One chart: Baltic Dry Index freight rates across all sectors rose in unison, rebounding from two-month lows.

2026-07-02 00:30:33

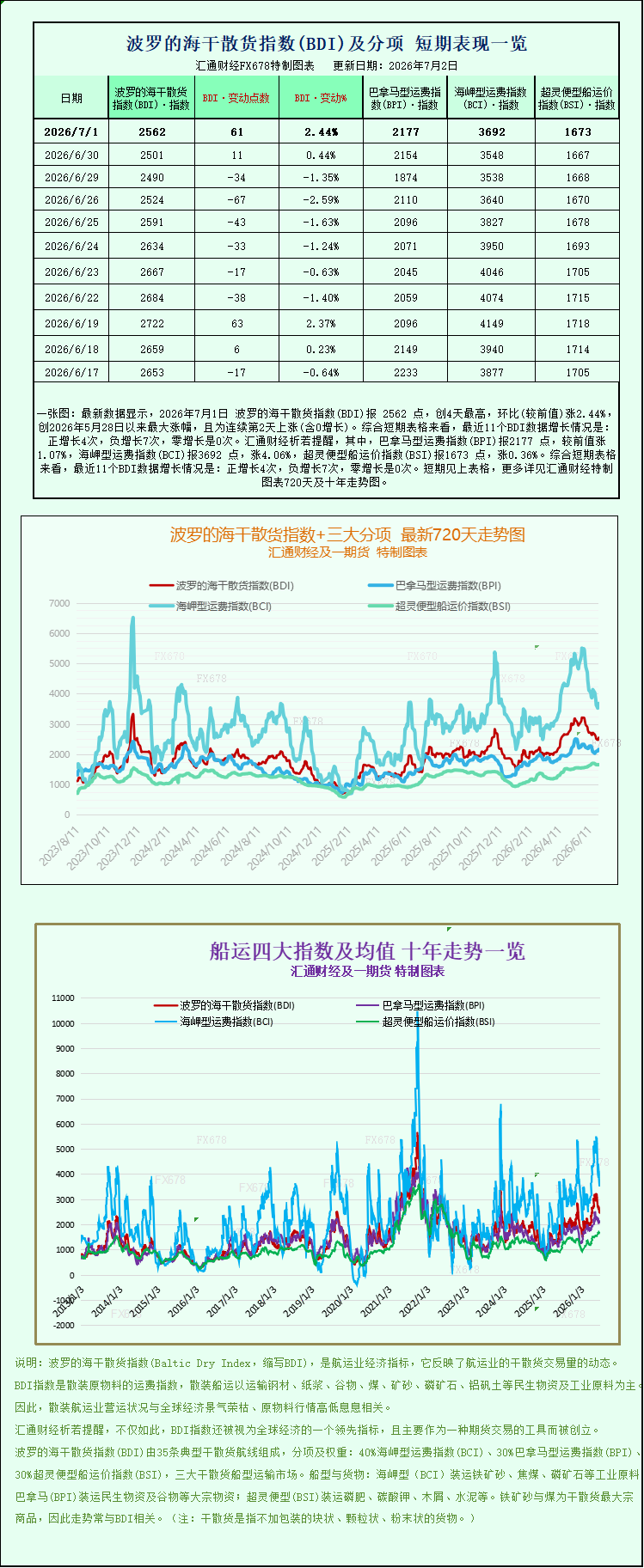

Latest data shows that the Baltic Dry Index (BDI) reached 2562 points on July 1, 2026, a four-day high, up 2.44% month-on-month (compared to the previous value), marking the largest increase since May 28, 2026, and the second consecutive day of increase (including zero growth). Looking at the short-term charts, the recent 11 BDI data points show: 4 positive increases, 7 negative increases, and 0 zero increases. Specifically, the Panamax Freight Index (BPI) reached 2177 points, up 1.07% from the previous value; the Capesize Freight Index (BCI) reached 3692 points, up 4.06%; and the Supramax Freight Index (BSI) reached 1673 points, up 0.36%. For detailed 720-day and 10-year trend charts of the Baltic Dry Index and its three main sub-indices, please refer to the specially designed charts.

On Wednesday, July 1, 2026, the international shipping market saw a significant recovery. The Baltic Dry Index (BDI), a key indicator of global dry bulk shipping rates, rose across the board. Supported by strong freight rates for the three main vessel types—Capesize, Panamax, and Supramax—the index rebounded from its two-month low earlier in the week, demonstrating a sustained recovery and signaling a clear marginal recovery in global commodity shipping demand. As the core pricing benchmark for global dry bulk trade, the Baltic Dry Index's fluctuations directly correlate with the cross-border transportation costs of basic commodities such as iron ore, thermal coal, grain, and fertilizers. The significant rebound in the index directly reflects the simultaneous recovery in transportation demand for global industrial production, energy supplies, and agricultural trade, injecting a temporary boost into the dry bulk shipping market, which had been under pressure in the first half of the year.

According to the closing data, the Baltic Dry Index (BDI) rose 61 points, a 2.4% increase, closing at 2562 points. Looking back at this week's market performance, the market had previously entered a period of sustained weakness and adjustment. On Monday, the index hit a low point, reaching its lowest level in nearly two and a half months since April 15th. At that time, the market was generally concerned that persistently weak global bulk shipping demand and an oversupply of shipping capacity would suppress freight rates in the long term. However, just two trading days later, the index staged a strong reversal, with freight rates for all three major ship types showing no decline, forming a rare pattern of across-the-board price increases. This reversed the previous one-sided downward market sentiment. Many shipping brokers stated that this rebound was supported by genuine freight orders and was not a short-term speculative surge, indicating a substantial recovery in market confidence.

Among the various ship types, the Capesize vessel sector, the largest in size and with the strongest impact on the overall index, led the market and became the core driver of this index rebound. The sub-index representing Capesize freight rates surged 144 points in a single day, a gain of 4.1%, closing at 3692 points, leading all ship types in both the increase and the percentage rise. Capesize vessels are the mainstay of the dry bulk shipping system, with standard deadweight tonnage reaching 150,000 tons. They primarily undertake long-distance transoceanic bulk commodity transportation, focusing on two core industrial raw materials: iron ore for steelmaking and thermal coal for power generation. Their routes cover key global industrial freight corridors such as Brazil to China, Australia to East Asia, and South Africa to Europe. Their freight rate fluctuations directly reflect the operating rates and raw material procurement schedules of the global steel and power industries.

Along with the significant rise in the index, the profitability of the Capesize vessel market has also improved substantially. The average daily earnings of standard Capesize vessels increased by $1,303 in a single day, with the latest average daily revenue firmly above the $29,981 mark. Compared to the low point at the beginning of this week, the current improvement in vessel operating profitability is significant, and the operating pressure on shipowners has been significantly alleviated. In the first half of the year, the global steel industry experienced longer maintenance cycles, overseas steel mills reduced production and inventories, and iron ore shipments slowed down in stages. As a result, a large number of Capesize vessels were either idled or forced to lower freight rates to attract cargo, leading to continued losses for many ocean shipping companies in this segment. From late June to early July, multiple positive factors materialized: East Asian steel mills resumed restocking raw materials after completing concentrated maintenance, and shipments from major iron ore producing regions in Australia and Brazil steadily rebounded; many European countries entered their summer peak electricity consumption period, and thermal power plants increased their imported coal reserves; meanwhile, fuel prices on ocean shipping routes fell slightly, reducing the marginal cost of ship operation. These multiple factors combined to drive up the demand for chartering large coal and mineral transport vessels, significantly enhancing shipowners' bargaining power and directly leading to a sharp jump in freight rates in the Cape of Good Hope region.

The Panamax sector, the main medium-sized vessel type, also recorded steady gains, with a stable trend and no significant divergence. The Panamax freight rate index rose 23 points, or 1.1%, to close at 2177 points. Panamax vessels have a deadweight tonnage between 60,000 and 70,000 tons, are compatible with Panama Canal navigation standards, have a wider route coverage, and can transport energy coal, corn, soybeans, wheat, and other food crops, as well as industrial auxiliary materials. They cater to both industrial and agricultural trade sectors, resulting in a more balanced market demand and freight rate fluctuations that are typically smaller than those of large Capesize vessels.

Corresponding market profit data shows that the average daily earnings of standard Panamax vessels rose by $208 in a single day, with current average daily operating revenue reaching $19,591. The peak season for global grain trade is the key driver supporting the strength of Panamax freight rates. The Northern Hemisphere is entering the peak season for summer grain harvests, and major grain-producing regions in the US and South America are beginning new seasons of wheat and corn shipments. A large number of grain orders are driving up charter demand on Atlantic and Pacific grain routes. At the same time, the continued expansion of industries in emerging markets in Southeast Asia and the Middle East, along with the continued import of thermal coal to ensure local power generation capacity, is supporting the Panamax shipping market with industrial bulk cargo demand. Compared to Capesize vessels, which are solely affected by the steel cycle, Panamax vessels are supported by demand from both grain and coal, making their market performance more resilient. Although the daily increase is not as large ore carriers, the steady upward trend confirms the simultaneous improvement in global demand for multi-category bulk cargo transportation.

The Supramax vessel sector, comprised of small and medium-sized flexible shipping vessels, continued its moderate upward trend, completing the overall sector's upward momentum. The Supramax freight rate index rose slightly by 6 points, or 0.4%, to close at 1673 points. Supramax vessels are smaller in tonnage and more adaptable to ports, capable of berthing at small and medium-sized feeder ports. They primarily handle short-haul, small-volume bulk cargo transportation such as fertilizers, cement clinker, small-batch grains, bauxite, and metal ores. Their routes are concentrated on short-haul regional shipping, including transshipment within Southeast Asia, short-haul trade along the Mediterranean coast, and feeder transport along the Americas coast, making them a core shipping capacity for regional trade and logistics.

The sector's gains were relatively moderate, primarily due to the ample number of vessels deployed on regional routes. The supply and demand balance in shipping capacity did not show a significant gap. However, the global manufacturing recovery boosted cross-border circulation of basic chemicals and building materials, coupled with the continued release of domestic demand in Southeast Asian and South Asian countries. This led to a steady increase in regional short-haul bulk cargo shipping orders, supporting a steady rise in freight rates and resulting in consecutive small increases. This completed a market trend of strength across all three vessel types.

Based on a comprehensive analysis of the current shipping market fundamentals, the recent rebound in the Baltic Dry Index from its recent lows is not driven by a single short-term factor, but rather by a recovery resulting from the convergence of multiple positive supply and demand factors. On the demand side, the global manufacturing sector is showing signs of recovery, with a concentrated release of restocking demand for industrial raw materials in East Asia, Europe, and Southeast Asia. Seaborne trade volumes for the three core bulk commodities—iron ore, coal, and grain—have all increased month-on-month. On the supply side, the scrapping of a large number of older vessels and the entry of some ships into their seasonal maintenance cycles have slightly reduced the effective operational capacity in the short term, alleviating the previous pressure of overcapacity. On the cost side, the temporary correction in international marine fuel prices has lowered shipowners' operating costs, encouraging companies to moderately increase charter rates, further pushing up freight rates.

However, shipping market participants remain rational and cautious, as multiple factors continue to exert downward pressure on the market in the medium to long term. On one hand, global central banks maintain tight monetary policies, and the pace of recovery in overseas manufacturing remains uncertain. If steel mills and power plants slow down their raw material procurement, large bulk carrier freight rates will face downward pressure. On the other hand, global shipyards have seen a continuous increase in new ship deliveries in recent years, and a large number of newly built dry bulk vessels will be launched into the market in the coming months. This expansion of shipping capacity in the medium to long term may again suppress the upward potential of freight rates. In addition, changes in geopolitical trade, adjustments to shipping policies in commodity-exporting countries, and the impact of extreme weather on port handling efficiency can all potentially alter short-term shipping trends at any time.

From an industry operations perspective, this round of index rebound is a substantial benefit to global dry bulk shipping companies. The profitability of ocean-going shipowners, which had been under continuous pressure in the first half of the year, has seen a phased recovery, especially for shipping companies holding large captive Cape and Panamax vessels. Their average daily vessel revenue has increased significantly, effectively covering operating costs such as fuel, port fees, and labor, alleviating the pressure of losses in the first half of the year. For commodity traders, the short-term rise in freight rates will slightly increase the overall cost of raw material imports, but current freight rates are still far lower than the high levels of the same period last year, and overall transportation costs remain within a controllable range, unlikely to have a significant impact on the end-consumer market for commodities.

Analysts at the Baltic Exchange noted in their market commentary that the current market structure, with all three vessel types showing simultaneous strength, is quite rare, indicating a comprehensive recovery in global bulk shipping demand, rather than a localized trend focused on a single cargo type or route. In the short term, with the continued release of demand for summer energy reserves and summer grain shipments, freight rates are likely to maintain a volatile but upward trend. Going forward, it will be necessary to continuously monitor three core indicators: iron ore shipment data from Australia and Brazil, grain export orders from the US and South America, and global steel mill operating rates, to determine the sustainability of this rebound. If cross-border freight volumes of bulk commodities can remain high, the Baltic Dry Index is expected to further recover, gradually regaining previous losses; however, if downstream purchasing demand declines rapidly, the index may re-enter a period of consolidation and adjustment.

By Wednesday's close, sentiment in the dry bulk shipping market had fundamentally reversed compared to the beginning of the week. The previously widespread pessimism had largely dissipated, with shipping brokers raising charter rates in tandem, and spot charter activity significantly increasing. Market participants will continue to closely monitor freight order placements in the coming days to determine whether this round of across-the-board freight rate increases can translate into a medium- to long-term upward trend. Furthermore, the subsequent movement of the Baltic Dry Index will continue to be a key leading indicator for observing the health of global industrial and agricultural cross-border trade.

On Wednesday, July 1, 2026, the international shipping market saw a significant recovery. The Baltic Dry Index (BDI), a key indicator of global dry bulk shipping rates, rose across the board. Supported by strong freight rates for the three main vessel types—Capesize, Panamax, and Supramax—the index rebounded from its two-month low earlier in the week, demonstrating a sustained recovery and signaling a clear marginal recovery in global commodity shipping demand. As the core pricing benchmark for global dry bulk trade, the Baltic Dry Index's fluctuations directly correlate with the cross-border transportation costs of basic commodities such as iron ore, thermal coal, grain, and fertilizers. The significant rebound in the index directly reflects the simultaneous recovery in transportation demand for global industrial production, energy supplies, and agricultural trade, injecting a temporary boost into the dry bulk shipping market, which had been under pressure in the first half of the year.

According to the closing data, the Baltic Dry Index (BDI) rose 61 points, a 2.4% increase, closing at 2562 points. Looking back at this week's market performance, the market had previously entered a period of sustained weakness and adjustment. On Monday, the index hit a low point, reaching its lowest level in nearly two and a half months since April 15th. At that time, the market was generally concerned that persistently weak global bulk shipping demand and an oversupply of shipping capacity would suppress freight rates in the long term. However, just two trading days later, the index staged a strong reversal, with freight rates for all three major ship types showing no decline, forming a rare pattern of across-the-board price increases. This reversed the previous one-sided downward market sentiment. Many shipping brokers stated that this rebound was supported by genuine freight orders and was not a short-term speculative surge, indicating a substantial recovery in market confidence.

Among the various ship types, the Capesize vessel sector, the largest in size and with the strongest impact on the overall index, led the market and became the core driver of this index rebound. The sub-index representing Capesize freight rates surged 144 points in a single day, a gain of 4.1%, closing at 3692 points, leading all ship types in both the increase and the percentage rise. Capesize vessels are the mainstay of the dry bulk shipping system, with standard deadweight tonnage reaching 150,000 tons. They primarily undertake long-distance transoceanic bulk commodity transportation, focusing on two core industrial raw materials: iron ore for steelmaking and thermal coal for power generation. Their routes cover key global industrial freight corridors such as Brazil to China, Australia to East Asia, and South Africa to Europe. Their freight rate fluctuations directly reflect the operating rates and raw material procurement schedules of the global steel and power industries.

Along with the significant rise in the index, the profitability of the Capesize vessel market has also improved substantially. The average daily earnings of standard Capesize vessels increased by $1,303 in a single day, with the latest average daily revenue firmly above the $29,981 mark. Compared to the low point at the beginning of this week, the current improvement in vessel operating profitability is significant, and the operating pressure on shipowners has been significantly alleviated. In the first half of the year, the global steel industry experienced longer maintenance cycles, overseas steel mills reduced production and inventories, and iron ore shipments slowed down in stages. As a result, a large number of Capesize vessels were either idled or forced to lower freight rates to attract cargo, leading to continued losses for many ocean shipping companies in this segment. From late June to early July, multiple positive factors materialized: East Asian steel mills resumed restocking raw materials after completing concentrated maintenance, and shipments from major iron ore producing regions in Australia and Brazil steadily rebounded; many European countries entered their summer peak electricity consumption period, and thermal power plants increased their imported coal reserves; meanwhile, fuel prices on ocean shipping routes fell slightly, reducing the marginal cost of ship operation. These multiple factors combined to drive up the demand for chartering large coal and mineral transport vessels, significantly enhancing shipowners' bargaining power and directly leading to a sharp jump in freight rates in the Cape of Good Hope region.

The Panamax sector, the main medium-sized vessel type, also recorded steady gains, with a stable trend and no significant divergence. The Panamax freight rate index rose 23 points, or 1.1%, to close at 2177 points. Panamax vessels have a deadweight tonnage between 60,000 and 70,000 tons, are compatible with Panama Canal navigation standards, have a wider route coverage, and can transport energy coal, corn, soybeans, wheat, and other food crops, as well as industrial auxiliary materials. They cater to both industrial and agricultural trade sectors, resulting in a more balanced market demand and freight rate fluctuations that are typically smaller than those of large Capesize vessels.

Corresponding market profit data shows that the average daily earnings of standard Panamax vessels rose by $208 in a single day, with current average daily operating revenue reaching $19,591. The peak season for global grain trade is the key driver supporting the strength of Panamax freight rates. The Northern Hemisphere is entering the peak season for summer grain harvests, and major grain-producing regions in the US and South America are beginning new seasons of wheat and corn shipments. A large number of grain orders are driving up charter demand on Atlantic and Pacific grain routes. At the same time, the continued expansion of industries in emerging markets in Southeast Asia and the Middle East, along with the continued import of thermal coal to ensure local power generation capacity, is supporting the Panamax shipping market with industrial bulk cargo demand. Compared to Capesize vessels, which are solely affected by the steel cycle, Panamax vessels are supported by demand from both grain and coal, making their market performance more resilient. Although the daily increase is not as large ore carriers, the steady upward trend confirms the simultaneous improvement in global demand for multi-category bulk cargo transportation.

The Supramax vessel sector, comprised of small and medium-sized flexible shipping vessels, continued its moderate upward trend, completing the overall sector's upward momentum. The Supramax freight rate index rose slightly by 6 points, or 0.4%, to close at 1673 points. Supramax vessels are smaller in tonnage and more adaptable to ports, capable of berthing at small and medium-sized feeder ports. They primarily handle short-haul, small-volume bulk cargo transportation such as fertilizers, cement clinker, small-batch grains, bauxite, and metal ores. Their routes are concentrated on short-haul regional shipping, including transshipment within Southeast Asia, short-haul trade along the Mediterranean coast, and feeder transport along the Americas coast, making them a core shipping capacity for regional trade and logistics.

The sector's gains were relatively moderate, primarily due to the ample number of vessels deployed on regional routes. The supply and demand balance in shipping capacity did not show a significant gap. However, the global manufacturing recovery boosted cross-border circulation of basic chemicals and building materials, coupled with the continued release of domestic demand in Southeast Asian and South Asian countries. This led to a steady increase in regional short-haul bulk cargo shipping orders, supporting a steady rise in freight rates and resulting in consecutive small increases. This completed a market trend of strength across all three vessel types.

Based on a comprehensive analysis of the current shipping market fundamentals, the recent rebound in the Baltic Dry Index from its recent lows is not driven by a single short-term factor, but rather by a recovery resulting from the convergence of multiple positive supply and demand factors. On the demand side, the global manufacturing sector is showing signs of recovery, with a concentrated release of restocking demand for industrial raw materials in East Asia, Europe, and Southeast Asia. Seaborne trade volumes for the three core bulk commodities—iron ore, coal, and grain—have all increased month-on-month. On the supply side, the scrapping of a large number of older vessels and the entry of some ships into their seasonal maintenance cycles have slightly reduced the effective operational capacity in the short term, alleviating the previous pressure of overcapacity. On the cost side, the temporary correction in international marine fuel prices has lowered shipowners' operating costs, encouraging companies to moderately increase charter rates, further pushing up freight rates.

However, shipping market participants remain rational and cautious, as multiple factors continue to exert downward pressure on the market in the medium to long term. On one hand, global central banks maintain tight monetary policies, and the pace of recovery in overseas manufacturing remains uncertain. If steel mills and power plants slow down their raw material procurement, large bulk carrier freight rates will face downward pressure. On the other hand, global shipyards have seen a continuous increase in new ship deliveries in recent years, and a large number of newly built dry bulk vessels will be launched into the market in the coming months. This expansion of shipping capacity in the medium to long term may again suppress the upward potential of freight rates. In addition, changes in geopolitical trade, adjustments to shipping policies in commodity-exporting countries, and the impact of extreme weather on port handling efficiency can all potentially alter short-term shipping trends at any time.

From an industry operations perspective, this round of index rebound is a substantial benefit to global dry bulk shipping companies. The profitability of ocean-going shipowners, which had been under continuous pressure in the first half of the year, has seen a phased recovery, especially for shipping companies holding large captive Cape and Panamax vessels. Their average daily vessel revenue has increased significantly, effectively covering operating costs such as fuel, port fees, and labor, alleviating the pressure of losses in the first half of the year. For commodity traders, the short-term rise in freight rates will slightly increase the overall cost of raw material imports, but current freight rates are still far lower than the high levels of the same period last year, and overall transportation costs remain within a controllable range, unlikely to have a significant impact on the end-consumer market for commodities.

Analysts at the Baltic Exchange noted in their market commentary that the current market structure, with all three vessel types showing simultaneous strength, is quite rare, indicating a comprehensive recovery in global bulk shipping demand, rather than a localized trend focused on a single cargo type or route. In the short term, with the continued release of demand for summer energy reserves and summer grain shipments, freight rates are likely to maintain a volatile but upward trend. Going forward, it will be necessary to continuously monitor three core indicators: iron ore shipment data from Australia and Brazil, grain export orders from the US and South America, and global steel mill operating rates, to determine the sustainability of this rebound. If cross-border freight volumes of bulk commodities can remain high, the Baltic Dry Index is expected to further recover, gradually regaining previous losses; however, if downstream purchasing demand declines rapidly, the index may re-enter a period of consolidation and adjustment.

By Wednesday's close, sentiment in the dry bulk shipping market had fundamentally reversed compared to the beginning of the week. The previously widespread pessimism had largely dissipated, with shipping brokers raising charter rates in tandem, and spot charter activity significantly increasing. Market participants will continue to closely monitor freight order placements in the coming days to determine whether this round of across-the-board freight rate increases can translate into a medium- to long-term upward trend. Furthermore, the subsequent movement of the Baltic Dry Index will continue to be a key leading indicator for observing the health of global industrial and agricultural cross-border trade.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.