With the trade deficit unchanged and the objectives unfulfilled, who is ultimately benefiting from this tariff drama?

2026-02-24 21:40:42

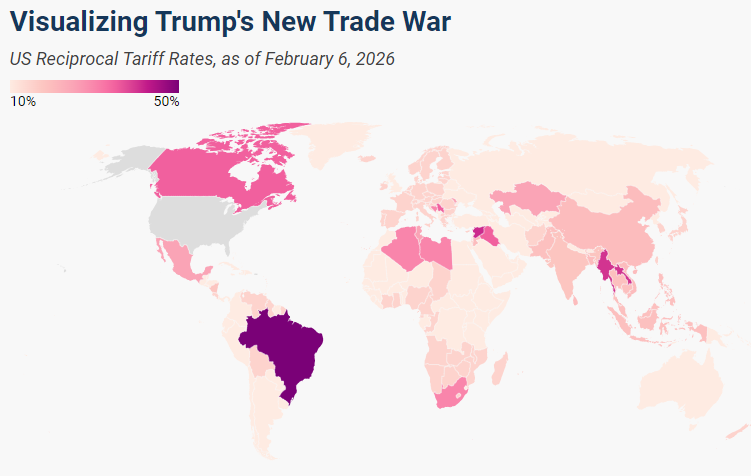

Since 2025, the Trump administration has continued to push forward with tough tariff policies. First, it imposed tariffs on major trading partners such as China, Canada, Mexico, and the European Union based on the International Emergency Economic Powers Act (IEEPA). At the same time, it implemented or threatened to implement tariff measures on multiple categories of goods, including automobiles, heavy trucks, steel, aluminum, timber, furniture, semiconductors, pharmaceuticals, and copper, based on Section 232 of the Trade Expansion Act of 1962.

These tariff policies have faced significant challenges at the judicial level.

The U.S. Supreme Court recently issued key rulings in two cases, Learning Resources Inc. v. Trump and VOS Selections v. United States, by a 6-3 vote, clarifying that the International Emergency Economic Powers Act does not grant the president the legal authority to impose tariffs.

In response to the judicial ruling, the Trump administration quickly activated its alternative plan, signing an executive order under Section 122 of the Trade Act of 1974 to impose a 10% tariff on all imported goods worldwide (with some categories exempted), and raising the tariff to 15% on February 21, 2026. The tariff officially took effect on February 24, with an implementation period of 150 days, covering approximately $1.2 trillion in annual imports, accounting for 34% of total U.S. imports.

The new round of tariff policies has been implemented, directly raising the level of tariffs levied by the United States on the vast majority of imported goods.

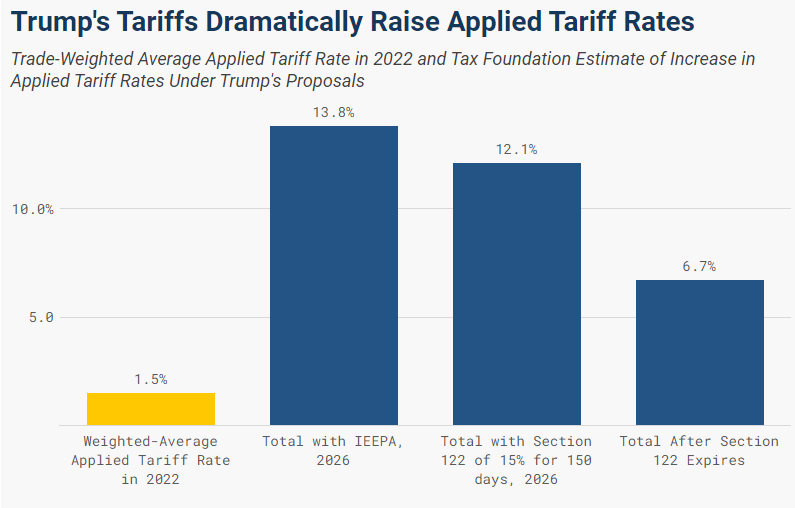

World Bank statistics show that the weighted average applicable tariff rate in the United States was only 1.5% in 2022; before the IEEPA tariffs were judicially repealed, this rate had rapidly risen to 13.8%. During the implementation phase of the Section 122 tariffs, the weighted average applicable tariff rate for US imports is expected to remain at 12.1%, and will fall back to 6.7% after the temporary tariffs expire.

(Weighted average tariff rate at different stages)

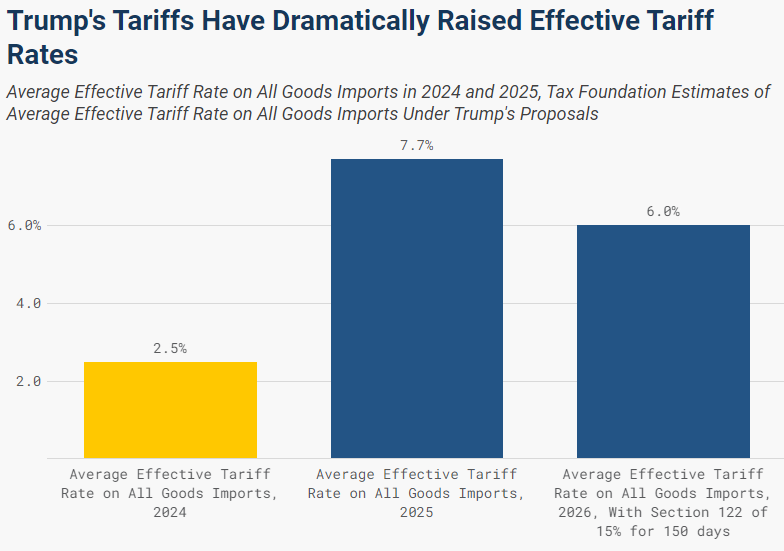

It is important to clarify that there is a fundamental difference between the weighted average applicable tariff rate and the average effective tariff rate: the former is the statutory tax standard for goods from different countries and categories, while the latter is calculated based on the proportion of actual tariff revenue to the total import value of goods, and thus better reflects the true tax burden.

Before the IEEPA tariffs are ruled illegal in 2025, the average effective tariff rate in the United States will rise sharply from 2.4% in 2024 to 7.7%, a new peak since 1947. If the 15% tariff under Section 122 is terminated as scheduled in 150 days, the average effective tariff rate in the United States in 2026 is expected to be 6.0%, still the highest level since 1971.

(Average effective tax rate in the United States at different stages)

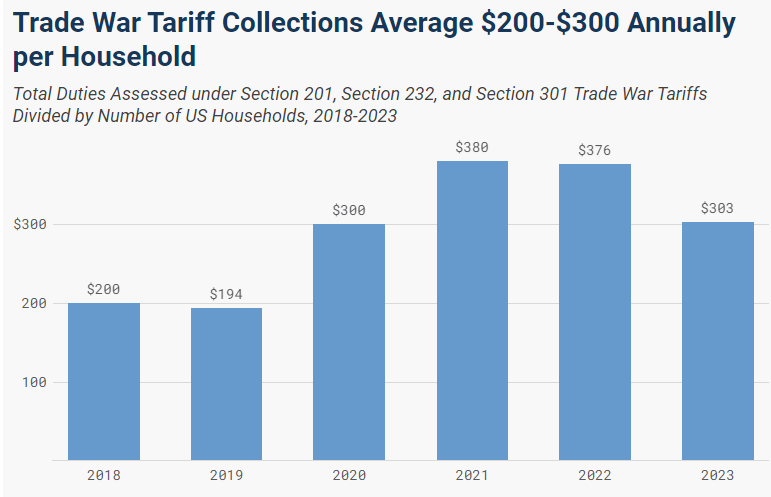

Tariff policies directly translate into a real burden on American families. By 2025, Trump's tariff package will directly increase the average annual tax burden on American families by $1,000.

After the IEEPA tariffs were ruled illegal, the remaining Section 232 tariffs will increase the average household tax burden by $400 in 2026. Combined with the new tariffs under Section 122, the burden on American households will increase by another $300-$700.

(Household tax burden before the US launched a global tariff war)

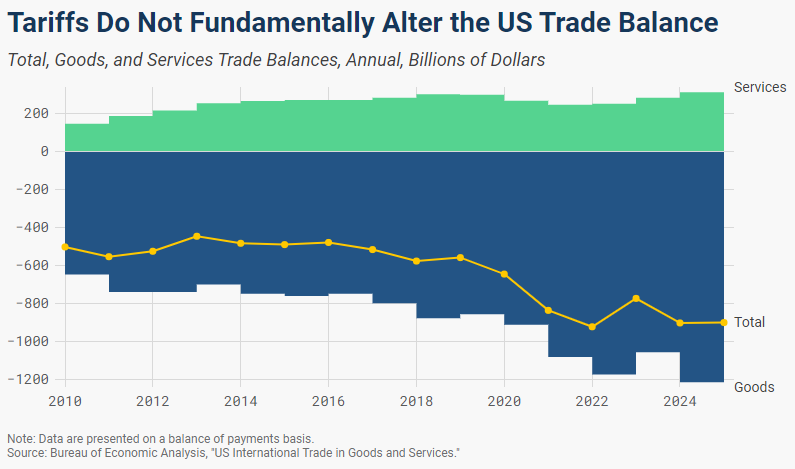

One of the core objectives of the Trump administration's tariff policy was to narrow the U.S. trade deficit.

However, from the perspective of macroeconomics and foreign exchange transactions, a country's trade balance is not simply driven by trade policy; it is essentially the result of macroeconomic equilibrium between domestic savings and investment, and net cross-border lending.

The United States has a persistently higher domestic investment demand than savings capacity, and must rely on foreign capital inflows to fill the funding gap. Tariff policies cannot directly change the domestic savings-investment balance, and therefore it is difficult to reverse the trade balance structure in the long run.

Since the United States recorded its last trade surplus in 1975, it has maintained a trade deficit for many years. This is not a short-term, obvious economic risk, but rather reflects, to some extent, global capital's confidence in the US economy, and is a manifestation of its status as a safe haven and core investment target for global capital.

The US trade deficit in 2025 will narrow by only $2.1 billion compared to 2024. The slight decline in the overall deficit will rely entirely on the expansion of the service trade surplus. In contrast, the goods trade deficit will increase by $25.5 billion year-on-year. Tariffs have not achieved the core goal of improving the trade balance.

(Trend chart of US terms of trade and trade deficit)

On January 20, 2025, Trump signed an executive order requiring relevant cabinet departments to research trade rules and submit tariff policy recommendations by April 1.

Subsequently, the U.S. proceeded with the implementation of several new tariffs and investigation procedures, while at least five lawsuits challenged the legality of the tariff executive order.

To date, the judiciary has not recognized the Trump administration's claim for unlimited emergency tariffs, but the executive branch has quickly initiated appeals against the relevant rulings, and the battle between policy and the judiciary will continue.

In terms of long-term impact, historical experience and empirical studies have repeatedly confirmed that tariffs are essentially a domestic tax burden, which will increase business costs and consumer prices, compress the supply of goods and services, and ultimately lead to a reduction in residents' income, fewer jobs, and a decline in economic output.

Although the current round of US tariff policies has maintained high tariff levels in the short term after judicial adjustments, it has failed to achieve its core policy objectives. Its subsequent implementation effects and overseas countermeasures will continue to disrupt the US economy and global foreign exchange and commodity markets.

(Global Tariff Level Map)

(US Dollar Index Monthly Chart, Source: FX678)

These tariff policies have faced significant challenges at the judicial level.

The U.S. Supreme Court recently issued key rulings in two cases, Learning Resources Inc. v. Trump and VOS Selections v. United States, by a 6-3 vote, clarifying that the International Emergency Economic Powers Act does not grant the president the legal authority to impose tariffs.

In response to the judicial ruling, the Trump administration quickly activated its alternative plan, signing an executive order under Section 122 of the Trade Act of 1974 to impose a 10% tariff on all imported goods worldwide (with some categories exempted), and raising the tariff to 15% on February 21, 2026. The tariff officially took effect on February 24, with an implementation period of 150 days, covering approximately $1.2 trillion in annual imports, accounting for 34% of total U.S. imports.

Tariff rates have increased significantly, and there are significant differences between the two statistical methods.

The new round of tariff policies has been implemented, directly raising the level of tariffs levied by the United States on the vast majority of imported goods.

World Bank statistics show that the weighted average applicable tariff rate in the United States was only 1.5% in 2022; before the IEEPA tariffs were judicially repealed, this rate had rapidly risen to 13.8%. During the implementation phase of the Section 122 tariffs, the weighted average applicable tariff rate for US imports is expected to remain at 12.1%, and will fall back to 6.7% after the temporary tariffs expire.

(Weighted average tariff rate at different stages)

It is important to clarify that there is a fundamental difference between the weighted average applicable tariff rate and the average effective tariff rate: the former is the statutory tax standard for goods from different countries and categories, while the latter is calculated based on the proportion of actual tariff revenue to the total import value of goods, and thus better reflects the true tax burden.

Before the IEEPA tariffs are ruled illegal in 2025, the average effective tariff rate in the United States will rise sharply from 2.4% in 2024 to 7.7%, a new peak since 1947. If the 15% tariff under Section 122 is terminated as scheduled in 150 days, the average effective tariff rate in the United States in 2026 is expected to be 6.0%, still the highest level since 1971.

(Average effective tax rate in the United States at different stages)

Household tax burden and fiscal revenue are under dual pressure

Tariff policies directly translate into a real burden on American families. By 2025, Trump's tariff package will directly increase the average annual tax burden on American families by $1,000.

After the IEEPA tariffs were ruled illegal, the remaining Section 232 tariffs will increase the average household tax burden by $400 in 2026. Combined with the new tariffs under Section 122, the burden on American households will increase by another $300-$700.

(Household tax burden before the US launched a global tariff war)

The trade balance has not changed the long-term pattern, and policy objectives have failed to materialize.

One of the core objectives of the Trump administration's tariff policy was to narrow the U.S. trade deficit.

However, from the perspective of macroeconomics and foreign exchange transactions, a country's trade balance is not simply driven by trade policy; it is essentially the result of macroeconomic equilibrium between domestic savings and investment, and net cross-border lending.

The United States has a persistently higher domestic investment demand than savings capacity, and must rely on foreign capital inflows to fill the funding gap. Tariff policies cannot directly change the domestic savings-investment balance, and therefore it is difficult to reverse the trade balance structure in the long run.

Since the United States recorded its last trade surplus in 1975, it has maintained a trade deficit for many years. This is not a short-term, obvious economic risk, but rather reflects, to some extent, global capital's confidence in the US economy, and is a manifestation of its status as a safe haven and core investment target for global capital.

The US trade deficit in 2025 will narrow by only $2.1 billion compared to 2024. The slight decline in the overall deficit will rely entirely on the expansion of the service trade surplus. In contrast, the goods trade deficit will increase by $25.5 billion year-on-year. Tariffs have not achieved the core goal of improving the trade balance.

(Trend chart of US terms of trade and trade deficit)

Policy advancement and judicial battles continue

On January 20, 2025, Trump signed an executive order requiring relevant cabinet departments to research trade rules and submit tariff policy recommendations by April 1.

Subsequently, the U.S. proceeded with the implementation of several new tariffs and investigation procedures, while at least five lawsuits challenged the legality of the tariff executive order.

To date, the judiciary has not recognized the Trump administration's claim for unlimited emergency tariffs, but the executive branch has quickly initiated appeals against the relevant rulings, and the battle between policy and the judiciary will continue.

In terms of long-term impact, historical experience and empirical studies have repeatedly confirmed that tariffs are essentially a domestic tax burden, which will increase business costs and consumer prices, compress the supply of goods and services, and ultimately lead to a reduction in residents' income, fewer jobs, and a decline in economic output.

Although the current round of US tariff policies has maintained high tariff levels in the short term after judicial adjustments, it has failed to achieve its core policy objectives. Its subsequent implementation effects and overseas countermeasures will continue to disrupt the US economy and global foreign exchange and commodity markets.

(Global Tariff Level Map)

(US Dollar Index Monthly Chart, Source: FX678)

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.