Warsh's speech on multiple reforms led to a sharp drop in the dollar and a strong rebound in gold.

2026-07-01 21:56:13

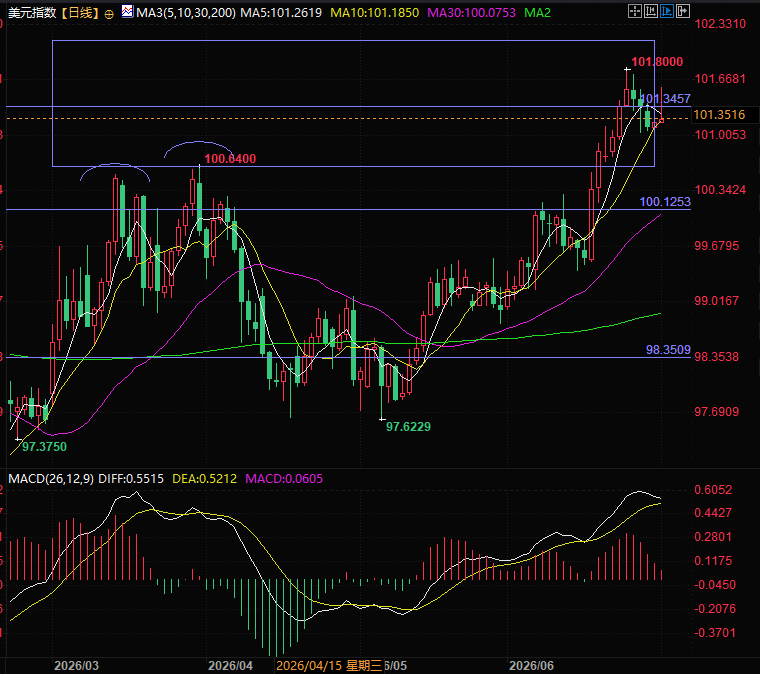

Recently, the US dollar index (DXY) has continued to demonstrate its hegemonic position at high levels. Currently, it has retreated from its highs ahead of the non-farm payrolls report and amid collective speeches by central banks around the world, and is trading around 101.37.

The core logic supporting this recent strength lies not only in the passive weakening of non-US currencies (such as the Japanese yen and the euro), but also in the continued buying of global funds into the underlying logic of "the resilience of the US economy + the Federal Reserve maintaining high interest rates".

However, the recent dramatic shift in the policy frameworks of major central banks around the world, and the Federal Reserve's latest statement on the relationship between artificial intelligence (AI) and interest rate hikes, have directly dispelled recent market concerns about Fed rate hikes. As mentioned in previous articles, after the decline in oil prices and the resolution of the core inflation problem caused by the Holmuz policy, gold prices will return to the logic of safe-haven demand and the influence of the Federal Reserve.

At the recently concluded European Central Bank forum, the world's two largest central banks signaled a weakening of forward guidance. ECB President Christine Lagarde admitted that the biggest regret of past policies was being overly constrained by rigid forward guidance.

Following this, Federal Reserve Chairman Kevin Warsh also made a significant statement: the Federal Reserve will no longer provide clear forward guidance on interest rates, and will instead use a new policy framework to enhance decision-making flexibility.

Forward guidance was once a powerful tool used by central banks to anchor market interest rate expectations in advance and reduce macroeconomic uncertainty.

However, once the central bank chooses to "remove this guiding light," the uncertainty of future monetary policy will increase significantly.

To compensate for unknown policy risks, investors will inevitably demand a higher risk premium, which initially triggered a surge in the pricing yield of US Treasury bonds globally.

However, the one-sided plunge in the bond market did not continue indefinitely. Subsequently, a recent discussion by Federal Reserve Chairman Warsh on interest rate hikes and artificial intelligence (AI) quickly cooled down the overheated bond market, causing yields and the dollar to fall from their short-term highs.

In this highly anticipated discussion about interest rate hikes, Warsh pointed out, "There is not enough information to determine whether artificial intelligence will lead to inflation." He further explained that AI companies are currently in a phase of intensive investment in the future, with the expectation that these huge investments will lead to a comprehensive expansion of the supply side in the future.

Walsh continued: If models hinder good policy, discard them; the task force leader may be announced next week.

From a macroeconomic perspective, increased productivity and expansion of the supply side mean an increase in potential output, which can fundamentally offset inflationary pressures.

This statement sends a crucial signal to the market: as AI is expected to lead to a significant expansion of the supply side in the future, the urgency and probability of the Federal Reserve raising interest rates further are decreasing significantly.

The surge in US Treasury yields triggered by the lack of guidance has found a balance thanks to the reassurance of declining interest rate hike expectations.

With the elimination of the tail risk of interest rate hikes, Treasury yields and the US dollar index subsequently experienced a rational pullback and respite from their highs, with the US dollar falling accordingly.

In a state of "blind flight" without forward-looking policy guidance, global financial markets experienced a devastating "bond market stampede" last night (June 30), with the 10-year US Treasury yield soaring. This terrifying storm was the trigger for a multi-faceted convergence of macroeconomic policy shifts, fundamentals, liquidity, and technical factors:

JOLTS job openings surged to a two-year high in May, shattering market expectations that the U.S. economy was cooling down rapidly and setting the stage for a bond market crash.

"Non-farm payroll fear" and the defense of the yen: In the face of the important non-farm payroll data to be released this week, bulls are selling off US Treasuries in advance to stop losses due to concerns that the data will continue to strengthen.

Meanwhile, the yen fell below its historic low of 162.8 against the dollar, fueling market concerns that the Japanese government might intervene in the foreign exchange market by selling its holdings of US Treasury bonds to buy yen, leading to a surge in psychological selling pressure.

The surge in US Treasury yields is essentially a violent repricing of the expectation that "the Federal Reserve will maintain high interest rates for a longer period of time" in the global market without any forward guidance, and it has directly injected a strong boost into the US dollar index.

Amidst the dramatic rollercoaster ride of expectations in the bond market, the latest June ADP employment data (non-farm payrolls) provides a "soft landing" support for the US dollar's fundamentals from another perspective.

Data shows that private sector employment increased by 98,000 in June, lower than the expected 118,000, signaling a slowdown in job creation. However, the underlying message of this report supports the "resilience" of the US dollar:

Layoffs have plummeted, but companies have not downsized: the number of planned layoffs has dropped by 53% to 45,849, a level typically seen in the summer.

The slowdown in recruitment is mainly due to the longer job search cycle and labor supply constraints in some industries, rather than large-scale layoffs by companies.

While artificial intelligence continues to reshape the employment landscape in the technology industry, there is no risk of a slowdown in the overall job market.

Job vacancies remain: the job vacancy-to-unemployment ratio was still as high as 1.04 in May. This means that although new hiring opportunities have narrowed, the labor market has significantly stabilized from last year's weakness.

For the US dollar, this report does not support the narrative of a panic-driven recession. Instead, it confirms the picture of a "moderate slowdown but not a stall" in the US economy. As long as the fundamentals of the US economy remain more resilient than those of Europe and Japan, which are mired in recession, the threshold for significant interest rate cuts remains high.

The abandonment of forward guidance by the US and European central banks has inadvertently increased the volatility of the global bond market, leading to a rise in US Treasury yields due to increased risk premiums.

However, Federal Reserve Chairman Warsh's statement that "AI will expand the supply side and reduce the probability of interest rate hikes" promptly reassured the market, causing Treasury yields and the dollar to fall from their highs, completing a short-term loop of bullish and bearish logic.

(US Dollar Index Daily Chart, Source: FX678)

Before the official non-farm payroll report and subsequent inflation developments are revealed, funds are still betting on interest rate hikes and better-than-expected US employment data. However, the complete reliance on data has begun to loosen. As mentioned in previous articles, before the five Warsh task forces are established and relevant discussions are given, the Federal Reserve will most likely continue to hold its positions, and the possibility of raising interest rates is not high.

Gold prices rebounded sharply as the dollar surged and then retreated, coupled with easing inflation concerns, making the Federal Reserve the most important factor influencing gold prices once again.

(Spot gold daily chart, source: FX678)

At 21:49 Beijing time, spot gold is trading at $4,090 per ounce, and the US dollar index is currently at 101.23.

The core logic supporting this recent strength lies not only in the passive weakening of non-US currencies (such as the Japanese yen and the euro), but also in the continued buying of global funds into the underlying logic of "the resilience of the US economy + the Federal Reserve maintaining high interest rates".

However, the recent dramatic shift in the policy frameworks of major central banks around the world, and the Federal Reserve's latest statement on the relationship between artificial intelligence (AI) and interest rate hikes, have directly dispelled recent market concerns about Fed rate hikes. As mentioned in previous articles, after the decline in oil prices and the resolution of the core inflation problem caused by the Holmuz policy, gold prices will return to the logic of safe-haven demand and the influence of the Federal Reserve.

At the recently concluded European Central Bank forum, the world's two largest central banks signaled a weakening of forward guidance. ECB President Christine Lagarde admitted that the biggest regret of past policies was being overly constrained by rigid forward guidance.

Following this, Federal Reserve Chairman Kevin Warsh also made a significant statement: the Federal Reserve will no longer provide clear forward guidance on interest rates, and will instead use a new policy framework to enhance decision-making flexibility.

Forward guidance was once a powerful tool used by central banks to anchor market interest rate expectations in advance and reduce macroeconomic uncertainty.

However, once the central bank chooses to "remove this guiding light," the uncertainty of future monetary policy will increase significantly.

To compensate for unknown policy risks, investors will inevitably demand a higher risk premium, which initially triggered a surge in the pricing yield of US Treasury bonds globally.

Unexpected Changes: Warsh Discusses the Game Between AI and Interest Rate Hike Expectations

However, the one-sided plunge in the bond market did not continue indefinitely. Subsequently, a recent discussion by Federal Reserve Chairman Warsh on interest rate hikes and artificial intelligence (AI) quickly cooled down the overheated bond market, causing yields and the dollar to fall from their short-term highs.

In this highly anticipated discussion about interest rate hikes, Warsh pointed out, "There is not enough information to determine whether artificial intelligence will lead to inflation." He further explained that AI companies are currently in a phase of intensive investment in the future, with the expectation that these huge investments will lead to a comprehensive expansion of the supply side in the future.

Walsh continued: If models hinder good policy, discard them; the task force leader may be announced next week.

From a macroeconomic perspective, increased productivity and expansion of the supply side mean an increase in potential output, which can fundamentally offset inflationary pressures.

This statement sends a crucial signal to the market: as AI is expected to lead to a significant expansion of the supply side in the future, the urgency and probability of the Federal Reserve raising interest rates further are decreasing significantly.

The surge in US Treasury yields triggered by the lack of guidance has found a balance thanks to the reassurance of declining interest rate hike expectations.

With the elimination of the tail risk of interest rate hikes, Treasury yields and the US dollar index subsequently experienced a rational pullback and respite from their highs, with the US dollar falling accordingly.

Last night's horror: The stampede and violent repricing of US debt in the vacuum of foresight

In a state of "blind flight" without forward-looking policy guidance, global financial markets experienced a devastating "bond market stampede" last night (June 30), with the 10-year US Treasury yield soaring. This terrifying storm was the trigger for a multi-faceted convergence of macroeconomic policy shifts, fundamentals, liquidity, and technical factors:

JOLTS job openings surged to a two-year high in May, shattering market expectations that the U.S. economy was cooling down rapidly and setting the stage for a bond market crash.

"Non-farm payroll fear" and the defense of the yen: In the face of the important non-farm payroll data to be released this week, bulls are selling off US Treasuries in advance to stop losses due to concerns that the data will continue to strengthen.

Meanwhile, the yen fell below its historic low of 162.8 against the dollar, fueling market concerns that the Japanese government might intervene in the foreign exchange market by selling its holdings of US Treasury bonds to buy yen, leading to a surge in psychological selling pressure.

The surge in US Treasury yields is essentially a violent repricing of the expectation that "the Federal Reserve will maintain high interest rates for a longer period of time" in the global market without any forward guidance, and it has directly injected a strong boost into the US dollar index.

Latest ADP report: Cooling down but not stalled, the US dollar remains "safe".

Amidst the dramatic rollercoaster ride of expectations in the bond market, the latest June ADP employment data (non-farm payrolls) provides a "soft landing" support for the US dollar's fundamentals from another perspective.

Data shows that private sector employment increased by 98,000 in June, lower than the expected 118,000, signaling a slowdown in job creation. However, the underlying message of this report supports the "resilience" of the US dollar:

Layoffs have plummeted, but companies have not downsized: the number of planned layoffs has dropped by 53% to 45,849, a level typically seen in the summer.

The slowdown in recruitment is mainly due to the longer job search cycle and labor supply constraints in some industries, rather than large-scale layoffs by companies.

While artificial intelligence continues to reshape the employment landscape in the technology industry, there is no risk of a slowdown in the overall job market.

Job vacancies remain: the job vacancy-to-unemployment ratio was still as high as 1.04 in May. This means that although new hiring opportunities have narrowed, the labor market has significantly stabilized from last year's weakness.

For the US dollar, this report does not support the narrative of a panic-driven recession. Instead, it confirms the picture of a "moderate slowdown but not a stall" in the US economy. As long as the fundamentals of the US economy remain more resilient than those of Europe and Japan, which are mired in recession, the threshold for significant interest rate cuts remains high.

Summarize:

The abandonment of forward guidance by the US and European central banks has inadvertently increased the volatility of the global bond market, leading to a rise in US Treasury yields due to increased risk premiums.

However, Federal Reserve Chairman Warsh's statement that "AI will expand the supply side and reduce the probability of interest rate hikes" promptly reassured the market, causing Treasury yields and the dollar to fall from their highs, completing a short-term loop of bullish and bearish logic.

(US Dollar Index Daily Chart, Source: FX678)

Before the official non-farm payroll report and subsequent inflation developments are revealed, funds are still betting on interest rate hikes and better-than-expected US employment data. However, the complete reliance on data has begun to loosen. As mentioned in previous articles, before the five Warsh task forces are established and relevant discussions are given, the Federal Reserve will most likely continue to hold its positions, and the possibility of raising interest rates is not high.

Gold prices rebounded sharply as the dollar surged and then retreated, coupled with easing inflation concerns, making the Federal Reserve the most important factor influencing gold prices once again.

(Spot gold daily chart, source: FX678)

At 21:49 Beijing time, spot gold is trading at $4,090 per ounce, and the US dollar index is currently at 101.23.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.