Political factors significantly weakened the pound's momentum.

2026-02-27 22:03:15

The euro successfully held key support against the dollar, rebounding strongly from the 50-day moving average. The core driving factor was that market expectations for a June rate cut by the Federal Reserve rose again to over 50%, significantly limiting the dollar's upside potential.

More importantly, the European Central Bank's asset allocation adjustments provided strong support for the euro: data shows that the ECB reduced its holdings of US assets from $51.9 billion to $50.9 billion, while simultaneously increasing its holdings of Japanese assets. As a result, the dollar's share of global foreign exchange reserves plummeted from 83% to 78%, a change exacerbated by exchange rate volatility and the trend of de-dollarization.

Global central banks' continued diversification of their gold and foreign exchange reserves has become a core driver of the gold price surge expected in 2024-2025. Currently, the market is highly uncertain about the prospects of Trump's policies. If regulators in various countries not only use gold but also accelerate the replacement of the US dollar with other non-US currencies, the US dollar will face medium- to long-term depreciation pressure. A recent MLIV Pulse survey shows that over 70% of investors are bearish on the US dollar, predicting a significant decline starting from the end of next month.

However, the US dollar has not easily relinquished its strong position. The Federal Reserve's extended pause in interest rate cuts has provided continued policy support for the dollar; meanwhile, yields on dollar-denominated assets remain high, while competing currencies such as the euro, pound sterling, and yen all have significant fundamental weaknesses.

Tokyo's core inflation fell to 1.8% for the first time since October 2024, significantly below the Bank of Japan's policy target of 2%. This data is a key leading indicator of national inflation in Japan, directly stripping USDJPY short sellers of significant leverage and severely weakening market expectations that the Bank of Japan will raise interest rates to normalize its policy.

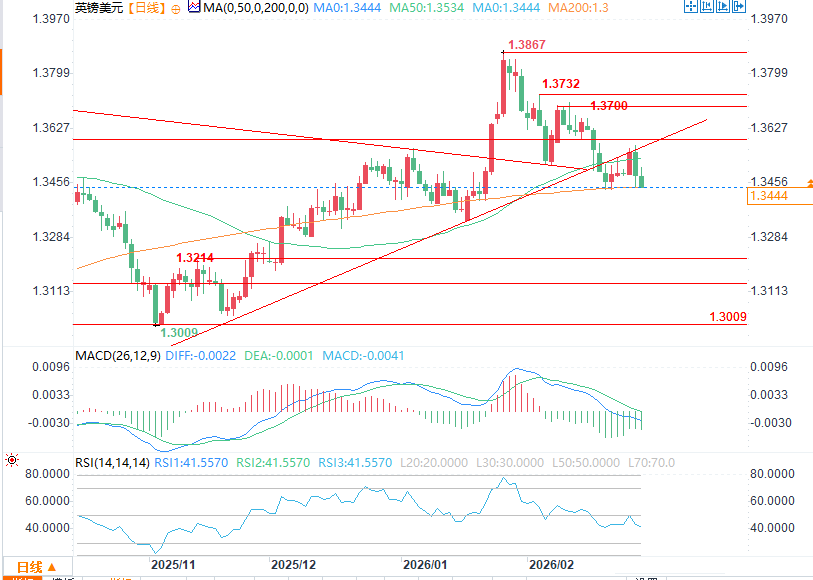

The British Labour Party suffered a devastating defeat in the elections in Gordon, Denton and Greater Manchester: the Green Party won seats for the first time in history, Reform Britain came in second, and Labour only came in third, with its vote share plummeting from 50.8% in 2024 to 25.4%.

Lee Hardman, a senior analyst at MUFG, pointed out that the Labour Party's crushing defeat will significantly increase the pressure on Prime Minister Starmer, and market concerns about the stability of British politics have fully erupted, with the pound facing the risk of continued selling pressure.

Commerzbank analyst Michael Pfister added: Even if Starmer does not resign immediately, leadership turmoil and policy uncertainty will continue to suppress the pound's valuation, and investors are beginning to demand a higher political risk premium for UK government bonds and pound assets.

ING's strategy team emphasizes that political turmoil and expectations of a Bank of England rate cut in March have created a double whammy, opening up downside potential for GBP/USD in the medium term. A break below 1.35 would target support at 1.33.

Goldman Sachs and Nomura both downgraded the pound's rating: Goldman Sachs is bearish on the pound depreciating by 6% against the euro over the next 12 months, while Nomura predicts the pound will fall another 3% by the end of April, with political risk being the core negative factor.

Escalating political risks, coupled with strong market expectations that the Bank of England will cut interest rates as early as March, are putting pressure on the pound/dollar exchange rate in the medium term, with the combined effects of political risks and expectations of monetary easing increasing.

(GBP/USD daily chart source: FX678)

It's noteworthy that gold did not blindly surge despite the weakening of major global currencies, but instead maintained a high level of fluctuation, closely monitoring the progress of US-Iran negotiations. The negotiations, originally scheduled for the near future, have been postponed to next week. The US stance has been somewhat negative, while Iran has claimed a major breakthrough, exacerbating market uncertainty due to the information gap between the two sides.

If diplomatic efforts fail, direct armed conflict is highly likely to erupt in the Middle East, triggering a massive influx of safe-haven funds into gold, potentially pushing prices above recent highs. Currently, gold prices have stabilized above $5200/ounce. The global central bank gold buying spree, expectations of a Federal Reserve interest rate cut, and geopolitical risks together form the "iron triangle" for a medium- to long-term upward trend in gold prices.

More importantly, the European Central Bank's asset allocation adjustments provided strong support for the euro: data shows that the ECB reduced its holdings of US assets from $51.9 billion to $50.9 billion, while simultaneously increasing its holdings of Japanese assets. As a result, the dollar's share of global foreign exchange reserves plummeted from 83% to 78%, a change exacerbated by exchange rate volatility and the trend of de-dollarization.

Global central banks' continued diversification of their gold and foreign exchange reserves has become a core driver of the gold price surge expected in 2024-2025. Currently, the market is highly uncertain about the prospects of Trump's policies. If regulators in various countries not only use gold but also accelerate the replacement of the US dollar with other non-US currencies, the US dollar will face medium- to long-term depreciation pressure. A recent MLIV Pulse survey shows that over 70% of investors are bearish on the US dollar, predicting a significant decline starting from the end of next month.

However, the US dollar has not easily relinquished its strong position. The Federal Reserve's extended pause in interest rate cuts has provided continued policy support for the dollar; meanwhile, yields on dollar-denominated assets remain high, while competing currencies such as the euro, pound sterling, and yen all have significant fundamental weaknesses.

Tokyo's core inflation fell to 1.8% for the first time since October 2024, significantly below the Bank of Japan's policy target of 2%. This data is a key leading indicator of national inflation in Japan, directly stripping USDJPY short sellers of significant leverage and severely weakening market expectations that the Bank of Japan will raise interest rates to normalize its policy.

The British Labour Party suffered a devastating defeat in the elections in Gordon, Denton and Greater Manchester: the Green Party won seats for the first time in history, Reform Britain came in second, and Labour only came in third, with its vote share plummeting from 50.8% in 2024 to 25.4%.

Lee Hardman, a senior analyst at MUFG, pointed out that the Labour Party's crushing defeat will significantly increase the pressure on Prime Minister Starmer, and market concerns about the stability of British politics have fully erupted, with the pound facing the risk of continued selling pressure.

Commerzbank analyst Michael Pfister added: Even if Starmer does not resign immediately, leadership turmoil and policy uncertainty will continue to suppress the pound's valuation, and investors are beginning to demand a higher political risk premium for UK government bonds and pound assets.

ING's strategy team emphasizes that political turmoil and expectations of a Bank of England rate cut in March have created a double whammy, opening up downside potential for GBP/USD in the medium term. A break below 1.35 would target support at 1.33.

Goldman Sachs and Nomura both downgraded the pound's rating: Goldman Sachs is bearish on the pound depreciating by 6% against the euro over the next 12 months, while Nomura predicts the pound will fall another 3% by the end of April, with political risk being the core negative factor.

Escalating political risks, coupled with strong market expectations that the Bank of England will cut interest rates as early as March, are putting pressure on the pound/dollar exchange rate in the medium term, with the combined effects of political risks and expectations of monetary easing increasing.

(GBP/USD daily chart source: FX678)

It's noteworthy that gold did not blindly surge despite the weakening of major global currencies, but instead maintained a high level of fluctuation, closely monitoring the progress of US-Iran negotiations. The negotiations, originally scheduled for the near future, have been postponed to next week. The US stance has been somewhat negative, while Iran has claimed a major breakthrough, exacerbating market uncertainty due to the information gap between the two sides.

If diplomatic efforts fail, direct armed conflict is highly likely to erupt in the Middle East, triggering a massive influx of safe-haven funds into gold, potentially pushing prices above recent highs. Currently, gold prices have stabilized above $5200/ounce. The global central bank gold buying spree, expectations of a Federal Reserve interest rate cut, and geopolitical risks together form the "iron triangle" for a medium- to long-term upward trend in gold prices.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.