A chart: The Baltic Dry Index hits a one-week high due to rising Capesize bulk carrier freight rates.

2026-06-19 23:53:16

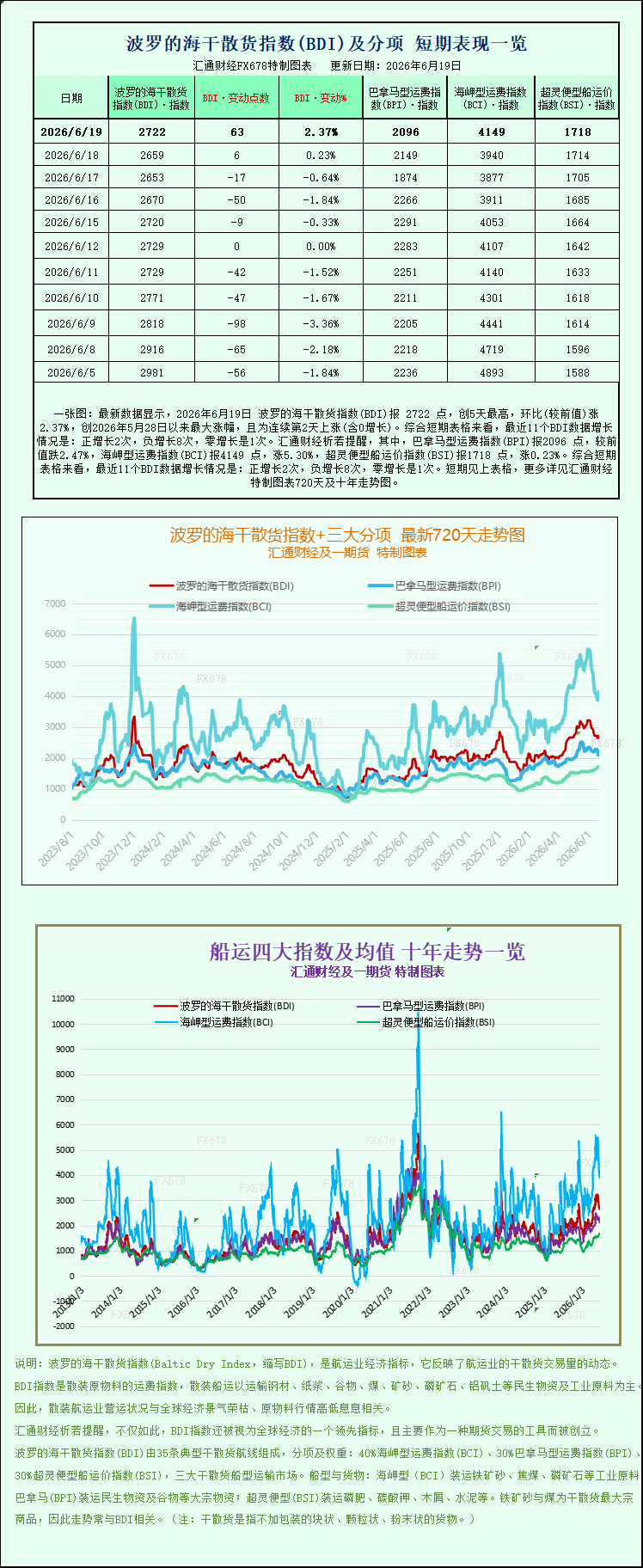

Latest data shows that the Baltic Dry Index (BDI) reached 2722 points on June 19, 2026, a five-day high, up 2.37% month-on-month (compared to the previous value), marking the largest increase since May 28, 2026, and the second consecutive day of increase (including zero growth). Looking at the short-term charts, the recent 11 BDI data points show: positive growth twice, negative growth eight times, and zero growth once. Specifically, the Panamax Freight Index (BPI) was 2096 points, down 2.47% from the previous value; the Capesize Freight Index (BCI) was 4149 points, up 5.30%; and the Supramax Freight Index (BSI) was 1718 points, up 0.23%. For detailed 720-day and 10-year trend charts of the Baltic Dry Index and its three main sub-indices, please refer to the specially designed charts.

On June 19, 2026, the latest shipping market data showed that the global dry bulk shipping market experienced structural differentiation. Driven by a significant surge in Capesize (Good Hope) bulk carrier freight rates, the Baltic Dry Index, a key indicator, rebounded strongly, reaching its highest point in nearly a week, injecting upward momentum into the previously sluggish dry bulk market. Although the performance of different vessel types was uneven, with Panamax freight rates continuing to weaken, the strong performance of Capesize vessels still drove a significant recovery in the overall index, reflecting a phased recovery in global commodity shipping demand.

As a core benchmark indicator for the global dry bulk shipping market, the Baltic Dry Index (BADI) comprehensively tracks freight rate fluctuations across the three major bulk carrier types: Capesize, Panamax, and Supramax. It serves as a key indicator of the activity in global maritime transport of industrial raw materials, food, and other bulk commodities, and is widely regarded as a leading indicator of global trade and industrial economics. This data shows that as of the close of trading on Friday, June 19th, the Baltic Dry Index surged 63 points, a single-day increase of 2.4%, ultimately closing at 2722 points, marking the highest closing level in a week since June 12th and ending the previous days of fluctuation and adjustment.

The core driver of this market rebound came from the strong surge in the Capesize bulk carrier market. This vessel type primarily transports ultra-large industrial raw materials such as iron ore and coal, and is the largest vessel type in the dry bulk market, most closely linked to industrial demand. Data shows that the Capesize Exclusive Freight Index (BACI) surged 209 points in a single day, a significant increase of 5.3%, closing at 4149 points. This not only marked the largest single-day increase in recent times but also reached a more than two-month high since April 10th. Looking at the weekly trend, the Capesize index has steadily risen by 1% this week, showing a continued upward trend and a clear upward trajectory in the market.

The impressive revenue figures further confirm the robust performance of the Capesize vessel market. Capesize bulk carriers with a standard deadweight tonnage of 150,000 tons, primarily responsible for long-distance transoceanic transport of bulk industrial raw materials such as iron ore, thermal coal, and metallurgical coal, saw their average daily revenue increase significantly by $1,900, reaching a latest average daily revenue of $34,128. This substantial increase in freight rates is primarily attributed to the phased recovery in the operating rate of the steel industry in the Asia-Pacific region, which boosted demand for iron ore imports. Simultaneously, the release of summer energy reserve replenishment demand in some European countries led to a significant increase in coal seaborne orders. Coupled with the recent tight supply of vessels on major Atlantic and Pacific routes, the available shipping slots in the spot market have contracted, and this supply-demand imbalance has directly driven up the ocean freight rates for Capesize vessels.

In stark contrast to the strong rise in Capesize vessels, the Panamax bulk carrier market continued its weakening trend, exhibiting a clear divergence. Data shows that the Panamax Freight Index (BPNI) fell 53 points, or 2.5%, to close at 2096 points, maintaining its weak momentum. On a weekly basis, the index has fallen sharply by 8.2% this week, becoming the main negative factor dragging down the overall market. Panamax vessels have a standard deadweight of 60,000 to 70,000 tons and mainly transport bulk commodities such as coal, grain, and fertilizer, catering to regional trade and grain shipping needs.

Revenue data also declined, with Panamax vessel daily revenue falling by $479 this week to a mere $18,860. Industry analysts point out that the continued decline in Panamax freight rates is mainly due to weak demand at the end of the peak season for global grain shipping. South American grain export orders are gradually wrapping up, while North American and Asia-Pacific grain exports have not yet entered their peak season, resulting in a gap in market orders. At the same time, the recent increase in new capacity deployment on regional routes has exacerbated the oversupply situation, further squeezing shipowners' profit margins and leading to a continued decline in freight rates.

The market for small and medium-sized bulk carriers remained relatively stable with minimal fluctuations, playing a role in stabilizing the overall market. The Supramax Freight Index (BSIS) rose slightly by 4 points, a mere 0.2%, closing at 1718 points. This type of vessel has a smaller deadweight tonnage and primarily handles short-haul, small-volume dry bulk cargo orders, covering transportation scenarios such as building materials, minor ores, and grain by-products. Market demand is relatively dispersed and stable, resulting in minimal fluctuations in freight rates. It has maintained stable operation during this round of market structural differentiation, without showing any significant upward or downward trends.

Looking at the overall dry bulk market, the industry is currently exhibiting significant structural differentiation, with a recovery in demand for large-scale industrial raw material transportation offsetting weak demand for small and medium-sized commercial bulk cargo. In the short term, the upward momentum for Capesize vessels is expected to continue. As the traditional peak season for the global steel industry approaches, the demand for iron ore transportation will be further released, coupled with continued global energy restocking demand, suggesting that freight rates on large dry bulk routes may remain high. The Panamax market, however, still needs to wait for the start of a new grain export cycle, and is likely to continue its weak and volatile pattern in the short term. Supramax vessels will continue to maintain a stable trend with limited overall fluctuations.

Shipping analysts believe that the Baltic Dry Index (BDI) will continue to rely on the recovery in demand for industrial raw materials. If industrial activity in the Asia-Pacific and Europe continues to pick up, Capesize freight rates are expected to rise further, driving the overall index higher. However, the uneven distribution of demand across different market segments remains a concern, and a broad-based price increase has not yet materialized. In the short term, the market will likely maintain a structural trend of "stronger large vessels and weaker medium and small vessels."

On June 19, 2026, the latest shipping market data showed that the global dry bulk shipping market experienced structural differentiation. Driven by a significant surge in Capesize (Good Hope) bulk carrier freight rates, the Baltic Dry Index, a key indicator, rebounded strongly, reaching its highest point in nearly a week, injecting upward momentum into the previously sluggish dry bulk market. Although the performance of different vessel types was uneven, with Panamax freight rates continuing to weaken, the strong performance of Capesize vessels still drove a significant recovery in the overall index, reflecting a phased recovery in global commodity shipping demand.

As a core benchmark indicator for the global dry bulk shipping market, the Baltic Dry Index (BADI) comprehensively tracks freight rate fluctuations across the three major bulk carrier types: Capesize, Panamax, and Supramax. It serves as a key indicator of the activity in global maritime transport of industrial raw materials, food, and other bulk commodities, and is widely regarded as a leading indicator of global trade and industrial economics. This data shows that as of the close of trading on Friday, June 19th, the Baltic Dry Index surged 63 points, a single-day increase of 2.4%, ultimately closing at 2722 points, marking the highest closing level in a week since June 12th and ending the previous days of fluctuation and adjustment.

The core driver of this market rebound came from the strong surge in the Capesize bulk carrier market. This vessel type primarily transports ultra-large industrial raw materials such as iron ore and coal, and is the largest vessel type in the dry bulk market, most closely linked to industrial demand. Data shows that the Capesize Exclusive Freight Index (BACI) surged 209 points in a single day, a significant increase of 5.3%, closing at 4149 points. This not only marked the largest single-day increase in recent times but also reached a more than two-month high since April 10th. Looking at the weekly trend, the Capesize index has steadily risen by 1% this week, showing a continued upward trend and a clear upward trajectory in the market.

The impressive revenue figures further confirm the robust performance of the Capesize vessel market. Capesize bulk carriers with a standard deadweight tonnage of 150,000 tons, primarily responsible for long-distance transoceanic transport of bulk industrial raw materials such as iron ore, thermal coal, and metallurgical coal, saw their average daily revenue increase significantly by $1,900, reaching a latest average daily revenue of $34,128. This substantial increase in freight rates is primarily attributed to the phased recovery in the operating rate of the steel industry in the Asia-Pacific region, which boosted demand for iron ore imports. Simultaneously, the release of summer energy reserve replenishment demand in some European countries led to a significant increase in coal seaborne orders. Coupled with the recent tight supply of vessels on major Atlantic and Pacific routes, the available shipping slots in the spot market have contracted, and this supply-demand imbalance has directly driven up the ocean freight rates for Capesize vessels.

In stark contrast to the strong rise in Capesize vessels, the Panamax bulk carrier market continued its weakening trend, exhibiting a clear divergence. Data shows that the Panamax Freight Index (BPNI) fell 53 points, or 2.5%, to close at 2096 points, maintaining its weak momentum. On a weekly basis, the index has fallen sharply by 8.2% this week, becoming the main negative factor dragging down the overall market. Panamax vessels have a standard deadweight of 60,000 to 70,000 tons and mainly transport bulk commodities such as coal, grain, and fertilizer, catering to regional trade and grain shipping needs.

Revenue data also declined, with Panamax vessel daily revenue falling by $479 this week to a mere $18,860. Industry analysts point out that the continued decline in Panamax freight rates is mainly due to weak demand at the end of the peak season for global grain shipping. South American grain export orders are gradually wrapping up, while North American and Asia-Pacific grain exports have not yet entered their peak season, resulting in a gap in market orders. At the same time, the recent increase in new capacity deployment on regional routes has exacerbated the oversupply situation, further squeezing shipowners' profit margins and leading to a continued decline in freight rates.

The market for small and medium-sized bulk carriers remained relatively stable with minimal fluctuations, playing a role in stabilizing the overall market. The Supramax Freight Index (BSIS) rose slightly by 4 points, a mere 0.2%, closing at 1718 points. This type of vessel has a smaller deadweight tonnage and primarily handles short-haul, small-volume dry bulk cargo orders, covering transportation scenarios such as building materials, minor ores, and grain by-products. Market demand is relatively dispersed and stable, resulting in minimal fluctuations in freight rates. It has maintained stable operation during this round of market structural differentiation, without showing any significant upward or downward trends.

Looking at the overall dry bulk market, the industry is currently exhibiting significant structural differentiation, with a recovery in demand for large-scale industrial raw material transportation offsetting weak demand for small and medium-sized commercial bulk cargo. In the short term, the upward momentum for Capesize vessels is expected to continue. As the traditional peak season for the global steel industry approaches, the demand for iron ore transportation will be further released, coupled with continued global energy restocking demand, suggesting that freight rates on large dry bulk routes may remain high. The Panamax market, however, still needs to wait for the start of a new grain export cycle, and is likely to continue its weak and volatile pattern in the short term. Supramax vessels will continue to maintain a stable trend with limited overall fluctuations.

Shipping analysts believe that the Baltic Dry Index (BDI) will continue to rely on the recovery in demand for industrial raw materials. If industrial activity in the Asia-Pacific and Europe continues to pick up, Capesize freight rates are expected to rise further, driving the overall index higher. However, the uneven distribution of demand across different market segments remains a concern, and a broad-based price increase has not yet materialized. In the short term, the market will likely maintain a structural trend of "stronger large vessels and weaker medium and small vessels."

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.