Multiple turning points converge, suggesting a potential reversal in the USD/JPY market.

2026-07-02 17:46:44

In the global macro-financial landscape, the Japanese yen (JPY) has always been known for its unique dual attributes as a "low-interest funding currency" and a "traditional safe-haven asset".

However, the yen has recently plummeted against the dollar (USD/JPY) to its lowest level in forty years since 1986.

Behind this extreme market situation lies not only a long-term capital game of profit-seeking regarding the "US-Japan interest rate differential," but also the result of a fierce collision between global politics, economics, and major sporting events at a critical juncture.

To understand the fluctuations in the US-Japan exchange rate, one must first look at the differences in the two countries' monetary policies.

Over the past few years, despite the pressure of domestic inflation exceeding 2%, the Bank of Japan (BOJ) has struggled to raise its benchmark interest rate to a multi-decade high of 1%. However, compared to the Federal Reserve's (Fed) previously high interest rate range, the huge interest rate differential between the two countries remains an insurmountable chasm.

This interest rate differential has given rise to Wall Street's largest "carry trade" model: global investment banks and hedge funds borrow low-cost yen, then sell it and convert it into dollars to buy high-yield US Treasury bonds or high-growth US tech stocks.

The continued outflow of capital has become the core cause of the disorderly and shallow depreciation of the yen, and has also directly increased the cost of domestic inflation in Japan, which is highly dependent on energy and food imports.

However, just as the market was habitually shorting the yen, several unprecedented major events have recently quietly changed the flow of funds:

A major geopolitical turning point in the Middle East: With the signing of the "60-day ceasefire agreement" and the official reopening of the key straits, the long-standing global oil supply chain crisis was instantly resolved.

International oil prices plummeted in response, which not only directly alleviated the imported inflation pressure on Japan, a major resource importer, but also caused the dollar's "geopolitical safe-haven aura" to begin to fade.

The World Cup and Betting: Meanwhile, the hosting of this top-tier global sporting event triggered a surge in employment in North America, effectively pre-emptively inflating the non-farm payroll job growth forecast.

Some long positions began to take profits from the previously crowded "USD/JPY carry trade," resulting in a subtle change in the liquidity structure of the foreign exchange market.

In this currency storm, the most crucial guiding force—the Federal Reserve's policy framework—has undergone a fundamental shift.

The Federal Reserve has completely shifted from its past approach of "single-minded anti-inflationary" or "hawkish rate hike predictions" to a pragmatic framework dominated by the latest real-time data.

Under this new framework, the first non-farm payroll report (NFP) following the geopolitical truce and the opening of the Taiwan Strait has become a crucial indicator that the entire market is holding its breath for:

Recalibrating Employment Data: With geopolitical tensions easing and lower supply chain costs for businesses, coupled with a surge in short-term service sector hiring spurred by the World Cup, the upcoming non-farm payroll data will directly reveal the true state of the US labor market, and may at least signal a peak.

Wage growth may have peaked: The mainstream market expectation is that with the recovery of supply chains and the lagged suppression of the real economy by high interest rates, the year-on-year wage growth in the United States is very likely to show a "peak and decline" signal in this data.

Once it is confirmed that wage growth has peaked, it will mean that the "wage-inflation spiral" of core inflation in the United States has been broken, and the Fed's data-driven interest rate cuts will be completely tilted.

Given the shift in the Federal Reserve's framework and the fact that the yen has hit a 40-year low, expectations for market intervention by the Japanese government (Ministry of Finance and Bank of Japan) have reached their maximum.

Although Japan has historically intervened by selling hundreds of billions of dollars worth of US Treasury bonds and buying yen, this has been insufficient to have a sustained and substantial impact on US Treasury yields, given the massive size of the US national debt.

However, its potential "deterrent effect" on the US stock market should not be underestimated: the risk of a stampede in carry trade: if the Bank of Japan decisively launches strong intervention, or even coordinates with the US, when the non-farm payroll data weakens (confirming that US wages have peaked) and the dollar actively declines, the yen will experience a sharp retaliatory appreciation.

This will directly lead to a surge in financing costs for Wall Street carry trades, forcing quantitative algorithms and hedge funds to "sell off US stock assets and buy back yen to pay off debts" in a short period of time.

The plunge in US tech stocks triggered by the Bank of Japan's interest rate hike in August 2024 was a perfect preview of this mechanism.

The current USD/JPY exchange rate is at a crossroads, a situation not seen in forty years.

With the global economic landscape shifting, the Federal Reserve moving towards data-driven strategies, and multiple catalysts such as geopolitical truce and the World Cup, the previous consensus of "blindly shorting the yen" has begun to loosen. This period, coupled with a weakening dollar, presents a window of opportunity with relatively low resistance to going long on the yen.

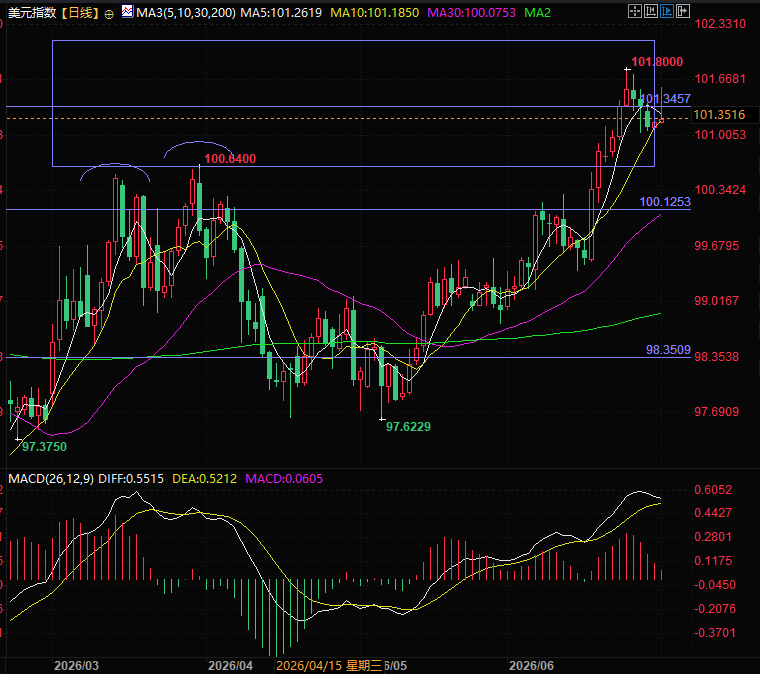

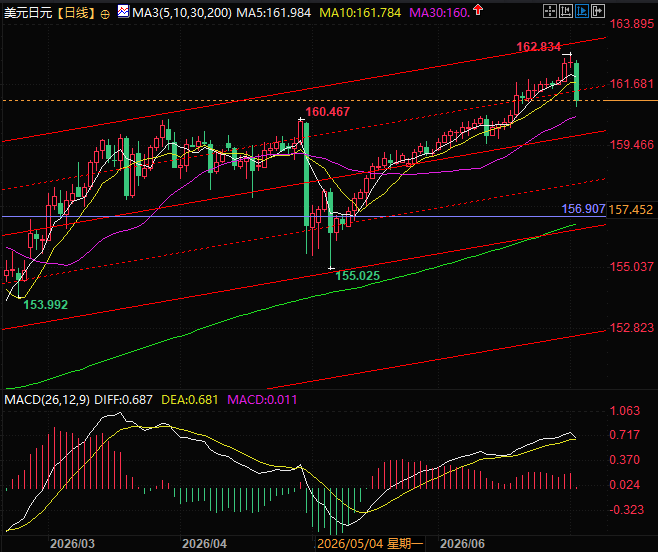

From a technical perspective, the US dollar has broken below the 5-day moving average and the midpoint of its trading range, while the Japanese yen has broken below its upward channel, both suggesting a potential trend reversal.

(US Dollar Index Daily Chart, Source: FX678)

For ordinary investors, keeping a close eye on the upcoming non-farm payroll data and wage growth indicators, and being wary of the Bank of Japan's swift actions in the foreign exchange market, will be of paramount importance in mitigating the risks of high volatility in US stocks and global assets.

(USD/JPY daily chart, source: FX678)

At 17:40 Beijing time, the US dollar index is currently at 100.99, and the US dollar/Japanese yen exchange rate is currently at 161.13/14.

However, the yen has recently plummeted against the dollar (USD/JPY) to its lowest level in forty years since 1986.

Behind this extreme market situation lies not only a long-term capital game of profit-seeking regarding the "US-Japan interest rate differential," but also the result of a fierce collision between global politics, economics, and major sporting events at a critical juncture.

The Deep-Rooted Logic Behind the Yen's Previous Extreme Weakness

To understand the fluctuations in the US-Japan exchange rate, one must first look at the differences in the two countries' monetary policies.

Over the past few years, despite the pressure of domestic inflation exceeding 2%, the Bank of Japan (BOJ) has struggled to raise its benchmark interest rate to a multi-decade high of 1%. However, compared to the Federal Reserve's (Fed) previously high interest rate range, the huge interest rate differential between the two countries remains an insurmountable chasm.

This interest rate differential has given rise to Wall Street's largest "carry trade" model: global investment banks and hedge funds borrow low-cost yen, then sell it and convert it into dollars to buy high-yield US Treasury bonds or high-growth US tech stocks.

The continued outflow of capital has become the core cause of the disorderly and shallow depreciation of the yen, and has also directly increased the cost of domestic inflation in Japan, which is highly dependent on energy and food imports.

A sweeping transformation: Geopolitics and the "withdrawal of funds" from international sporting events.

However, just as the market was habitually shorting the yen, several unprecedented major events have recently quietly changed the flow of funds:

A major geopolitical turning point in the Middle East: With the signing of the "60-day ceasefire agreement" and the official reopening of the key straits, the long-standing global oil supply chain crisis was instantly resolved.

International oil prices plummeted in response, which not only directly alleviated the imported inflation pressure on Japan, a major resource importer, but also caused the dollar's "geopolitical safe-haven aura" to begin to fade.

The World Cup and Betting: Meanwhile, the hosting of this top-tier global sporting event triggered a surge in employment in North America, effectively pre-emptively inflating the non-farm payroll job growth forecast.

Some long positions began to take profits from the previously crowded "USD/JPY carry trade," resulting in a subtle change in the liquidity structure of the foreign exchange market.

Framework Shift: The Fed's Data-Driven Logic and the "First Non-Farm Payrolls"

In this currency storm, the most crucial guiding force—the Federal Reserve's policy framework—has undergone a fundamental shift.

The Federal Reserve has completely shifted from its past approach of "single-minded anti-inflationary" or "hawkish rate hike predictions" to a pragmatic framework dominated by the latest real-time data.

Under this new framework, the first non-farm payroll report (NFP) following the geopolitical truce and the opening of the Taiwan Strait has become a crucial indicator that the entire market is holding its breath for:

Recalibrating Employment Data: With geopolitical tensions easing and lower supply chain costs for businesses, coupled with a surge in short-term service sector hiring spurred by the World Cup, the upcoming non-farm payroll data will directly reveal the true state of the US labor market, and may at least signal a peak.

Wage growth may have peaked: The mainstream market expectation is that with the recovery of supply chains and the lagged suppression of the real economy by high interest rates, the year-on-year wage growth in the United States is very likely to show a "peak and decline" signal in this data.

Once it is confirmed that wage growth has peaked, it will mean that the "wage-inflation spiral" of core inflation in the United States has been broken, and the Fed's data-driven interest rate cuts will be completely tilted.

A ripple effect: Expectations of Bank of Japan intervention and the fate of US stocks.

Given the shift in the Federal Reserve's framework and the fact that the yen has hit a 40-year low, expectations for market intervention by the Japanese government (Ministry of Finance and Bank of Japan) have reached their maximum.

Although Japan has historically intervened by selling hundreds of billions of dollars worth of US Treasury bonds and buying yen, this has been insufficient to have a sustained and substantial impact on US Treasury yields, given the massive size of the US national debt.

However, its potential "deterrent effect" on the US stock market should not be underestimated: the risk of a stampede in carry trade: if the Bank of Japan decisively launches strong intervention, or even coordinates with the US, when the non-farm payroll data weakens (confirming that US wages have peaked) and the dollar actively declines, the yen will experience a sharp retaliatory appreciation.

This will directly lead to a surge in financing costs for Wall Street carry trades, forcing quantitative algorithms and hedge funds to "sell off US stock assets and buy back yen to pay off debts" in a short period of time.

The plunge in US tech stocks triggered by the Bank of Japan's interest rate hike in August 2024 was a perfect preview of this mechanism.

Conclusion:

The current USD/JPY exchange rate is at a crossroads, a situation not seen in forty years.

With the global economic landscape shifting, the Federal Reserve moving towards data-driven strategies, and multiple catalysts such as geopolitical truce and the World Cup, the previous consensus of "blindly shorting the yen" has begun to loosen. This period, coupled with a weakening dollar, presents a window of opportunity with relatively low resistance to going long on the yen.

From a technical perspective, the US dollar has broken below the 5-day moving average and the midpoint of its trading range, while the Japanese yen has broken below its upward channel, both suggesting a potential trend reversal.

(US Dollar Index Daily Chart, Source: FX678)

For ordinary investors, keeping a close eye on the upcoming non-farm payroll data and wage growth indicators, and being wary of the Bank of Japan's swift actions in the foreign exchange market, will be of paramount importance in mitigating the risks of high volatility in US stocks and global assets.

(USD/JPY daily chart, source: FX678)

At 17:40 Beijing time, the US dollar index is currently at 100.99, and the US dollar/Japanese yen exchange rate is currently at 161.13/14.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.