One chart: The Baltic Dry Index jumps to a more than two-month high, with shipping prices rising across the board.

2026-03-02 23:13:37

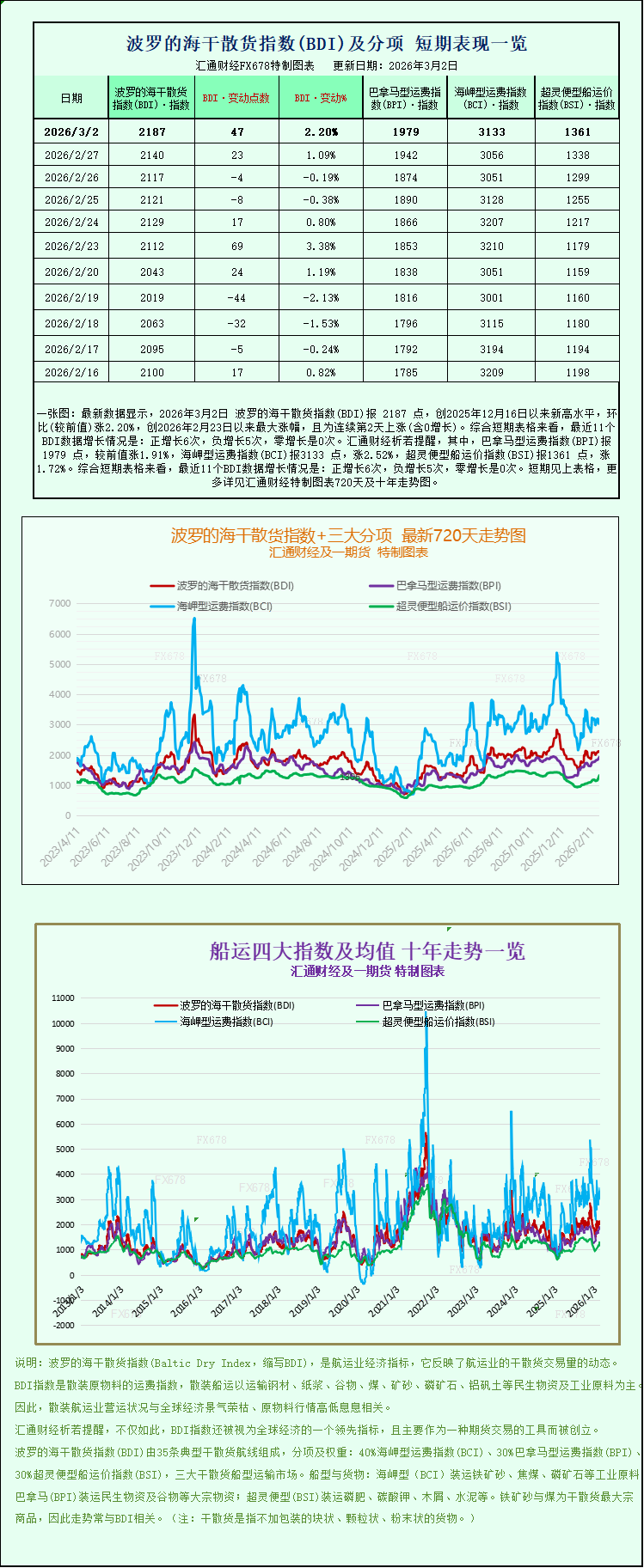

Latest data shows that the Baltic Dry Index (BDI) reached 2187 points on March 2, 2026, a new high since December 16, 2025, up 2.20% month-on-month, the largest increase since February 23, 2026, and marking the second consecutive day of increase (including zero growth). Looking at the short-term charts, the recent 11 BDI data points show: 6 positive increases, 5 negative increases, and 0 zero increases. Specifically, the Panamax Freight Index (BPI) reached 1979 points, up 1.91% from the previous value; the Capesize Freight Index (BCI) reached 3133 points, up 2.52%; and the Supramax Freight Index (BSI) reached 1361 points, up 1.72%. For detailed 720-day and 10-year trend charts of the Baltic Dry Index and its three main sub-indices, please refer to the specially designed charts.

Strongly supported by rising freight rates across all vessel types in the global dry bulk shipping market, the Baltic Dry Index (BDI) surged on Monday (March 2nd), reaching its highest level in over two months, becoming a significant signal of the recent recovery in the global shipping market. As an authoritative measure of international dry bulk shipping prices, the BDI primarily monitors global shipping prices for bulk commodities such as coal, iron ore, and grain. Its fluctuations directly reflect the level of global trade activity and the demand for bulk commodity transportation, and are considered one of the leading barometers of global economic health.

Specifically, the Baltic Dry Index, which tracks freight rates for major global dry bulk carriers, performed impressively, rising 47 points, or 2.2%, to close at 2187 points. This figure not only marked the highest level since December 16, 2025, but also signified a substantial rebound in the index's volatile adjustment since the end of last year, demonstrating the strong recovery momentum of the dry bulk shipping market.

As the "mainstay vessel type" in the dry bulk shipping market, the freight rate performance of Capesize vessels (also known as Good Hope sizes) was one of the core drivers of this index increase. Data shows that the Capesize index rose 77 points, or 2.5%, to close at 3133 points, continuing its recent upward trend. Capesize vessels, among the world's largest dry bulk carriers, have a deadweight tonnage of approximately 150,000 tons per ship and primarily undertake transoceanic transportation of core industrial raw materials such as iron ore and coking coal, serving as a crucial support for the global steel industry supply chain. Correspondingly, the average daily revenue of 150,000-ton Capesize vessels transporting iron ore and coal increased by $699 on the day, ultimately reaching $24,910, resulting in a steady improvement in shipowner profitability.

It is worth noting that the trend of iron ore prices is linked to dry bulk freight rates, further boosting the rise in Capesize vessel freight rates. On that day, iron ore futures prices reversed a slight decline in the morning session, continuing to rise in the afternoon and ultimately closing higher. Market analysts pointed out that the rebound in iron ore prices was mainly due to two factors: first, investors focused on expectations of increased freight rates due to geopolitical conflicts in the Middle East; and second, shipments from major global iron ore suppliers experienced a temporary decline, and the subtle changes in the supply-demand balance drove up ore prices, thereby increasing demand for iron ore transportation and indirectly supporting the rise in Capesize vessel freight rates. According to the Tonghuashun financial database, on March 2, the closing price of the Dalian Commodity Exchange's main iron ore futures contract (IZL2) was 754.5 yuan/ton, up 6.5 yuan from the previous day's settlement price, a rise of 0.87%, confirming this trend.

The core background to this surge in dry bulk freight rates is the continued escalation of geopolitical tensions in the Middle East. According to trade sources on Saturday (February 28), the Iranian Islamic Revolutionary Guard Corps officially announced the closure of the Strait of Hormuz due to the military attacks launched by the United States and Israel against Iran. This move has directly led to drastic changes in the global energy transportation landscape. The Strait of Hormuz, the only sea passage connecting the Persian Gulf and the Gulf of Oman, is known as the "world's oil valve," handling approximately 20% of global oil transportation and 20% of liquefied natural gas (LNG) exports. It carries about 20 million barrels of crude oil daily and is a lifeline for oil-producing countries in the Middle East, such as Saudi Arabia and the UAE. Following the closure, many international tanker owners, large oil companies, and trading companies have urgently suspended the transport of crude oil, fuel oil, and LNG through the strait. A large number of ships have stopped sailing in the surrounding waters to avoid danger, and risk aversion in the shipping market continues to rise.

The impact of geopolitical conflicts on the global economy and shipping industry has also drawn attention from institutions. Analysts at Barclays Bank stated in a recent research report: "The ongoing conflict in Iran and the resulting rise in international oil prices may exert inflationary pressure and negatively impact global GDP growth, dragging down the pace of global economic recovery. However, for shipping companies, their profitability is far more sensitive to changes in freight rates than to changes in global economic demand. Therefore, against the backdrop of continuously rising freight rates, shipping companies are expected to effectively hedge against the potential risks brought about by geopolitical conflicts and achieve stable profit growth."

Besides Capesize vessels, freight rates for medium-sized dry bulk carriers also rose in tandem, further confirming the comprehensive recovery of the dry bulk shipping market. The Panamax index rose 37 points, or 1.9%, to close at 1979 points. Panamax vessels are the backbone of global dry bulk shipping, typically with a deadweight tonnage between 60,000 and 75,000 tons. Named for their ability to pass through the Panama Canal when fully loaded, they primarily handle the transoceanic transport of essential goods and bulk commodities such as coal and grain. Their freight rate fluctuations directly reflect global demand for agricultural and energy supplies. Correspondingly, the average daily revenue of Panamax vessels rose by $333 to $17,814, continuing the recent upward trend and highlighting the steady recovery in global demand for bulk commodity transportation.

In the small and medium-sized dry bulk carrier segment, Supramax vessels also performed strongly, becoming an important supplementary force driving market growth. Data shows that the Supramax vessel index rose 23 points, or 1.7%, to close at 1361 points. Supramax vessels have a deadweight tonnage of approximately 48,000 to 60,000 tons, are highly adaptable to ports and canals, and are often equipped with loading and unloading equipment, allowing for flexible operation. They primarily transport goods such as grain, cement, and steel pipes. The rise in their freight rates reflects a gradual recovery in demand in the global small and medium-sized dry bulk shipping market.

Industry analysts point out that the recent surge in the Baltic Dry Index is a result of a convergence of geopolitical factors, changes in commodity supply and demand, and the shipping market's own cyclical patterns. The closure of the Strait of Hormuz, leading to route adjustments and rising insurance costs, has further increased dry bulk shipping costs, while the steady recovery in global commodity demand provides fundamental support for the freight rate increase. However, some institutions caution that further escalation of geopolitical conflicts in the Middle East or a weaker-than-expected global economic recovery could introduce uncertainty into the future trajectory of the dry bulk shipping market.

Strongly supported by rising freight rates across all vessel types in the global dry bulk shipping market, the Baltic Dry Index (BDI) surged on Monday (March 2nd), reaching its highest level in over two months, becoming a significant signal of the recent recovery in the global shipping market. As an authoritative measure of international dry bulk shipping prices, the BDI primarily monitors global shipping prices for bulk commodities such as coal, iron ore, and grain. Its fluctuations directly reflect the level of global trade activity and the demand for bulk commodity transportation, and are considered one of the leading barometers of global economic health.

Specifically, the Baltic Dry Index, which tracks freight rates for major global dry bulk carriers, performed impressively, rising 47 points, or 2.2%, to close at 2187 points. This figure not only marked the highest level since December 16, 2025, but also signified a substantial rebound in the index's volatile adjustment since the end of last year, demonstrating the strong recovery momentum of the dry bulk shipping market.

As the "mainstay vessel type" in the dry bulk shipping market, the freight rate performance of Capesize vessels (also known as Good Hope sizes) was one of the core drivers of this index increase. Data shows that the Capesize index rose 77 points, or 2.5%, to close at 3133 points, continuing its recent upward trend. Capesize vessels, among the world's largest dry bulk carriers, have a deadweight tonnage of approximately 150,000 tons per ship and primarily undertake transoceanic transportation of core industrial raw materials such as iron ore and coking coal, serving as a crucial support for the global steel industry supply chain. Correspondingly, the average daily revenue of 150,000-ton Capesize vessels transporting iron ore and coal increased by $699 on the day, ultimately reaching $24,910, resulting in a steady improvement in shipowner profitability.

It is worth noting that the trend of iron ore prices is linked to dry bulk freight rates, further boosting the rise in Capesize vessel freight rates. On that day, iron ore futures prices reversed a slight decline in the morning session, continuing to rise in the afternoon and ultimately closing higher. Market analysts pointed out that the rebound in iron ore prices was mainly due to two factors: first, investors focused on expectations of increased freight rates due to geopolitical conflicts in the Middle East; and second, shipments from major global iron ore suppliers experienced a temporary decline, and the subtle changes in the supply-demand balance drove up ore prices, thereby increasing demand for iron ore transportation and indirectly supporting the rise in Capesize vessel freight rates. According to the Tonghuashun financial database, on March 2, the closing price of the Dalian Commodity Exchange's main iron ore futures contract (IZL2) was 754.5 yuan/ton, up 6.5 yuan from the previous day's settlement price, a rise of 0.87%, confirming this trend.

The core background to this surge in dry bulk freight rates is the continued escalation of geopolitical tensions in the Middle East. According to trade sources on Saturday (February 28), the Iranian Islamic Revolutionary Guard Corps officially announced the closure of the Strait of Hormuz due to the military attacks launched by the United States and Israel against Iran. This move has directly led to drastic changes in the global energy transportation landscape. The Strait of Hormuz, the only sea passage connecting the Persian Gulf and the Gulf of Oman, is known as the "world's oil valve," handling approximately 20% of global oil transportation and 20% of liquefied natural gas (LNG) exports. It carries about 20 million barrels of crude oil daily and is a lifeline for oil-producing countries in the Middle East, such as Saudi Arabia and the UAE. Following the closure, many international tanker owners, large oil companies, and trading companies have urgently suspended the transport of crude oil, fuel oil, and LNG through the strait. A large number of ships have stopped sailing in the surrounding waters to avoid danger, and risk aversion in the shipping market continues to rise.

The impact of geopolitical conflicts on the global economy and shipping industry has also drawn attention from institutions. Analysts at Barclays Bank stated in a recent research report: "The ongoing conflict in Iran and the resulting rise in international oil prices may exert inflationary pressure and negatively impact global GDP growth, dragging down the pace of global economic recovery. However, for shipping companies, their profitability is far more sensitive to changes in freight rates than to changes in global economic demand. Therefore, against the backdrop of continuously rising freight rates, shipping companies are expected to effectively hedge against the potential risks brought about by geopolitical conflicts and achieve stable profit growth."

Besides Capesize vessels, freight rates for medium-sized dry bulk carriers also rose in tandem, further confirming the comprehensive recovery of the dry bulk shipping market. The Panamax index rose 37 points, or 1.9%, to close at 1979 points. Panamax vessels are the backbone of global dry bulk shipping, typically with a deadweight tonnage between 60,000 and 75,000 tons. Named for their ability to pass through the Panama Canal when fully loaded, they primarily handle the transoceanic transport of essential goods and bulk commodities such as coal and grain. Their freight rate fluctuations directly reflect global demand for agricultural and energy supplies. Correspondingly, the average daily revenue of Panamax vessels rose by $333 to $17,814, continuing the recent upward trend and highlighting the steady recovery in global demand for bulk commodity transportation.

In the small and medium-sized dry bulk carrier segment, Supramax vessels also performed strongly, becoming an important supplementary force driving market growth. Data shows that the Supramax vessel index rose 23 points, or 1.7%, to close at 1361 points. Supramax vessels have a deadweight tonnage of approximately 48,000 to 60,000 tons, are highly adaptable to ports and canals, and are often equipped with loading and unloading equipment, allowing for flexible operation. They primarily transport goods such as grain, cement, and steel pipes. The rise in their freight rates reflects a gradual recovery in demand in the global small and medium-sized dry bulk shipping market.

Industry analysts point out that the recent surge in the Baltic Dry Index is a result of a convergence of geopolitical factors, changes in commodity supply and demand, and the shipping market's own cyclical patterns. The closure of the Strait of Hormuz, leading to route adjustments and rising insurance costs, has further increased dry bulk shipping costs, while the steady recovery in global commodity demand provides fundamental support for the freight rate increase. However, some institutions caution that further escalation of geopolitical conflicts in the Middle East or a weaker-than-expected global economic recovery could introduce uncertainty into the future trajectory of the dry bulk shipping market.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.