. For highly valued sectors, this means that expectations of a declining discount rate have been weakened, and the earnings narrative must face greater pressure to be validated.

Technology stocks remain the main theme, but crowding is increasing, leading to greater volatility.

The most noteworthy aspect of this correction is the structural divergence. While the index decline hasn't reached panic levels, technology and semiconductor-related assets have experienced more significant volatility. On June 9th, the Nasdaq Composite Index fell by approximately 1%, and the S&P 500 fell by 0.3%, but the intraday reversal of high-flying AI-related assets was more pronounced, indicating that investors' tolerance for crowded trades is decreasing.

This doesn't mean the technology theme has been completely rejected by the market. On the contrary, many funds still see leading technology companies as the area with the highest profit elasticity, but are simultaneously buying insurance at the index level. Analysts believe that current macro-level stock index protection still has strong risk-reward appeal because the correlation between individual stocks remains low, making index protection "still plausible." The implication is that traders haven't denied the upward momentum of a single strong company, but are instead guarding against macro factors triggering a synchronized revaluation of a basket of assets.

The real risk is the correlation shock, not the single-day drop.

The current market vulnerability lies not in the S&P 500's approximately 3% pullback from its peak, but in the excessively low protective positions and overly optimistic pricing during the previous rally. If energy prices remain high, US Treasury yields may continue to suppress stock valuations, and the correlation between index constituents may increase. At that point, the technology, consumer discretionary, semiconductor, and high-valuation growth sectors may shift from "stock differentiation" to "homogeneous adjustment of risk assets."

It is important to emphasize that this is not a trading judgment on market direction, but rather an observation of risk pricing mechanisms. Increased index skewness, a rise in the proportion of put options, the VIX moving away from its lows, and increased uncertainty surrounding the CPI and the Fed's path all indicate that the market is repricing tail risks.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.