A chart shows that Capesize freight rates remain weak, and the Baltic Dry Index continues its downward trend.

2026-07-17 00:32:12

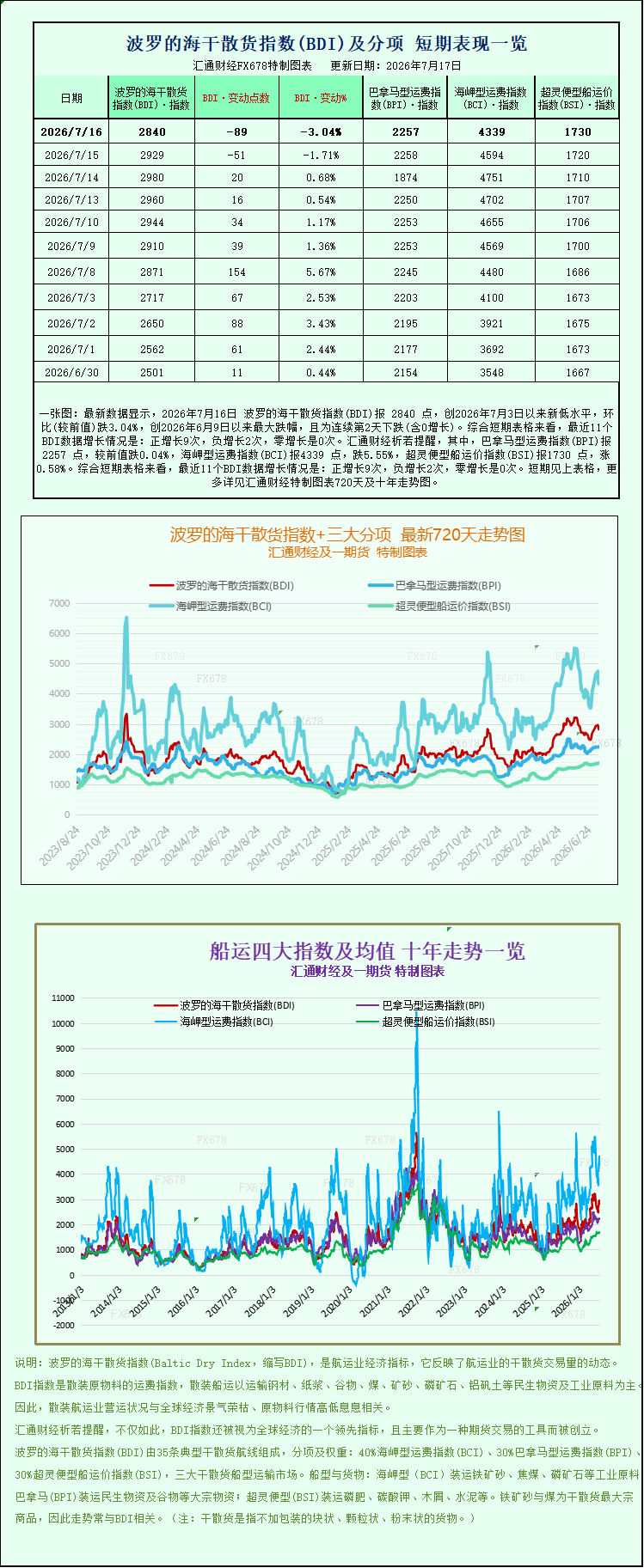

Latest data shows that the Baltic Dry Index (BDI) closed at 2840 points on July 16, 2026, a new low since July 3, 2026, down 3.04% month-on-month, the largest drop since June 9, 2026, and marking the second consecutive day of decline (including zero growth). Looking at the short-term charts, the BDI has seen positive growth 9 times, negative growth 2 times, and zero growth in the last 11 data points. Specifically, the Panamax Freight Index (BPI) closed at 2257 points, down 0.04% from the previous value; the Capesize Freight Index (BCI) closed at 4339 points, down 5.55%; and the Supramax Freight Index (BSI) closed at 1730 points, up 0.58%. For detailed charts of the latest 720-day and 10-year trends of the Baltic Dry Index and its three main sub-indices, please refer to the charts specially created by FX678.  On Thursday, the Baltic Dry Index (BADI), a key indicator of the global shipping market, continued its downward trend, marking its second consecutive day of decline. The main drag on this correction was a significant weakening of Capesize bulk carrier freight rates, with sluggish demand for large vessels completely dominating short-term market movements. By the close of trading, the composite index and the sub-ship type indices showed a clear divergence, with freight rates for large dry bulk carriers falling sharply, while freight rates for small and medium-sized vessels bucked the trend and rose slightly, reflecting the current structurally uneven market characteristics of global dry bulk trade. Data shows that the Baltic Dry Index, which tracks freight rates for the three major dry bulk carrier types—Capesma, Panamax, and Supramax—fell sharply by 89 points, a 3% drop, closing at 2840 points, its lowest level in nearly ten days since July 6th. This continuous decline also ended the index's previous period of consolidation. Looking at the data from different ship types, the market is highly differentiated. Large vessels transporting bulk raw materials are facing significant pressure on freight rates, while smaller vessels are bucking the trend and rising due to regional trade demand. As the ship type with the highest index weighting and most sensitive to bulk raw material trade, Capesize vessels were the core drag on the index this time. The Capesize index fell sharply by 255 points, a drop of 5.6%, closing at 4339 points, a new low in over a week, far exceeding the decline of other ship types. In terms of specific operating revenue, Capesize vessels, mainly transporting ultra-large industrial raw materials such as iron ore and coal (150,000 tons), saw a significant drop in average daily earnings, with daily revenue decreasing by $2314 compared to the previous day, ultimately settling at $35849, indicating a continued contraction in the profit margins of large vessels. Industry analysts point out that Capesize vessels account for nearly 40% of the Baltic Dry Index, and their freight rate fluctuations have a decisive impact on the overall index trend. This round of sharp drops in large vessel freight rates is the core trigger for the deep correction in the index. The medium-sized vessel market remained generally stable with minimal fluctuations. Data shows that the Panamax index fell only slightly by 1 point, a decrease of 0.04%, almost unchanged from the previous trading day, closing at 2257 points. For Panamax vessels primarily transporting 60,000 to 70,000 tons of bulk commodities such as coal and grain, the average daily earnings decreased slightly by $9, ultimately closing at $20,316. The overall operating trend remained stable, with no significant supply-demand imbalance, and its drag on the composite index was negligible. In contrast, the small dry bulk vessel market showed a stark contrast in performance, becoming a bright spot in the current shipping market. The Supramax index rose 10 points, an increase of 0.6%, closing at 1730 points, a nearly four-year high since August 2022. The rise in freight rates for small vessels bucked the trend, primarily driven by stable demand in regional short-haul bulk cargo trade, niche building materials, and agricultural product transportation. This, coupled with the flexible allocation of small vessel capacity and a tight regional supply-demand balance, supported the continued increase in freight rates, fully reflecting the structural divergence in the current dry bulk shipping market: weakening demand for large vessels and robust demand for small vessels. From the perspective of upstream commodity fundamentals, the core reason for weak ocean freight demand lies in the slowdown in iron ore trade and intensified market competition between bulls and bears. Currently, global iron ore prices are experiencing limited fluctuations and remain relatively stable, with traders and shipping professionals continuously weighing multiple complex factors. On the one hand, major global iron ore producers are steadily increasing their production capacity, leading to an overall increase in market supply. On the other hand, as the world's largest iron ore consumer, China is currently in its traditional off-season for industry, with downstream steel industry demand slowing down and steel mills showing weak purchasing intentions. This directly resulted in a significant reduction in iron ore cargoes for ocean shipping, suppressing demand for Capesize vessels. Meanwhile, the ongoing strike by workers at BHP Billiton's Port Hedland in Australia poses a risk of disruption to port operations, creating uncertainty in the iron ore supply chain and fueling market caution, further suppressing short-term shipping activity. Overall, the recent decline in the Baltic Dry Index is a result of multiple factors, including a short-term off-season for demand, a slowdown in bulk commodity trade, and a mismatch between supply and demand for shipping capacity. The current dry bulk shipping market exhibits a clear structural divergence, with the large-scale industrial raw material transportation market continuing to weaken, while the small and medium-sized bulk regional trade market remains resilient. Industry analysts believe that in the short term, with the traditional off-season for domestic steel production continuing and the pace of bulk commodity shipments slowing, Capesize freight rates may continue to fluctuate weakly, and the Baltic Dry Index will still face downward pressure. The medium- to long-term trend will depend on the pace of recovery in Chinese industrial demand, the stability of the global mineral supply chain, and changes in dry bulk vessel capacity deployment.

On Thursday, the Baltic Dry Index (BADI), a key indicator of the global shipping market, continued its downward trend, marking its second consecutive day of decline. The main drag on this correction was a significant weakening of Capesize bulk carrier freight rates, with sluggish demand for large vessels completely dominating short-term market movements. By the close of trading, the composite index and the sub-ship type indices showed a clear divergence, with freight rates for large dry bulk carriers falling sharply, while freight rates for small and medium-sized vessels bucked the trend and rose slightly, reflecting the current structurally uneven market characteristics of global dry bulk trade. Data shows that the Baltic Dry Index, which tracks freight rates for the three major dry bulk carrier types—Capesma, Panamax, and Supramax—fell sharply by 89 points, a 3% drop, closing at 2840 points, its lowest level in nearly ten days since July 6th. This continuous decline also ended the index's previous period of consolidation. Looking at the data from different ship types, the market is highly differentiated. Large vessels transporting bulk raw materials are facing significant pressure on freight rates, while smaller vessels are bucking the trend and rising due to regional trade demand. As the ship type with the highest index weighting and most sensitive to bulk raw material trade, Capesize vessels were the core drag on the index this time. The Capesize index fell sharply by 255 points, a drop of 5.6%, closing at 4339 points, a new low in over a week, far exceeding the decline of other ship types. In terms of specific operating revenue, Capesize vessels, mainly transporting ultra-large industrial raw materials such as iron ore and coal (150,000 tons), saw a significant drop in average daily earnings, with daily revenue decreasing by $2314 compared to the previous day, ultimately settling at $35849, indicating a continued contraction in the profit margins of large vessels. Industry analysts point out that Capesize vessels account for nearly 40% of the Baltic Dry Index, and their freight rate fluctuations have a decisive impact on the overall index trend. This round of sharp drops in large vessel freight rates is the core trigger for the deep correction in the index. The medium-sized vessel market remained generally stable with minimal fluctuations. Data shows that the Panamax index fell only slightly by 1 point, a decrease of 0.04%, almost unchanged from the previous trading day, closing at 2257 points. For Panamax vessels primarily transporting 60,000 to 70,000 tons of bulk commodities such as coal and grain, the average daily earnings decreased slightly by $9, ultimately closing at $20,316. The overall operating trend remained stable, with no significant supply-demand imbalance, and its drag on the composite index was negligible. In contrast, the small dry bulk vessel market showed a stark contrast in performance, becoming a bright spot in the current shipping market. The Supramax index rose 10 points, an increase of 0.6%, closing at 1730 points, a nearly four-year high since August 2022. The rise in freight rates for small vessels bucked the trend, primarily driven by stable demand in regional short-haul bulk cargo trade, niche building materials, and agricultural product transportation. This, coupled with the flexible allocation of small vessel capacity and a tight regional supply-demand balance, supported the continued increase in freight rates, fully reflecting the structural divergence in the current dry bulk shipping market: weakening demand for large vessels and robust demand for small vessels. From the perspective of upstream commodity fundamentals, the core reason for weak ocean freight demand lies in the slowdown in iron ore trade and intensified market competition between bulls and bears. Currently, global iron ore prices are experiencing limited fluctuations and remain relatively stable, with traders and shipping professionals continuously weighing multiple complex factors. On the one hand, major global iron ore producers are steadily increasing their production capacity, leading to an overall increase in market supply. On the other hand, as the world's largest iron ore consumer, China is currently in its traditional off-season for industry, with downstream steel industry demand slowing down and steel mills showing weak purchasing intentions. This directly resulted in a significant reduction in iron ore cargoes for ocean shipping, suppressing demand for Capesize vessels. Meanwhile, the ongoing strike by workers at BHP Billiton's Port Hedland in Australia poses a risk of disruption to port operations, creating uncertainty in the iron ore supply chain and fueling market caution, further suppressing short-term shipping activity. Overall, the recent decline in the Baltic Dry Index is a result of multiple factors, including a short-term off-season for demand, a slowdown in bulk commodity trade, and a mismatch between supply and demand for shipping capacity. The current dry bulk shipping market exhibits a clear structural divergence, with the large-scale industrial raw material transportation market continuing to weaken, while the small and medium-sized bulk regional trade market remains resilient. Industry analysts believe that in the short term, with the traditional off-season for domestic steel production continuing and the pace of bulk commodity shipments slowing, Capesize freight rates may continue to fluctuate weakly, and the Baltic Dry Index will still face downward pressure. The medium- to long-term trend will depend on the pace of recovery in Chinese industrial demand, the stability of the global mineral supply chain, and changes in dry bulk vessel capacity deployment.

On Thursday, the Baltic Dry Index (BADI), a key indicator of the global shipping market, continued its downward trend, marking its second consecutive day of decline. The main drag on this correction was a significant weakening of Capesize bulk carrier freight rates, with sluggish demand for large vessels completely dominating short-term market movements. By the close of trading, the composite index and the sub-ship type indices showed a clear divergence, with freight rates for large dry bulk carriers falling sharply, while freight rates for small and medium-sized vessels bucked the trend and rose slightly, reflecting the current structurally uneven market characteristics of global dry bulk trade. Data shows that the Baltic Dry Index, which tracks freight rates for the three major dry bulk carrier types—Capesma, Panamax, and Supramax—fell sharply by 89 points, a 3% drop, closing at 2840 points, its lowest level in nearly ten days since July 6th. This continuous decline also ended the index's previous period of consolidation. Looking at the data from different ship types, the market is highly differentiated. Large vessels transporting bulk raw materials are facing significant pressure on freight rates, while smaller vessels are bucking the trend and rising due to regional trade demand. As the ship type with the highest index weighting and most sensitive to bulk raw material trade, Capesize vessels were the core drag on the index this time. The Capesize index fell sharply by 255 points, a drop of 5.6%, closing at 4339 points, a new low in over a week, far exceeding the decline of other ship types. In terms of specific operating revenue, Capesize vessels, mainly transporting ultra-large industrial raw materials such as iron ore and coal (150,000 tons), saw a significant drop in average daily earnings, with daily revenue decreasing by $2314 compared to the previous day, ultimately settling at $35849, indicating a continued contraction in the profit margins of large vessels. Industry analysts point out that Capesize vessels account for nearly 40% of the Baltic Dry Index, and their freight rate fluctuations have a decisive impact on the overall index trend. This round of sharp drops in large vessel freight rates is the core trigger for the deep correction in the index. The medium-sized vessel market remained generally stable with minimal fluctuations. Data shows that the Panamax index fell only slightly by 1 point, a decrease of 0.04%, almost unchanged from the previous trading day, closing at 2257 points. For Panamax vessels primarily transporting 60,000 to 70,000 tons of bulk commodities such as coal and grain, the average daily earnings decreased slightly by $9, ultimately closing at $20,316. The overall operating trend remained stable, with no significant supply-demand imbalance, and its drag on the composite index was negligible. In contrast, the small dry bulk vessel market showed a stark contrast in performance, becoming a bright spot in the current shipping market. The Supramax index rose 10 points, an increase of 0.6%, closing at 1730 points, a nearly four-year high since August 2022. The rise in freight rates for small vessels bucked the trend, primarily driven by stable demand in regional short-haul bulk cargo trade, niche building materials, and agricultural product transportation. This, coupled with the flexible allocation of small vessel capacity and a tight regional supply-demand balance, supported the continued increase in freight rates, fully reflecting the structural divergence in the current dry bulk shipping market: weakening demand for large vessels and robust demand for small vessels. From the perspective of upstream commodity fundamentals, the core reason for weak ocean freight demand lies in the slowdown in iron ore trade and intensified market competition between bulls and bears. Currently, global iron ore prices are experiencing limited fluctuations and remain relatively stable, with traders and shipping professionals continuously weighing multiple complex factors. On the one hand, major global iron ore producers are steadily increasing their production capacity, leading to an overall increase in market supply. On the other hand, as the world's largest iron ore consumer, China is currently in its traditional off-season for industry, with downstream steel industry demand slowing down and steel mills showing weak purchasing intentions. This directly resulted in a significant reduction in iron ore cargoes for ocean shipping, suppressing demand for Capesize vessels. Meanwhile, the ongoing strike by workers at BHP Billiton's Port Hedland in Australia poses a risk of disruption to port operations, creating uncertainty in the iron ore supply chain and fueling market caution, further suppressing short-term shipping activity. Overall, the recent decline in the Baltic Dry Index is a result of multiple factors, including a short-term off-season for demand, a slowdown in bulk commodity trade, and a mismatch between supply and demand for shipping capacity. The current dry bulk shipping market exhibits a clear structural divergence, with the large-scale industrial raw material transportation market continuing to weaken, while the small and medium-sized bulk regional trade market remains resilient. Industry analysts believe that in the short term, with the traditional off-season for domestic steel production continuing and the pace of bulk commodity shipments slowing, Capesize freight rates may continue to fluctuate weakly, and the Baltic Dry Index will still face downward pressure. The medium- to long-term trend will depend on the pace of recovery in Chinese industrial demand, the stability of the global mineral supply chain, and changes in dry bulk vessel capacity deployment.- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.