The unwavering stance of the lone dove: Wall Street's contrarian indicator, Hollenhorst, insists on three rate cuts this year.

2026-06-17 02:56:36

Amidst uncertainty surrounding the Federal Reserve's policy outlook, Citigroup's chief U.S. economist, Andrew Hollenhorst, maintains an isolated prediction: the Fed will cut interest rates three times by 2026. This stance contrasts sharply with the mainstream hawkish view on Wall Street, but the underlying logic is sound, and his past record of predictions is enough to prompt market reflection.

Event Recap: From Data Release to Public Defend

On June 5th, the U.S. Department of Labor released its May non-farm payroll data, showing an increase of 172,000 jobs, far exceeding market expectations of 85,000, while the unemployment rate remained at 4.3%. This unexpectedly strong employment data instantly ignited market concerns about inflation and interest rate hikes. Wall Street giants such as Goldman Sachs and JPMorgan Chase quickly adjusted their forecasts, incorporating interest rate hike scenarios or significantly delaying expectations of interest rate cuts.

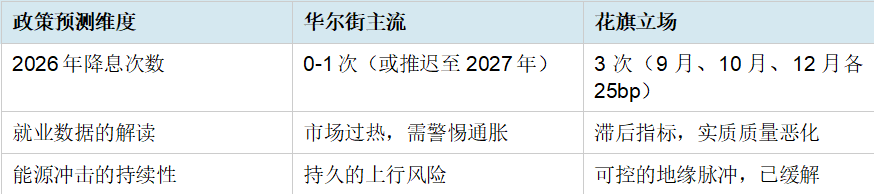

On the same day, Citigroup withstood market pressure and released an emergency report maintaining its forecast of three rate cuts this year: 25 basis points each in September, October, and December. In this report, Hollenhorst explicitly pointed out that strong employment data masked the inherent fragility of the economy.

On June 15-16, amidst widespread market panic over interest rate hikes and skepticism from peers, Hollenhorst gave a series of interviews to multiple media outlets (including Bloomberg), once again publicly and forcefully defending Citigroup's views. He emphasized that strong short-term data cannot mask the underlying cracks in the economy, and that the Fed's policy path will not be swayed by a single report.

Going against the trend: Three supporting arguments

1. The false energy alert has been lifted.

Recent tensions in the Middle East briefly pushed up oil prices, with markets worried that energy costs would drive up core PCE inflation and anchor it above 3% for an extended period. This was also a significant catalyst for several major banks turning hawkish. However, Hollenhorst's latest assessment is that oil prices have clearly retreated from their highs, with Brent crude falling below $80 per barrel this week for the first time in over three months. With the US and Iran reaching an agreement on the Strait of Hormuz and a ceasefire, supply pressures have eased significantly. The decline in oil prices is shifting inflationary pressures from upside risks to downside risks, opening up room for the Federal Reserve to ease monetary policy rather than forcing it to tighten. Citigroup's assessment is that this is not a sustained inflationary shock, but rather a manageable geopolitical pulse.

2. The labor market is clearly bloated.

The strong May non-farm payroll data led many institutions to believe the labor market was overheated, and that the Federal Reserve needed to be wary of renewed inflation and even consider raising interest rates. Hollenhorst strongly refuted this, arguing that non-farm payrolls are a lagging indicator, and actual hiring intentions have clearly cooled, with wage growth slowing. The key issue is that many companies are coping with cost pressures by reducing working hours and benefits rather than directly laying off employees, resulting in a seemingly strong employment figure, but with a deterioration in the quality of actual employment. He predicts that the true weakness of the labor market will be fully exposed within the next three months, at which point the Fed's focus will quickly shift from preventing inflation to stabilizing employment.

3. High interest rates have reached a restrictive threshold.

The Federal Reserve's current policy rate is at a high level of 3.50%-3.75%, a level that Citigroup believes is sufficiently restrictive. Raising rates due to short-term fluctuations would constitute a disastrous over-tightening of policy. In his latest defense, Hollenhorst reiterated that the threshold for raising rates is extremely high, almost outside the Fed's baseline scenario. Current high interest rates are already a significant drag on the economy, and the risks of further tightening far outweigh the risks of premature easing.

Citigroup's clear interest rate cut path

Citigroup maintains a clear timeline:

Note: Citi expects this rate-cutting cycle to continue until early 2027.

From Indicator to Prophet: Hollenhorst's Predictive Record

It's worth noting that Andrew Hollenhorst has a reputation as a contrarian on Wall Street. Over the past three years, when his predictions have contradicted the market consensus, the market has often moved in the opposite direction in the short term, making his predictions seem outlandish. This is why his prediction of three rate cuts was met with widespread skepticism as soon as it was released. However, what is more noteworthy is the long-term accuracy of his predictions.

Back in 2023, when the market widely expected the Federal Reserve to maintain high interest rates in 2024, Hollenhorst began warning of an impending rate-cutting cycle. While his timing initially proved premature—rate cuts did indeed begin in September 2024 rather than earlier—his judgment on the trend's direction was fully validated. More importantly, as the rate-cutting cycle progressed in 2024, his predictions regarding the size and frequency of each cut were relatively accurate. This demonstrates that while he is often countered by the market at precise timing points, his judgments on macroeconomic trends and medium-term direction are generally correct.

Market psychologists might explain this phenomenon: Hollenhorst's predictions often precede the formation of market consensus. In the short term, market sentiment, technical factors, and news-driven factors can cause prices to move in opposite directions. However, over a medium-term perspective of 3-6 months, fundamentals ultimately dominate pricing, and his predictions demonstrate their value.

Mainstream Wall Street vs. Citigroup Views

Conclusion: Fundamentals ultimately speak for themselves.

Amidst widespread market panic, Citigroup's defiant dovish stance stems from a firm assessment of the cyclical nature of data releases and a deep understanding of the Federal Reserve's dual mandate (employment and inflation equilibrium). Horenhorst's strong defense today further reinforces this view: short-term noise will eventually dissipate, and policy will ultimately return to fundamental logic.

When the clock strikes midnight on September for the Federal Reserve meeting, the market will ultimately decide whether Citigroup's prediction is insightful or unfounded. However, for investors familiar with Hollenhorst's forecasting track record, predictions that are initially contradicted by the market in the short term often provide accurate guidance on long-term trends. Traders are currently oscillating wildly between rate hikes and cuts, but historical data shows that fundamentals ultimately dominate pricing, and Citigroup's prediction is precisely based on a sober analysis of these fundamentals.

Event Recap: From Data Release to Public Defend

On June 5th, the U.S. Department of Labor released its May non-farm payroll data, showing an increase of 172,000 jobs, far exceeding market expectations of 85,000, while the unemployment rate remained at 4.3%. This unexpectedly strong employment data instantly ignited market concerns about inflation and interest rate hikes. Wall Street giants such as Goldman Sachs and JPMorgan Chase quickly adjusted their forecasts, incorporating interest rate hike scenarios or significantly delaying expectations of interest rate cuts.

On the same day, Citigroup withstood market pressure and released an emergency report maintaining its forecast of three rate cuts this year: 25 basis points each in September, October, and December. In this report, Hollenhorst explicitly pointed out that strong employment data masked the inherent fragility of the economy.

On June 15-16, amidst widespread market panic over interest rate hikes and skepticism from peers, Hollenhorst gave a series of interviews to multiple media outlets (including Bloomberg), once again publicly and forcefully defending Citigroup's views. He emphasized that strong short-term data cannot mask the underlying cracks in the economy, and that the Fed's policy path will not be swayed by a single report.

Going against the trend: Three supporting arguments

1. The false energy alert has been lifted.

Recent tensions in the Middle East briefly pushed up oil prices, with markets worried that energy costs would drive up core PCE inflation and anchor it above 3% for an extended period. This was also a significant catalyst for several major banks turning hawkish. However, Hollenhorst's latest assessment is that oil prices have clearly retreated from their highs, with Brent crude falling below $80 per barrel this week for the first time in over three months. With the US and Iran reaching an agreement on the Strait of Hormuz and a ceasefire, supply pressures have eased significantly. The decline in oil prices is shifting inflationary pressures from upside risks to downside risks, opening up room for the Federal Reserve to ease monetary policy rather than forcing it to tighten. Citigroup's assessment is that this is not a sustained inflationary shock, but rather a manageable geopolitical pulse.

2. The labor market is clearly bloated.

The strong May non-farm payroll data led many institutions to believe the labor market was overheated, and that the Federal Reserve needed to be wary of renewed inflation and even consider raising interest rates. Hollenhorst strongly refuted this, arguing that non-farm payrolls are a lagging indicator, and actual hiring intentions have clearly cooled, with wage growth slowing. The key issue is that many companies are coping with cost pressures by reducing working hours and benefits rather than directly laying off employees, resulting in a seemingly strong employment figure, but with a deterioration in the quality of actual employment. He predicts that the true weakness of the labor market will be fully exposed within the next three months, at which point the Fed's focus will quickly shift from preventing inflation to stabilizing employment.

3. High interest rates have reached a restrictive threshold.

The Federal Reserve's current policy rate is at a high level of 3.50%-3.75%, a level that Citigroup believes is sufficiently restrictive. Raising rates due to short-term fluctuations would constitute a disastrous over-tightening of policy. In his latest defense, Hollenhorst reiterated that the threshold for raising rates is extremely high, almost outside the Fed's baseline scenario. Current high interest rates are already a significant drag on the economy, and the risks of further tightening far outweigh the risks of premature easing.

Citigroup's clear interest rate cut path

Citigroup maintains a clear timeline:

Note: Citi expects this rate-cutting cycle to continue until early 2027.

From Indicator to Prophet: Hollenhorst's Predictive Record

It's worth noting that Andrew Hollenhorst has a reputation as a contrarian on Wall Street. Over the past three years, when his predictions have contradicted the market consensus, the market has often moved in the opposite direction in the short term, making his predictions seem outlandish. This is why his prediction of three rate cuts was met with widespread skepticism as soon as it was released. However, what is more noteworthy is the long-term accuracy of his predictions.

Back in 2023, when the market widely expected the Federal Reserve to maintain high interest rates in 2024, Hollenhorst began warning of an impending rate-cutting cycle. While his timing initially proved premature—rate cuts did indeed begin in September 2024 rather than earlier—his judgment on the trend's direction was fully validated. More importantly, as the rate-cutting cycle progressed in 2024, his predictions regarding the size and frequency of each cut were relatively accurate. This demonstrates that while he is often countered by the market at precise timing points, his judgments on macroeconomic trends and medium-term direction are generally correct.

Market psychologists might explain this phenomenon: Hollenhorst's predictions often precede the formation of market consensus. In the short term, market sentiment, technical factors, and news-driven factors can cause prices to move in opposite directions. However, over a medium-term perspective of 3-6 months, fundamentals ultimately dominate pricing, and his predictions demonstrate their value.

Mainstream Wall Street vs. Citigroup Views

Conclusion: Fundamentals ultimately speak for themselves.

Amidst widespread market panic, Citigroup's defiant dovish stance stems from a firm assessment of the cyclical nature of data releases and a deep understanding of the Federal Reserve's dual mandate (employment and inflation equilibrium). Horenhorst's strong defense today further reinforces this view: short-term noise will eventually dissipate, and policy will ultimately return to fundamental logic.

When the clock strikes midnight on September for the Federal Reserve meeting, the market will ultimately decide whether Citigroup's prediction is insightful or unfounded. However, for investors familiar with Hollenhorst's forecasting track record, predictions that are initially contradicted by the market in the short term often provide accurate guidance on long-term trends. Traders are currently oscillating wildly between rate hikes and cuts, but historical data shows that fundamentals ultimately dominate pricing, and Citigroup's prediction is precisely based on a sober analysis of these fundamentals.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.