Interpreting the Fed's June Interest Rate Decision: Interest Rates Remain Unchanged, Dot Plot Turns Significantly Hawkish

2026-06-18 02:39:51

On June 18, the Federal Open Market Committee (FOMC) of the Federal Reserve completed its latest monetary policy decision vote, with all members unanimously agreeing to maintain the benchmark interest rate range at 3.50%-3.75%. This marks the fourth consecutive meeting where the Fed has chosen to hold rates steady. Although no interest rates were adjusted at this meeting, the dot plot, the Summary of Economic Projections (SEP), and the newly revised policy statement released simultaneously sent a very strong hawkish signal, completely reversing the market's previous accommodative pricing logic. The interest rate futures market immediately repriced, and expectations for a rate hike in 2026 have risen sharply.

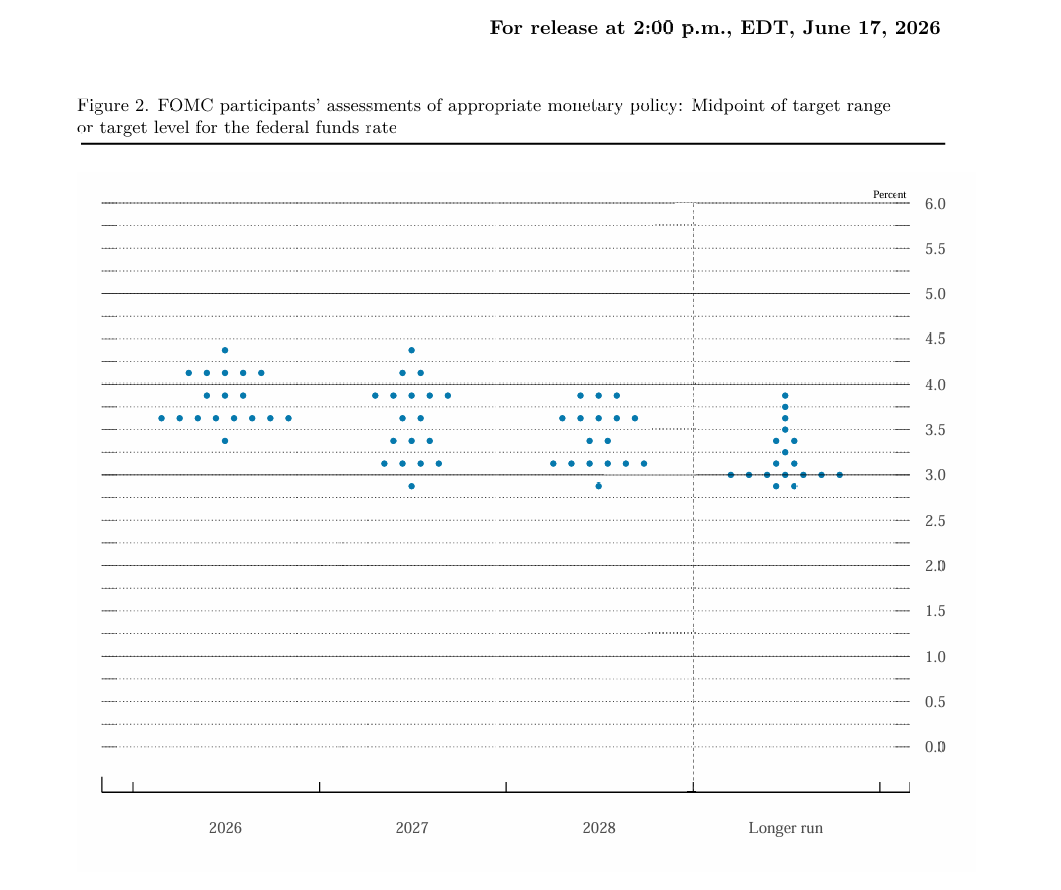

I. Dot plot shows a significant hawkish shift: half of the officials expect interest rate hikes, and the central interest rate for 2026 is expected to be revised upwards significantly.

This dot plot shows a clear policy tightening trend, with a significant widening of divergence in officials' expectations and a substantial increase in expectations for interest rate hikes. Of the 19 FOMC officials, 18 submitted complete dot plots and economic projections, while one official did not submit a complete SEP (Security Expenditures) projection; the market widely speculates that this is the new Fed Chairman, Warsh.

Looking at the latest forecast structure, 9 out of 18 officials who submitted forecasts expect the Federal Reserve to raise interest rates in 2026, accounting for half. This represents a fundamental shift from the March forecasts, with the hawkish stance exceeding market expectations. The specific path of interest rate hikes is clearly divergent:

One official projects a cumulative 75 basis point rate hike (three hikes) by 2026; five officials project a cumulative 50 basis point hike (two hikes); and three officials project a cumulative 25 basis point hike (one hike). Of the remaining officials, eight predict interest rates will remain unchanged in 2026, while only one predicts a 25 basis point rate cut. This overall distribution of expectations indicates that a prevailing view within the Federal Reserve is that "inflation risks outweigh growth risks."

With the update to the dot plot, the Federal Reserve has significantly raised its forecast for the central level of interest rates over the next few years: the median federal funds rate at the end of 2026 will be raised from 3.4% in March to 3.8%, the median rate at the end of 2027 will be 3.6%, and it will fall back to 3.4% at the end of 2028, while the median long-term equilibrium rate will remain at 3.1%. This means that US monetary policy will remain above the neutral interest rate for a long period of time over the next three years, and the duration of high interest rates will be significantly extended.

II. Market Expectations for Rapid Repricing: A 30 basis point rate hike is priced in by the end of the year, with a higher probability of a September rate hike than expected.

Following the release of the hawkish dot plot, the market quickly revised its expectations for the Fed's policy path. Current interest rate futures pricing indicates that the Fed's cumulative rate hike expectations by the end of 2026 have reached 30 basis points, an increase of 9 basis points from pre-announcement pricing, indicating a rapid rise in tightening expectations.

The short-term policy window has also changed significantly. Short-term interest rate futures data show that the probability of the Federal Reserve raising interest rates at its September meeting has exceeded the probability of keeping interest rates unchanged, and the possibility of raising interest rates this year has increased significantly.

Michelle, global head of fixed income at JPMorgan Chase, stated that the dot plot results exceeded market expectations, with half of the officials favoring rate hikes, clearly sending a signal that current interest rates have not yet reached a neutral level, and the Federal Reserve is highly likely to implement two rate hikes this year.

III. Latest Economic Forecasts: Inflation expectations have been significantly revised upwards, growth forecasts have been slightly revised downwards, and employment resilience has improved.

This SEP economic forecast presents a combination of characteristics: "significantly rising inflationary pressures, a moderate economic slowdown, and stronger employment resilience," providing data support for the Fed's hawkish shift, with significant revisions to core indicators.

On the inflation front, the median overall PCE inflation forecast for 2026 has been significantly revised upward from 2.7% in March to 3.6%, while the median core PCE inflation forecast has risen from 2.7% to 3.3%, a very substantial increase that directly reflects the Federal Reserve's repricing of inflation stickiness and the risk of inflation rebound. In their risk assessments, most officials explicitly pointed out that the current uncertainty surrounding PCE and core PCE inflation is high, and the overall risk is trending upward.

On the growth front, the Federal Reserve slightly lowered its economic growth forecast, reducing the median real GDP growth rate for 2026 from 2.4% to 2.2%, and the median GDP growth rates for 2027 and 2028 to 2.3% and 2.2% respectively. The overall economy remains in a steady expansion range and there are no signs of recession.

On the employment side, the labor market performed slightly better than previously predicted. The median unemployment rate in 2026 improved slightly from 4.4% to 4.3%. Employment growth was basically in line with labor supply, the unemployment rate remained stable, and the employment market showed sufficient resilience.

In the medium to long term, the Federal Reserve predicts that inflation will gradually decline from 2026 to 2028, but short-term inflationary pressures are much higher than previously expected, and the high inflation period will last longer.

IV. Comprehensive Restructuring of Policy Statements: Warsh Style Emerges, Major Changes to the Fed's Communication Framework

This year's Federal Reserve policy statement features the most significant revisions in recent years, with a marked reduction in overall length, the removal of all traditional forward guidance language, and a complete overhaul of the communication logic and style. It deeply reflects the policy thinking of the new Chairman, Warsh, marking a major adjustment to the Fed's communication framework.

The statement removed previously recurring phrases like "potential further adjustments to interest rates," abandoning the practice of pre-setting policy directions for the market and focusing on core missions, explicitly emphasizing that "the Committee will achieve price stability." It also added several key statements aligned with current economic fundamentals and Warsh's policy concerns: First, despite high uncertainty from external factors such as the Middle East conflict, US economic activity continues to expand at a steady pace; second, strong domestic productivity growth and capital investment echo Warsh's long-held view of the AI investment boom and technology-driven economic logic; third, job growth is in sync with labor force growth, and the overall unemployment rate remains stable; and fourth, current inflation remains high, with some inflationary pressures stemming from supply-side shocks such as those in the energy sector.

Market analysts point out that this adjustment brings the Federal Reserve's communication style back to the low-transparency, data-dependent model predating the financial crisis, weakening advance guidance while retaining policy flexibility. At the same time, the Fed broke with tradition by eliminating the release of specific voting results from committee members, further reducing market predictability.

Nick Timiraos, the “new Fed communicator,” commented: “This dot plot shows a clear hawkish bias. The policy statement has been fully revised and significantly shortened. The Fed’s overall communication framework has undergone major changes, and future policies will rely more on real-time economic data.”

V. Immediate Global Asset Reactions: US Treasuries and the US dollar strengthened, while stocks, gold, and cryptocurrencies collectively retreated.

Following the hawkish decision, global financial markets quickly repriced, with various assets experiencing sharp fluctuations and exhibiting typical contractionary trading conditions.

U.S. Treasury yields rose across the board, with the 10-year Treasury yield climbing to 4.465% and the 2-year yield climbing to 4.138%. Both long-term and short-term interest rates rose in tandem, reinforcing market expectations of a prolonged period of high interest rates.

U.S. stocks fell in the short term, with all three major indexes closing lower. The Dow Jones Industrial Average fell 0.1%, the S&P 500 fell 0.44%, and the Nasdaq Composite Index fell 0.47%-0.61%. Growth stocks were more significantly suppressed by high interest rates.

The US dollar index rose 35 basis points in the short term, rebounding strongly, while non-US currencies generally weakened. The euro fell nearly 50 points against the dollar, the pound fell more than 40 points, and the dollar rose more than 20 points against the yen.

Commodities and cryptocurrencies were under pressure in tandem, with spot gold falling by more than $50 in the short term; Bitcoin prices retreated to around $65,000; and crude oil prices saw relatively limited short-term fluctuations, remaining generally stable.

VI. Institutional Analysis and Future Policy Outlook

Luzzetti, chief U.S. economist at Deutsche Bank, said the Fed’s decision and statement sent a clear signal of interest rate hikes. To curb persistently high inflation, the Fed needs to further tighten monetary policy, and the overall tone was entirely within the hawkish range expected.

In summary, although the meeting maintained the interest rate unchanged, the fact that more than half of the officials expected a rate hike, that inflation forecasts were revised significantly upward, and that policy communication turned hawkish across the board is enough to prove that the Federal Reserve's concerns about the persistence of inflation have intensified significantly. The market's previous expectations of easing have been largely cleared out, and the logic of tightening trades has once again dominated the market.

The market is currently paying close attention to Warsh's remarks at the post-meeting press conference, as they are used to confirm the pace of interest rate hikes and policy thresholds for the year. In the medium to long term, the Fed's subsequent policies will not be fixed, and will depend on three key variables: first, the actual trend of US inflation data, which is the core basis for policy adjustments; second, the growth intensity of productivity and AI-related capital investment, which determines the resilience of economic fundamentals; and third, changes in the global geopolitical situation, which will help assess the extent to which external supply shocks will affect inflation.

I. Dot plot shows a significant hawkish shift: half of the officials expect interest rate hikes, and the central interest rate for 2026 is expected to be revised upwards significantly.

This dot plot shows a clear policy tightening trend, with a significant widening of divergence in officials' expectations and a substantial increase in expectations for interest rate hikes. Of the 19 FOMC officials, 18 submitted complete dot plots and economic projections, while one official did not submit a complete SEP (Security Expenditures) projection; the market widely speculates that this is the new Fed Chairman, Warsh.

Looking at the latest forecast structure, 9 out of 18 officials who submitted forecasts expect the Federal Reserve to raise interest rates in 2026, accounting for half. This represents a fundamental shift from the March forecasts, with the hawkish stance exceeding market expectations. The specific path of interest rate hikes is clearly divergent:

One official projects a cumulative 75 basis point rate hike (three hikes) by 2026; five officials project a cumulative 50 basis point hike (two hikes); and three officials project a cumulative 25 basis point hike (one hike). Of the remaining officials, eight predict interest rates will remain unchanged in 2026, while only one predicts a 25 basis point rate cut. This overall distribution of expectations indicates that a prevailing view within the Federal Reserve is that "inflation risks outweigh growth risks."

With the update to the dot plot, the Federal Reserve has significantly raised its forecast for the central level of interest rates over the next few years: the median federal funds rate at the end of 2026 will be raised from 3.4% in March to 3.8%, the median rate at the end of 2027 will be 3.6%, and it will fall back to 3.4% at the end of 2028, while the median long-term equilibrium rate will remain at 3.1%. This means that US monetary policy will remain above the neutral interest rate for a long period of time over the next three years, and the duration of high interest rates will be significantly extended.

II. Market Expectations for Rapid Repricing: A 30 basis point rate hike is priced in by the end of the year, with a higher probability of a September rate hike than expected.

Following the release of the hawkish dot plot, the market quickly revised its expectations for the Fed's policy path. Current interest rate futures pricing indicates that the Fed's cumulative rate hike expectations by the end of 2026 have reached 30 basis points, an increase of 9 basis points from pre-announcement pricing, indicating a rapid rise in tightening expectations.

The short-term policy window has also changed significantly. Short-term interest rate futures data show that the probability of the Federal Reserve raising interest rates at its September meeting has exceeded the probability of keeping interest rates unchanged, and the possibility of raising interest rates this year has increased significantly.

Michelle, global head of fixed income at JPMorgan Chase, stated that the dot plot results exceeded market expectations, with half of the officials favoring rate hikes, clearly sending a signal that current interest rates have not yet reached a neutral level, and the Federal Reserve is highly likely to implement two rate hikes this year.

III. Latest Economic Forecasts: Inflation expectations have been significantly revised upwards, growth forecasts have been slightly revised downwards, and employment resilience has improved.

This SEP economic forecast presents a combination of characteristics: "significantly rising inflationary pressures, a moderate economic slowdown, and stronger employment resilience," providing data support for the Fed's hawkish shift, with significant revisions to core indicators.

On the inflation front, the median overall PCE inflation forecast for 2026 has been significantly revised upward from 2.7% in March to 3.6%, while the median core PCE inflation forecast has risen from 2.7% to 3.3%, a very substantial increase that directly reflects the Federal Reserve's repricing of inflation stickiness and the risk of inflation rebound. In their risk assessments, most officials explicitly pointed out that the current uncertainty surrounding PCE and core PCE inflation is high, and the overall risk is trending upward.

On the growth front, the Federal Reserve slightly lowered its economic growth forecast, reducing the median real GDP growth rate for 2026 from 2.4% to 2.2%, and the median GDP growth rates for 2027 and 2028 to 2.3% and 2.2% respectively. The overall economy remains in a steady expansion range and there are no signs of recession.

On the employment side, the labor market performed slightly better than previously predicted. The median unemployment rate in 2026 improved slightly from 4.4% to 4.3%. Employment growth was basically in line with labor supply, the unemployment rate remained stable, and the employment market showed sufficient resilience.

In the medium to long term, the Federal Reserve predicts that inflation will gradually decline from 2026 to 2028, but short-term inflationary pressures are much higher than previously expected, and the high inflation period will last longer.

IV. Comprehensive Restructuring of Policy Statements: Warsh Style Emerges, Major Changes to the Fed's Communication Framework

This year's Federal Reserve policy statement features the most significant revisions in recent years, with a marked reduction in overall length, the removal of all traditional forward guidance language, and a complete overhaul of the communication logic and style. It deeply reflects the policy thinking of the new Chairman, Warsh, marking a major adjustment to the Fed's communication framework.

The statement removed previously recurring phrases like "potential further adjustments to interest rates," abandoning the practice of pre-setting policy directions for the market and focusing on core missions, explicitly emphasizing that "the Committee will achieve price stability." It also added several key statements aligned with current economic fundamentals and Warsh's policy concerns: First, despite high uncertainty from external factors such as the Middle East conflict, US economic activity continues to expand at a steady pace; second, strong domestic productivity growth and capital investment echo Warsh's long-held view of the AI investment boom and technology-driven economic logic; third, job growth is in sync with labor force growth, and the overall unemployment rate remains stable; and fourth, current inflation remains high, with some inflationary pressures stemming from supply-side shocks such as those in the energy sector.

Market analysts point out that this adjustment brings the Federal Reserve's communication style back to the low-transparency, data-dependent model predating the financial crisis, weakening advance guidance while retaining policy flexibility. At the same time, the Fed broke with tradition by eliminating the release of specific voting results from committee members, further reducing market predictability.

Nick Timiraos, the “new Fed communicator,” commented: “This dot plot shows a clear hawkish bias. The policy statement has been fully revised and significantly shortened. The Fed’s overall communication framework has undergone major changes, and future policies will rely more on real-time economic data.”

V. Immediate Global Asset Reactions: US Treasuries and the US dollar strengthened, while stocks, gold, and cryptocurrencies collectively retreated.

Following the hawkish decision, global financial markets quickly repriced, with various assets experiencing sharp fluctuations and exhibiting typical contractionary trading conditions.

U.S. Treasury yields rose across the board, with the 10-year Treasury yield climbing to 4.465% and the 2-year yield climbing to 4.138%. Both long-term and short-term interest rates rose in tandem, reinforcing market expectations of a prolonged period of high interest rates.

U.S. stocks fell in the short term, with all three major indexes closing lower. The Dow Jones Industrial Average fell 0.1%, the S&P 500 fell 0.44%, and the Nasdaq Composite Index fell 0.47%-0.61%. Growth stocks were more significantly suppressed by high interest rates.

The US dollar index rose 35 basis points in the short term, rebounding strongly, while non-US currencies generally weakened. The euro fell nearly 50 points against the dollar, the pound fell more than 40 points, and the dollar rose more than 20 points against the yen.

Commodities and cryptocurrencies were under pressure in tandem, with spot gold falling by more than $50 in the short term; Bitcoin prices retreated to around $65,000; and crude oil prices saw relatively limited short-term fluctuations, remaining generally stable.

VI. Institutional Analysis and Future Policy Outlook

Luzzetti, chief U.S. economist at Deutsche Bank, said the Fed’s decision and statement sent a clear signal of interest rate hikes. To curb persistently high inflation, the Fed needs to further tighten monetary policy, and the overall tone was entirely within the hawkish range expected.

In summary, although the meeting maintained the interest rate unchanged, the fact that more than half of the officials expected a rate hike, that inflation forecasts were revised significantly upward, and that policy communication turned hawkish across the board is enough to prove that the Federal Reserve's concerns about the persistence of inflation have intensified significantly. The market's previous expectations of easing have been largely cleared out, and the logic of tightening trades has once again dominated the market.

The market is currently paying close attention to Warsh's remarks at the post-meeting press conference, as they are used to confirm the pace of interest rate hikes and policy thresholds for the year. In the medium to long term, the Fed's subsequent policies will not be fixed, and will depend on three key variables: first, the actual trend of US inflation data, which is the core basis for policy adjustments; second, the growth intensity of productivity and AI-related capital investment, which determines the resilience of economic fundamentals; and third, changes in the global geopolitical situation, which will help assess the extent to which external supply shocks will affect inflation.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.