Fed releases dovish signals; latest allocation strategies for US stocks, gold, and short-term bonds.

2026-07-07 21:52:24

New York Federal Reserve President Williams recently signaled a dovish monetary policy stance, providing a comprehensive assessment of the US economy, inflation, employment, and industry trends.

He admitted that the overall inflation level is still relatively high, but the decline in energy prices is a significant positive factor. He expects energy prices to fall further in the coming months, which will continue to drive down overall inflation. He also noted that the upward pressure on prices from tariffs has likely peaked, and the upward pressure on prices will gradually ease.

From an economic fundamentals perspective, the job market remains stable, the overall US economy is able to maintain steady growth, the AI industry investment boom will continue, and industrial expansion will continue to support the economy. Regarding monetary policy, Williams believes the current policy interest rate range is appropriate, and existing monetary policy is sufficient to achieve the dual goals of price stability and full employment.

Meanwhile, constrained by multiple market uncertainties, the Federal Reserve should not release overly clear long-term forward guidance, and there is no need for aggressive interest rate hikes in the short term. Its overall wording is dovish, which provides some support for market expectations of interest rate cuts.

BlackRock's mid-year outlook for 2026 suggests that the global economy is currently entering a scarcity cycle, and the continued expansion of industrial investment is amplifying supply constraints in many upstream categories. From this, BlackRock has extracted three core investment themes: scarce growth, sustainable income, and breaking traditional asset classifications. It advocates actively investing to uncover opportunities in scarce sectors and has a core overweight position in US stocks.

Coupled with Fed Chair Williams' latest dovish remarks, the macroeconomic environment of declining inflation, stable economy, and no tightening of monetary policy is simultaneously beneficial to multiple asset classes, including US stocks, short-duration fixed income, and precious metals. Structural opportunities across various asset classes are becoming clearer, and we can build tiered allocation portfolios based on both macroeconomic and institutional themes.

BlackRock noted that the AI industry is progressing steadily, but there are supply bottlenecks in upstream sectors such as electricity, chips, and data centers. Related companies have sufficient long-term orders and resilient profitability. However, compared to the main theme of asset allocation, AI is only a catalyst for phased growth, and there is no need to over-concentrate on the technology sector.

Funds have already priced in the long-term growth dividends of the industry, and the S&P 500 index surged earlier, achieving its best quarterly performance in six years.

There's no need for aggressive, heavy investment in technology-related assets. A moderate allocation to upstream hardware stocks is sufficient; there's no need to chase after hyped-up downstream application themes.

The fundamentals supporting US stock earnings are very solid, with the S&P 500's second-quarter earnings expected to grow by 23% year-on-year, marking the seventh consecutive quarter of double-digit growth.

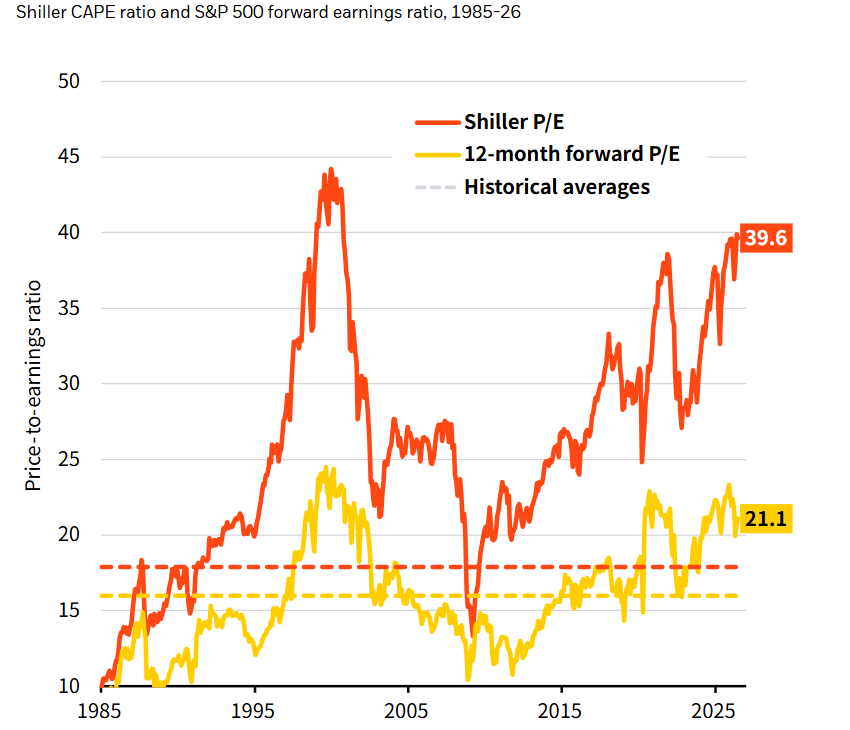

Despite Shiller's price-to-earnings ratio rising to a high of 40 times during the dot-com bubble, the 12-month forward price-to-earnings ratio is only 21 times, with rising earnings diluting valuation pressures; the incremental profit margins of the technology industry chain are better than the market average, which can continuously increase corporate earnings.

(Growth expectations and valuations are rising in tandem, digesting some of the valuation bubble)

In contrast, Europe, the UK, and Japan lack high-growth industries and have insufficient growth elasticity, making them only suitable for neutral allocation.

Williams believes that the continued decline in energy prices will continue to lower inflation, the price shock from tariffs has peaked, high inflationary pressures will gradually ease, and at the same time, stable employment, steady economic operation, and continued industrial investment will support the real economy.

The current level of monetary policy is in line with policy objectives. Given multiple uncertainties, no strong tightening guidance will be given, and the probability of a significant interest rate hike has decreased significantly.

This relatively loose macroeconomic environment directly benefits three types of core assets: First, US stocks on the equity side, which are supported by the expectation of interest rate cuts and the resilience of corporate profits.

Second, for short- and medium-term bonds, inflation has fallen and expectations of interest rate hikes have cooled, reducing upward pressure on interest rates. However, long-duration bonds remain highly sensitive to interest rates, making short-duration yield bonds more cost-effective.

Third, precious metals, represented by gold, are seeing their value rise due to expectations of declining real interest rates, global geopolitical uncertainties, and demand for safe-haven currencies. This combination can hedge against equity market volatility and enhance the portfolio's hedging capabilities.

Two supporting investment themes and asset allocation strategies

With global bond yields remaining high, the value of income-generating assets is becoming increasingly apparent.

Prioritize allocation to short- and medium-term Eurozone government bonds, while also investing in public and private credit products with stable cash flow; avoid highly volatile long-term bonds, as long-term bond interest rate fluctuations pose a high risk and have a weak hedging effect.

The credit market requires careful selection, allocating only to targets with clear cash flow, sound debt protection, and high recovery value, while avoiding credit assets with weak fundamentals.

In the realm of precious metals, gold is a supplementary asset that combines the attributes of preserving value and hedging. During periods of peaking and declining interest rates, gold prices have medium- to long-term upside potential and can be used as a base holding for diversified portfolio allocation to hedge against risks arising from stock market corrections and geopolitical conflicts.

The traditional simplistic classification of stocks, bonds, and alternative assets is no longer suitable for the current market. Investment should first identify industry themes and risk exposures, and then select suitable investment tools. Infrastructure assets are a typical example, as they can meet the supporting needs of various industries, provide long-term stable cash flow, and have both growth and return attributes. Precious metals such as gold are independent of the traditional stock and bond cycles and are excellent cross-cycle hedging tools.

A clear tactical allocation framework is defined by asset class: on the equity side, US stocks are overweighted, while European, UK, and Japanese stocks are maintained at a neutral level, and the technology sector is moderately diversified without heavy holdings; on the fixed income side, the focus is on short- and medium-term government bonds; on the credit side, the focus is on selecting high-quality targets and strictly controlling creditworthiness; on alternative assets, gold and infrastructure are allocated slightly to hedge against portfolio volatility.

Combining BlackRock's 2026 mid-year scarcity cycle investment framework with the latest dovish remarks from Fed Chair Williams, the core market logic resonates: the scarcity logic supports the resilience of US stock earnings, inflation is falling, and the expectation of easing as the rate hike cycle nears its end is also favorable for short-duration bonds and gold and precious metals. The market as a whole is mainly driven by structural opportunities, and there is no possibility of a broad-based rally or a systemic crash.

The core strategy is to balance growth, fixed income, and safe-haven assets, with US stocks as the core equity, short-term bonds to stabilize cash flow, and gold to hedge tail risks. The strategy involves actively selecting targets and abandoning the passive allocation approach of heavy investment in a single sector.

He admitted that the overall inflation level is still relatively high, but the decline in energy prices is a significant positive factor. He expects energy prices to fall further in the coming months, which will continue to drive down overall inflation. He also noted that the upward pressure on prices from tariffs has likely peaked, and the upward pressure on prices will gradually ease.

From an economic fundamentals perspective, the job market remains stable, the overall US economy is able to maintain steady growth, the AI industry investment boom will continue, and industrial expansion will continue to support the economy. Regarding monetary policy, Williams believes the current policy interest rate range is appropriate, and existing monetary policy is sufficient to achieve the dual goals of price stability and full employment.

Meanwhile, constrained by multiple market uncertainties, the Federal Reserve should not release overly clear long-term forward guidance, and there is no need for aggressive interest rate hikes in the short term. Its overall wording is dovish, which provides some support for market expectations of interest rate cuts.

Institutional Allocation Views

BlackRock's mid-year outlook for 2026 suggests that the global economy is currently entering a scarcity cycle, and the continued expansion of industrial investment is amplifying supply constraints in many upstream categories. From this, BlackRock has extracted three core investment themes: scarce growth, sustainable income, and breaking traditional asset classifications. It advocates actively investing to uncover opportunities in scarce sectors and has a core overweight position in US stocks.

Coupled with Fed Chair Williams' latest dovish remarks, the macroeconomic environment of declining inflation, stable economy, and no tightening of monetary policy is simultaneously beneficial to multiple asset classes, including US stocks, short-duration fixed income, and precious metals. Structural opportunities across various asset classes are becoming clearer, and we can build tiered allocation portfolios based on both macroeconomic and institutional themes.

BlackRock noted that the AI industry is progressing steadily, but there are supply bottlenecks in upstream sectors such as electricity, chips, and data centers. Related companies have sufficient long-term orders and resilient profitability. However, compared to the main theme of asset allocation, AI is only a catalyst for phased growth, and there is no need to over-concentrate on the technology sector.

Funds have already priced in the long-term growth dividends of the industry, and the S&P 500 index surged earlier, achieving its best quarterly performance in six years.

There's no need for aggressive, heavy investment in technology-related assets. A moderate allocation to upstream hardware stocks is sufficient; there's no need to chase after hyped-up downstream application themes.

The fundamentals supporting US stock earnings are very solid, with the S&P 500's second-quarter earnings expected to grow by 23% year-on-year, marking the seventh consecutive quarter of double-digit growth.

Despite Shiller's price-to-earnings ratio rising to a high of 40 times during the dot-com bubble, the 12-month forward price-to-earnings ratio is only 21 times, with rising earnings diluting valuation pressures; the incremental profit margins of the technology industry chain are better than the market average, which can continuously increase corporate earnings.

(Growth expectations and valuations are rising in tandem, digesting some of the valuation bubble)

In contrast, Europe, the UK, and Japan lack high-growth industries and have insufficient growth elasticity, making them only suitable for neutral allocation.

Favorable Macroeconomic Environment: Williams' Dovish Stance Broadens the Range of Beneficial Assets

Williams believes that the continued decline in energy prices will continue to lower inflation, the price shock from tariffs has peaked, high inflationary pressures will gradually ease, and at the same time, stable employment, steady economic operation, and continued industrial investment will support the real economy.

The current level of monetary policy is in line with policy objectives. Given multiple uncertainties, no strong tightening guidance will be given, and the probability of a significant interest rate hike has decreased significantly.

This relatively loose macroeconomic environment directly benefits three types of core assets: First, US stocks on the equity side, which are supported by the expectation of interest rate cuts and the resilience of corporate profits.

Second, for short- and medium-term bonds, inflation has fallen and expectations of interest rate hikes have cooled, reducing upward pressure on interest rates. However, long-duration bonds remain highly sensitive to interest rates, making short-duration yield bonds more cost-effective.

Third, precious metals, represented by gold, are seeing their value rise due to expectations of declining real interest rates, global geopolitical uncertainties, and demand for safe-haven currencies. This combination can hedge against equity market volatility and enhance the portfolio's hedging capabilities.

Two supporting investment themes and asset allocation strategies

With global bond yields remaining high, the value of income-generating assets is becoming increasingly apparent.

Prioritize allocation to short- and medium-term Eurozone government bonds, while also investing in public and private credit products with stable cash flow; avoid highly volatile long-term bonds, as long-term bond interest rate fluctuations pose a high risk and have a weak hedging effect.

The credit market requires careful selection, allocating only to targets with clear cash flow, sound debt protection, and high recovery value, while avoiding credit assets with weak fundamentals.

In the realm of precious metals, gold is a supplementary asset that combines the attributes of preserving value and hedging. During periods of peaking and declining interest rates, gold prices have medium- to long-term upside potential and can be used as a base holding for diversified portfolio allocation to hedge against risks arising from stock market corrections and geopolitical conflicts.

The traditional simplistic classification of stocks, bonds, and alternative assets is no longer suitable for the current market. Investment should first identify industry themes and risk exposures, and then select suitable investment tools. Infrastructure assets are a typical example, as they can meet the supporting needs of various industries, provide long-term stable cash flow, and have both growth and return attributes. Precious metals such as gold are independent of the traditional stock and bond cycles and are excellent cross-cycle hedging tools.

A clear tactical allocation framework is defined by asset class: on the equity side, US stocks are overweighted, while European, UK, and Japanese stocks are maintained at a neutral level, and the technology sector is moderately diversified without heavy holdings; on the fixed income side, the focus is on short- and medium-term government bonds; on the credit side, the focus is on selecting high-quality targets and strictly controlling creditworthiness; on alternative assets, gold and infrastructure are allocated slightly to hedge against portfolio volatility.

Summarize

Combining BlackRock's 2026 mid-year scarcity cycle investment framework with the latest dovish remarks from Fed Chair Williams, the core market logic resonates: the scarcity logic supports the resilience of US stock earnings, inflation is falling, and the expectation of easing as the rate hike cycle nears its end is also favorable for short-duration bonds and gold and precious metals. The market as a whole is mainly driven by structural opportunities, and there is no possibility of a broad-based rally or a systemic crash.

The core strategy is to balance growth, fixed income, and safe-haven assets, with US stocks as the core equity, short-term bonds to stabilize cash flow, and gold to hedge tail risks. The strategy involves actively selecting targets and abandoning the passive allocation approach of heavy investment in a single sector.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.