What is the underlying logic behind central bank gold purchases? It involves a triple interplay of holding levels, geopolitical risks, and the dollar cycle.

2026-06-16 20:01:31

The special survey jointly conducted by the World Gold Council and YouGov in 2026 (execution period from February 5 to May 19) achieved the highest participation rate in nine years with 76 valid questionnaires. The sample covers major developed economies and emerging markets and developing economies (EMDE) around the world, making it highly representative.

It is worth noting that the vast majority of the feedback came after the outbreak of the Middle East conflict, truly reflecting the central bank's asset allocation strategy under the escalation of geopolitical risks.

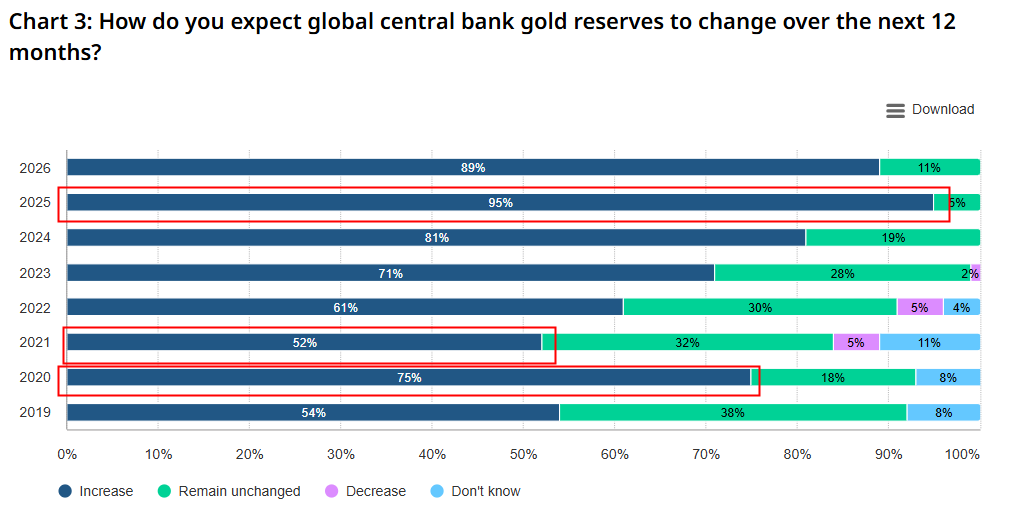

Research shows that central banks' optimistic expectations for gold continue to strengthen: 89% of the surveyed institutions predict that global official gold reserves will continue to rise over the next 12 months.

(Central banks' expectations regarding whether they will increase or decrease their gold holdings in the future. Source: World Gold Council)

The data comparison above reveals a correlation between gold price performance and the bullish sentiment of central banks. For instance, in 2022, only slightly over 50% of central banks were bullish, and gold prices did consolidate for a year. Later, as gold prices continued to rise, central banks remained bullish on gold. In 2026, while central banks were generally bullish on gold, the number of central banks bullish on it was declining compared to 2025. This is noteworthy, as it may indicate that some central banks believe they need to reduce their gold holdings, such as central banks in the Middle East that need to convert to US dollars for emergencies.

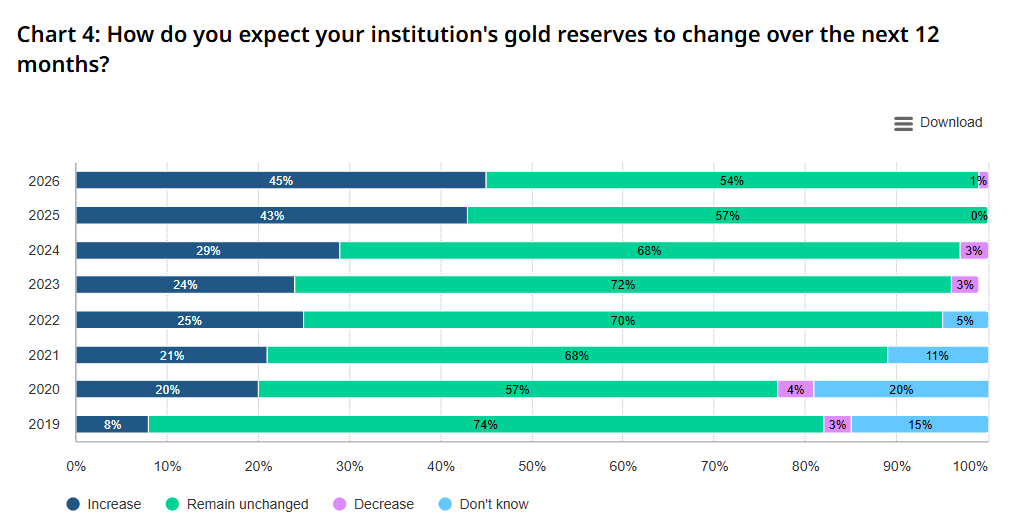

(Central banks' expectations for whether institutions will increase or decrease their gold holdings in the future. Source: World Gold Council)

Asset diversification has become a core keyword in central bank reserve management.

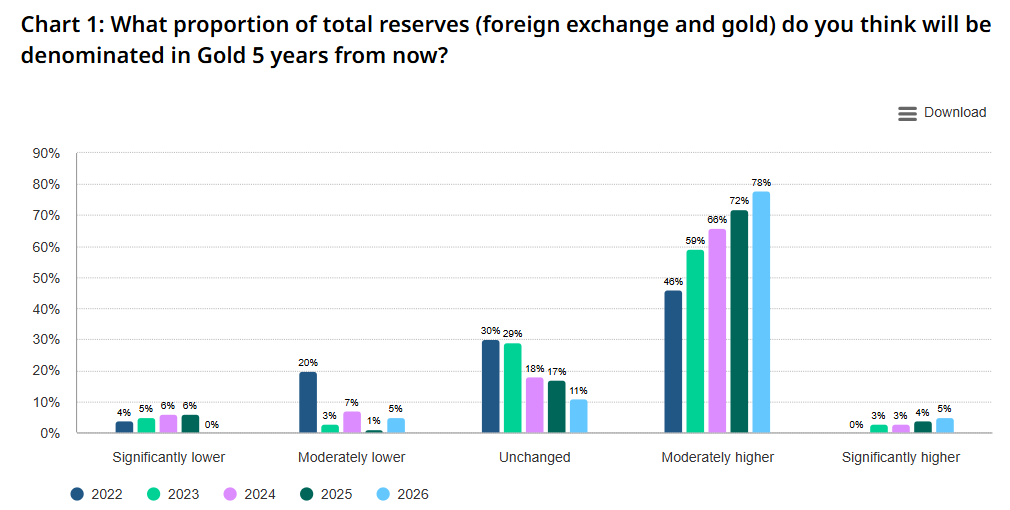

74% of the surveyed central banks predict that the proportion of the US dollar in global foreign exchange reserves will decline to varying degrees over the next five years, while the proportions of non-US dollar currencies such as the euro and the renminbi will remain basically flat, and only the proportion of gold holdings will continue to rise.

This trend has become a consensus among developed economies and EMDE central banks, confirming the gradual adjustment of the global reserve currency system.

(The central bank's forecast for the proportion of gold in its central bank reserves over the next 5 years. Source: World Gold Council)

Looking at long-term expectations, 84% of the surveyed institutions believe that the proportion of gold in total reserves will rise moderately or significantly in five years, a further increase from 76% last year.

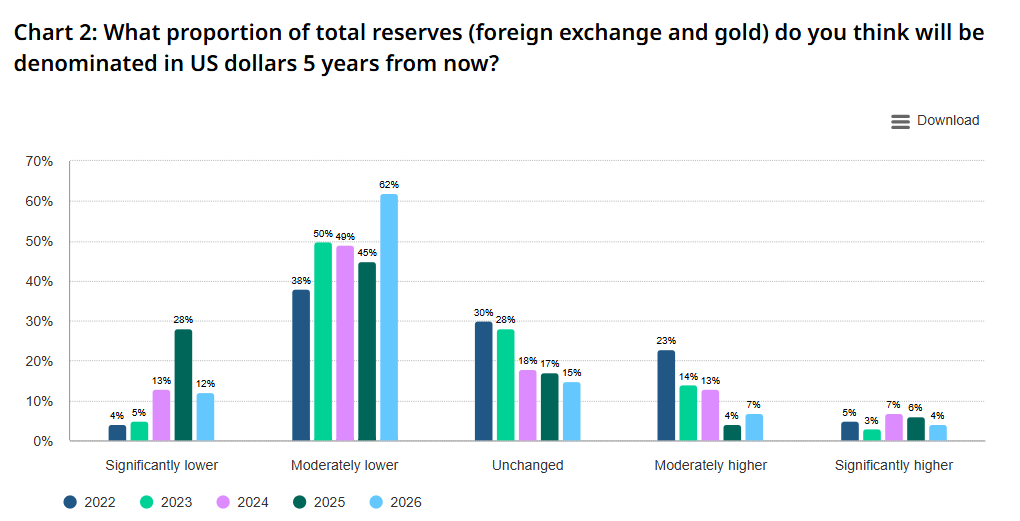

Although the US dollar still holds the dominant reserve currency position, data from the International Monetary Fund shows that its share has entered a long-term, slow downward trend. Meanwhile, gold's status as a "non-credit asset" is making it a core choice for central banks to hedge against risks in the monetary system.

(The central bank's forecast for the proportion of US dollars in central bank reserves over the next 5 years. Source: World Gold Council)

The core logic behind central banks' allocation of gold focuses on three key aspects: 90% of the surveyed institutions recognize gold's value hedging performance during crisis cycles (a nine-year high in the survey), 84% value its long-term value storage capabilities, and 83% acknowledge its portfolio diversification effect.

(Key factors that central banks around the world believe influence gold allocation. Source: World Gold Council)

It is worth noting that you can find the mainstream logic for allocating gold in the above chart, and more than half of the reasons are based on the central bank's view that the correlation is more than 50%.

Geopolitical risk hedging has become a new core driver, with 85% of EMDE central banks listing it as a key consideration, far higher than the 56% of developed economy central banks, reflecting the differences in risks faced by different economies. The figure is not shown here.

In practice, London qualified delivery gold bars remain the preferred choice, with 62% of surveyed institutions listing them as their priority purchase target and 93% of institutions holding gold based on this standard.

In terms of funding sources, half of the central banks conduct regular domestic gold purchases using local currency, while 38% choose to reduce their existing asset holdings to purchase gold.

Storage strategies are showing a trend of "decentralization": the Bank of England's vaults remain the preferred choice with a 57% share, but 49% of institutions choose domestic storage, 9% of institutions have expanded their domestic storage scale in the past 12 months, and 10% have completed a multi-location overseas distribution (a significant increase from 2% last year). More central banks plan to follow this adjustment in the future.

In addition, 37% of central banks have begun to actively manage their gold reserves, with the core objectives shifting from "profiting from short-term trading" to "increasing returns" (85%) and "hedging tail risks" (42%). The latter has nearly doubled compared to last year, reflecting the trend of central banks to operate their gold assets in a more refined manner.

The 2026 survey data clearly shows that global central banks have a very diverse and professional understanding of gold.

Against the backdrop of multiple risks such as geopolitical conflicts, inflationary pressures, and interest rate fluctuations, gold's high security, ample liquidity, and stable value preservation and appreciation attributes perfectly align with the core objectives of central bank reserve management.

We also found other restrictions on central bank gold purchases, such as comparing holding levels with historical levels. This means that when gold prices rise, the relative proportion of gold in the central bank's overall reserves increases, causing the central bank to slow down its gold purchases. This results in gold fluctuating around a central value and around the central bank's holdings. When holdings are low, the central bank buys some, and when holdings are high, the central bank sells some. Currently, if oil sales in the Gulf countries improve, they may buy back the gold they recently sold to replenish their banks' currency reserves.

(Spot gold daily chart, source: FX678)

At 19:57 Beijing time, spot gold was trading at $4,338 per ounce.

It is worth noting that the vast majority of the feedback came after the outbreak of the Middle East conflict, truly reflecting the central bank's asset allocation strategy under the escalation of geopolitical risks.

Research shows that central banks' optimistic expectations for gold continue to strengthen: 89% of the surveyed institutions predict that global official gold reserves will continue to rise over the next 12 months.

(Central banks' expectations regarding whether they will increase or decrease their gold holdings in the future. Source: World Gold Council)

The data comparison above reveals a correlation between gold price performance and the bullish sentiment of central banks. For instance, in 2022, only slightly over 50% of central banks were bullish, and gold prices did consolidate for a year. Later, as gold prices continued to rise, central banks remained bullish on gold. In 2026, while central banks were generally bullish on gold, the number of central banks bullish on it was declining compared to 2025. This is noteworthy, as it may indicate that some central banks believe they need to reduce their gold holdings, such as central banks in the Middle East that need to convert to US dollars for emergencies.

45% of institutions plan to increase their own reserves during the same period, a record high.

(Central banks' expectations for whether institutions will increase or decrease their gold holdings in the future. Source: World Gold Council)

Changes in reserve structure: Dollar share declines, gold weight increases

Asset diversification has become a core keyword in central bank reserve management.

74% of the surveyed central banks predict that the proportion of the US dollar in global foreign exchange reserves will decline to varying degrees over the next five years, while the proportions of non-US dollar currencies such as the euro and the renminbi will remain basically flat, and only the proportion of gold holdings will continue to rise.

This trend has become a consensus among developed economies and EMDE central banks, confirming the gradual adjustment of the global reserve currency system.

(The central bank's forecast for the proportion of gold in its central bank reserves over the next 5 years. Source: World Gold Council)

Looking at long-term expectations, 84% of the surveyed institutions believe that the proportion of gold in total reserves will rise moderately or significantly in five years, a further increase from 76% last year.

Although the US dollar still holds the dominant reserve currency position, data from the International Monetary Fund shows that its share has entered a long-term, slow downward trend. Meanwhile, gold's status as a "non-credit asset" is making it a core choice for central banks to hedge against risks in the monetary system.

(The central bank's forecast for the proportion of US dollars in central bank reserves over the next 5 years. Source: World Gold Council)

Configuration Logic and Practical Strategies: Security, Diversification, Hedging

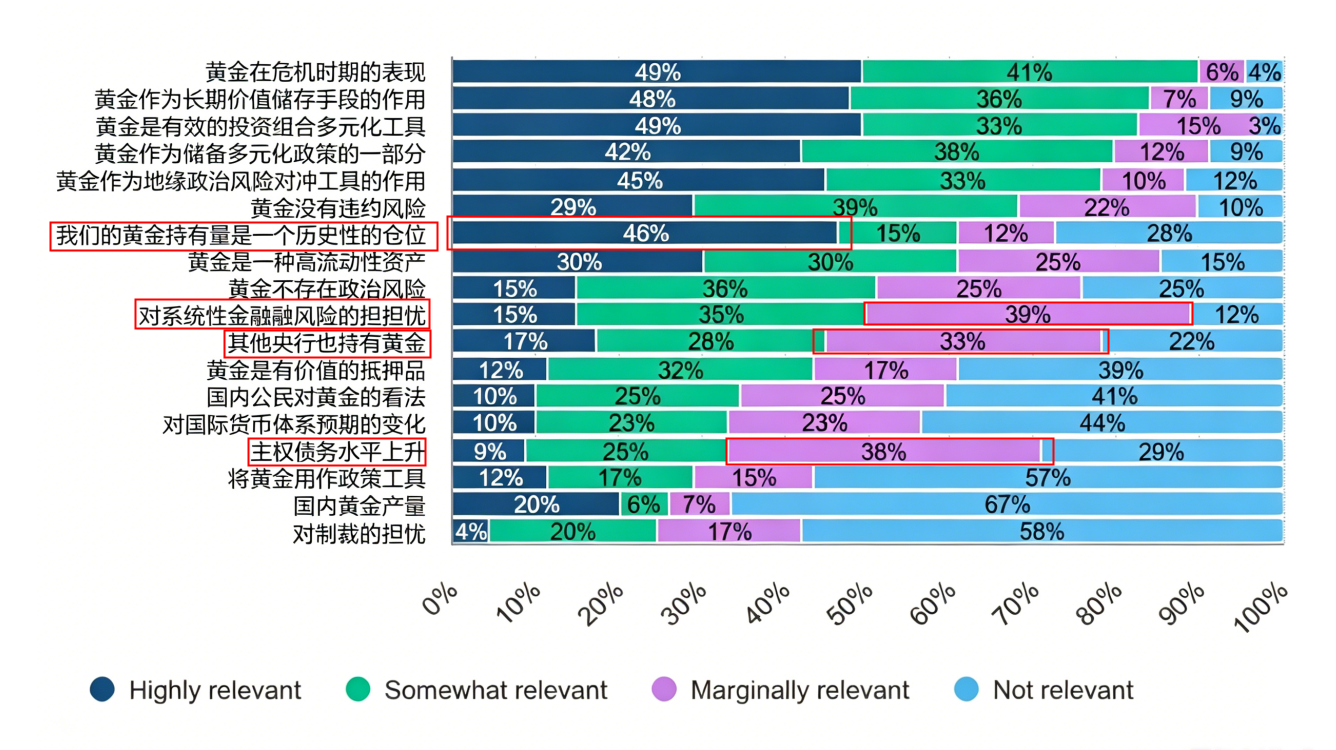

The core logic behind central banks' allocation of gold focuses on three key aspects: 90% of the surveyed institutions recognize gold's value hedging performance during crisis cycles (a nine-year high in the survey), 84% value its long-term value storage capabilities, and 83% acknowledge its portfolio diversification effect.

(Key factors that central banks around the world believe influence gold allocation. Source: World Gold Council)

It is worth noting that you can find the mainstream logic for allocating gold in the above chart, and more than half of the reasons are based on the central bank's view that the correlation is more than 50%.

Geopolitical risk hedging has become a new core driver, with 85% of EMDE central banks listing it as a key consideration, far higher than the 56% of developed economy central banks, reflecting the differences in risks faced by different economies. The figure is not shown here.

In practice, London qualified delivery gold bars remain the preferred choice, with 62% of surveyed institutions listing them as their priority purchase target and 93% of institutions holding gold based on this standard.

In terms of funding sources, half of the central banks conduct regular domestic gold purchases using local currency, while 38% choose to reduce their existing asset holdings to purchase gold.

Storage strategies are showing a trend of "decentralization": the Bank of England's vaults remain the preferred choice with a 57% share, but 49% of institutions choose domestic storage, 9% of institutions have expanded their domestic storage scale in the past 12 months, and 10% have completed a multi-location overseas distribution (a significant increase from 2% last year). More central banks plan to follow this adjustment in the future.

In addition, 37% of central banks have begun to actively manage their gold reserves, with the core objectives shifting from "profiting from short-term trading" to "increasing returns" (85%) and "hedging tail risks" (42%). The latter has nearly doubled compared to last year, reflecting the trend of central banks to operate their gold assets in a more refined manner.

Conclusion: Gold's strategic value is being upgraded again.

The 2026 survey data clearly shows that global central banks have a very diverse and professional understanding of gold.

Against the backdrop of multiple risks such as geopolitical conflicts, inflationary pressures, and interest rate fluctuations, gold's high security, ample liquidity, and stable value preservation and appreciation attributes perfectly align with the core objectives of central bank reserve management.

We also found other restrictions on central bank gold purchases, such as comparing holding levels with historical levels. This means that when gold prices rise, the relative proportion of gold in the central bank's overall reserves increases, causing the central bank to slow down its gold purchases. This results in gold fluctuating around a central value and around the central bank's holdings. When holdings are low, the central bank buys some, and when holdings are high, the central bank sells some. Currently, if oil sales in the Gulf countries improve, they may buy back the gold they recently sold to replenish their banks' currency reserves.

(Spot gold daily chart, source: FX678)

At 19:57 Beijing time, spot gold was trading at $4,338 per ounce.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.