One chart: The Baltic Dry Index weakened, dragging down the overall market with large bulk carrier freight rates.

2026-06-16 23:26:44

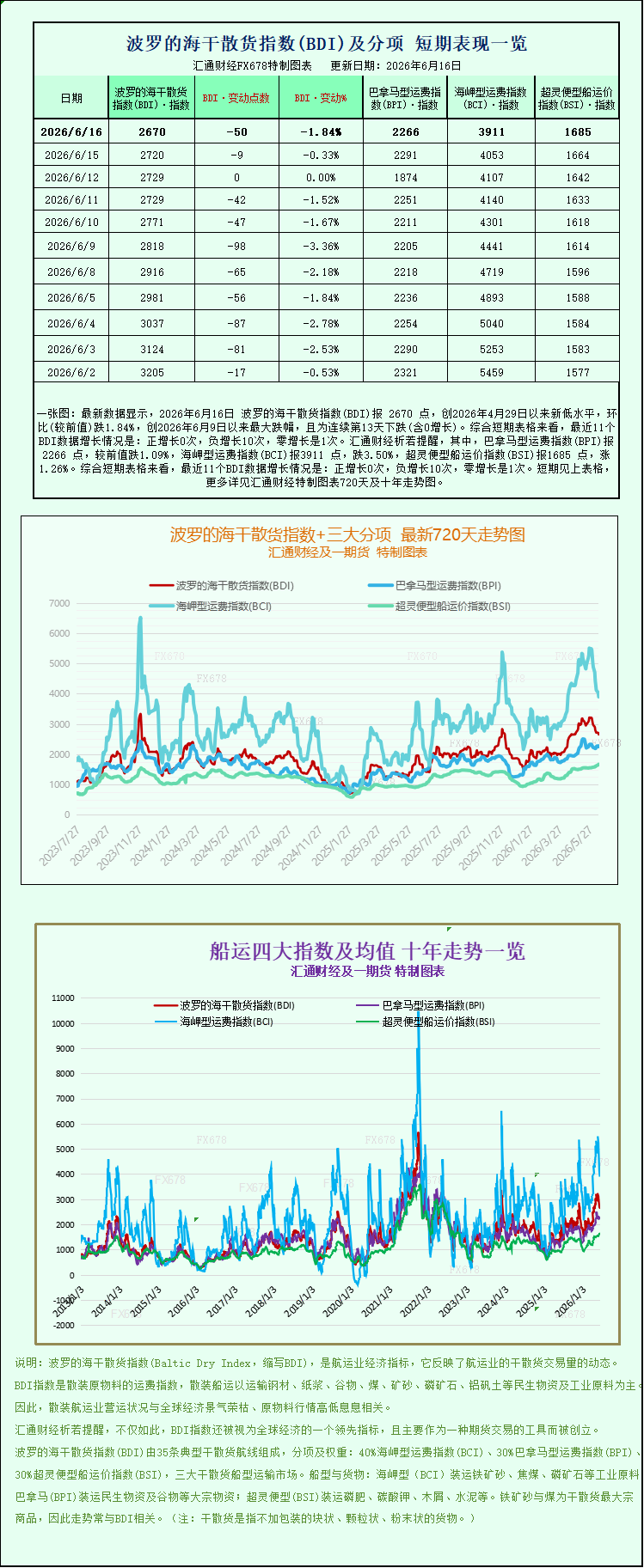

Latest data shows that the Baltic Dry Index (BDI) closed at 2670 points on June 16, 2026, a new low since April 29, 2026, down 1.84% month-on-month, the largest drop since June 9, 2026, and marking the 13th consecutive day of decline (including zero growth). Looking at the short-term charts, the recent 11 BDI data points show: 0 positive growths, 10 negative growths, and 1 zero growth. Specifically, the Panamax Freight Index (BPI) closed at 2266 points, down 1.09% from the previous value; the Capesize Freight Index (BCI) closed at 3911 points, down 3.50%; and the Supramax Freight Index (BSI) closed at 1685 points, up 1.26%. For detailed 720-day and 10-year trend charts of the Baltic Dry Index and its three main sub-indices, please refer to the specially designed charts.

The Baltic Dry Index (BDI), a key indicator of international shipping trends, recorded a significant decline on Tuesday, reflecting a cooling of overall market sentiment. The main drag came from the simultaneous weakening of freight rates for the two major bulk carrier types, Capesize and Panamax. Only small and medium-sized Supramax vessels bucked the trend with slight increases, resulting in a clear divergence in the market: "large vessels weaken, small vessels hold firm." As a core indicator tracking global shipping costs for dry bulk commodities, BDI fluctuations directly reflect the cross-border trade activity of basic industrial raw materials such as iron ore, coal, and grain, as well as agricultural products. This decline in the index also reflects a temporary slowdown in global demand for industrial raw material transportation.

On the data front, the benchmark index, which comprehensively reflects the time charter rates of the three major types of bulk carriers, fell 50 points, a drop of 1.8%, closing at 2670 points. Looking back at the market trend in early June, the BDI had already experienced a multi-day correction. Previously, from the first quarter to May, the market had seen sustained increases driven by iron ore shipments and global grain trade. This decline is a phase of adjustment after the previous surge, with the supply-demand mismatch of specific ship types being the core driver of the index's decline. In terms of index weighting, Capesize vessels account for approximately 40% of the BDI calculation, while Panamax and Supramax vessels each account for 30%. The simultaneous weakness of these two large vessel types directly dragged down the overall market performance.

Capesize freight rates plummeted, creating a negative feedback loop as demand weakened across the steel supply chain.

On that day, the Capesize freight rate index plummeted by 142 points, a 3.5% drop, closing at 3911 points. The average daily charter revenue for a 150,000-ton Capesize standard vessel decreased by $1285, falling back to $31968. Capesize vessels are the absolute mainstay of ocean-going iron ore, thermal coal, and coking coal transportation, carrying over 70% of global iron ore seaborne volume. Their freight rate trends are deeply tied to the demand from China's steel industry.

The underlying logic behind the recent plunge in Capesize freight rates stems from the chain reaction caused by persistently weak domestic steel demand. On Tuesday, two key domestic data points—new home sales and crude steel production—both fell short of market expectations, directly triggering a simultaneous weakening of iron ore futures prices and putting pressure on the entire ferrous metals industry chain. Real estate is the largest downstream consumer of steel. Since 2026, national commercial housing sales have been on a downward trend, with residential sales area declining by 12.2% year-on-year from January to April. The unsold area of commercial housing remains at a historically high level, and real estate companies' willingness to acquire land and start new construction remains weak, leading to a significant contraction in demand for construction steel, according to the National Bureau of Statistics. Coupled with continuous rainfall and high temperatures in many parts of southern China in June, outdoor infrastructure and housing construction slowed down, and the traditional off-season for the steel industry appeared early. Faced with continuously squeezed weak end-user profits, steel mills adopted extremely conservative procurement strategies, generally purchasing only as needed, actively reducing iron ore raw material inventories, and significantly decreasing orders for imported iron ore from overseas.

The contraction in demand directly impacted maritime trade flows: the volume of shipments of major iron ore from Australia and Brazil to China decreased significantly, the number of vessels waiting to unload at port anchorages declined, and the size of the Capesize fleet returning to port continued to expand. This relative oversupply of capacity further suppressed shipowners' bargaining power, ultimately resulting in a sharp decline in average daily charter rates. Meanwhile, although the net capacity growth rate of the Capesize fleet in 2026 is only 2.2%, lower than the industry average, the precipitous weakening of short-term demand completely offset the supporting logic on the supply side, making it difficult to quickly reverse the downward pressure on freight rates in the short term.

Panamax vessels weakened in tandem, and growth in coal and grain trade was insufficient.

The Panamax index also fell 25 points, or 1.1%, to close at 2266 points; the average daily earnings for standard 60,000-70,000 tonne Panamax vessels decreased by $224 to $20,393. This vessel type mainly transports transoceanic thermal coal, grains, and fertilizers, with routes covering coal trade in the Asia-Pacific region and Europe and the Americas, as well as grain export routes to North and South America. The decline in freight rates reflects a lack of incremental demand for seaborne coal and agricultural products.

In the coal sector, the EU's coal import subsidies were gradually phased out in the first half of the year, European power plant inventories remained high, and new purchase orders decreased. While India maintained imports to meet its basic needs, its purchase prices remained low, leading to a contraction in demand for long-term ocean-going contracts. Regarding grains, the new season's grains in the Northern Hemisphere have not yet entered their peak shipping period, and the shipping season for South American soybeans and corn is nearing its end. Global grain seaborne shipments are entering a seasonal lull in the short term, and these two factors are suppressing the number of Panamax vessels. Coupled with the steady recovery in new Panamax vessel deliveries in recent years and continued ample shipping capacity, freight rates naturally face downward pressure during the off-season.

Structural differentiation in the market is becoming more pronounced, with Supramax vessels bucking the trend and rising to offset the overall market decline.

In stark contrast to the weakness in the two major ship types, the index for small and medium-sized Supramax vessels bucked the trend, rising 21 points, or 1.3%, to close at 1685 points, becoming the only sector to rise in the entire market. Supramax vessels have a deadweight tonnage of 30,000-50,000 tons, shallow draft, and are suitable for small and medium-sized feeder ports. They mainly carry small batches of bauxite, minor grains, cement clinker, industrial auxiliary materials, and other bulk cargo. Their routes are mainly domestic trade and short-haul regional ocean trade, and they are less affected by the long-term trade cycles of large iron ore and coal contracts.

The core logic supporting the current strength of Supramax freight rates rests on two points: first, the trade in raw materials for manufacturing in Southeast Asia and the Middle East remains resilient, with ample cargo volume on regional short-haul routes; second, infrastructure construction and mineral development at small and medium-sized ports continue to generate demand for small-volume bulk cargo transportation, diverting some capacity and eliminating the problem of "concentrated empty runs and overcapacity" for large vessels. This divergent trend between large and small vessel types confirms that the recent decline in the Baltic Dry Index (BDI) is not due to a comprehensive global economic recession, but rather a structural market driven by temporary weakness in demand for bulk industrial raw materials, with a complete divergence in the prosperity of specific sectors.

Short-term outlook: Freight rates for large vessels may remain weak, awaiting signs of demand recovery.

According to shipping brokers and commodity institutions, Capesize and Panamax freight rates will remain under downward pressure in the short term. The adjustment cycle in the domestic real estate market is not yet over, and the off-season effect for steel in June and July will continue to intensify, making it difficult for steel mills to replenish their iron ore inventories in the short term. The peak transportation window for coal and grain will not gradually open until the end of the third quarter, and before then, both vessel types lack demand support.

In the medium to long term, the market still has expectations for recovery: on the one hand, domestic policies to stabilize the real estate market, such as urban village renovation and affordable housing, are gradually being implemented, coupled with special bonds supporting infrastructure investment, which may lead to marginal improvement in steel end-user demand in the second half of the year, potentially driving a recovery in iron ore imports; on the other hand, the gradual release of production capacity from new overseas projects such as the Simandou iron ore mine will increase the long-term shipping distance for ocean-going iron ore, benefiting the demand for Capesize vessels. Meanwhile, Supramax vessels, supported by diversified regional trade, will continue to outperform large bulk carriers in terms of freight rate resilience, and the structural differentiation in the overall market may continue into the third quarter.

Overall, the recent decline in the BDI index clearly signals a temporary cooling in global industrial commodity demand. The shipping and ferrous metals industry chains will simultaneously enter a period of weak demand. The subsequent market trend will be highly dependent on the marginal improvement in domestic real estate and steel data, as well as the pace of increase in overseas mineral and grain trade orders.

The Baltic Dry Index (BDI), a key indicator of international shipping trends, recorded a significant decline on Tuesday, reflecting a cooling of overall market sentiment. The main drag came from the simultaneous weakening of freight rates for the two major bulk carrier types, Capesize and Panamax. Only small and medium-sized Supramax vessels bucked the trend with slight increases, resulting in a clear divergence in the market: "large vessels weaken, small vessels hold firm." As a core indicator tracking global shipping costs for dry bulk commodities, BDI fluctuations directly reflect the cross-border trade activity of basic industrial raw materials such as iron ore, coal, and grain, as well as agricultural products. This decline in the index also reflects a temporary slowdown in global demand for industrial raw material transportation.

On the data front, the benchmark index, which comprehensively reflects the time charter rates of the three major types of bulk carriers, fell 50 points, a drop of 1.8%, closing at 2670 points. Looking back at the market trend in early June, the BDI had already experienced a multi-day correction. Previously, from the first quarter to May, the market had seen sustained increases driven by iron ore shipments and global grain trade. This decline is a phase of adjustment after the previous surge, with the supply-demand mismatch of specific ship types being the core driver of the index's decline. In terms of index weighting, Capesize vessels account for approximately 40% of the BDI calculation, while Panamax and Supramax vessels each account for 30%. The simultaneous weakness of these two large vessel types directly dragged down the overall market performance.

Capesize freight rates plummeted, creating a negative feedback loop as demand weakened across the steel supply chain.

On that day, the Capesize freight rate index plummeted by 142 points, a 3.5% drop, closing at 3911 points. The average daily charter revenue for a 150,000-ton Capesize standard vessel decreased by $1285, falling back to $31968. Capesize vessels are the absolute mainstay of ocean-going iron ore, thermal coal, and coking coal transportation, carrying over 70% of global iron ore seaborne volume. Their freight rate trends are deeply tied to the demand from China's steel industry.

The underlying logic behind the recent plunge in Capesize freight rates stems from the chain reaction caused by persistently weak domestic steel demand. On Tuesday, two key domestic data points—new home sales and crude steel production—both fell short of market expectations, directly triggering a simultaneous weakening of iron ore futures prices and putting pressure on the entire ferrous metals industry chain. Real estate is the largest downstream consumer of steel. Since 2026, national commercial housing sales have been on a downward trend, with residential sales area declining by 12.2% year-on-year from January to April. The unsold area of commercial housing remains at a historically high level, and real estate companies' willingness to acquire land and start new construction remains weak, leading to a significant contraction in demand for construction steel, according to the National Bureau of Statistics. Coupled with continuous rainfall and high temperatures in many parts of southern China in June, outdoor infrastructure and housing construction slowed down, and the traditional off-season for the steel industry appeared early. Faced with continuously squeezed weak end-user profits, steel mills adopted extremely conservative procurement strategies, generally purchasing only as needed, actively reducing iron ore raw material inventories, and significantly decreasing orders for imported iron ore from overseas.

The contraction in demand directly impacted maritime trade flows: the volume of shipments of major iron ore from Australia and Brazil to China decreased significantly, the number of vessels waiting to unload at port anchorages declined, and the size of the Capesize fleet returning to port continued to expand. This relative oversupply of capacity further suppressed shipowners' bargaining power, ultimately resulting in a sharp decline in average daily charter rates. Meanwhile, although the net capacity growth rate of the Capesize fleet in 2026 is only 2.2%, lower than the industry average, the precipitous weakening of short-term demand completely offset the supporting logic on the supply side, making it difficult to quickly reverse the downward pressure on freight rates in the short term.

Panamax vessels weakened in tandem, and growth in coal and grain trade was insufficient.

The Panamax index also fell 25 points, or 1.1%, to close at 2266 points; the average daily earnings for standard 60,000-70,000 tonne Panamax vessels decreased by $224 to $20,393. This vessel type mainly transports transoceanic thermal coal, grains, and fertilizers, with routes covering coal trade in the Asia-Pacific region and Europe and the Americas, as well as grain export routes to North and South America. The decline in freight rates reflects a lack of incremental demand for seaborne coal and agricultural products.

In the coal sector, the EU's coal import subsidies were gradually phased out in the first half of the year, European power plant inventories remained high, and new purchase orders decreased. While India maintained imports to meet its basic needs, its purchase prices remained low, leading to a contraction in demand for long-term ocean-going contracts. Regarding grains, the new season's grains in the Northern Hemisphere have not yet entered their peak shipping period, and the shipping season for South American soybeans and corn is nearing its end. Global grain seaborne shipments are entering a seasonal lull in the short term, and these two factors are suppressing the number of Panamax vessels. Coupled with the steady recovery in new Panamax vessel deliveries in recent years and continued ample shipping capacity, freight rates naturally face downward pressure during the off-season.

Structural differentiation in the market is becoming more pronounced, with Supramax vessels bucking the trend and rising to offset the overall market decline.

In stark contrast to the weakness in the two major ship types, the index for small and medium-sized Supramax vessels bucked the trend, rising 21 points, or 1.3%, to close at 1685 points, becoming the only sector to rise in the entire market. Supramax vessels have a deadweight tonnage of 30,000-50,000 tons, shallow draft, and are suitable for small and medium-sized feeder ports. They mainly carry small batches of bauxite, minor grains, cement clinker, industrial auxiliary materials, and other bulk cargo. Their routes are mainly domestic trade and short-haul regional ocean trade, and they are less affected by the long-term trade cycles of large iron ore and coal contracts.

The core logic supporting the current strength of Supramax freight rates rests on two points: first, the trade in raw materials for manufacturing in Southeast Asia and the Middle East remains resilient, with ample cargo volume on regional short-haul routes; second, infrastructure construction and mineral development at small and medium-sized ports continue to generate demand for small-volume bulk cargo transportation, diverting some capacity and eliminating the problem of "concentrated empty runs and overcapacity" for large vessels. This divergent trend between large and small vessel types confirms that the recent decline in the Baltic Dry Index (BDI) is not due to a comprehensive global economic recession, but rather a structural market driven by temporary weakness in demand for bulk industrial raw materials, with a complete divergence in the prosperity of specific sectors.

Short-term outlook: Freight rates for large vessels may remain weak, awaiting signs of demand recovery.

According to shipping brokers and commodity institutions, Capesize and Panamax freight rates will remain under downward pressure in the short term. The adjustment cycle in the domestic real estate market is not yet over, and the off-season effect for steel in June and July will continue to intensify, making it difficult for steel mills to replenish their iron ore inventories in the short term. The peak transportation window for coal and grain will not gradually open until the end of the third quarter, and before then, both vessel types lack demand support.

In the medium to long term, the market still has expectations for recovery: on the one hand, domestic policies to stabilize the real estate market, such as urban village renovation and affordable housing, are gradually being implemented, coupled with special bonds supporting infrastructure investment, which may lead to marginal improvement in steel end-user demand in the second half of the year, potentially driving a recovery in iron ore imports; on the other hand, the gradual release of production capacity from new overseas projects such as the Simandou iron ore mine will increase the long-term shipping distance for ocean-going iron ore, benefiting the demand for Capesize vessels. Meanwhile, Supramax vessels, supported by diversified regional trade, will continue to outperform large bulk carriers in terms of freight rate resilience, and the structural differentiation in the overall market may continue into the third quarter.

Overall, the recent decline in the BDI index clearly signals a temporary cooling in global industrial commodity demand. The shipping and ferrous metals industry chains will simultaneously enter a period of weak demand. The subsequent market trend will be highly dependent on the marginal improvement in domestic real estate and steel data, as well as the pace of increase in overseas mineral and grain trade orders.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.