A chart shows the Baltic Dry Index (BDI) slightly declining to a near two-month low, with Capesize and Panamax bulk carrier freight rates falling.

2026-06-18 01:09:27

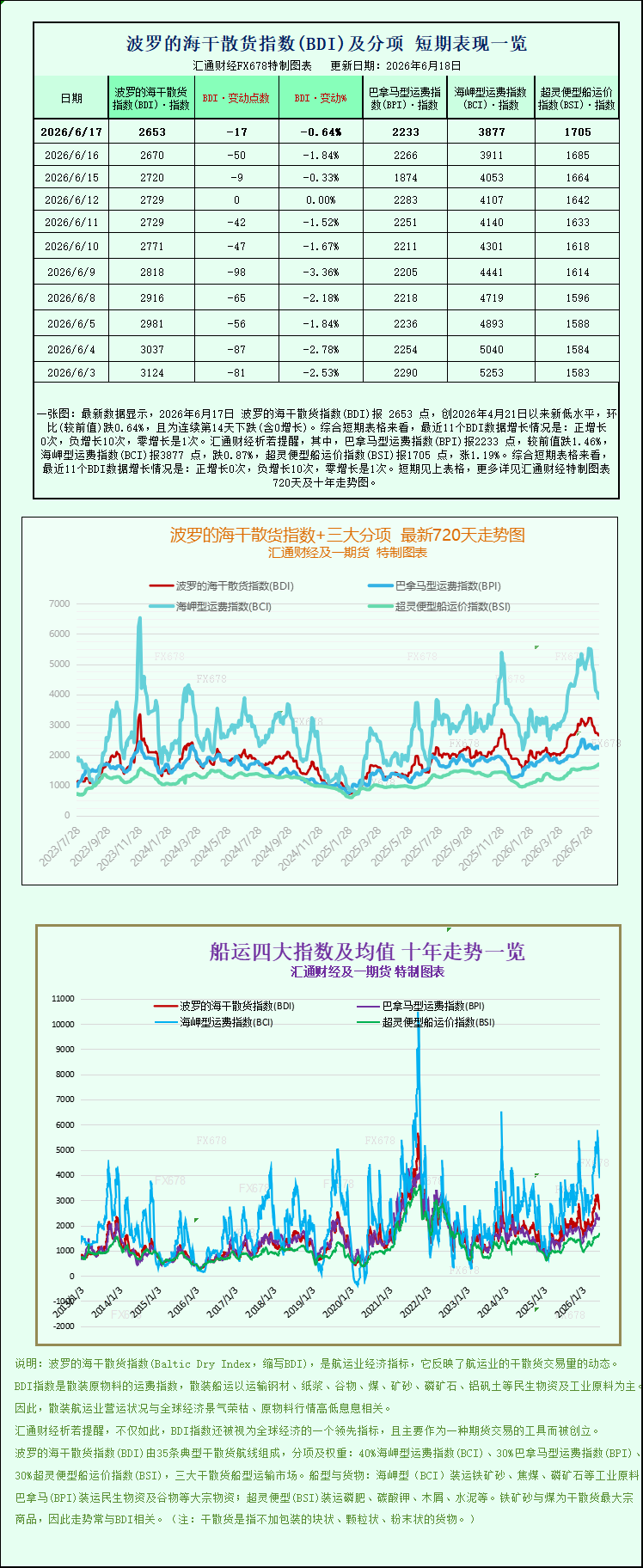

Latest data shows that the Baltic Dry Index (BDI) was at 2653 points on June 17, 2026, a new low since April 21, 2026, down 0.64% month-on-month, marking the 14th consecutive day of decline (including zero growth). Looking at the short-term charts, the recent 11 BDI data points show: 0 positive growths, 10 negative growths, and 1 zero growth. Specifically, the Panamax Freight Index (BPI) was at 2233 points, down 1.46% from the previous value; the Capesize Freight Index (BCI) was at 3877 points, down 0.87%; and the Supramax Freight Index (BSI) was at 1705 points, up 1.19%. For detailed 720-day and 10-year trend charts of the Baltic Dry Index and its three main sub-indices, please refer to the specially designed charts.

The Baltic Dry Index (BADI), which tracks global dry bulk shipping rates, continued its weak trend on Wednesday, marking its third consecutive day of decline and falling to its lowest point in nearly two months. This pullback was primarily driven by the simultaneous weakening of the Capesize and Panamax shipping segments, reflecting a continued cooling of the overall global dry bulk shipping market. As a core indicator of the global dry bulk shipping industry, the continued decline in the Baltic Dry Index directly reflects the current weak international demand for commodity shipping and the imbalance between supply and demand in the market.

Data shows that the Baltic Dry Index (BDI), which covers freight rates for the three major bulk carrier types—Capemax, Panamax, and Supramax—fell by 17 points on the day, a 0.6% overall decline, closing at 2653 points. This level marks the lowest point in nearly two months since April 21, 2026, signifying that the dry bulk shipping market has officially entered a period of adjustment after a period of stability. Looking at the pace of this decline, the index has closed lower for three consecutive trading days, indicating a sustained downward trend rather than short-term market fluctuations, fully reflecting the continued pressure on market demand.

Capesize vessels, the mainstay of large dry bulk shipping, were the primary drag on the index this round. Data shows that the Capesize vessel index fell 34 points, a 0.9% drop, closing at 3877 points, also a new low in over two months, representing the most significant decline among the three main vessel types. On the revenue side, the profitability of Capesize vessels, which primarily transport bulk industrial raw materials such as iron ore and coal, also declined. The average daily revenue of 150,000-tonnage Capesize vessels dropped sharply by $309, with the latest daily earnings at $31,659, indicating a continued contraction in the profit margins of large ocean-going dry bulk carriers.

The sluggish performance of the Capesize vessel market is primarily driven by weakening end-user demand for commodities in China. Wednesday saw significant market volatility in China, with widespread and continuous heavy rainfall affecting major steel-producing areas and riverside logistics hubs. This extreme weather not only directly hampered steel spot transportation, warehousing, and outdoor construction progress but also significantly suppressed the production intentions of downstream steel companies. As a result, domestic iron ore futures prices plummeted, leading to a rapid contraction in demand for steelmaking raw materials. This, in turn, impacted the upstream ocean shipping market, resulting in a substantial decrease in cross-border shipping orders for industrial raw materials such as international iron ore and thermal coal. Consequently, demand for large Capesize vessels declined, naturally putting downward pressure on freight rates.

Besides weakening physical demand, pessimistic market sentiment has further exacerbated the downward pressure on the shipping sector. At a recent international shipping industry conference in Singapore, numerous industry organizations, traders, and shipping company representatives participated in discussions. The conference released a clear market signal: a substantial recovery in China's bulk commodity import demand is unlikely in the short term, and the demand for raw material restocking in the steel industry chain is likely to remain sluggish. The industry recovery will be slower than previously expected. This industry consensus has completely reversed the market's previous optimism. Traders have generally postponed their long-haul bookings, and shipping companies are finding it difficult to boost order growth through price adjustments. The overall market trading atmosphere remains sluggish, providing sentiment-based support for the decline in Capesize vessel freight rates.

Panamax vessels, the main medium-sized ship type, also failed to buck the trend and continued their overall decline. Data shows that the Panamax index fell 43 points that day, a drop of 1.9%, significantly larger than that of Capesize vessels. The index closed at 2223 points, making it the sub-segment with the largest decline that day. Panamax vessels mainly transport bulk commodities such as coal, grain, and fertilizers in the 60,000 to 70,000 tonne class, while also catering to the maritime transport needs of industrial raw materials and agricultural products. The sharp drop in its index reflects the simultaneous weakening of global demand for cross-border transportation of industrial consumables and grains and oils, indicating a widespread and widespread weakness in the dry bulk market demand.

It's worth noting that the revenue performance of Panamax vessels diverged slightly from the index trend. Statistics show that the average daily revenue of Panamax vessels actually increased by $384, eventually reaching $20,009. Industry analysts attribute this divergence primarily to short-term route restructuring, with some short-haul routes experiencing slight increases in freight rates, offsetting some of the downward pressure on long-haul routes. However, overall market order volume and forward freight contracts remain in a downward trend, making the short-term revenue rebound unsustainable, and the overall weak trend in the Panamax vessel market remains unchanged.

Amidst a general market decline, the small dry bulk shipping sector demonstrated resilience, becoming the only sub-sector to rise on the day. The Supramax index rose 20 points, or 1.2%, to close at 1705 points, slightly offsetting the overall market decline. Supramax vessels have smaller deadweight tonnage and greater transport flexibility, primarily suited for the cross-border transport of niche commodities, regional goods, and small-batch industrial raw materials. They are less affected by large steel mills' raw material restocking and fluctuations in global bulk industrial demand. Meanwhile, stable regional shipping demand in Southeast Asia and the Middle East supported a slight increase in freight rates for small vessels, resulting in a structural differentiation in the dry bulk shipping market: "large vessels are weak, small vessels are resilient."

In summary, the core logic behind the current weakness in the Baltic Dry Index (BDI) lies in two main dimensions: firstly, weak demand, with China's steel industry chain affected by extreme weather and sluggish end-user consumption, leading to a continued decline in raw material import demand and suppressing orders for major vessel types; secondly, weak market expectations, with pessimistic signals from industry conferences leaving the market lacking confidence in recovery, and trade and shipping transactions becoming more cautious. Looking at the short-term industry trend, heavy rainfall in China is expected to continue, making it difficult for steel companies to quickly recover their operating rates. Demand for replenishing bulk commodities is likely to remain low, and Capesize and Panamax freight rates may continue their downward trend. Meanwhile, Supramax vessels, leveraging their regional demand advantage, are expected to maintain relative resilience, and the structural differentiation in the market may continue.

The global dry bulk shipping market is currently in a cyclical adjustment phase, and the pace of its recovery will heavily depend on the progress of domestic weather improvement, the resumption of production in the steel industry, and the strength of the recovery in global commodity trade demand. If end-user demand fails to recover as expected, the Baltic Dry Index will likely continue to fluctuate at low levels, potentially further squeezing the profit margins of shipping companies.

The Baltic Dry Index (BADI), which tracks global dry bulk shipping rates, continued its weak trend on Wednesday, marking its third consecutive day of decline and falling to its lowest point in nearly two months. This pullback was primarily driven by the simultaneous weakening of the Capesize and Panamax shipping segments, reflecting a continued cooling of the overall global dry bulk shipping market. As a core indicator of the global dry bulk shipping industry, the continued decline in the Baltic Dry Index directly reflects the current weak international demand for commodity shipping and the imbalance between supply and demand in the market.

Data shows that the Baltic Dry Index (BDI), which covers freight rates for the three major bulk carrier types—Capemax, Panamax, and Supramax—fell by 17 points on the day, a 0.6% overall decline, closing at 2653 points. This level marks the lowest point in nearly two months since April 21, 2026, signifying that the dry bulk shipping market has officially entered a period of adjustment after a period of stability. Looking at the pace of this decline, the index has closed lower for three consecutive trading days, indicating a sustained downward trend rather than short-term market fluctuations, fully reflecting the continued pressure on market demand.

Capesize vessels, the mainstay of large dry bulk shipping, were the primary drag on the index this round. Data shows that the Capesize vessel index fell 34 points, a 0.9% drop, closing at 3877 points, also a new low in over two months, representing the most significant decline among the three main vessel types. On the revenue side, the profitability of Capesize vessels, which primarily transport bulk industrial raw materials such as iron ore and coal, also declined. The average daily revenue of 150,000-tonnage Capesize vessels dropped sharply by $309, with the latest daily earnings at $31,659, indicating a continued contraction in the profit margins of large ocean-going dry bulk carriers.

The sluggish performance of the Capesize vessel market is primarily driven by weakening end-user demand for commodities in China. Wednesday saw significant market volatility in China, with widespread and continuous heavy rainfall affecting major steel-producing areas and riverside logistics hubs. This extreme weather not only directly hampered steel spot transportation, warehousing, and outdoor construction progress but also significantly suppressed the production intentions of downstream steel companies. As a result, domestic iron ore futures prices plummeted, leading to a rapid contraction in demand for steelmaking raw materials. This, in turn, impacted the upstream ocean shipping market, resulting in a substantial decrease in cross-border shipping orders for industrial raw materials such as international iron ore and thermal coal. Consequently, demand for large Capesize vessels declined, naturally putting downward pressure on freight rates.

Besides weakening physical demand, pessimistic market sentiment has further exacerbated the downward pressure on the shipping sector. At a recent international shipping industry conference in Singapore, numerous industry organizations, traders, and shipping company representatives participated in discussions. The conference released a clear market signal: a substantial recovery in China's bulk commodity import demand is unlikely in the short term, and the demand for raw material restocking in the steel industry chain is likely to remain sluggish. The industry recovery will be slower than previously expected. This industry consensus has completely reversed the market's previous optimism. Traders have generally postponed their long-haul bookings, and shipping companies are finding it difficult to boost order growth through price adjustments. The overall market trading atmosphere remains sluggish, providing sentiment-based support for the decline in Capesize vessel freight rates.

Panamax vessels, the main medium-sized ship type, also failed to buck the trend and continued their overall decline. Data shows that the Panamax index fell 43 points that day, a drop of 1.9%, significantly larger than that of Capesize vessels. The index closed at 2223 points, making it the sub-segment with the largest decline that day. Panamax vessels mainly transport bulk commodities such as coal, grain, and fertilizers in the 60,000 to 70,000 tonne class, while also catering to the maritime transport needs of industrial raw materials and agricultural products. The sharp drop in its index reflects the simultaneous weakening of global demand for cross-border transportation of industrial consumables and grains and oils, indicating a widespread and widespread weakness in the dry bulk market demand.

It's worth noting that the revenue performance of Panamax vessels diverged slightly from the index trend. Statistics show that the average daily revenue of Panamax vessels actually increased by $384, eventually reaching $20,009. Industry analysts attribute this divergence primarily to short-term route restructuring, with some short-haul routes experiencing slight increases in freight rates, offsetting some of the downward pressure on long-haul routes. However, overall market order volume and forward freight contracts remain in a downward trend, making the short-term revenue rebound unsustainable, and the overall weak trend in the Panamax vessel market remains unchanged.

Amidst a general market decline, the small dry bulk shipping sector demonstrated resilience, becoming the only sub-sector to rise on the day. The Supramax index rose 20 points, or 1.2%, to close at 1705 points, slightly offsetting the overall market decline. Supramax vessels have smaller deadweight tonnage and greater transport flexibility, primarily suited for the cross-border transport of niche commodities, regional goods, and small-batch industrial raw materials. They are less affected by large steel mills' raw material restocking and fluctuations in global bulk industrial demand. Meanwhile, stable regional shipping demand in Southeast Asia and the Middle East supported a slight increase in freight rates for small vessels, resulting in a structural differentiation in the dry bulk shipping market: "large vessels are weak, small vessels are resilient."

In summary, the core logic behind the current weakness in the Baltic Dry Index (BDI) lies in two main dimensions: firstly, weak demand, with China's steel industry chain affected by extreme weather and sluggish end-user consumption, leading to a continued decline in raw material import demand and suppressing orders for major vessel types; secondly, weak market expectations, with pessimistic signals from industry conferences leaving the market lacking confidence in recovery, and trade and shipping transactions becoming more cautious. Looking at the short-term industry trend, heavy rainfall in China is expected to continue, making it difficult for steel companies to quickly recover their operating rates. Demand for replenishing bulk commodities is likely to remain low, and Capesize and Panamax freight rates may continue their downward trend. Meanwhile, Supramax vessels, leveraging their regional demand advantage, are expected to maintain relative resilience, and the structural differentiation in the market may continue.

The global dry bulk shipping market is currently in a cyclical adjustment phase, and the pace of its recovery will heavily depend on the progress of domestic weather improvement, the resumption of production in the steel industry, and the strength of the recovery in global commodity trade demand. If end-user demand fails to recover as expected, the Baltic Dry Index will likely continue to fluctuate at low levels, potentially further squeezing the profit margins of shipping companies.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.