Hawk or dove? It's too early to judge Warsh's policy stance.

2026-06-25 01:14:06

After Kevin Warsh held his first press conference as Federal Reserve Chairman, analysts and the market reached a consensus: he is a hawk, adheres to the traditional policy framework, and is by no means a policy puppet of the president. However, this hawkish interpretation is premature and may even be completely inaccurate; everything still needs time to prove.

This was Warsh's first Federal Open Market Committee (FOMC) policy meeting. A Fed chair's policy reputation is often established upon their first appearance on the scene, and policy credibility is fundamental to their position. At the meeting, Warsh pointed out that the Fed's inflation target has been missed for five consecutive years, with the current inflation rate climbing to 4% and the labor market generally booming. Against this macroeconomic backdrop, he emphasized the core objective of price stability.

In his heart, Warsh may lean towards hawkishness and has good reason to believe that the Fed's previous forward guidance was overly protective of the market and too direct in its information delivery. Even though Donald Trump has toned down his rhetoric after this policy meeting, acknowledging that the conditions for a rate cut are not currently in place, his continued pressure on the Fed to cut rates still casts a shadow over Warsh.

This is why the policy statement did not provide any forward guidance, Warsh himself did not submit his personal interest rate projections in the dot plot, and avoided commenting on the future path of interest rates throughout, which aligns with his own practical considerations. If Trump learns that Warsh's interest rate projections do not support rate cuts, he will inevitably launch another public attack. Meanwhile, other FOMC members submitted their projections as usual, with nine members supporting rate hikes. Market discussion was completely dominated by expectations of rate hikes, and US Treasury yields rose accordingly—essentially, the financial market spontaneously absorbed the actual effect of monetary tightening.

The launch of several new assessment programs is justified.

The new chairman's proposal to review the Fed's current policy mechanisms is reasonable. Warsh's establishment of five special working groups to review the Fed's communication mechanisms, inflation policy framework, balance sheet, economic data methodology, productivity, and employment is quite significant. The inflation framework and productivity issues deserve particular attention and may become key clues for determining Warsh's true policy inclination (hawkish or dovish).

According to the plan, all assessment work must be completed within six months, compressing a large amount of research and analysis work into an extremely short period. Anyone familiar with government operations knows that the definition of the working group's research responsibilities and personnel composition are crucial in determining the final conclusions. Does the working group's research boundaries and member configuration uphold neutrality and objectivity, or does it carry a pre-existing policy bias?

Regarding the inflation policy framework, two core questions will directly influence the future direction of interest rates: What constitutes price stability? And what indicators should be used to measure inflation?

Walsh seems to agree with the 2% target for price stability, but he suggests a logical fallacy in the use of zeros after the decimal point, implying a false sense of precision. If this argument holds true, the reasonable range for price stability might be broadened to 2.49%.

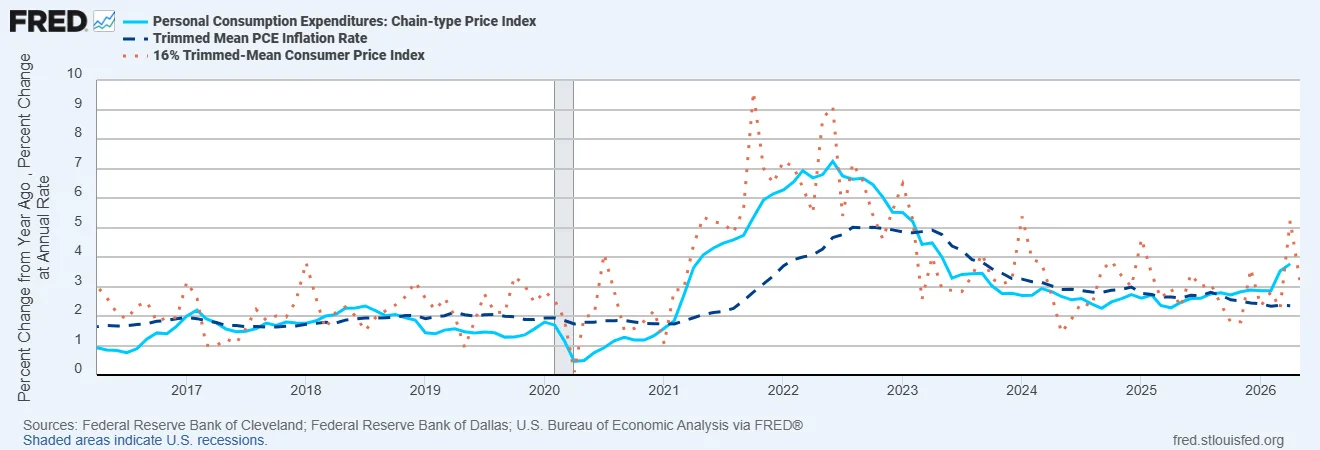

Furthermore, the debate surrounding inflation metrics has never ceased. Warsh mentioned a preference for using cut-down mean inflation metrics: the Dallas Fed's cut-down mean personal consumption expenditures (PCE) inflation is currently below 2.5%, while regular PCE inflation is approaching 4%; the Cleveland Fed's cut-down mean consumer price index (CPI) inflation has exceeded 3%.

Chart 1: What inflation measure should the Federal Reserve use?

(Data source: Federal Reserve Bank of Cleveland, Federal Reserve Bank of Dallas, Bureau of Economic Analysis, U.S. Department of Commerce)

The difference between the cut-off mean inflation and the standard PCE inflation will continue to fluctuate with the economic cycle. If the Federal Reserve were to use the cut-off mean PCE indicator at this stage, coupled with an inflation tolerance range that is actually slightly higher than 2%, achieving the price stability goal would be significantly easier.

Regardless of which inflation indicator is ultimately chosen, adjusting the inflation rules midway before PCE inflation returns to 2%, or at least clearly enters a downward trend, could severely damage the Federal Reserve's policy credibility. Meanwhile, central banks worldwide consistently face significant challenges in assessing the medium-term inflation outlook. However, if one argues that the Fed is unable to offset supply shocks and weaken the impact of the second-order transmission effect of inflation, this argument can support room for looser monetary policy.

There is a huge disagreement regarding productivity-related claims.

Drawing on the economic experience of the United States in the 1990s during the Alan Greenspan era, Warsh argues that artificial intelligence will boost overall productivity and drive economic growth without creating inflationary pressures, thus creating policy space for interest rate cuts.

This viewpoint is highly controversial in academic circles. Greenspan delayed interest rate hikes precisely because he anticipated continued productivity growth. In the short term, the boost to aggregate demand from AI-related investments and industrial expansion far outweighs supply-side capacity expansion, thus creating upward inflationary pressure. Many economists believe that productivity gains will push up the natural equilibrium interest rate; and that technological innovation's penetration into the real economy and its transmission to people's daily lives is very slow.

In short, most economists are skeptical that "the productivity revolution of artificial intelligence can change the direction of inflation and interest rates in the short term."

In summary, the staffing of the working group and its final research conclusions are crucial: the two sets of arguments—inflation measurement standards and productivity—can both deduce the feasibility of interest rate cuts and corroborate the necessity of maintaining high interest rates.

It's premature to conclude that Warsh is a hawk based on just one press conference. Currently, high inflation, supply shocks, geopolitical conflicts, fiscal imbalances, the impact of artificial intelligence, and the restructuring of macroeconomic logic are intertwined, compounded by a president determined to suppress market interest rates. Warsh and the FOMC are navigating a complex and treacherous policy landscape. Whether Warsh is a staunch hawk, a "paper hawk" who only makes empty threats, or a moderate dove, only time will tell.

(The author of this article, Mark Sobel, is the U.S. Chairman of the Official Monetary and Financial Forum (OMFIF).)

This was Warsh's first Federal Open Market Committee (FOMC) policy meeting. A Fed chair's policy reputation is often established upon their first appearance on the scene, and policy credibility is fundamental to their position. At the meeting, Warsh pointed out that the Fed's inflation target has been missed for five consecutive years, with the current inflation rate climbing to 4% and the labor market generally booming. Against this macroeconomic backdrop, he emphasized the core objective of price stability.

In his heart, Warsh may lean towards hawkishness and has good reason to believe that the Fed's previous forward guidance was overly protective of the market and too direct in its information delivery. Even though Donald Trump has toned down his rhetoric after this policy meeting, acknowledging that the conditions for a rate cut are not currently in place, his continued pressure on the Fed to cut rates still casts a shadow over Warsh.

This is why the policy statement did not provide any forward guidance, Warsh himself did not submit his personal interest rate projections in the dot plot, and avoided commenting on the future path of interest rates throughout, which aligns with his own practical considerations. If Trump learns that Warsh's interest rate projections do not support rate cuts, he will inevitably launch another public attack. Meanwhile, other FOMC members submitted their projections as usual, with nine members supporting rate hikes. Market discussion was completely dominated by expectations of rate hikes, and US Treasury yields rose accordingly—essentially, the financial market spontaneously absorbed the actual effect of monetary tightening.

The launch of several new assessment programs is justified.

The new chairman's proposal to review the Fed's current policy mechanisms is reasonable. Warsh's establishment of five special working groups to review the Fed's communication mechanisms, inflation policy framework, balance sheet, economic data methodology, productivity, and employment is quite significant. The inflation framework and productivity issues deserve particular attention and may become key clues for determining Warsh's true policy inclination (hawkish or dovish).

According to the plan, all assessment work must be completed within six months, compressing a large amount of research and analysis work into an extremely short period. Anyone familiar with government operations knows that the definition of the working group's research responsibilities and personnel composition are crucial in determining the final conclusions. Does the working group's research boundaries and member configuration uphold neutrality and objectivity, or does it carry a pre-existing policy bias?

Regarding the inflation policy framework, two core questions will directly influence the future direction of interest rates: What constitutes price stability? And what indicators should be used to measure inflation?

Walsh seems to agree with the 2% target for price stability, but he suggests a logical fallacy in the use of zeros after the decimal point, implying a false sense of precision. If this argument holds true, the reasonable range for price stability might be broadened to 2.49%.

Furthermore, the debate surrounding inflation metrics has never ceased. Warsh mentioned a preference for using cut-down mean inflation metrics: the Dallas Fed's cut-down mean personal consumption expenditures (PCE) inflation is currently below 2.5%, while regular PCE inflation is approaching 4%; the Cleveland Fed's cut-down mean consumer price index (CPI) inflation has exceeded 3%.

Chart 1: What inflation measure should the Federal Reserve use?

(Data source: Federal Reserve Bank of Cleveland, Federal Reserve Bank of Dallas, Bureau of Economic Analysis, U.S. Department of Commerce)

The difference between the cut-off mean inflation and the standard PCE inflation will continue to fluctuate with the economic cycle. If the Federal Reserve were to use the cut-off mean PCE indicator at this stage, coupled with an inflation tolerance range that is actually slightly higher than 2%, achieving the price stability goal would be significantly easier.

Regardless of which inflation indicator is ultimately chosen, adjusting the inflation rules midway before PCE inflation returns to 2%, or at least clearly enters a downward trend, could severely damage the Federal Reserve's policy credibility. Meanwhile, central banks worldwide consistently face significant challenges in assessing the medium-term inflation outlook. However, if one argues that the Fed is unable to offset supply shocks and weaken the impact of the second-order transmission effect of inflation, this argument can support room for looser monetary policy.

There is a huge disagreement regarding productivity-related claims.

Drawing on the economic experience of the United States in the 1990s during the Alan Greenspan era, Warsh argues that artificial intelligence will boost overall productivity and drive economic growth without creating inflationary pressures, thus creating policy space for interest rate cuts.

This viewpoint is highly controversial in academic circles. Greenspan delayed interest rate hikes precisely because he anticipated continued productivity growth. In the short term, the boost to aggregate demand from AI-related investments and industrial expansion far outweighs supply-side capacity expansion, thus creating upward inflationary pressure. Many economists believe that productivity gains will push up the natural equilibrium interest rate; and that technological innovation's penetration into the real economy and its transmission to people's daily lives is very slow.

In short, most economists are skeptical that "the productivity revolution of artificial intelligence can change the direction of inflation and interest rates in the short term."

In summary, the staffing of the working group and its final research conclusions are crucial: the two sets of arguments—inflation measurement standards and productivity—can both deduce the feasibility of interest rate cuts and corroborate the necessity of maintaining high interest rates.

It's premature to conclude that Warsh is a hawk based on just one press conference. Currently, high inflation, supply shocks, geopolitical conflicts, fiscal imbalances, the impact of artificial intelligence, and the restructuring of macroeconomic logic are intertwined, compounded by a president determined to suppress market interest rates. Warsh and the FOMC are navigating a complex and treacherous policy landscape. Whether Warsh is a staunch hawk, a "paper hawk" who only makes empty threats, or a moderate dove, only time will tell.

(The author of this article, Mark Sobel, is the U.S. Chairman of the Official Monetary and Financial Forum (OMFIF).)

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.